Amid a market awash with contradictory "AI bubble" and "AI eating software" narratives, the picks-and-shovels leader, global AI chip titan NVIDIA, delivered a world-watched FY26 Q4 report. NVIDIA's FY26 Q4 (November/December 2025 through January 2026) again beat expectations, and its FY27 Q1 guidance once again stunned Wall Street. As the highest-revenue, highest-net-income company in global semiconductor history, NVIDIA continues to shatter industry ceilings; this quarter, net income claimed the global number-one spot.

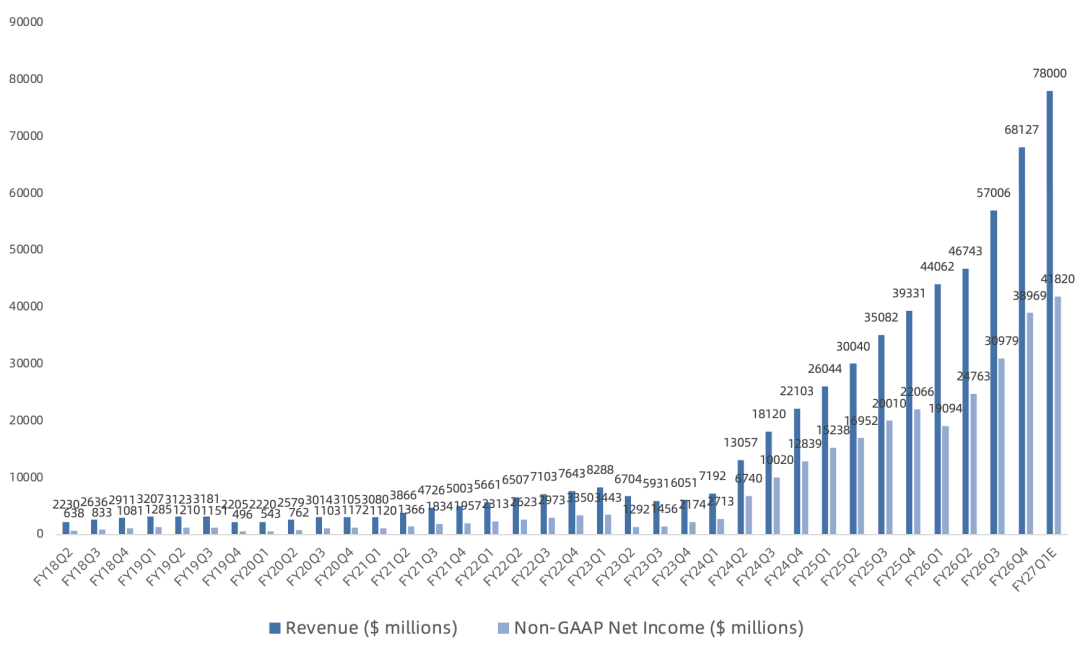

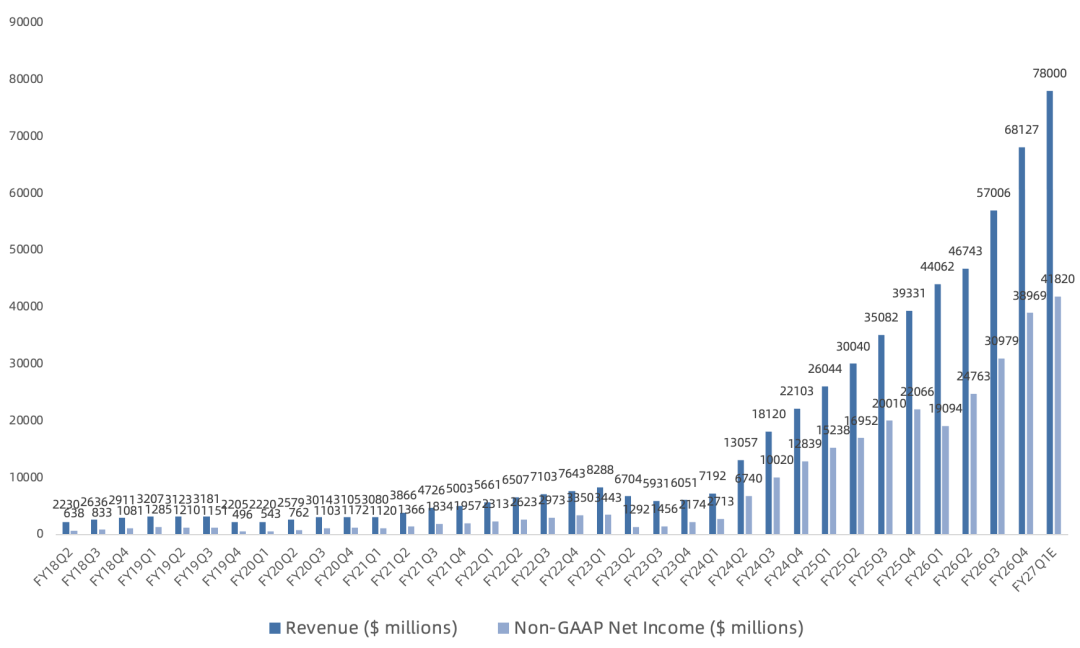

