Amid pervasive 'AI bubble' narratives, global AI chip leader NVIDIA responded with a widely watched FY26 Q3 earnings release. NVIDIA's FY26 Q3 (Aug/Sep/Oct 2025) again beat expectations, with Q4 guidance significantly above consensus. As the highest-revenue, highest-net-income company in global semiconductor history, NVIDIA continues to break industry ceilings. This quarter it ranked second globally in net income; next quarter it is poised to claim the top spot.

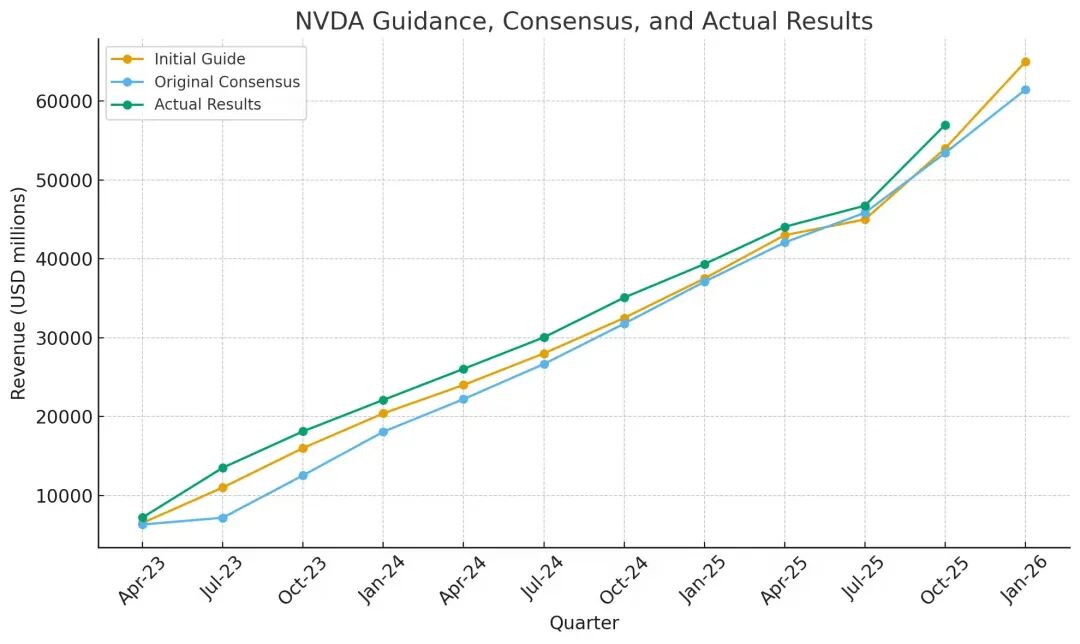

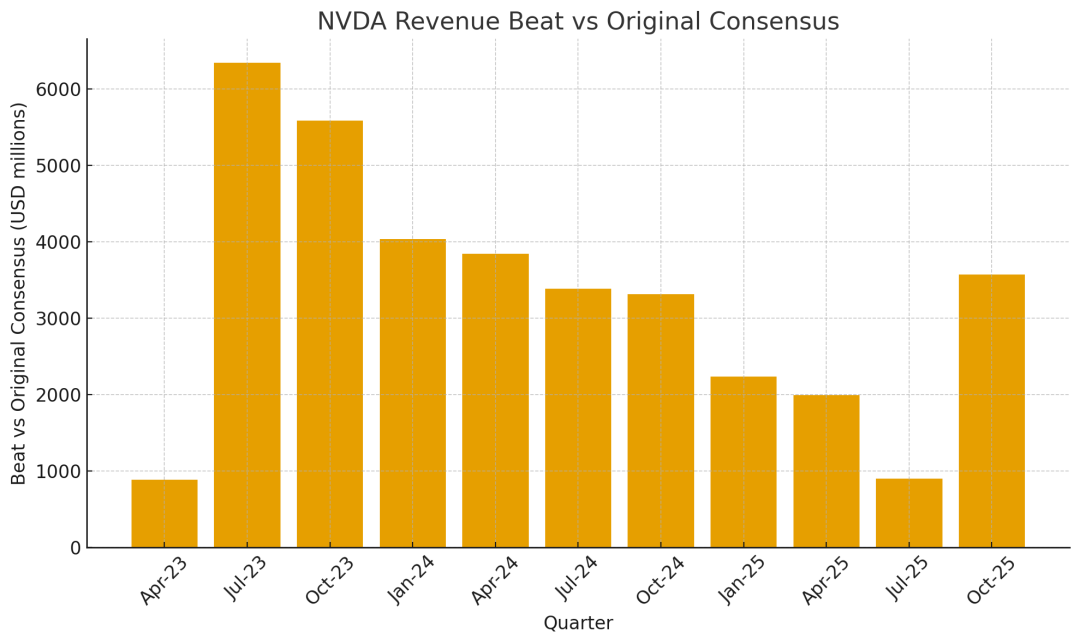

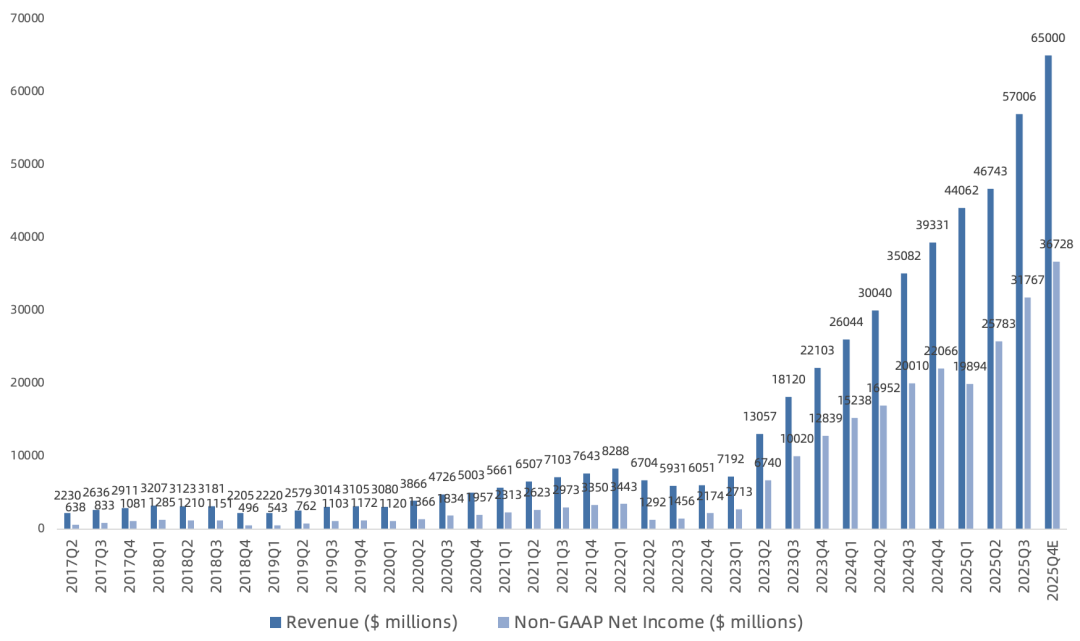

Revenue was $57.0B, up 63% year over year and 22% sequentially, significantly above the $54.95B consensus and the prior $54B guidance.

GAAP gross margin was 73.4%, down 1.2 percentage points year over year but up 1.6 points sequentially, in line with the 73.4% consensus and the prior 73.3% guidance.

Non-GAAP gross margin was 73.6%, down 1.4 percentage points year over year but up 0.9 points sequentially, in line with the 73.6% consensus and the prior 73.5% guidance.

GAAP net income was $31.91B, up 65% year over year and 21% sequentially, significantly above the $29.38B consensus and the prior $28.54B guidance.

Non-GAAP net income was $31.78B, up 59% year over year and 23% sequentially, above the $30.74B consensus and the prior $30.05B guidance.

