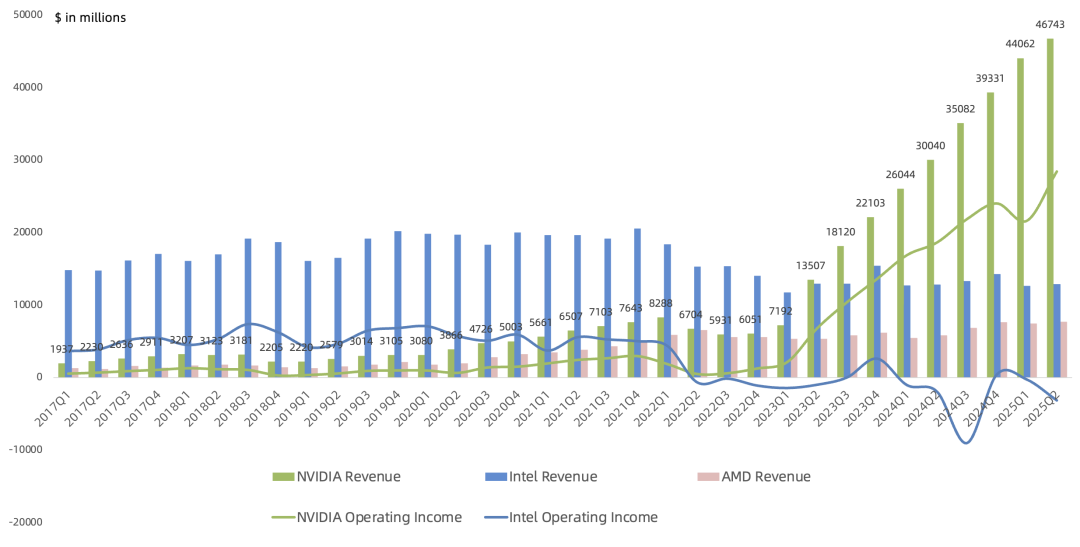

As the company most negatively impacted by politics, with H20 prospects uncertain, NVIDIA's FY26 Q2 earnings (May/Jun/Jul 2025) again beat expectations, with Q3 guidance also above expectations, notably excluding H20. As the highest-revenue, highest-net-income company in global semiconductor history, NVIDIA continues to break industry ceilings, with quarterly net income poised to become the global leader.