Revenue was $68.1B, up 73% year over year and 20% sequentially, significantly above the consensus estimate of $65.9B; prior guidance was $65B.

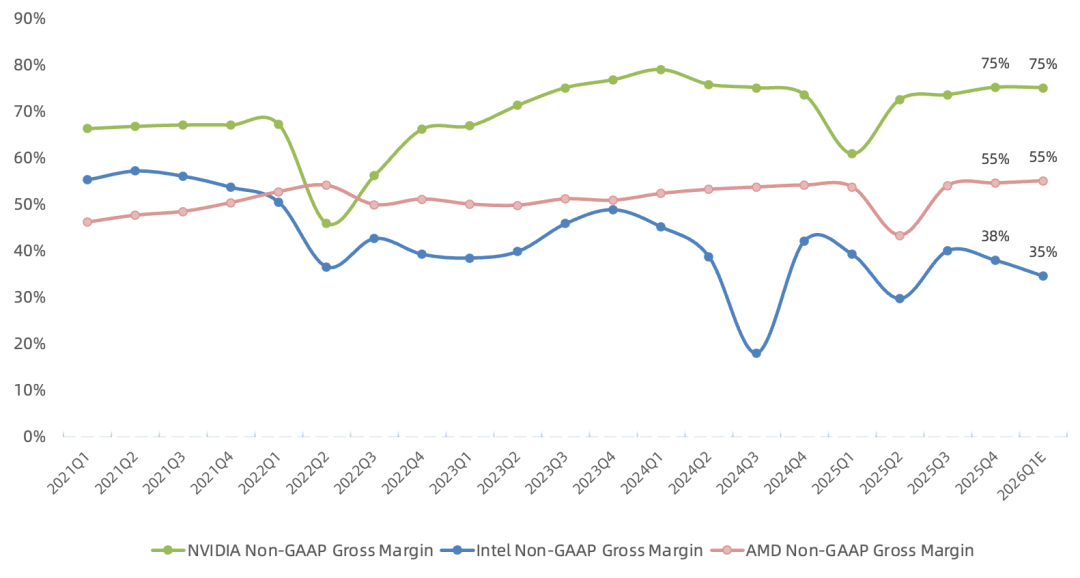

GAAP gross margin was 75%, up 2 percentage points year over year and 1.6 percentage points sequentially, slightly above the consensus estimate of 74.9%; prior guidance was 74.8%.

Non-GAAP gross margin was 75.2%, up 1.7 percentage points year over year and 1.6 percentage points sequentially, slightly above the consensus estimate of 75%; prior guidance was also 75%.

GAAP net income was $42.96B, up 94% year over year and 35% sequentially, significantly above the consensus estimate of $36.3B; prior guidance was $35.2B.

