NVIDIA beat expectations again in FY27Q1 and issued another above-consensus outlook for FY27Q2, continuing to push the revenue and profit ceiling for the global semiconductor industry.

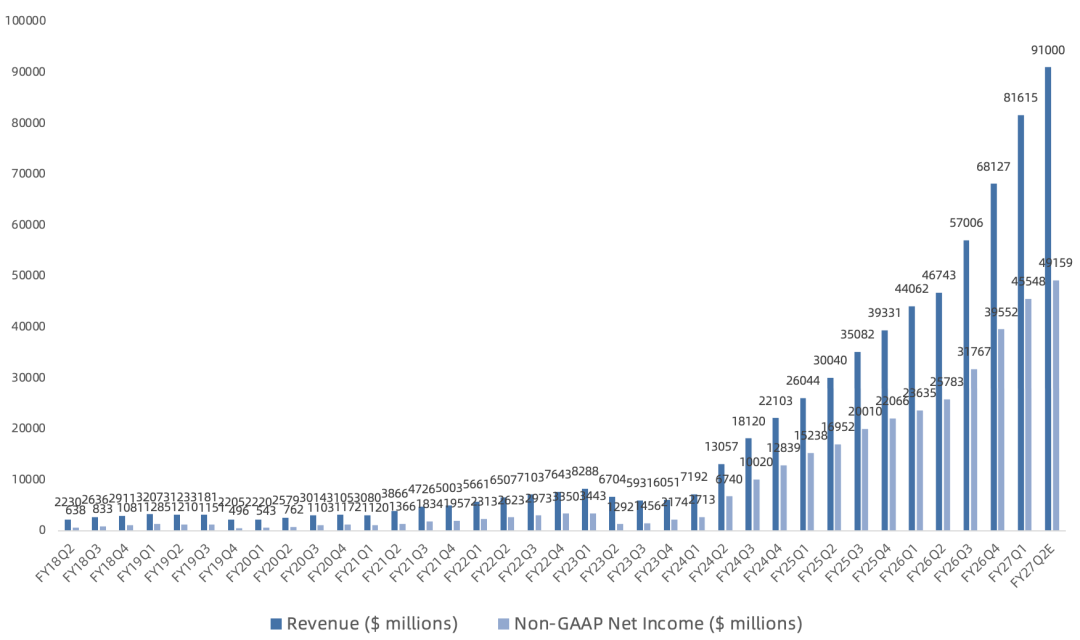

Revenue reached $81.6B, up 85% year over year and 20% sequentially, above the $78.7B consensus estimate and the prior $78B guidance.

