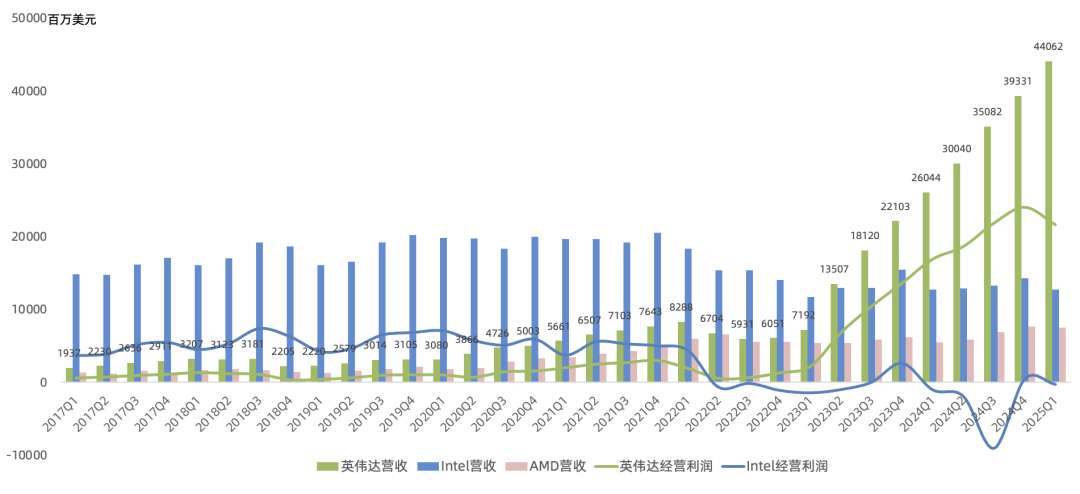

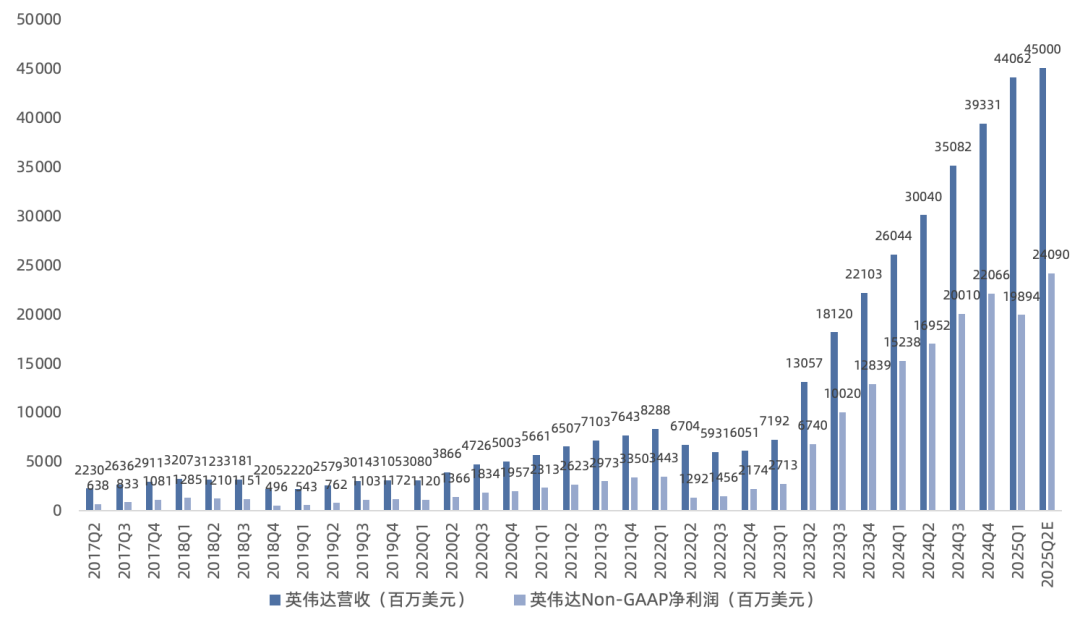

As the company most negatively impacted by US politics, NVIDIA still beat expectations in FY26Q1 (Feb 2025/Apr 2025) despite a $4.5B H20 charge (prior guide $5.5B), and gave in-line Q2 guidance — especially beating on an ex-H20 basis. As the highest-revenue, highest-net-income semiconductor company in history, NVIDIA continues to shatter industry ceilings.

