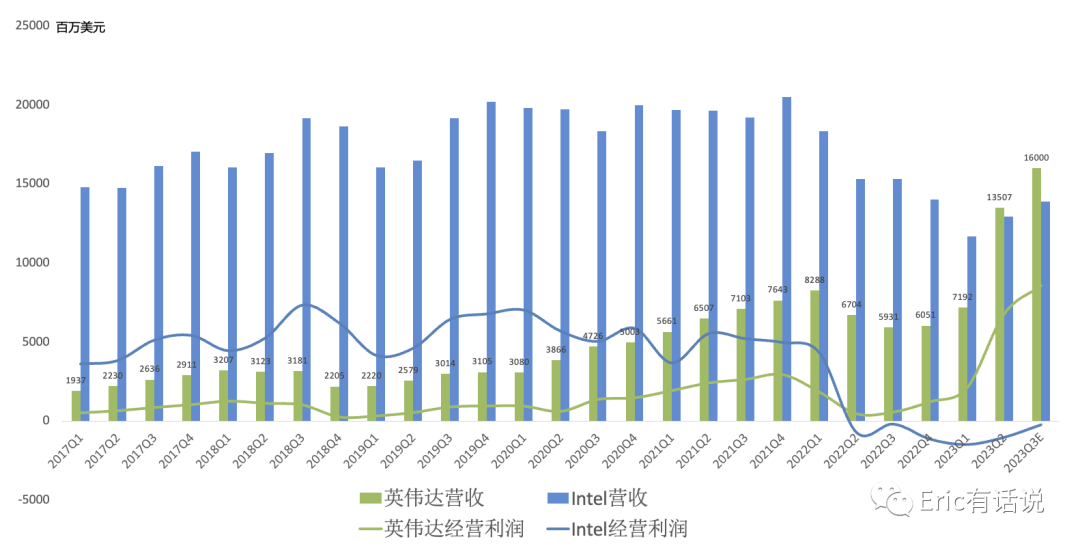

NVIDIA's Q2 earnings continued to far exceed expectations, with equally strong Q3 guidance (Q3 revenue guide of $16B vs. consensus of $12.5B), also modestly above my personal estimate of $15B. I had previously optimistically predicted that Q3 single-quarter revenue could overtake Intel; now Q2 revenue scale has already surpassed Intel ($12.95B) and Samsung ($11.14B), trailing only the global foundry leader TSMC ($15.68B), making NVIDIA the world's highest-revenue semiconductor chip company—a new era has begun.

Looking back to my 2021 call that NVIDIA revenue would soon surpass Intel, many thought it was fantasy; that is precisely the allure of technology.

There isn't much to update on Q2 results: gaming has rebounded for three consecutive quarters since bottoming in Q3 last year, and Q3 will approach the range floor of the 2021 Q2–2022 Q1 mining peak (around $3B per quarter), while Intel and AMD's PC businesses are only just starting to recover.