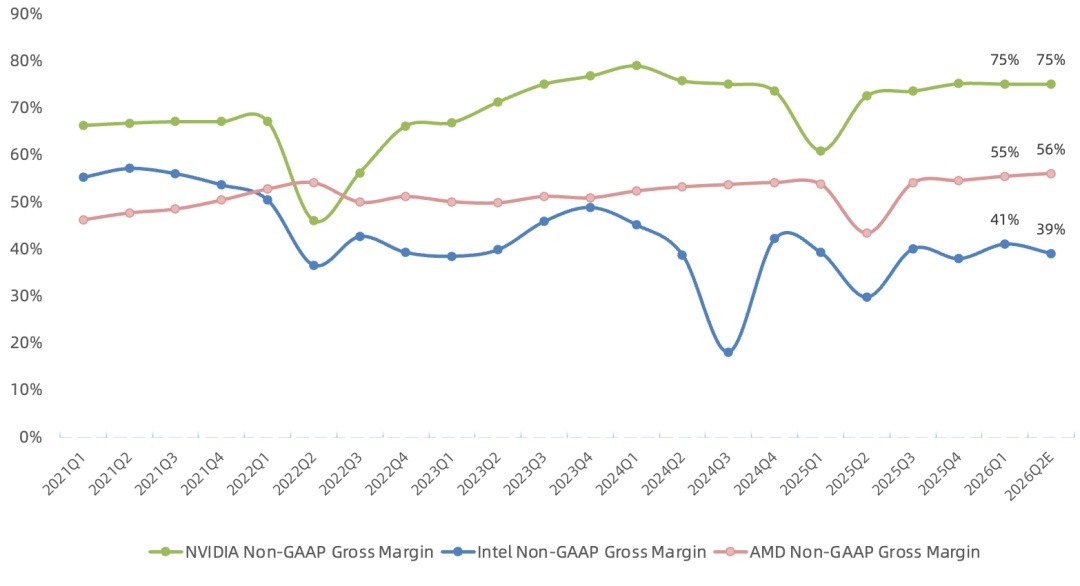

GAAP gross margin was 74.9%, up 14.2 percentage points year over year and down 0.1 points sequentially, exactly matching guidance.

Non-GAAP gross margin was 75%, up 1.7 percentage points year over year and down 0.1 points sequentially, also matching guidance.

GAAP net income reached $58.3B, up 211% year over year and 36% sequentially. Other income, primarily investment gains, contributed $15.9B.

Non-GAAP net income reached $45.5B, up 139% year over year and 17% sequentially, above the $43.1B consensus estimate.

NVIDIA finally changed its segment disclosure this quarter, reporting Data Center and Edge Computing rather than separately disclosing the much smaller Gaming, Professional Visualization, and Automotive businesses.

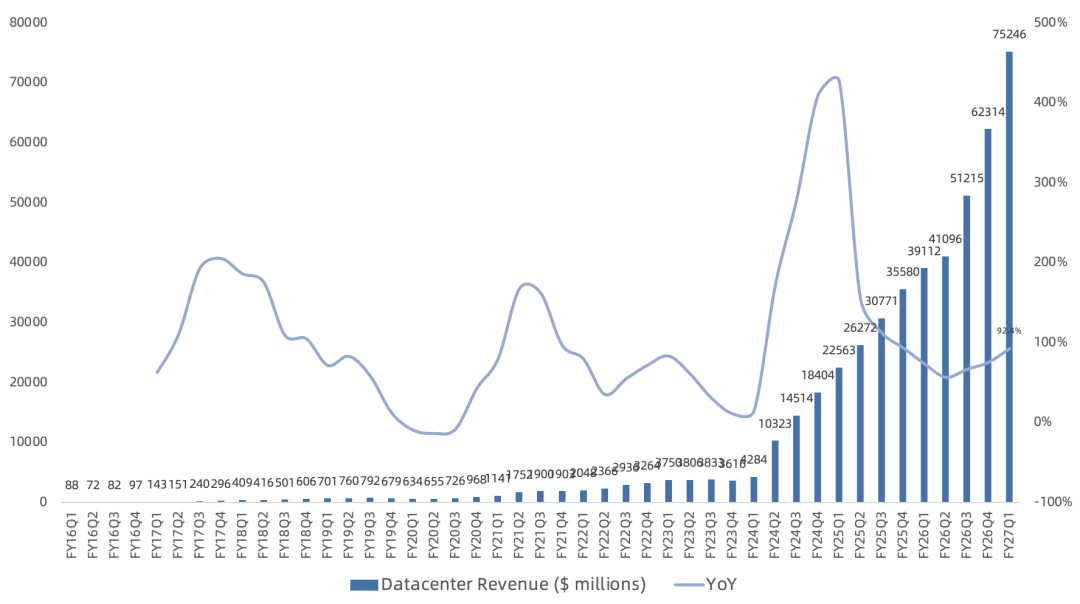

Data Center Q1 revenue reached $62.3B, up 92% year over year and 21% sequentially, representing 93% of NVIDIA's total revenue and driven primarily by the Blackwell Ultra ramp. Edge Computing revenue reached $6.4B, up 29% year over year and 10% sequentially, led by demand for Blackwell workstations. Consumer demand declined slightly because of higher memory and system prices, while Physical AI continued to gain momentum and generated more than $9B over the past 12 months.

