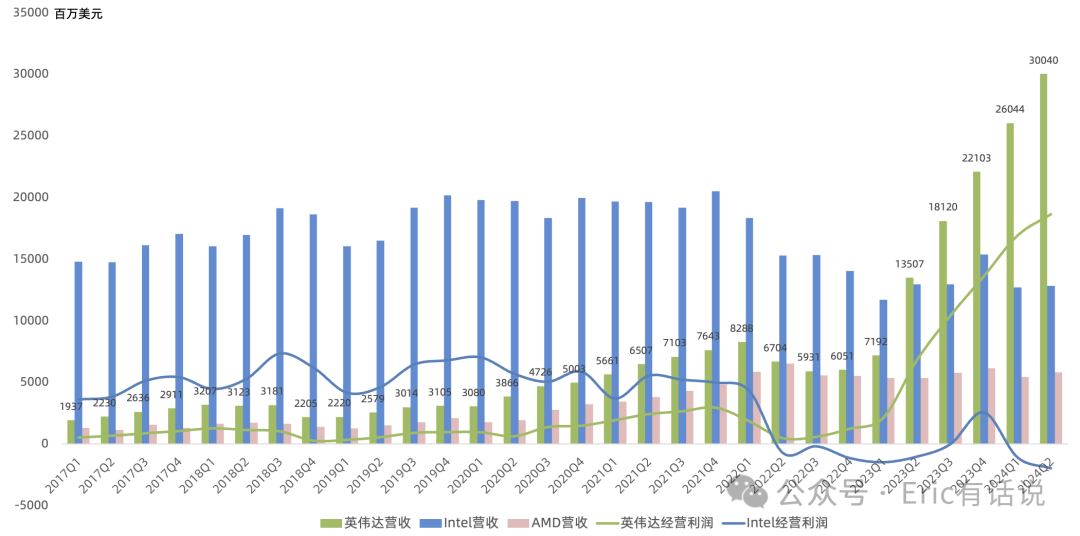

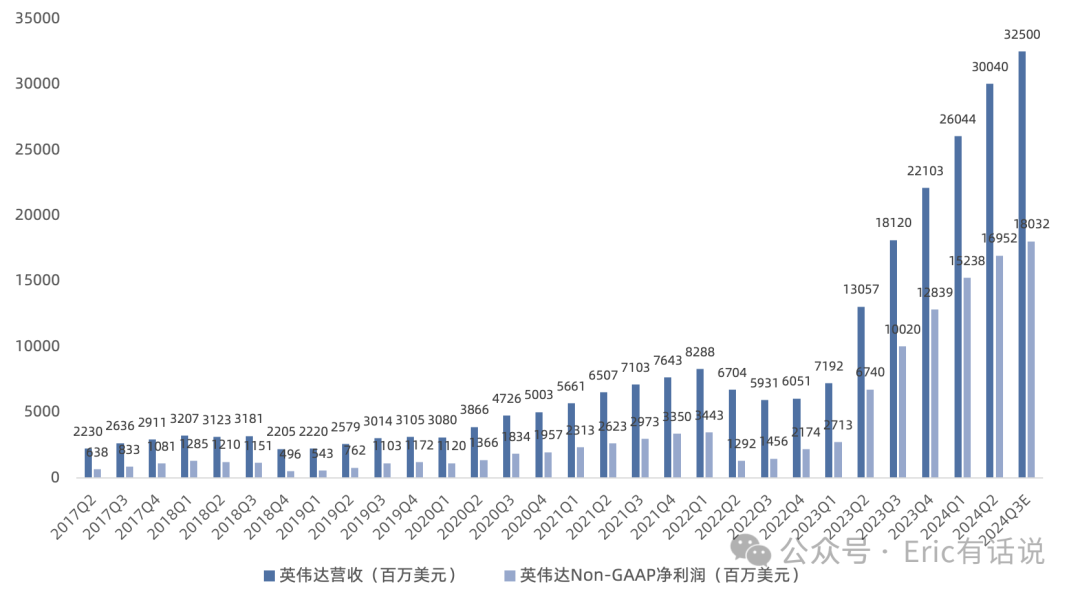

NVIDIA's Q2 earnings (May/June/July) again beat expectations, with Q3 guidance equally strong (Q3 revenue guided at $32.5B vs. consensus $31.8B). The media narrative of "missing the highest expectations" simply reset the bar. As the world's highest-revenue, highest-profit semiconductor company, NVIDIA keeps shattering industry ceilings and remains a lightning rod — something to get used to.