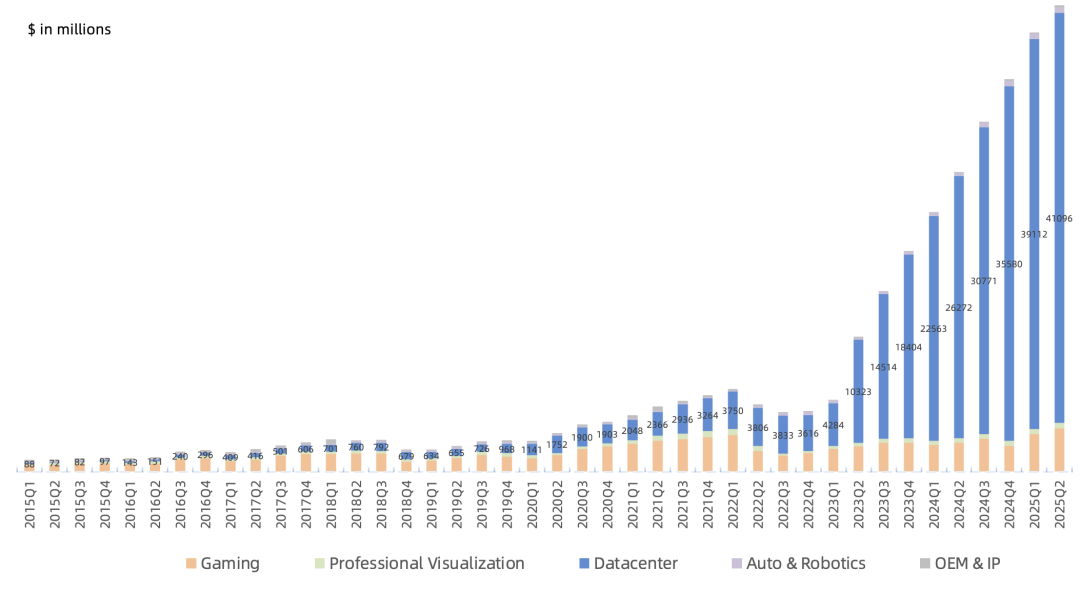

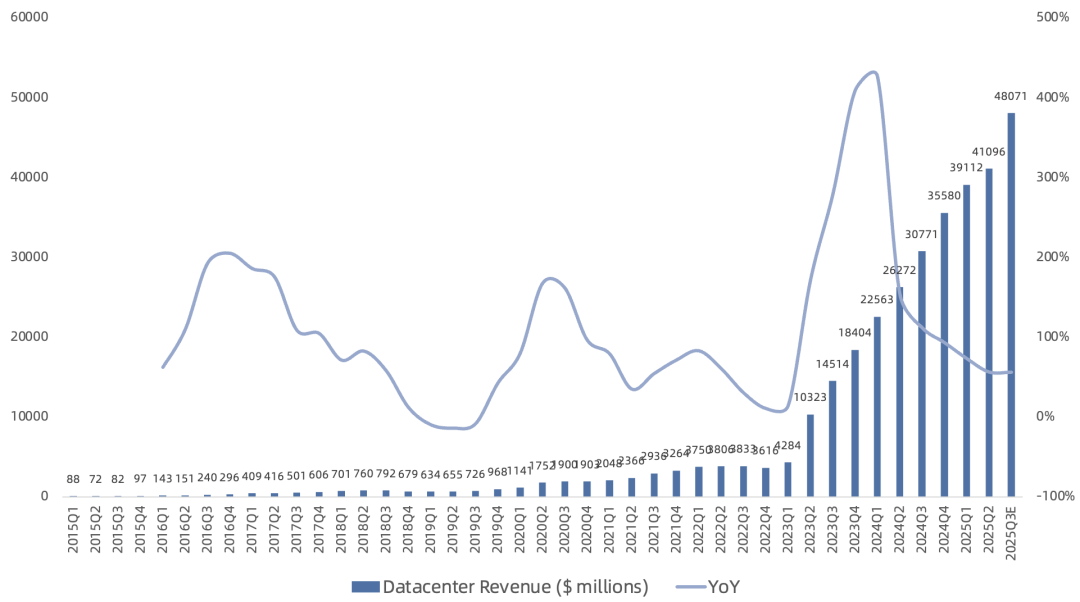

Data Center Q2 revenue was $41.1B, up 56% year over year and 5% sequentially, representing 88% of total NVIDIA revenue. Blackwell accounted for nearly 80% of Data Center compute revenue this quarter (~$27B, up from ~$23B last quarter). Hopper shipments also grew. GB200 NVL72 has begun ramping, deployed across major cloud providers and consumer internet companies. Because GB300 shares architecture, software, and physical dimensions with GB200, the transition to GB300 is seamless. Factory lines successfully converted in late July/early August to support GB300 capacity ramp, producing ~1,000 racks per week. With additional capacity coming online, Q3 output is expected to accelerate further, reflected in Q3 Data Center revenue guidance, where the sequential increase will set a company record.

