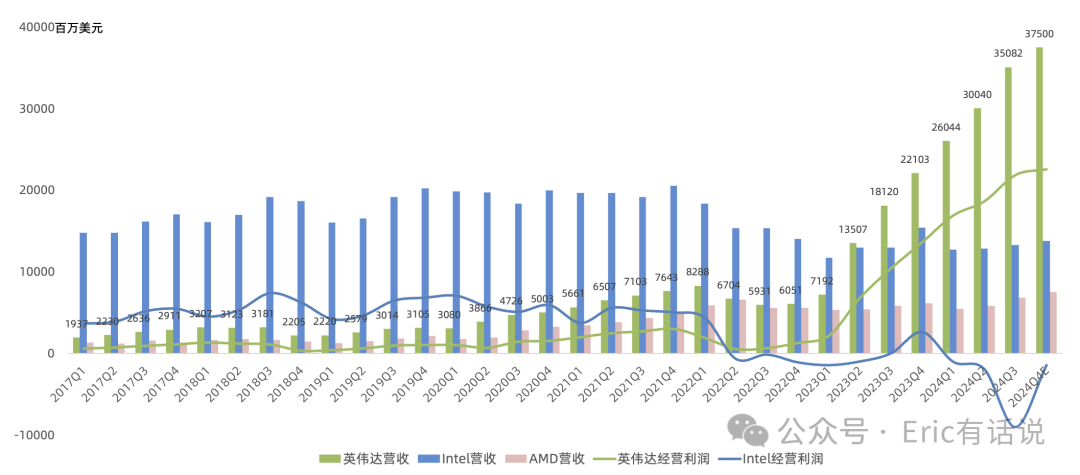

NVIDIA Q3 (Aug/Oct) beat again, and Q4 guidance also beat (Q4 revenue guide $37.5B vs. consensus $37.1B). Media claims of "missing highest expectations" are unique to this company. As the highest-revenue, highest-profit semiconductor company in history, NVIDIA keeps shattering industry ceilings and remains a lightning rod.