Non-GAAP net income was $38.97B, up 77% year over year and 26% sequentially, above the consensus estimate of $37.5B; prior guidance was $36.7B.

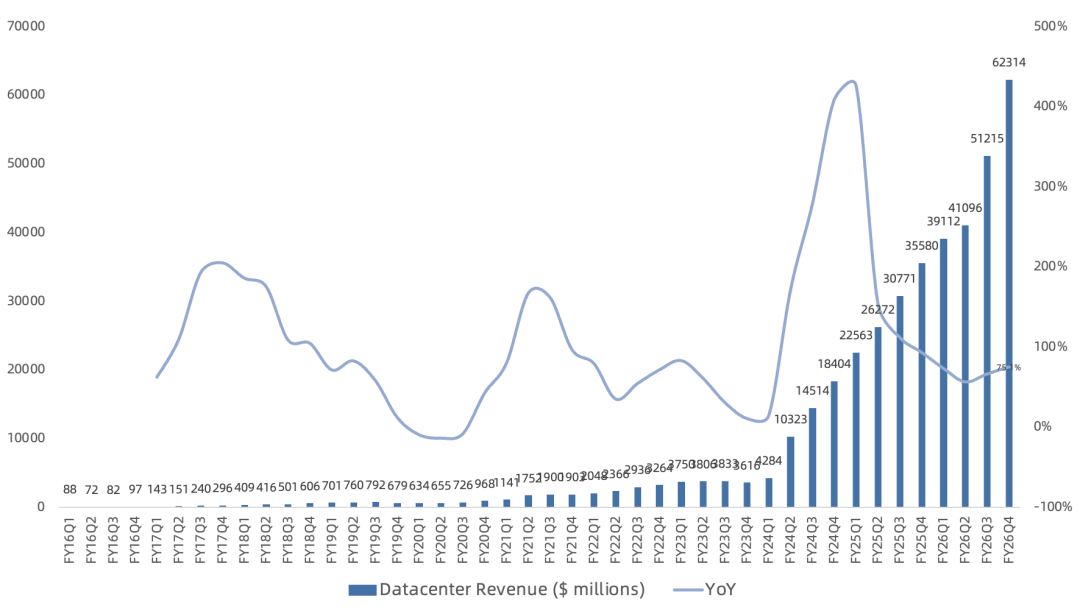

Data center Q4 revenue was $62.3B, up 75% year over year and 22% sequentially, representing 92% of total NVIDIA revenue, driven primarily by Blackwell ramp and Blackwell Ultra ramp. Management noted that since ChatGPT's emergence, data center revenue has grown nearly 13x.