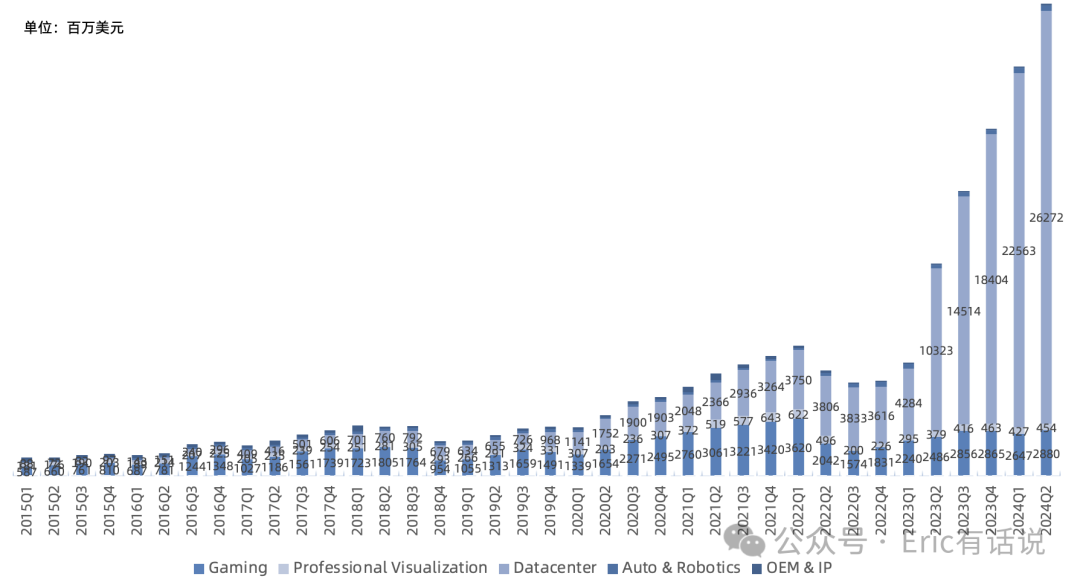

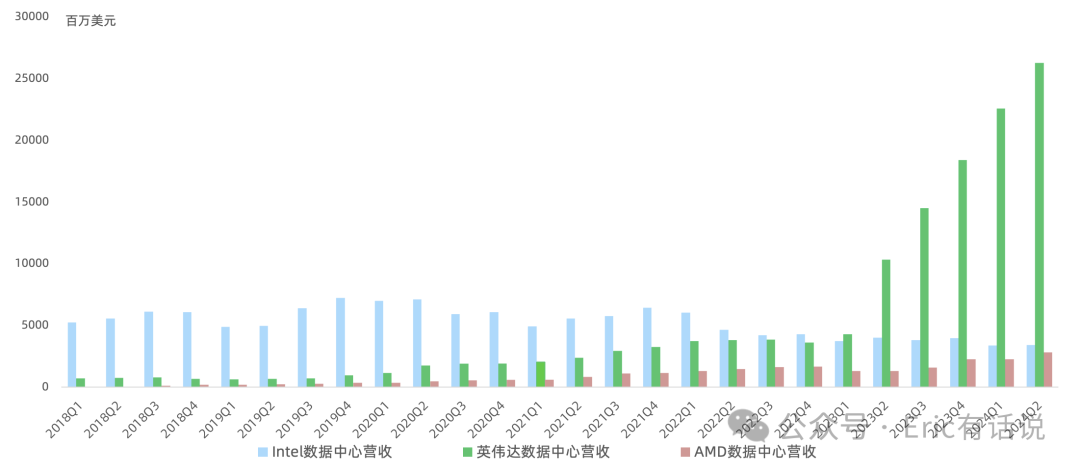

Data center Q2 revenue was $26.272B, up 16% sequentially and representing 88% of NVIDIA's total revenue, just $9M below AWS Q2 revenue. Growth was driven by Hopper training and inference GPUs and networking products, with most sequential growth coming from internet and other vertical industries. Enterprise AI adoption is accelerating across most Fortune 100 companies. CSPs accounted for 45% of data center revenue and vertical industries for more than 50%. Automotive and healthcare are each expected to contribute several billion dollars of revenue this year.