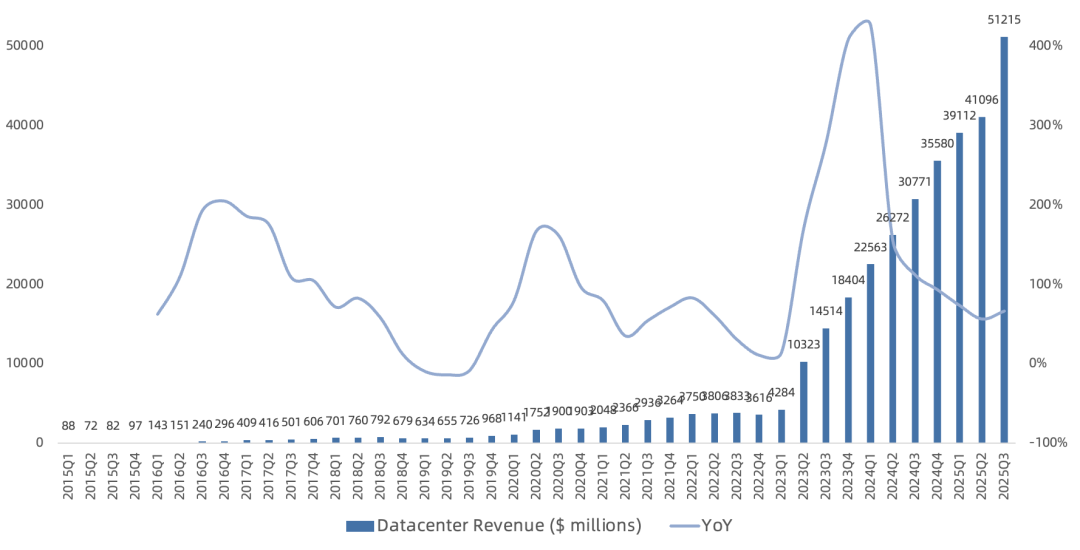

Data Center Q3 revenue was $51.2B, up 66% year over year and 25% sequentially, representing 90% of total NVIDIA revenue, driven primarily by the Blackwell Ultra ramp.

Inside Data Center:

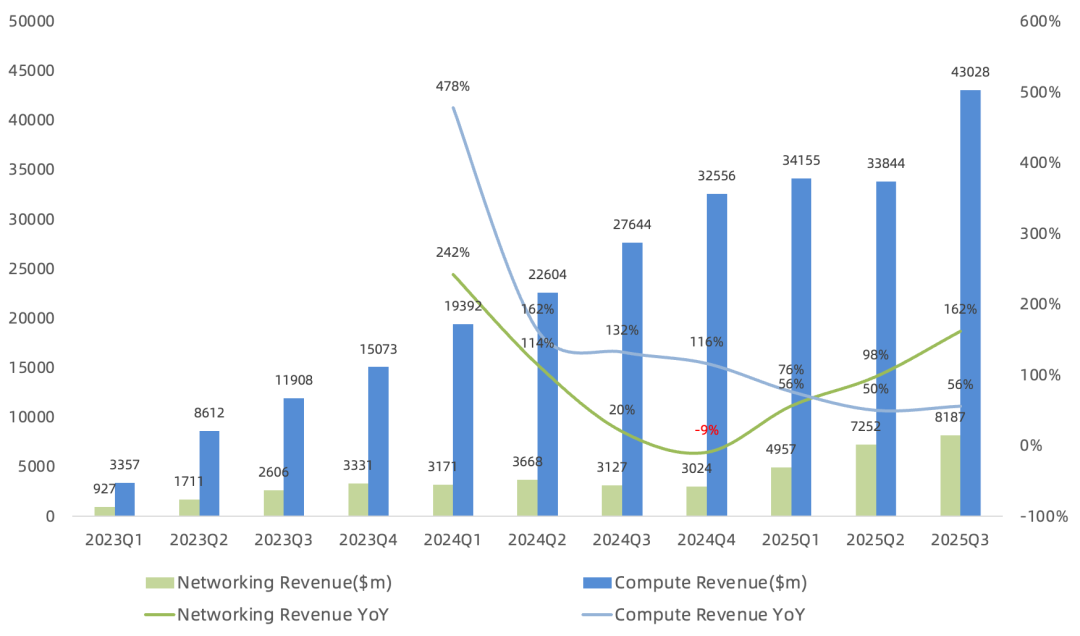

Compute revenue was $43.0B, up 56% year over year and 27% sequentially. GB300 shipments exceeded GB200, contributing roughly two-thirds of total Blackwell platform revenue (Blackwell revenue $41.0B, Blackwell Ultra $27.3B, other $13.7B). Legacy Blackwell demand remains strong. Hopper, in its 13th quarter since launch, generated ~$2.0B this quarter. H20 revenue was ~$50M.