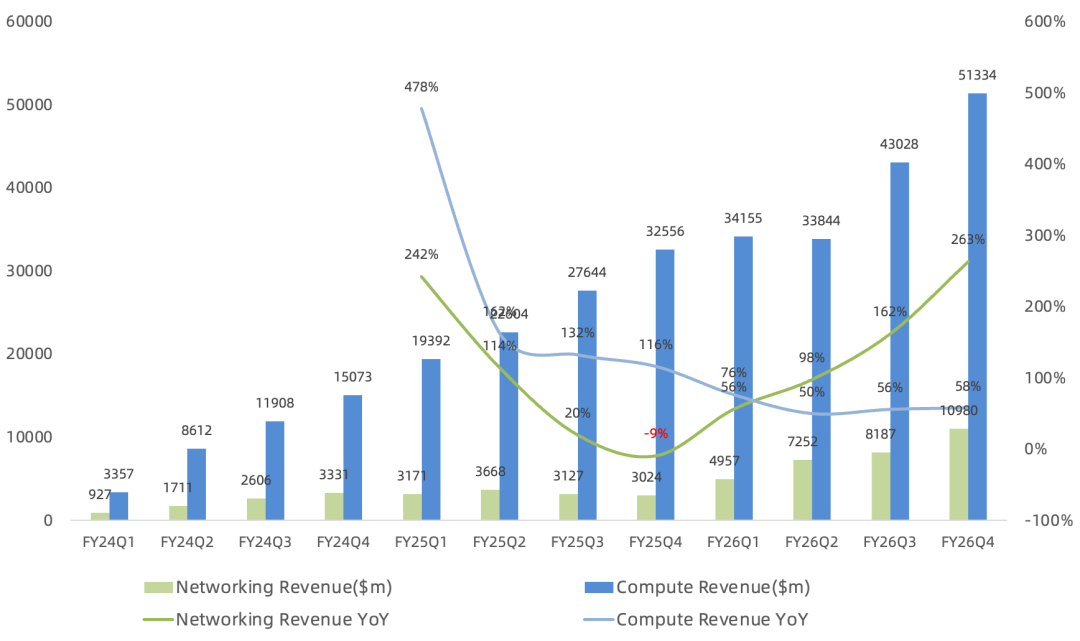

Inside Data Center:

Compute revenue was $51.3B, up 58% year over year and 19% sequentially. Grace Blackwell racks (GB200/GB300) accounted for approximately 2/3 of data center revenue this quarter.

Networking revenue was $11.0B, up 263% year over year and 34% sequentially, breaking the $10B quarterly threshold for the first time; networking business is now global number one in scale. Both scale-up and scale-out technology demand hit records, with both growing double-digits sequentially, driven by strong adoption of NVLink, Spectrum-X Ethernet, and InfiniBand. NVLink significantly propelled networking growth: each rack has 9 switch nodes, each with 2 NVLink chips, and this will increase further; the switching volume per rack is staggering. NVLink opens another growth curve: this quarter NVIDIA announced NVLink Fusion (ALAB) for AWS to enable integration with its custom chips. Since acquiring Mellanox, networking revenue has grown over 10x.

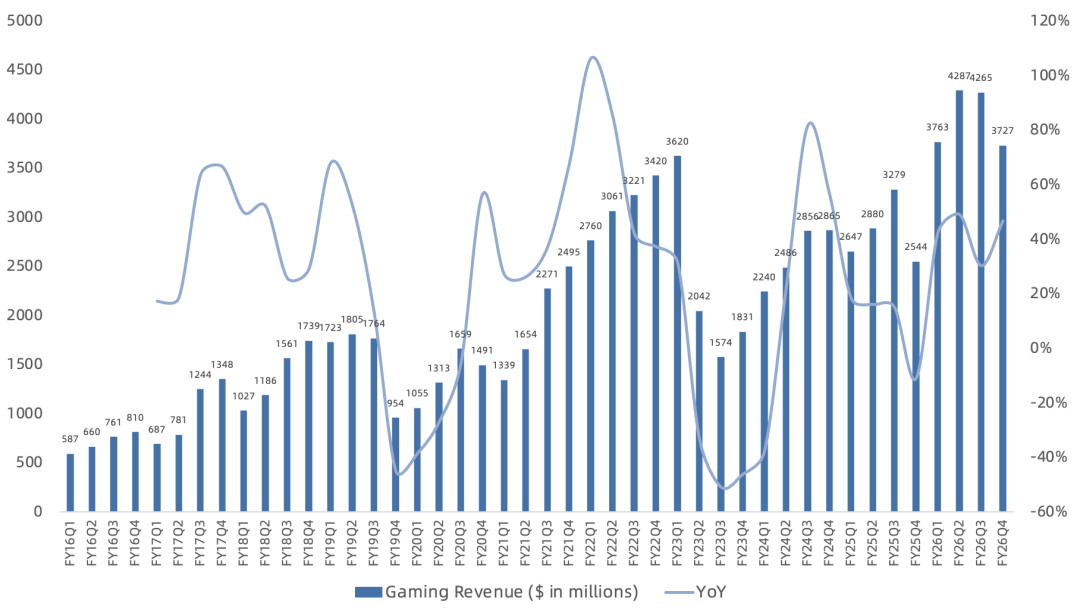

Gaming Q4 revenue was $3.7B, up 47% year over year and down 13% sequentially, representing 6% of total NVIDIA revenue, driven by strong Blackwell demand and improved supply. Looking ahead, despite strong end demand and healthy channel inventory, supply constraints are expected to be a headwind for gaming in Q1 and beyond. If supply improves by year-end, year-over-year growth could return.