Inside Data Center:

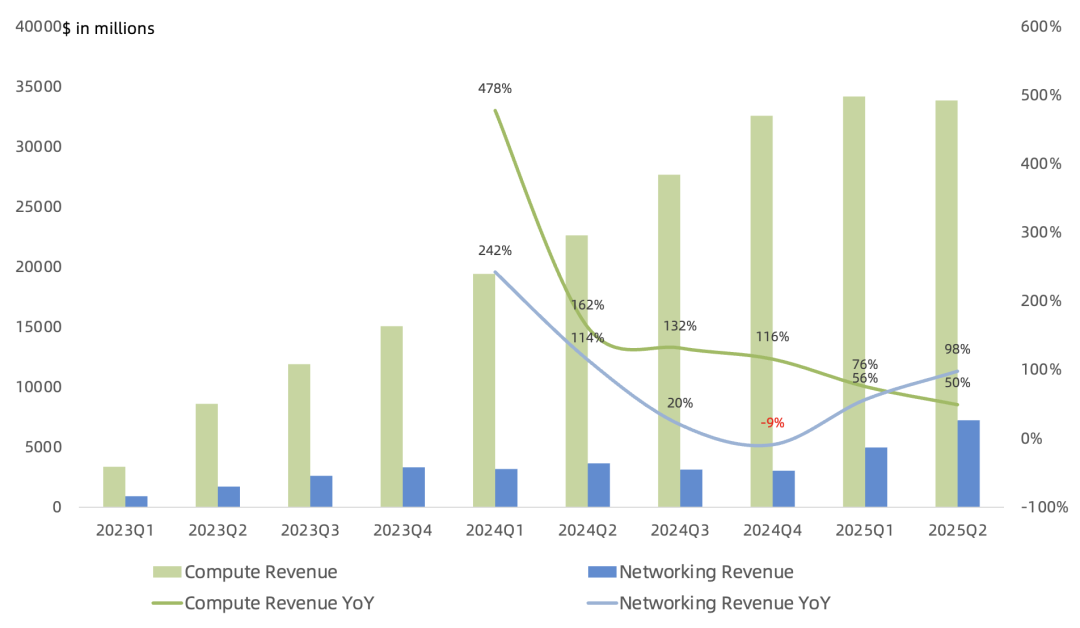

Compute revenue was $33.8B, up 50% year over year, down 1% sequentially, sparking market concern, primarily due to the Hopper-to-Blackwell product transition. Although Blackwell products are still early, software optimization has already doubled performance (Hopper products improved 4x over 2+ years). RTX Pro servers are now in full production for global system builders.

Networking revenue was $7.3B (Broadcom FY25 Q1 ~$4.6B, then discontinued disclosure), up 98% year over year and 46% sequentially, far exceeding expectations, driven by rack demand. Spectrum-X Ethernet, InfiniBand, and NVLink saw strong demand. InfiniBand revenue nearly doubled sequentially. Spectrum-X grew double digits both year over year and sequentially, with quarterly revenue exceeding $2.5B and a run rate above $10B. The company's four networking compute platforms—NVLink + Spectrum-X + InfiniBand + BlueField DPU—cover scale-up, scale-out, and scale-across. The networking chip business is poised to open a second growth curve for NVIDIA's Data Center segment.