Networking revenue was $8.2B, up 162% year over year and 13% sequentially, making it the largest networking business globally. Growth was driven by high double-digit gains in NVLink scale-up, Spectrum-X Ethernet, and Quantum-X InfiniBand. Most AI deployments now use NVIDIA switches; Ethernet GPU attach rates are roughly on par with InfiniBand. Meta, Microsoft, Oracle, and xAI are building GW-scale AI factories with Spectrum-X Ethernet switches. NVIDIA states it is the only company with AI scale-up, scale-out, and scale-across platforms. Customer interest in NVLink Fusion continues to grow, with partnerships announced with Fujitsu, Intel, and Arm.

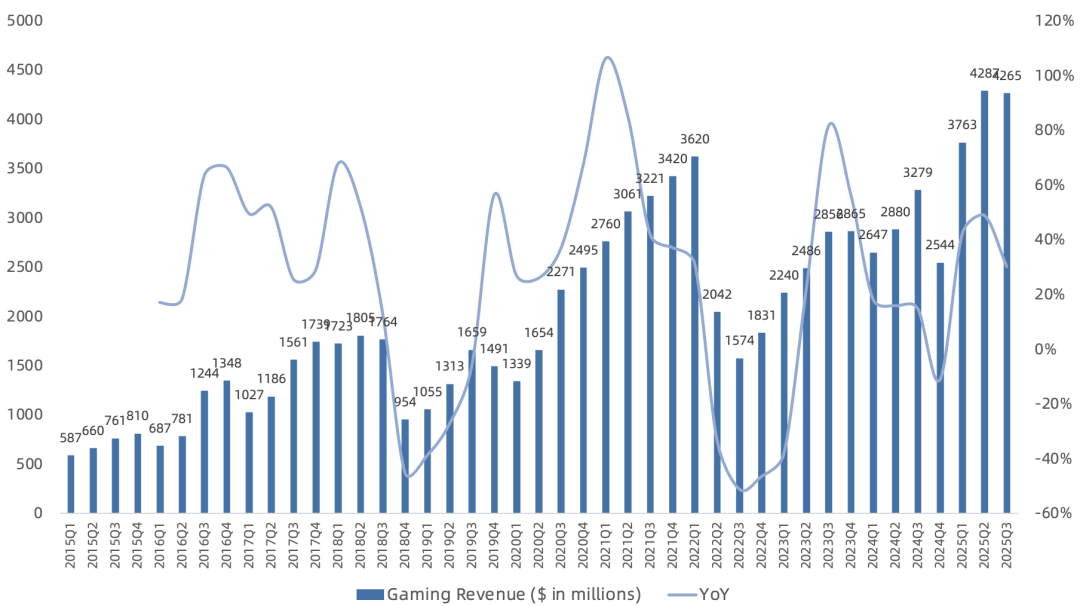

Gaming Q3 revenue was $4.3B, up 30% year over year but down 1% sequentially. Blackwell product demand remains strong; end-market sell-through remains robust. Channel inventory is at normal levels ahead of the holiday season, causing the sequential dip. Steam recently surpassed 42M concurrent users.

Guidance calls for Q4 revenue of $65.0B, up 65% year over year, excluding H20, benefiting from Blackwell Ultra volume. Q4 GAAP gross margin guidance is 74.8%, Non-GAAP 75%, returning to the 75% level for the first time in four quarters, and expected to hold at 75% next year. GAAP net income guidance is $35.2B, up 59% year over year. Non-GAAP net income guidance is $36.7B, up 66% year over year, positioned to set a new global single-quarter net income record.

At its recent Analyst Day, AMD gave strong 3-5 year performance guidance but only 55-58% gross margin, not much above its current level (Q4 2025 guidance 54.5%). NVIDIA, by contrast, expects to maintain 75% gross margin next year, preserving its lead over AMD.