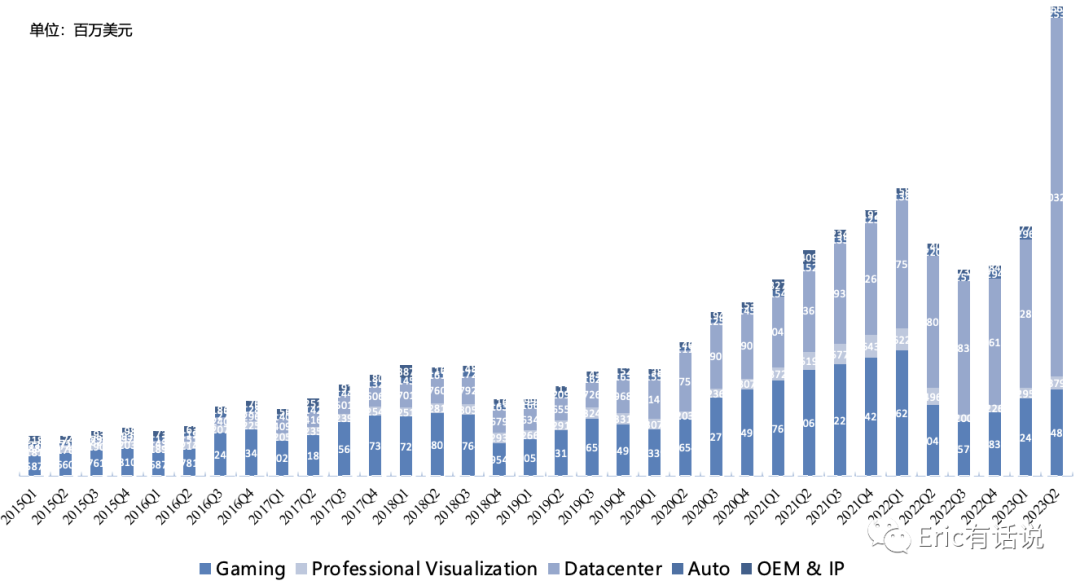

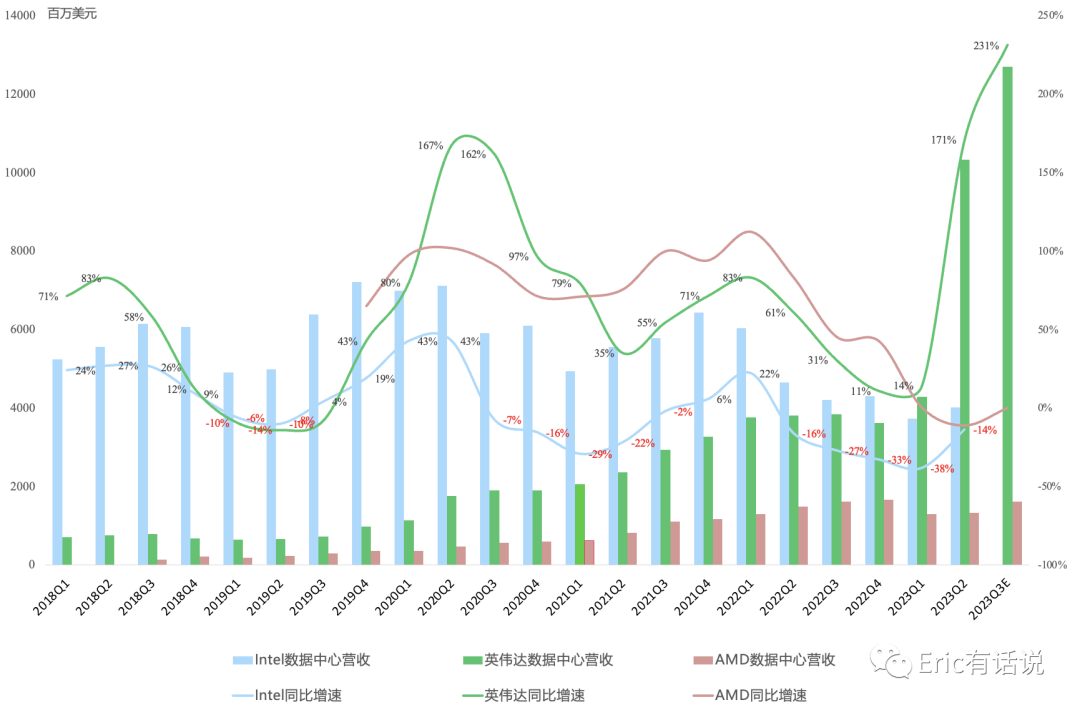

Another data center milestone: this quarter data center revenue exceeded $10B for the first time! The data center business alone now exceeds NVIDIA's revenue at any point in its history—effectively creating another NVIDIA.

Per guidance, Q3 revenue of $16B implies 170% year-over-year growth; GAAP net income of $7.3B implies 980% year-over-year growth; non-GAAP net income of $8.2B implies 464% year-over-year growth. Management expects data center supply to grow through next year; linearly extrapolating Q3 results, full-year 2023 non-GAAP net income should be at least $26B. Applying NVIDIA's long-term valuation range of 50–70x yields a market cap of $1.3–1.8T.