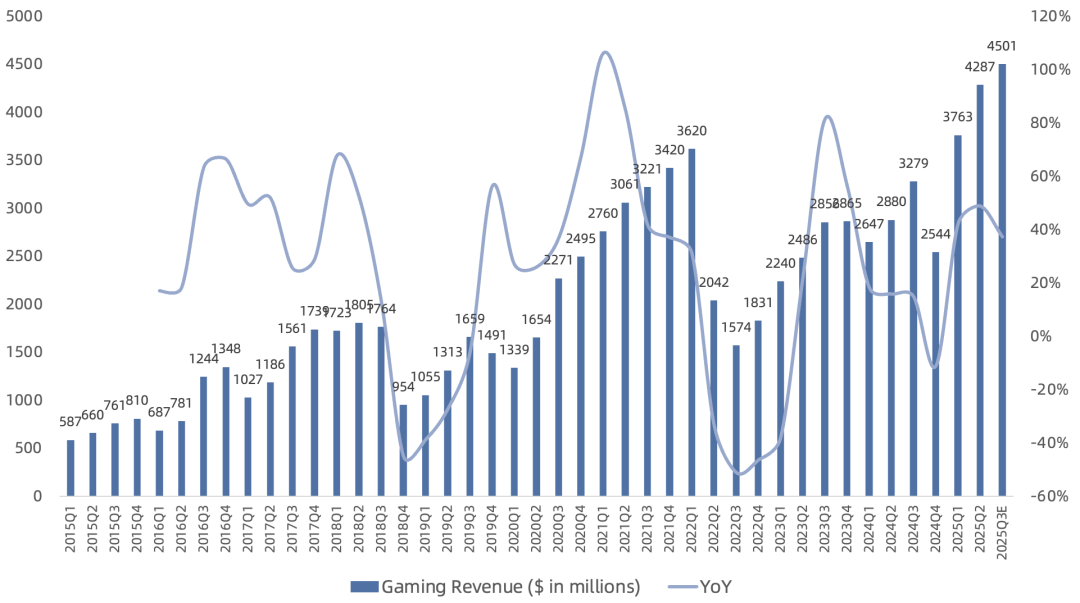

Gaming Q2 revenue was $4.3B, up 49% year over year and 14% sequentially, setting a new all-time high. Driven by full-volume ramp of Blackwell GPUs, which became the fastest-ramping gaming GPU in company history. Blackwell arrives on GeForce NOW in September. GFN library now exceeds 4,500 titles.

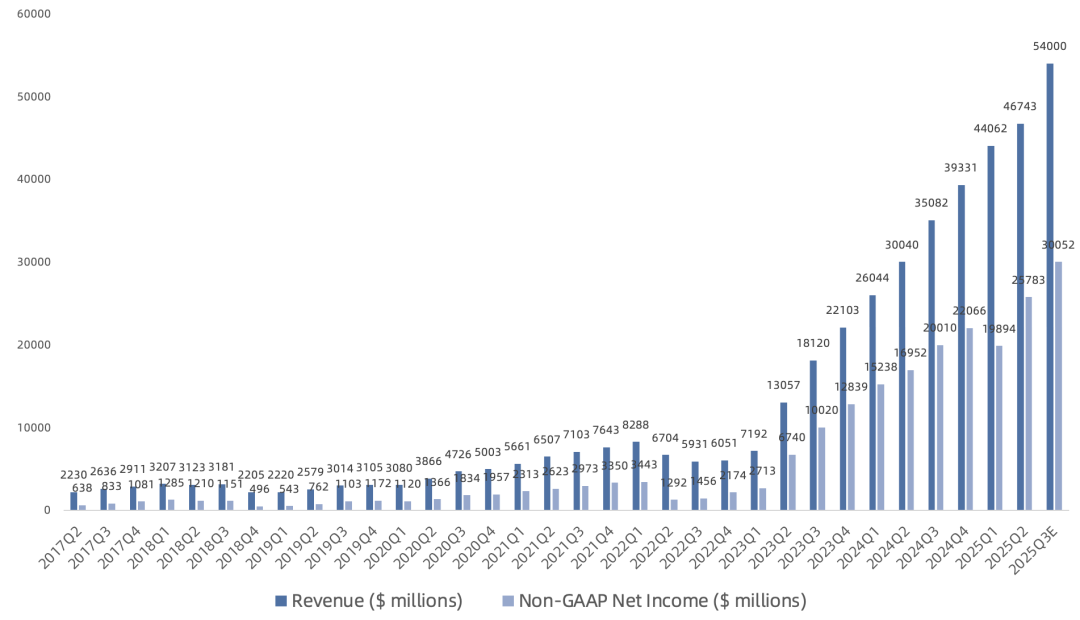

Per guidance, Q3 revenue is $54B, up 54% year over year, excluding H20. Benefiting from Blackwell Ultra platform ramp, Data Center compute chips return to high growth, with Data Center revenue guided at $48B, up 56% year over year.