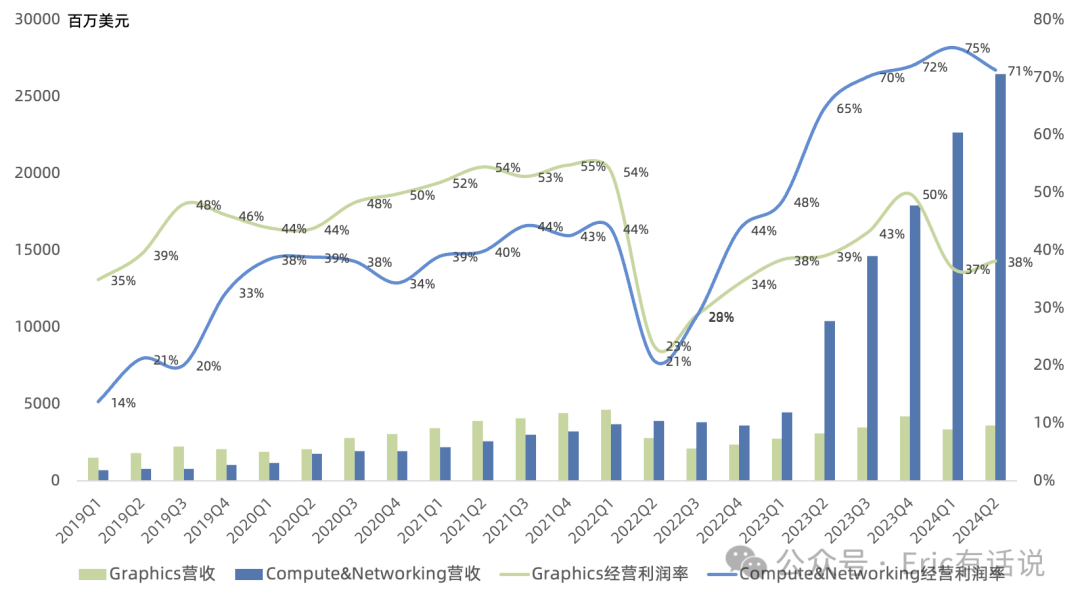

Inside Data Center:

Compute revenue $22.604B, up 163% year over year and 17% sequentially.

Networking revenue $3.668B, up 114% year over year and 16% sequentially. Driven by InfiniBand and Ethernet; Spectrum-X revenue doubled sequentially, expected to contribute several billion dollars for the full year (directly competing with Broadcom). Surpassing Broadcom to become the #1 networking chip vendor globally this year is highly likely.

Per guidance, Q3 revenue $32.5B, up 79% year over year; GAAP net income $16.8B, up 82%; Non-GAAP net income $18B, up 80%. Regarding concerns about growth deceleration, Q3 sits squarely in the H100-H200-Blackwell transition, and Blackwell is poised to launch the next growth wave.

In the previous article "NVIDIA Q1 Earnings: AI Supercomputer Is Not a 'Pick-and-Shovel Play,' It's a 'Money Printing Machine'," I noted: "Optimistically, full-year 2024 Non-GAAP net income could challenge the $80B mark." That now looks very plausible, with a floor of $70B. Q4 Non-GAAP net income could challenge $20B, directly challenging Apple, Microsoft, and Google (note their growth rates and valuations) — writing a new chapter for semiconductors.

Of course, views on AI sustainability vary. Skepticism, bearish calls, and even fabrications about NVIDIA have never ceased. I maintain my prior view: NVIDIA's future growth will likely come from two shifts — data center growth expanding from cloud-dominated to vertical industries and sovereign AI proliferating everywhere, and the seven-chip product matrix and roadmap moving from biennial to annual cadence.

On China, I maintain my prior view: "Given US-China dynamics, AI decoupling is inevitable; better short pain than long pain, especially since short-term pain is minimal — that's the most bullish signal."

FY25Q2 Call Highlights:

Blackwell delay: Blackwell mask change completed, production issues resolved. Sampling began in Q2; volume production starts in Q4, expected to contribute several billion dollars in Q4 revenue.