Per guidance, FY27 Q1 revenue is $78B (excluding mainland China data center revenue), up 77% year over year, far above the consensus estimate of $72.8B, primarily benefiting from Blackwell Ultra platform ramp. Q1 GAAP gross margin guided at 74.9%, non-GAAP at 75%, with full year expected to hold at the 75% level. GAAP operating income guided at $50.7B, up 134% year over year; non-GAAP operating income guided at $51.0B, up 136% year over year, continuing to lead globally.

Views on AI's sustainability still differ, and criticism of NVIDIA has never disappeared. I maintain that future growth will come mainly from two shifts: Data Center demand expanding beyond cloud computing into vertical industries and sovereign AI, a trend accelerated by DeepSeek's democratization of AI, and a broader chip portfolio supported by annual rather than biennial product cycles. The global AI factory buildout remains in its early stages, with demand spanning cloud providers, sovereign nations, frontier-model companies, enterprises, and supercomputing centers.

On China, I still hold the prior view that AI decoupling is inevitable given U.S.-China relations and that a clean break is preferable to prolonged uncertainty. Jensen Huang remains reluctant to abandon a $50B market, but at least the issue is no longer driving near-term sentiment. The U.S. government approved H200 shipments to China in February, but China has not yet granted approval and NVIDIA has recognized no H200 revenue from the market.

FY26 Q4 Call Highlights:

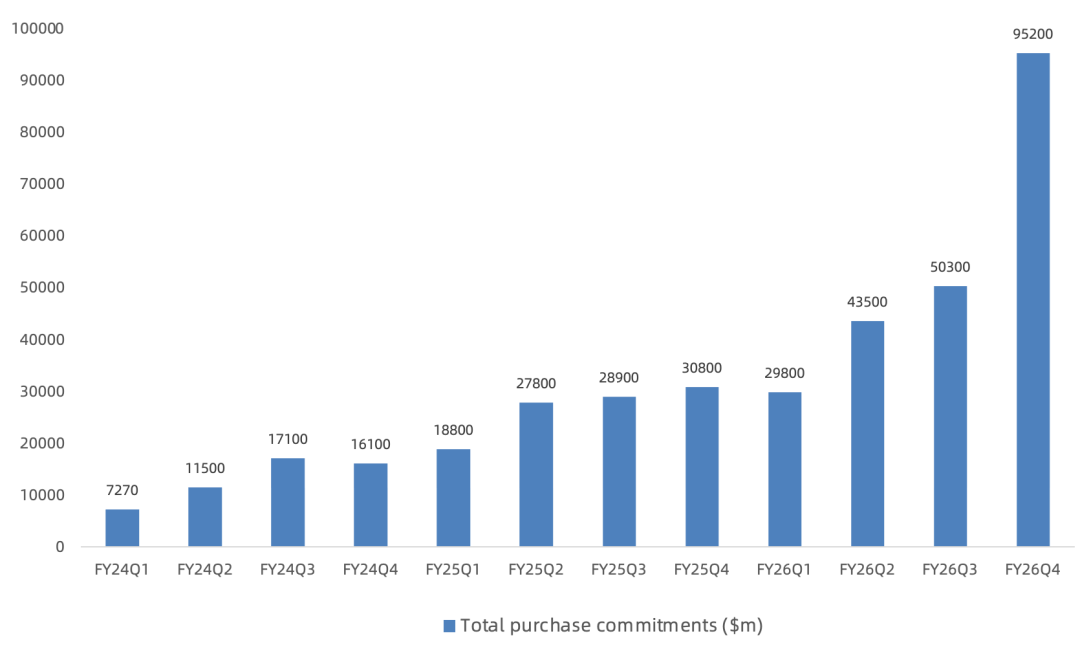

Total supply-related commitments reached $95.2B this quarter, up 89% sequentially, pre-booking wafer and CoWoS packaging capacity at TSMC, and HBM, DRAM, and NAND capacity at Samsung, SK hynix, and Micron.