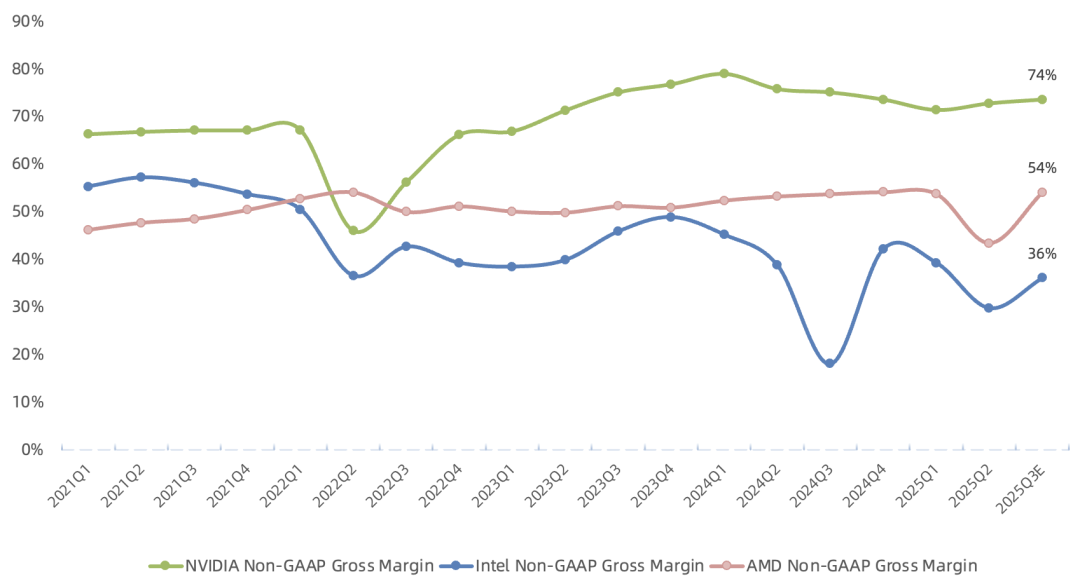

Q3 GAAP gross margin guided at 73.3%, non-GAAP at 73.5%. GAAP net income guided at $28.5B, up 48% year over year. Non-GAAP net income guided at $30.1B, breaking the $30B profit threshold for the first time, up 50% year over year. Q4 gross margin expected to recover to 75%.

Views on AI sustainability vary; skepticism, bearishness, and rumors about NVIDIA have never ceased. I maintain my prior view: NVIDIA's future growth will likely come from two shifts: Data Center growth expanding from cloud-led to vertical industries and sovereign AI proliferating (DeepSeek accelerated AI democratization), and the seven-chip product matrix and roadmap moving from biennial to annual cadence. Future plans include multiple 10GW AI factories; average 1GW AI factory capex is ~$50B, with NVIDIA products representing ~35% of value. The global AI factory build-out is still early. Next quarter, RTX Pro product line targeting enterprise AI demand begins shipping.

On China, I maintain my prior view: 'Given US-China dynamics, AI decoupling is inevitable; better short pain than long pain.' But Jensen remains reluctant to abandon the $50B market.

FY26 Q2 Call Highlights:

Over the past few weeks, some mainland China customers have obtained licenses but have not yet shipped any H20 products under those licenses; the U.S. government has not yet formalized the 15% revenue-share requirement in regulation. Q3 guidance excludes H20; if geopolitical issues are resolved, Q3 H20 product revenue is expected to be between $2B and $5B. In Q2, approximately $650M of H20 products were sold to an unrestricted customer outside mainland China.

To support Blackwell and Blackwell Ultra capacity ramp, inventory rose from $11B in Q1 to $15B in Q2 sequentially, impacting OCF and FCF.

Sovereign AI Progress: FY sovereign AI revenue expected >$20B, doubling year over year.

Global AI capex is ~$600B this year, projected to reach $3-4T by 2030.

Two new businesses added this quarter with potential multi-billion annualized revenue: RTX Pro servers and automotive Thor chip.