Legacy Data Center Disclosure:

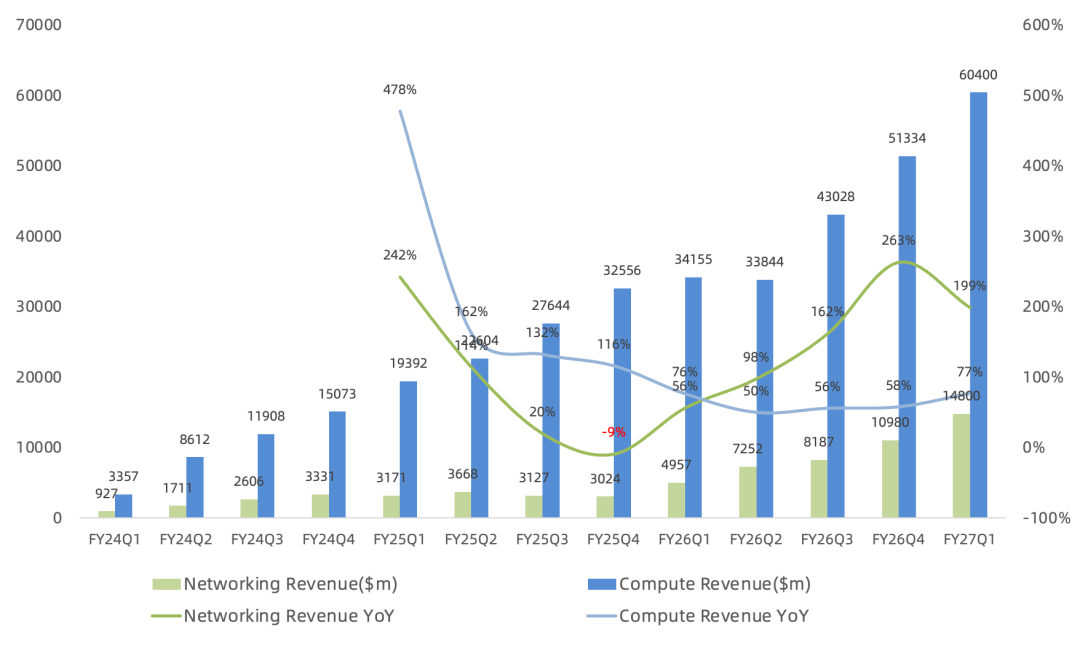

Compute revenue reached $60.4B, up 77% year over year. Demand for GB300 and NVL72 was particularly strong, with frontier-model developers and hyperscalers each deploying hundreds to thousands of Blackwell GPUs. This is the fastest product ramp in NVIDIA's history.

Networking revenue reached $15B, nearly quadrupling year over year. Spectrum-X, NVIDIA's end-to-end Ethernet platform built specifically for AI, is now larger than all competing Ethernet networking businesses combined. InfiniBand also delivered strong growth of more than five times year over year, driven by next-generation XDR deployments.

New Data Center Disclosure:

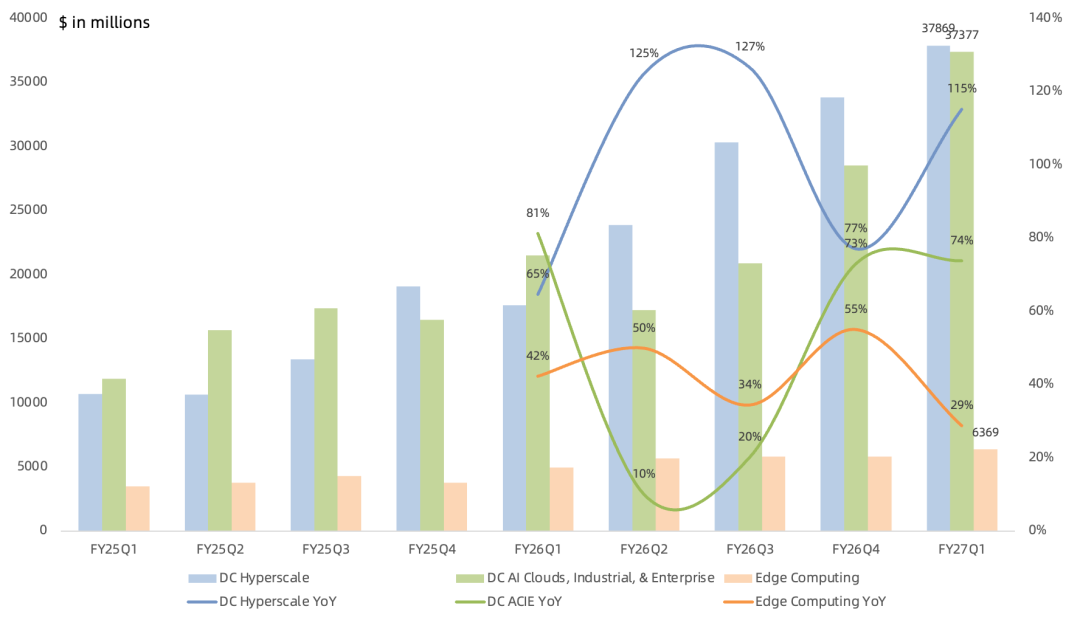

Hyperscale Data Center revenue reached $37.9B, up 115% year over year and representing 50% of Data Center revenue. This category includes public cloud providers and the world's largest consumer internet company, Meta.

AI Clouds, Industrial, and Enterprise, or ACIE, generated $37.4B, up 74% year over year and representing the other 50% of Data Center revenue. ACIE covers diversified AI-focused data centers and AI factories across industries and countries, including neoclouds. AI Cloud revenue more than quadrupled year over year, while sovereign AI revenue grew more than 80%. NVIDIA infrastructure is now deployed in nearly 40 countries, and the number of partner data centers above 10 MW has almost doubled in one year to more than 80 sites. NVIDIA's share of AI inference is expanding rapidly.

FY27Q2 revenue guidance is $91B, excluding China Data Center revenue, implying 95% year-over-year and 11% sequential growth and exceeding consensus. GAAP gross margin is guided to 74.9% and non-GAAP gross margin to 75%, with the full-year level expected to remain near 75%. Non-GAAP net income guidance of $49.2B implies 91% year-over-year and 8% sequential growth, continuing to lead global peers.

Views on AI's sustainability still differ, and criticism of NVIDIA has never disappeared. I maintain that future growth will come mainly from two shifts: Data Center demand expanding beyond cloud computing into vertical industries and sovereign AI, a trend accelerated by DeepSeek's democratization of AI, and a broader chip portfolio supported by annual rather than biennial product cycles. The global AI factory buildout remains in its early stages, with demand spanning cloud providers, sovereign nations, frontier-model companies, enterprises, and supercomputing centers.

On China, I still hold the prior view that AI decoupling is inevitable given U.S.-China relations and that a clean break is preferable to prolonged uncertainty. Jensen Huang remains reluctant to abandon a $50B market, but at least the issue is no longer driving near-term sentiment. The U.S. government approved H200 shipments to China in February, but China has not yet granted approval and NVIDIA has recognized no H200 revenue from the market.

Total supply-related commitments reached $119B, up 25% sequentially. NVIDIA has secured wafer and CoWoS packaging capacity, including from TSMC, as well as HBM, DRAM, and NAND supply from Samsung, SK Hynix, and Micron.

FY27Q1 Earnings Call Highlights:

At GTC, NVIDIA guided to more than $1T of Blackwell and Rubin Data Center compute revenue from the beginning of 2025 through the end of 2027. That framework excludes the newly disclosed CPU opportunity and future LPX revenue.