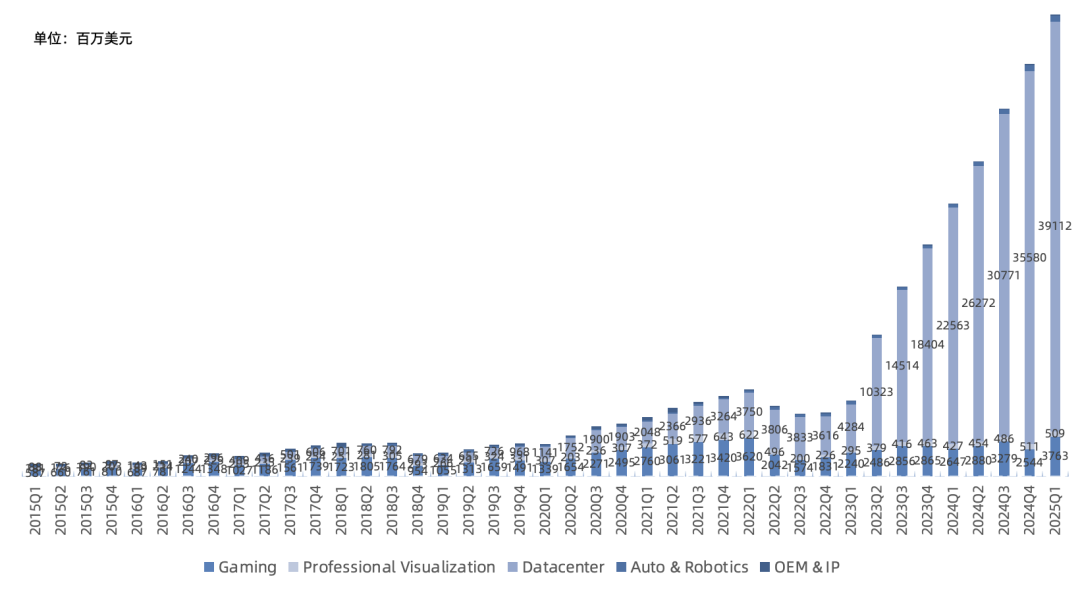

Data center Q1 revenue $39.11B, up 73% year over year and 10% sequentially, representing 89% of total NVIDIA revenue. Blackwell accounted for nearly 70% of data center compute revenue this quarter (>$23B, up from $11B last quarter). GB200 NVL72 in full volume ramp; major CSP customers deploying nearly 1,000 NVL72 racks per week on average, with Q2 ramp accelerating. Microsoft has deployed 100K Blackwell GPUs and is preparing to ramp hundreds of thousands of GB200s for OpenAI. H20 original revenue would have been $7B; export ban prevented ~$2.5B in shipments; actual recognized revenue $4.6B. CSP share of data center revenue below 50%; internet and vertical industries above 50%.

Inside Data Center:

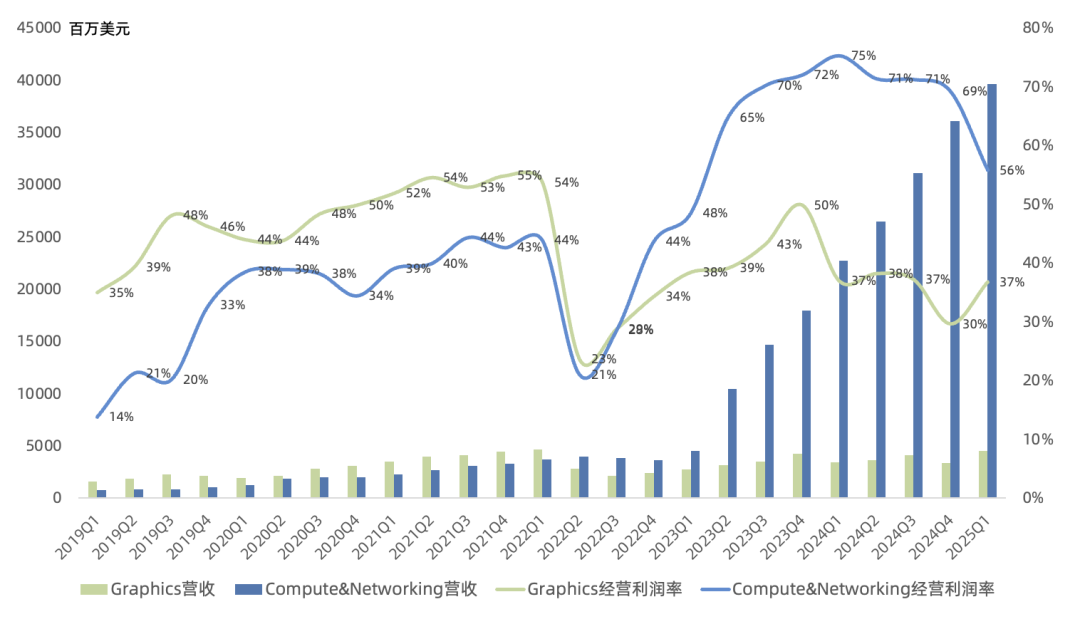

Compute revenue $34.155B, up 76% year over year and 5% sequentially. GB300 began sampling to major CSPs in early May, volume production in July; GB300 and GB200 are drop-in compatible. Customer AI inference demand surged this quarter (OpenAI, Microsoft, Google). Microsoft processed over 100 trillion tokens in Q1, up 5x year over year. Inference driving exponential compute demand. Agentic AI empowering enterprise AI. Despite Blackwell being early, software optimization delivered 1.5x performance gain in one month (Hopper took 2+ years for 4x).

Networking revenue $4.957B (Broadcom ~$4.6B last quarter), up 56% year over year and 64% sequentially. Driven by NVLink growth from GB200 ramp and Ethernet product demand. NVLink quarterly revenue >$1B (NVLink Fusion could be a future growth driver). Spectrum-X strong growth both year over year and sequentially, quarterly revenue >$2B. Added Google and Meta as customers this quarter; prior customers: CoreWeave, Microsoft, Oracle, xAI. Four major networking compute platforms: NVLink + Spectrum-X + InfiniBand + BlueField DPU. 2025 full-year networking revenue on track to surpass Broadcom.

Gaming Q1 revenue $3.76B, up 42% year over year and 48% sequentially, a record high. Driven by full Blackwell GPU ramp; fastest-ramping gaming GPU in company history.

Per guidance, Q2 revenue $45B, up 50% year over year, including an $8B H20 revenue hit. This implies original Q2 guidance of $53B, up 76% year over year. Net income on track to breach $30B — a shame the H20 ban is self-inflicted by the US.