Q2 repurchased $9.7B, paid $244M in dividends, announced a $60B buyback program (third-largest in US equities), with $74.7B remaining authorization.

Purchase commitments and obligations for inventory and manufacturing capacity were $43.5 billion (QoQ+46%) ;

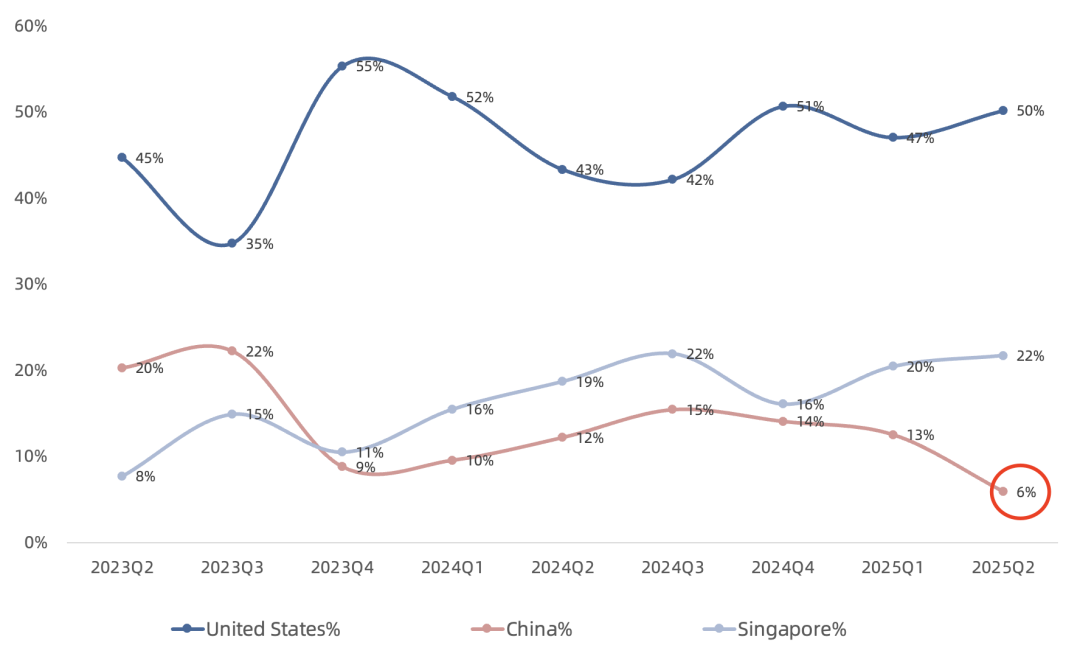

By billing geography this quarter: US 50%, Singapore 22% (99% of Data Center compute revenue from US customers), Taiwan 18%, Mainland China 6%. Top customer 23%, second 16%, third 14%, fourth 11%, fifth 11%, sixth 10%.

Rubin platform chips are in fab, including Vera CPU, Rubin GPU, CX9 SuperNIC, NVLink 144 scale-up switch, Spectrum-X scale-out and scale-across switches, and silicon photonics CPO processor. Rubin platform on track for volume production next year, which will be another record year.

Overall, on this earnings call, Jensen again emphasized the high ROI of AI infrastructure using GB300 and expressed high hopes for next year's Rubin platform. The market will track Rubin ramp progress as closely as it did Blackwell last year.

Previously noted: the unexpected 10-for-1 split implies management expects annualized net income to exceed $100B. If quarterly EPS returns to $1, that implies $25B quarterly net income, a $100B run rate, likely achievable this year with Blackwell's help. A milestone moment where net income surpasses Apple to become the world's most profitable company is probable this year.

Many may not yet realize that virtually all current AI large models are trained on older Hopper or legacy TPUs. Even GPT-5-Thinking training uses H100/H200. No one has yet seen a large model trained on new Blackwell GPUs. On paper, the performance specs are worth anticipating.