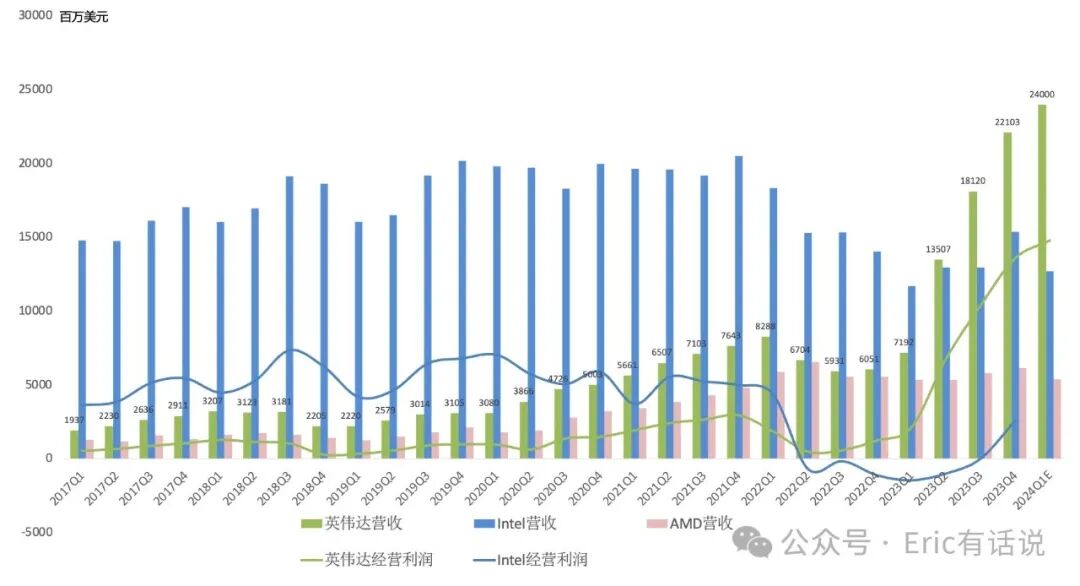

NVIDIA Q4 earnings (Nov/Dec/Jan) once again comprehensively beat expectations, with equally strong Q1 guidance (Q1 revenue guided at $24B vs. consensus $22.1B). NVIDIA has been the world's highest-revenue semiconductor company for two consecutive quarters.