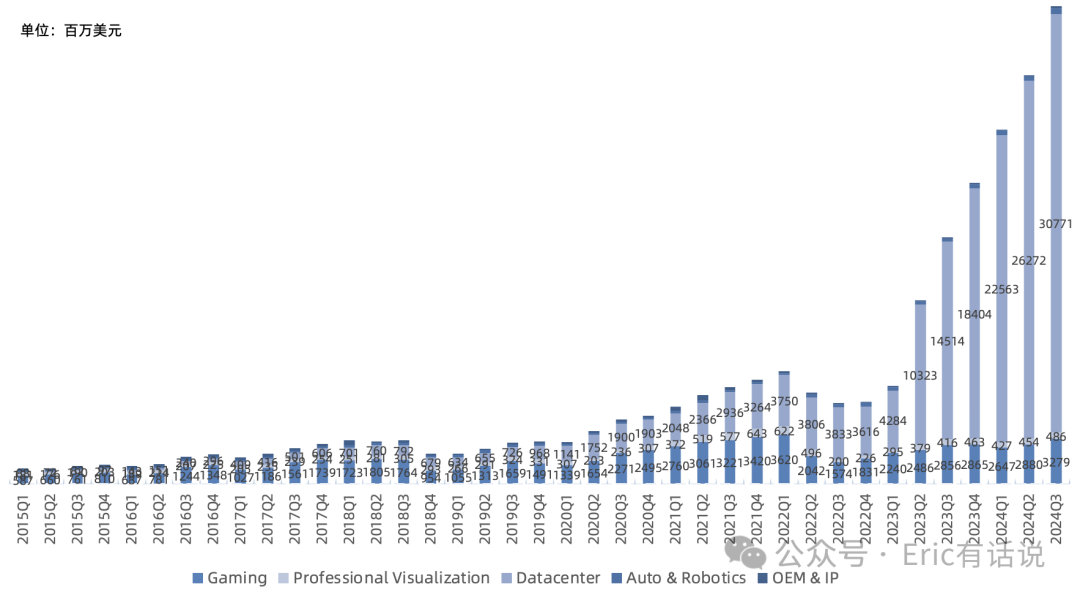

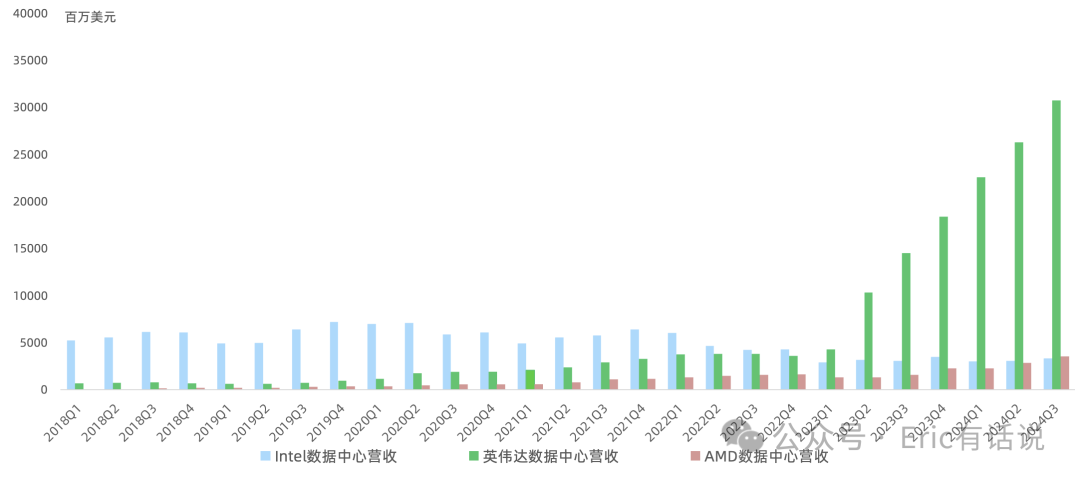

Data center Q3 revenue $30.771B, up 17% sequentially, 88% of total revenue. This single segment far exceeds AWS Q3 revenue ($27.5B). Growth driven by Hopper training and inference cards. H200 quarterly revenue surpassed $10B, now live on AWS, CoreWeave, Azure, with Google Cloud and OCI coming soon. CSPs ~50% of data center revenue; internet and verticals ~50%. NVIDIA is the world's largest inference platform.

Q4 Hopper and Blackwell ship together, both supply-constrained. Blackwell Q4 revenue will exceed prior guidance of several billion dollars; supply constraints to persist through next year. Hopper demand growing through H1 next year. Blackwell shipments to grow sequentially through next year, overtaking Hopper in Q1.

Inside Data Center:

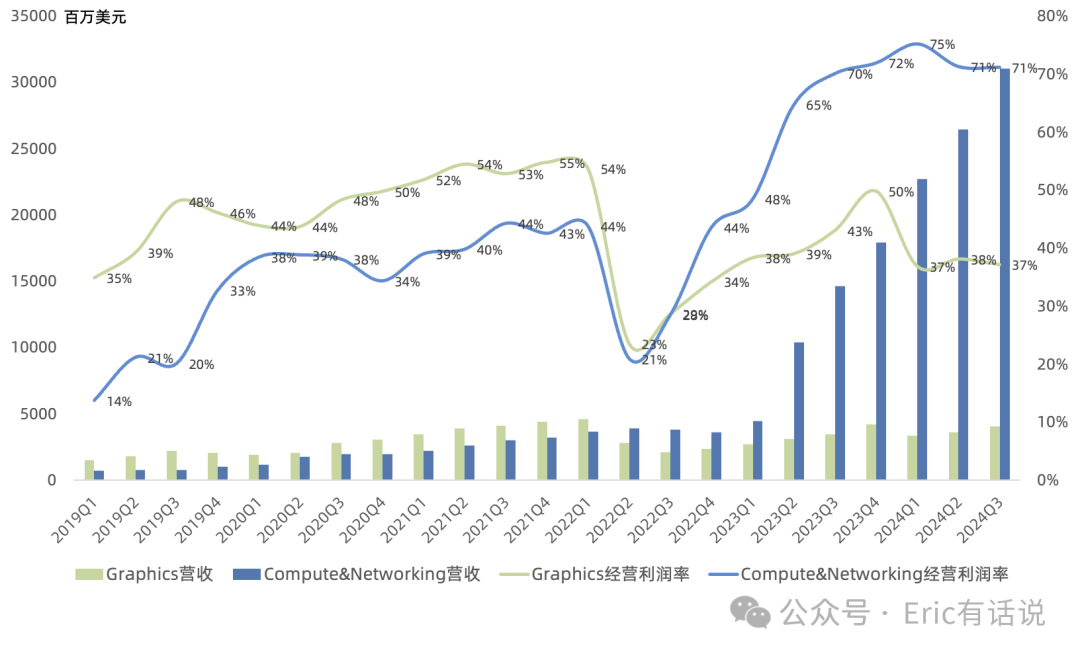

Compute revenue $27.644B, up 132% year over year and 22% sequentially. Oracle planning world's first zettascale AI supercomputer with 131,072 Blackwell GPUs. Microsoft to be first cloud provider offering GB200 service.

Networking revenue $3.127B, up 20% year over year, down 15% sequentially. Growth driven by Spectrum-X (directly competing with Broadcom). Networking demand remains strong and growing. Q4 expected to return to sequential growth. Full-year networking revenue scale may approach Broadcom's; overtaking Broadcom may wait until next year.

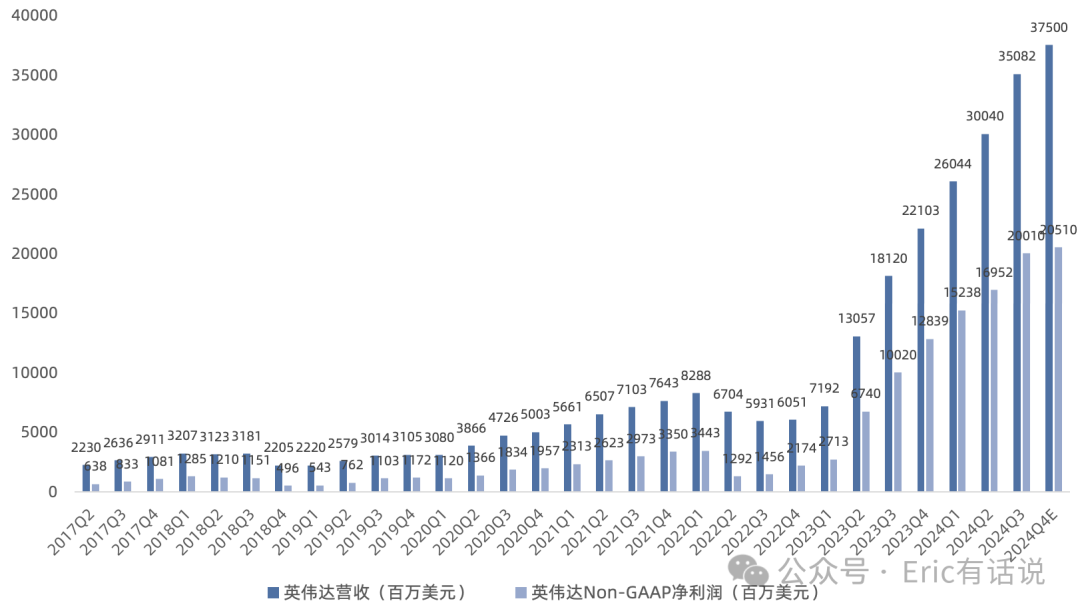

Guidance: Q4 revenue $37.5B, up 70% year over year. GAAP net income $19.2B, up 56% year over year. Non-GAAP net income $20.5B, up 60% year over year. On deceleration concerns: Q4 is in Blackwell ramp, and Jensen's guidance is historically conservative. Q4 could challenge $40B revenue.