Sovereign AI progress exceeding expectations: Full-year sovereign AI revenue raised from high single-digit billions ($6-9B) to low double-digit billions ($10-13B).

Hopper still growing during product transition: During the H100-H200-Blackwell transition, Hopper demand continues to grow; second-half shipments expected to increase sequentially.

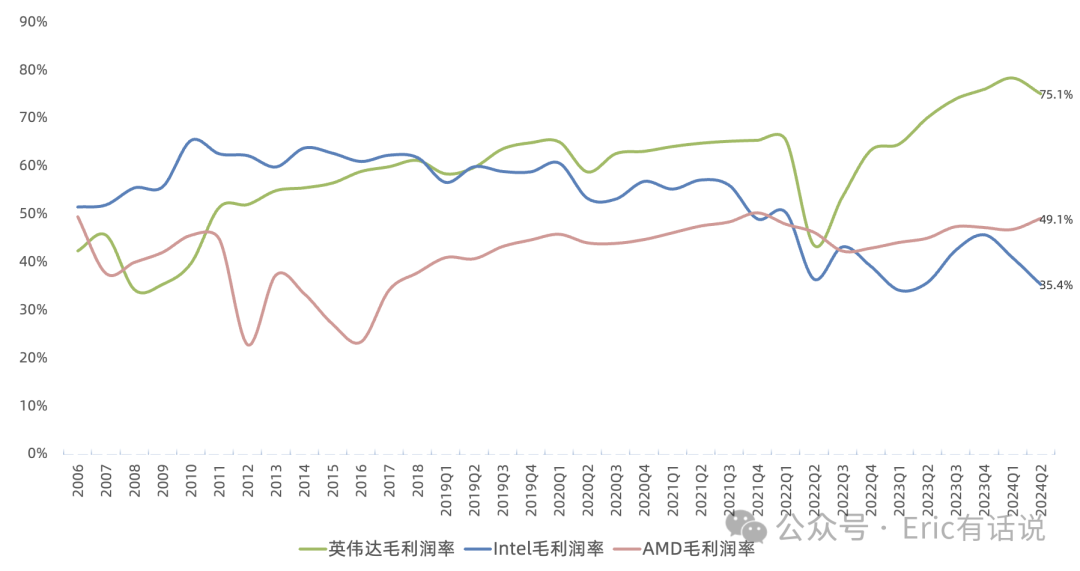

Sequential gross margin decline: Primarily due to Blackwell ramp and data center product mix shift. FY25 gross margin guided at 75% (consistent with prior guidance). Market concerns about Q4 margin above 72% are noted; opex expected up mid-to-upper 40% year over year (prior guidance low-40%). But with Non-GAAP net margin stable at 55%+, the market appears to be nitpicking.

Software progress exceeding expectations: Year-end software annualized revenue expected above $2B (prior guidance >$1B), including AI Enterprise (NeMo, NIMs, NIM Agent Blueprint, AI Foundry) continuing to grow.

Q2 repurchases $7B, dividends $246M. Prior remaining authorization $3.9B. As anticipated, an additional $50B buyback authorized.

Purchase commitments and obligations for inventory and manufacturing capacity were $27.8 billion (QoQ+48%) . Prepaid supply agreements were $4.7 billion (QoQ-16%) . DIS of 81 (QoQ-14) .

Blackwell is more than a GPU; it encompasses seven chip platforms: GPU, CPU, NVLink, ConnectX NIC, BlueField DPU, Quantum InfiniBand, Spectrum-X Ethernet.

Next year data center expected to grow significantly; all seven chip platforms expected to ship at record volumes.

Overall, on this earnings call, Jensen Huang emphasized the Blackwell platform vision; next year's earnings explosion is highly anticipated.

Previously noted: the beat-and-raise 10-for-1 split implied management's expectation of eventual annualized net income exceeding $100B. If quarterly EPS returns to $1, that implies $25B quarterly net income, a $100B run rate — achievable next year with Blackwell. A milestone quarter where net income surpasses Apple's is likely next year.

For NVIDIA, short-term stock volatility, media hit pieces, and even fabrications are par for the course — tall trees catch the wind. Best to keep a level head.