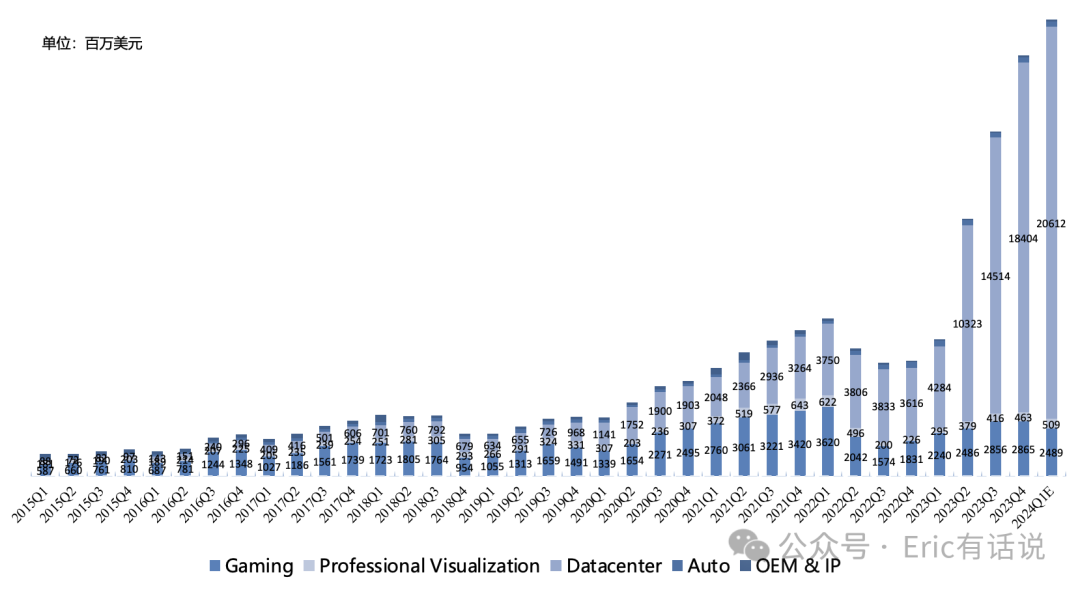

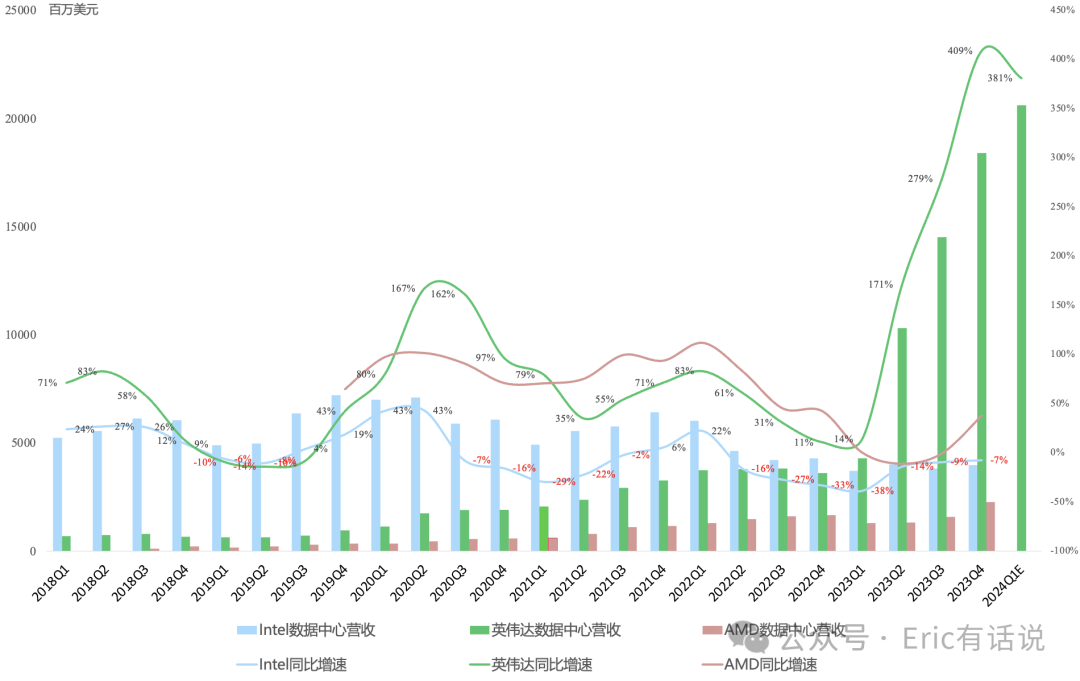

The core of this quarter's earnings remains the data center. Data center Q4 revenue was $18.404B, up 27% sequentially, accounting for 83% of NVIDIA's total revenue. Within the data center, networking revenue grew over 500% year over year again driven by compute, while compute revenue grew 488% year over year.

Given the outsized data center revenue share, NVIDIA may change its reporting segmentation to separately disclose compute and networking businesses. Notably, data center Q1 revenue is on track to exceed $20B, a scale that already surpasses Azure and approaches AWS.

Per guidance, Q1 revenue of $24B implies 234% year-over-year growth; GAAP net income of $12.5B implies 512% year-over-year growth; Non-GAAP net income of $13.5B implies 397% year-over-year growth. Management expects data center demand visibility to extend through 2025 and beyond. In the prior article "NVIDIA Q3 Earnings: Global Semiconductor Revenue Leader, Data Center Visibility Through 2025," I noted "2023 full-year Non-GAAP net income floors at $30.6B, making a $1.3-1.8T valuation look cheap." Now, 2023 full-year Non-GAAP net income reached $32.3B, and 2024 full-year Non-GAAP net income is expected to floor at $50B.

Of course, views on AI sustainability vary; skepticism and bearish calls on NVIDIA have never ceased. I believe NVIDIA's future growth may come primarily from two shifts: data center growth expanding from cloud-led to vertical industries and sovereign AI proliferating, and the product roadmap accelerating from a two-year cadence to an annual cadence.

Regarding the China market, I maintain my prior view: "Given US-China dynamics, AI decoupling is inevitable; better short pain than long pain, especially since the short-term pain appears minimal for now, which is the most positive news."

FY24 Q4 call highlights:

Data center compute revenue grew 488% year over year and 27% sequentially; strong demand from verticals including automotive, financial services, and healthcare; CSPs account for over half of data center revenue, including internal and external demand; this quarter's data center growth was driven primarily by Hopper training and inference products and InfiniBand products; China data center revenue share declined sharply to mid-single digits, expected to remain unchanged in Q1; compliant products have shipped; Hopper capacity is increasing but demand remains very strong; next-generation Blackwell demand far exceeds supply; nearly 40% of data center revenue this fiscal year is AI inference-related, as recommendation systems previously based on CPUs have migrated to GPUs; nearly 80 global automakers use NVIDIA AI cards for model training; automotive data center revenue exceeded $1B this fiscal year.

Data center networking revenue grew 217% year over year and 28% sequentially; annualized run rate exceeds $13B; InfiniBand revenue grew over 5x year over year; Spectrum-X Q1 ramp for traditional Ethernet users (challenging Broadcom); Q1 data center expected to continue sequential growth; data center demand visibility extends through 2025 and beyond; data center install base expected to double over the next 5 years, with an annual market size exceeding $100B.

Software revenue continues to grow, annualized run rate exceeding $1B, primarily DGX Cloud + AI Enterprise; AI Enterprise at $4,500/GPU/year; DGX Cloud now available on AWS, Azure, Google Cloud, and Oracle Cloud, bringing the CUDA ecosystem to public clouds.

Q4 repurchases of $2.66B, dividends of $99M; remaining repurchase authorization of $22.5B.

On the prior Q3 earnings call, Jensen Huang outlined three future growth engines: CPU, networking, and software. The sovereign AI concept introduced last quarter has now begun deployment in Japan, Canada, France, and other countries. On this Q4 call, Jensen Huang stated that, like the AC power plants of the industrial revolution, NVIDIA AI supercomputers are essentially the AI factories of this industrial revolution.

Short-term stock volatility is inevitable; a level-headed approach is warranted. This year's March GTC will be the first in-person event in five years, with anticipation for the B100 launch. Once more, Jensen Huang's words: "We started the AI journey with the hyperscale cloud providers and consumer internet companies. And now, every industry is on board, from automotive to healthcare to financial services, to industrial to telecom, media and entertainment." — Jensen Huang