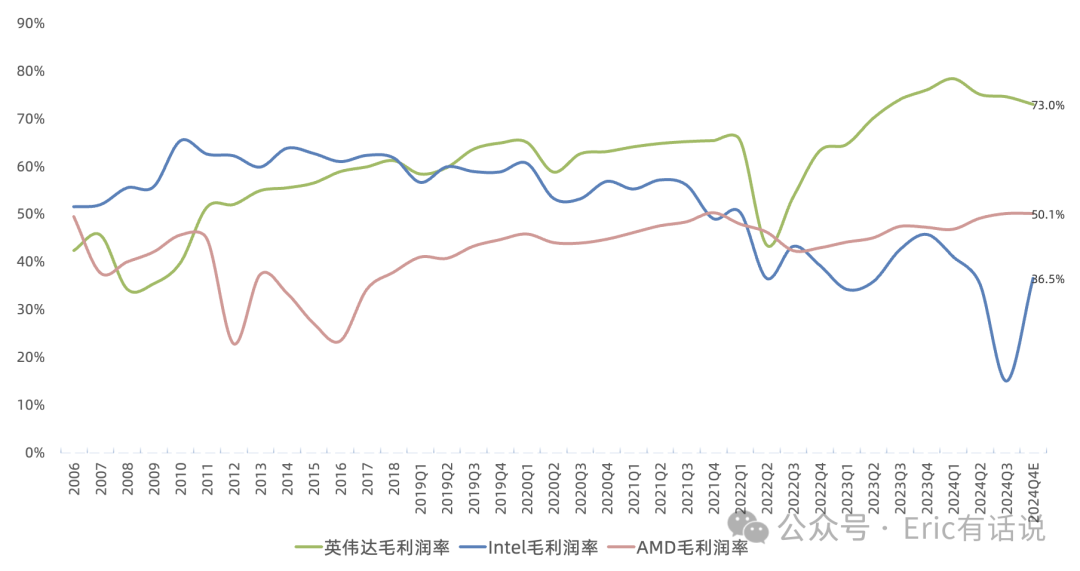

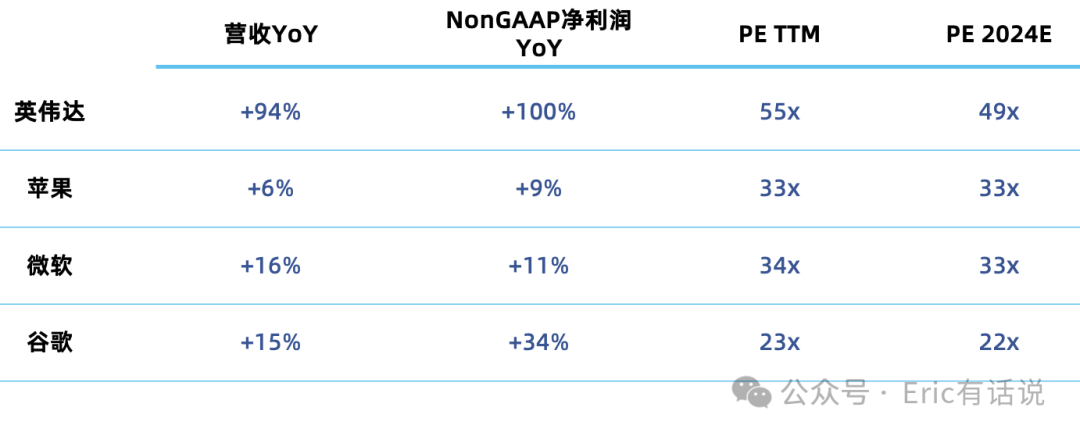

In the earlier "NVIDIA Q1 Earnings: AI Supercomputer Is Not a 'Shovel Seller' but a 'Money Printer'" piece, I noted: "Optimistically, FY24 full-year Non-GAAP net income could challenge $80B." That looks achievable; floor is $72.7B. I also said Q4 Non-GAAP net income could challenge $20B — Q3 already hit that. Now challenging Apple, Microsoft, Google (note their growth rates and valuations), writing a new semiconductor chapter.

Views on AI sustainability vary. Skepticism, bear cases, and FUD around NVIDIA have never stopped. I maintain my view: NVIDIA's future growth will come from two shifts: data center expansion from cloud-centric to verticals and sovereign AI everywhere, and a product roadmap moving from biennial to annual cadence across seven chip families. On AI trends, inference demand is just beginning to explode; Huang's goal is every tech company running 24/7 inference.

On China, I maintain my prior view: "Given US-China dynamics, AI decoupling is inevitable; better short pain than long pain, especially since short-term pain is minimal — that's the most bullish signal."

FY25Q3 Call Highlights:

Blackwell shipments: Q3 sampled 13,000 Blackwell GPUs, including first Blackwell DGX systems to OpenAI.