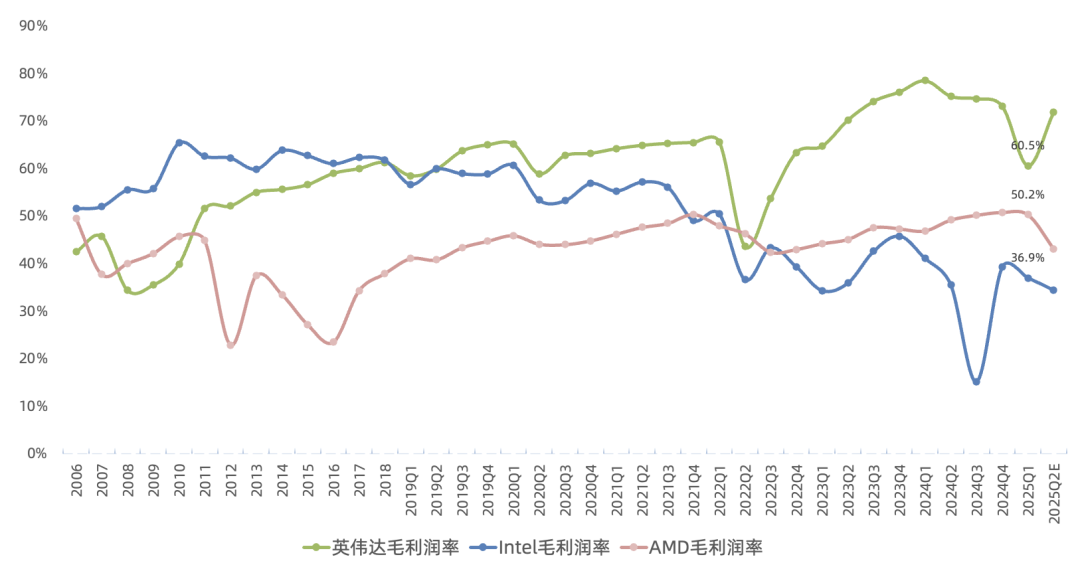

Q2 GAAP gross margin guided at 71.8%, Non-GAAP at 72%. H20 charge impact dissipates quickly. GAAP net income guided at $22.6B, up 36% year over year. Non-GAAP net income guided at $24.1B, up 42% year over year. Regarding margin concerns: the removal of low-margin H20 actually helps H2 margins recover toward 75% quickly.

Views on AI sustainability vary. Skepticism, bearish calls, and FUD around NVIDIA have never ceased. I maintain my prior view: NVIDIA's future growth will come from two shifts — data center growth expanding from cloud-led to vertical industries and sovereign AI everywhere (DeepSeek accelerated AI democratization), and the chip product matrix/roadmap moving from biennial to annual cadence. This quarter, global NVIDIA AI factories neared 100, count doubled year over year, GPUs per factory also doubled. Multiple 10GW AI factories planned. Global AI factory build-out still in early innings. RTX Pro, DGX Spark, DGX Station product lines directly targeting enterprise AI.

On China, I maintain my prior view: 'Given US-China dynamics, AI decoupling is inevitable; better short pain than long pain.' But Jensen remains reluctant to abandon the $50B market.

Also noted in this quarter's 10Q: another Jensen share sale plan, expecting to sell 6M shares by end of 2025 (~$800M+), giving media more fuel for panic narratives.

FY26Q1 Call Transcript Highlights:

Sovereign AI progress: Japan, South Korea, India, Canada, France, UK, Germany, Italy, Spain, Sweden, among others, are now building national AI factories to empower startups, industry, and society.

Q1 repurchases $14.1B (nearly doubled sequentially), dividends $244M. $21B remaining on authorization. Expect subsequent large buyback announcement ($60-100B).

Purchase commitments and obligations for inventory and manufacturing capacity were $29.8 billion (QoQ-3%) . Prepaid supply agreements were $4.2 billion (QoQ-18%) . DIS of 59 (QoQ-27) .

By billing location this quarter: U.S. revenue share 47%, Singapore 20% (99% of H100/H200/Blackwell data center revenue came from U.S. customers), Taiwan 16%, Mainland China 13%; top customer 16%, second 14%, third 13%, fourth 11%.

Overall, on this earnings call Huang again emphasized that enterprise AI and sovereign AI are just getting started, and GB200 is just beginning to ramp.

Previously noted: the unexpected 10-for-1 split implies management expects annualized net income to exceed $100B. If quarterly EPS returns to $1, that implies $25B quarterly net income, a $100B run rate, likely achievable this year with Blackwell's help. A milestone moment where net income surpasses Apple to become the world's most profitable company is probable this year.

The market's core focus is now on 2026 CSP capex growth to gauge 2026 earnings.