Vera Rubin remains on schedule to begin volume shipments in Q3 and ramp in Q4. Early demand is exceptionally strong, and management expects Vera Rubin to be more successful than Grace Blackwell.

Vera CPU has three deployment models. First, NVIDIA expects to sell millions of Rubin GPUs with one Vera CPU paired to every two Rubins. Second, Vera will be sold as a standalone CPU. Third, Vera can be paired with CX9 and dedicated software stacks for storage, security, compute isolation, and confidential computing. Vera opens a new $200B TAM that NVIDIA has never addressed before, and every major hyperscaler and system manufacturer is working on deployments. Standalone CPU revenue, excluding CPUs inside GPU racks, is expected to approach $20B this year, already larger than Intel's or AMD's comparable scale and positioning NVIDIA as a leading global CPU supplier.

Management expects NVIDIA to grow faster than hyperscaler capex. Anthropic, OpenAI, Gemini, SpaceX AI, Meta, MSL, Microsoft AI, TML, Inflection AI, Perplexity, Cursor, and other major frontier laboratories are all building on NVIDIA's platform. NVIDIA therefore expects its share of frontier AI models to increase materially, a view that differs sharply from current market expectations.

NVIDIA repurchased $19.3B of stock in Q1, versus zero at Google, and paid $243M in dividends. The board added $80B to the repurchase authorization, leaving $118.5B available. Beginning in Q2, the quarterly dividend rises 25-fold from $0.01 to $0.25 per share, implying more than $24B of annual dividends.

By customer headquarters, the United States contributed 78% of fiscal-quarter revenue, Taiwan 15%, and mainland China 6%. The three largest customers represented 21%, 17%, and 16% of revenue, respectively.

H100 rental prices have risen 20% year to date, while cloud pricing for A100 has increased nearly 15%. The versatility of NVIDIA's platform and continuing software-driven performance gains allow customers to generate profitable revenue beyond the GPUs' depreciable lives. Ongoing CUDA optimization and full-stack innovation have improved GB300 throughput by 2.7 times versus six months ago while reducing token cost by 60%.

Management expects LPX and other SRAM-based AI chips focused on decode and high-token-rate generation to remain niche products for some time. Service providers that already offer high-token-rate workloads can add LPX to improve delivery. Whether the category ultimately represents 10% or 20% of the market will depend on how AI workloads evolve.

There are three sources of upside beyond the $1T revenue framework. First, NVIDIA expects to gain share in frontier AI models. Second, the framework includes no Vera CPU or standalone CPU revenue, which management sees as the next-largest opportunity. Third, LPX adds another growth vector. Together, Vera Rubin and LPX allow NVIDIA to cover the full AI spectrum from pretraining and post-training to inference and agentic AI.

Overall, NVIDIA's results provide a strong rebuttal to the AI bubble argument and address investor concerns about older-GPU depreciation and declining gross margin, reinforcing the U.S. AI investment narrative. Current guidance implies full-year non-GAAP net income of $114.2B, with net income potentially exceeding $200B next year.

GPT-5.5 ultimately demonstrated the strength of a major AI model trained on Blackwell, increasing expectations for models trained on Vera Rubin. NVIDIA has repeatedly challenged the AI bubble narrative and addressed concerns about older-card depreciation and gross margin, sustaining the AI semiconductor thesis, yet the market has still reacted negatively to four consecutive earnings reports.

Even a path toward at least $200B of FY27 net income has not overcome the market's enthusiasm for in-house AI chips. A $20B Vera CPU revenue outlook has likewise failed to draw attention away from the Intel, AMD, and Arm CPU narrative. Record buybacks and dividends have been dismissed with the label of 'the next Apple.'

The biggest positive surprise for me was NVIDIA's willingness to disclose the Hyperscale metric. It signals management's confidence in the long-term growth of the business investors fear is most exposed to in-house AI chips, carrying the same kind of strategic significance as the earlier 10-for-1 stock split announcement.