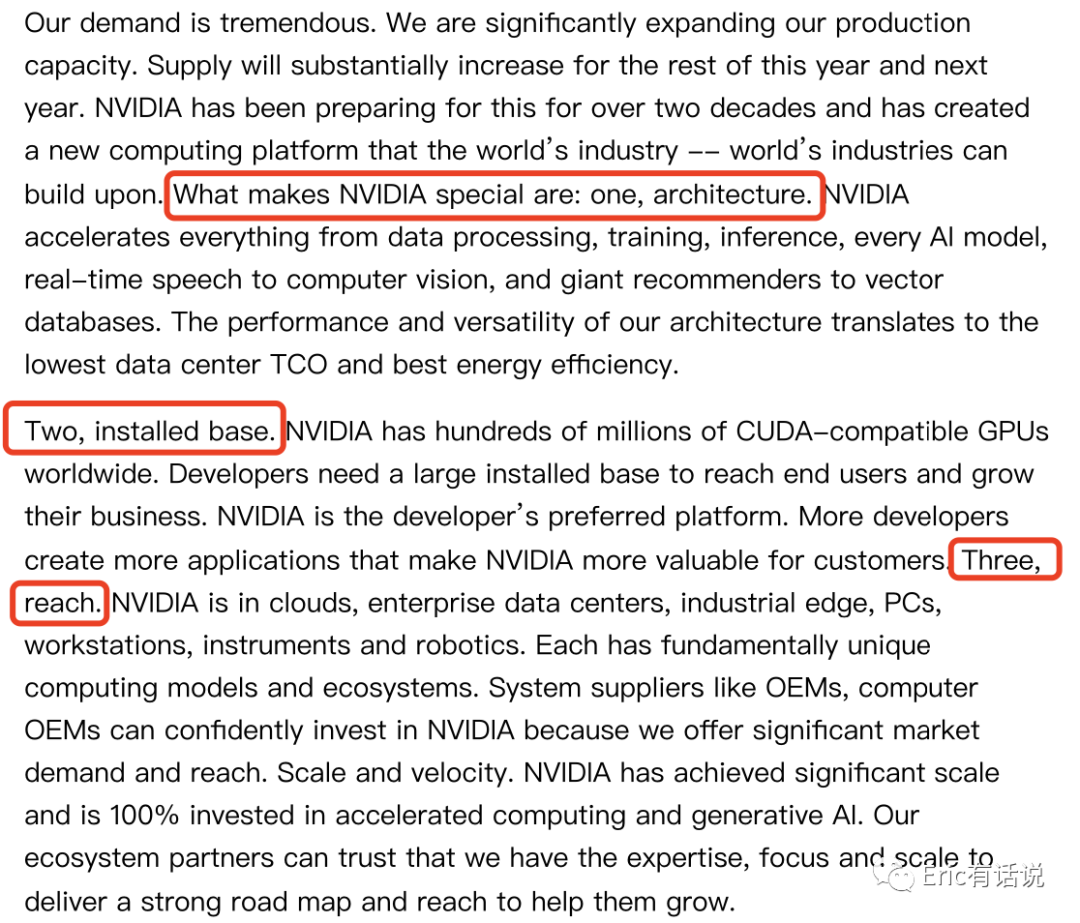

Of course, AI sustainability remains to be seen, and opinions vary; skepticism and bearish calls on NVIDIA have never ceased. Jensen has consistently emphasized that the installed base of data center semiconductors is $1T (annual spend of $250B) and growing, but historically this spend was CPU-centric, whereas going forward it will shift to GPU-centric AI data centers, and penetration is still very low.

FY24 Q2 Call Highlights:

Data center compute revenue grew 195% year over year, driven primarily by CSP and consumer internet demand for the HGX platform; supply is expected to increase each quarter; US data center growth is strongest; China revenue, including both compute and networking, remains in the historical 20–25% range; data center revenue mix: HGX > DGX > GPU; H100 typically ships as HGX; CSPs account for over 50% of data center revenue, followed by consumer internet, then enterprise & HPC.

L40S is not constrained by packaging supply and is shipping in volume; L40S positioning differs from H100, targeting fine-tuning workloads, compatible with standard servers for plug-and-play deployment, suited for the enterprise market; nearly 100 NVIDIA AI Enterprise-ready servers have launched; GH200, including the Grace CPU, has shipped to OEMs this quarter; DGX GH200 is expected to ship by year-end, with Google Cloud, Meta, and Microsoft as launch partners; the HBM3e version of GH200 will not ship until Q2 2024; leading CSPs are currently evaluating the next-generation product.

Data center networking revenue grew 94% year over year, with strong InfiniBand demand attached to HGX shipments; for traditional Ethernet users, Spectrum-X paired with BlueField-3 is available; Q3 data center revenue is expected to grow significantly sequentially; data center demand visibility extends through next year, with capacity continuing to grow over the next several quarters.

Gaming sequential growth was driven by strong notebook RTX 40-series sales; overall notebook and desktop demand is robust; RTX install base is 47%, with 20% at RTX 3060 or above, leaving significant penetration upside; notebook GPU shipments exceeded desktop in several regions, and Q3 will remain strong; over 330 games/applications now support DLSS.

Visualization workstations are recovering, with strong demand for Ada visualization products; software revenue continues to grow, now at an annualized run rate of several hundred million dollars.

Automotive revenue declined sequentially due to weak China NEV sales; collaboration with MediaTek on automotive.

Q2 repurchases of $3.28B and dividends of $100M; announced an additional $25B repurchase authorization, with $4B remaining from the prior program.

Going forward, I remain eager to see how NVIDIA's Grace CPU performs as an Arm challenger breaking the Intel/AMD x86 duopoly in the data center CPU market. Short-term stock volatility is inevitable, but a level-headed perspective is warranted.

We are fortunate to live in an era of technological explosion, yet long after GPT-4's launch, most people in China still haven't experienced a large AI model; AAA game graphics are nearly photorealistic, yet many still associate gaming visuals with mobile games; chip process nodes are approaching the angstrom era, yet many still believe semiconductor scaling is near its physical limits.