FY27 data center is expected to grow sequentially each quarter. Current order visibility already exceeds the prior $500B revenue guide.

Starting next quarter, the company will no longer exclude stock-based compensation from non-GAAP (SBC as a percentage of revenue far exceeds other semiconductor companies, and as a percentage of operating expense is also significant). This proactive tightening of the non-GAAP definition reflects management's confidence in continued profit growth.

Management stated that as long as each generation delivers far-better-than-Moore's-Law performance-per-watt gains and far-better-than-system-cost-inflation performance-per-dollar gains, gross margin can be sustained.

Sovereign AI revenue exceeded $30B this fiscal year, up 2x year over year. Long term, sovereign AI opportunity is expected to grow at least in line with the AI infrastructure market, with countries investing in AI proportionally to GDP.

CUDA software continues to optimize, delivering up to 5x performance gains on GB200 and NVL72 in just 4 months. The plan is to achieve X-fold performance-per-watt leaps each generation and sustainably widen the lead long term.

Q4 repurchases were $3.8B, dividends $243M. Buyback authorization remaining: $58.5B. Future balance between buybacks and ecosystem investment.

By headquarters geography this fiscal year: US 69%, Taiwan 20% (76% of downstream customers are US), mainland China 9%. Top customer 22%, second customer 14%, concentration declining; customer base increasingly diversified. CSPs slightly exceeded 50% of data center revenue this quarter; the remainder is internet and vertical industries.

Earlier this week, first Vera Rubin samples were shipped to customers, still on track for volume production in H2 this year. CUDA GPU's long useful life is a significant TCO advantage versus other AI chips. CUDA compatibility and massive installed base extend NVIDIA AI chip lifetimes far beyond initial estimates; even Hopper and many Ampere-architecture products from 6 years ago remain sold out in the cloud.

Grace Blackwell NVL72 systems have been shipping for nearly a year. Blackwell-related infrastructure deployed and consumed by major cloud providers, hyperscalers, AI model developers, and enterprise customers has reached 9 GW in scale.

GPT-5.3 Codex training and inference run on Grace Blackwell and NVL72 systems. Anthropic will train and infer on Grace Blackwell and Vera Rubin systems. Claude Cowork and OpenClaw are driving compute demand surge; Agentic AI's "ChatGPT moment" has arrived.

Signed a non-exclusive licensing agreement with Groq to use its low-latency inference technology; more details to be shared at March GTC.

Jensen stated that anyone should extend the single-chip/fewer-dielet path as far as possible, because crossing each dielet means crossing an interface, and each interface adds unnecessary latency and power. Not opposed to dielets, and they are used, but only when there is no alternative. Grace Blackwell and Rubin use two large die near the reticle limit, then bonded, reducing cross-boundary overhead. Competitors' "dielet tax" will show up in architectural efficiency.

Overall, NVIDIA's results provide a strong rebuttal to the AI bubble argument and address investor concerns about older-GPU depreciation and declining gross margin, reinforcing the U.S. AI investment narrative. Current guidance implies full-year non-GAAP net income of $114.2B, with net income potentially exceeding $200B next year.

Overall, NVIDIA's report again refutes the AI bubble narrative and addresses market concerns about legacy GPU depreciation and margin compression, continuing to underpin the US AI semiconductor thesis, even as the company itself becomes a target from all sides. FY26 full-year actual non-GAAP net income was $113.8B, consistent with our prior estimate. Based on current guidance, FY27 full-year net income is expected to start at $200B.

"Legacy software was pre-recorded: content and logic were pre-written, compiled, and recorded. Now everything is generated in real time. Real-time generation means the user, scenario, question, and intent can all be incorporated into the context to generate the result. Real-time generation requires far more compute than pre-recorded, just as a computer needs far more compute than a DVD player. AI needs far more compute than legacy software." — Jensen