Blackwell gross margin: Ramp gross margin expected in low-70%s, rising to mid-70%s by H2 next year.

Hopper demand during transition: Hopper demand continues growing through H1 next year amid H100-H200-Blackwell transition.

Software progress on track: Software revenue reached a $1.5B annualized run rate this quarter, expected to exceed $2B by year-end (unchanged); AI Enterprise revenue, including NeMo, NIMs, NIM Agent Blueprint, and AI Foundry, doubled year over year; nearly 1,000 companies are now using NIMs.

Q3 repurchased $11B, paid $245M in dividends; $46.4B remains authorized for repurchases.

Purchase commitments and obligations for inventory and manufacturing capacity were $28.9 billion (QoQ+4%) . Prepaid supply agreements were $4.7 billion (QoQ+11%) . DIS of 78 (QoQ-3) .

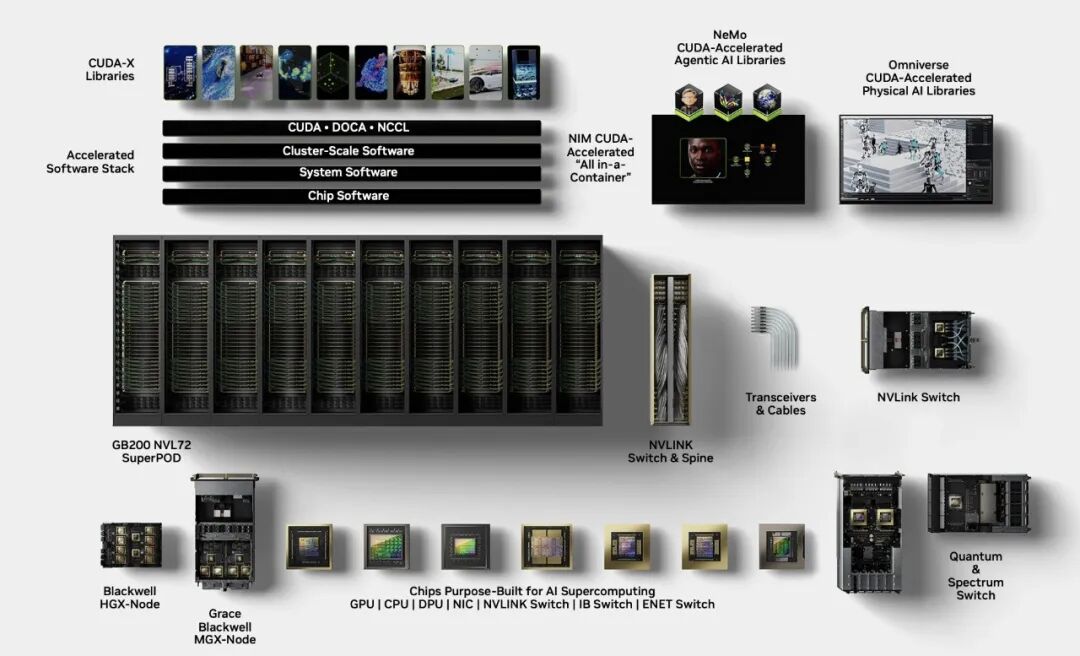

Blackwell system SKUs come in 7 types: liquid-cooled/air-cooled, NVL8/36/72, x86/Grace.

Revenue by billing location this quarter: US 42%, Singapore 22%, Mainland China 15%, Taiwan 15%; top customer 12%, second 12%, third 12%, fourth below 10%.

Overall, on this earnings call Jensen Huang again emphasized the explosion in inference demand and the platformization prospects of Blackwell; next year's earnings breakout is highly anticipated.

Previously noted, the unexpected 10-for-1 split implied management's expectation of annualized net income exceeding $100B. If quarterly EPS returns to $1, that implies $25B quarterly net income, a $100B run rate, achievable next year with Blackwell's help. A milestone moment where net income likely surpasses Apple to become the world's highest will probably occur in the first half of next year (though Q3 GAAP net income already exceeded Apple's, Apple was impacted by a one-time tax charge).

For NVIDIA, short-term stock volatility, media smears, and rumors are inevitable—tall trees catch the wind; best to view them with equanimity.