Views on AI sustainability naturally differ. Skepticism, bearish calls, and fabricated attacks on NVIDIA have never ceased. I maintain my prior view: NVIDIA's future growth will likely come from two shifts: data center expansion broadening from cloud-led to vertical industries and sovereign AI proliferating (DeepSeek accelerated AI democratization), and its seven-chip product matrix and roadmap moving from biennial to annual cadence. The global AI factory build-out is still early. In the past quarter alone, AI factory and infrastructure projects totaling 5M GPUs were announced, spanning every market: CSPs, sovereign nations, model companies, enterprises, and supercomputing centers.

On China, I maintain my prior view: 'Given US-China dynamics, AI decoupling is inevitable; better short pain than long pain.' Although Jensen remains reluctant to abandon the $50B market, at least it won't weigh on sentiment in the near term.

FY26 Q3 Call Highlights:

AI demand continues to exceed expectations. Cloud GPUs are sold out, whether current or prior-gen AI products, including Blackwell, Hopper, and Ampere, all fully utilized. A100s shipped six years ago are still running at full capacity today.

The $500B data center revenue guide for Blackwell and Rubin from early 2025 through end-2026 has upside potential. Recent large deals, including Anthropic, are not yet factored in.

To support Blackwell Ultra capacity ramp, inventory rose sequentially from $15B in Q2 to $19.8B. Supply commitments grew 63% sequentially in Q3, preparing for significant future growth.

Global 2030 AI capex is estimated at $3-4T/year, with CSP demand accounting for half and large-model compute the other half. From Ampere to Hopper to Blackwell to future Rubin, the share of data center capex keeps rising. Hopper may be 20-25%, Blackwell (especially Grace Blackwell) 30%, and Rubin higher still.

Strategic investments in Anthropic, Mistral, OpenAI, Reflection, Thinking Machines, and others represent partnerships to develop the CUDA AI ecosystem and ensure every model runs optimally on NVIDIA platforms. The company will continue strategic investments while maintaining cash flow discipline.

Q3 repurchased $12.5B, paid $243M in dividends. $62.2B remains authorized. Repurchase pace will continue to increase.

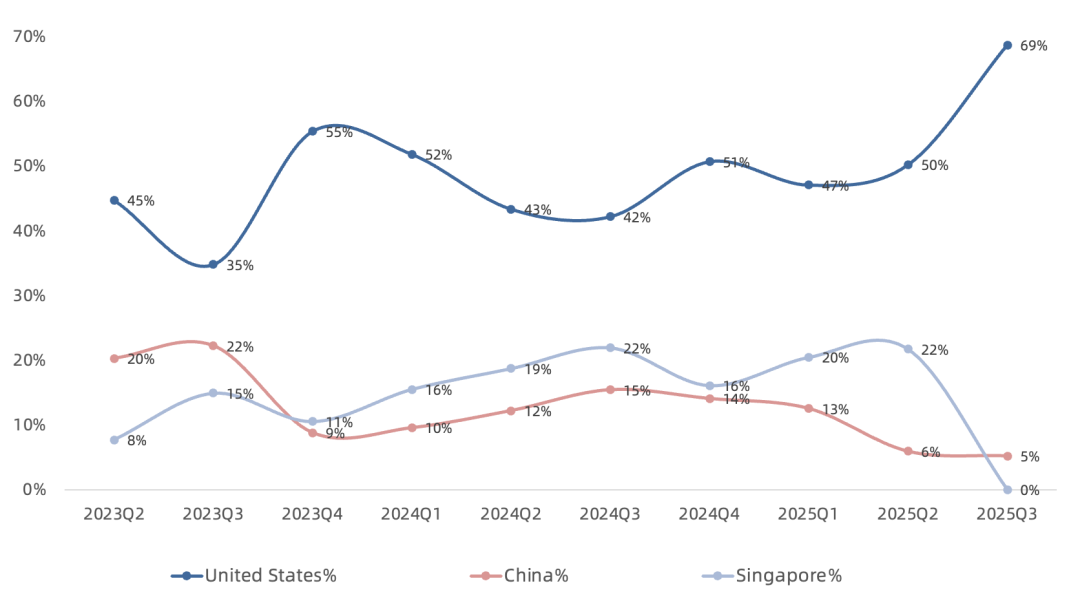

By headquarters geography this quarter: US 69% of revenue, Taiwan 24% (86% of downstream customers are US and Europe), Mainland China 5%, Singapore 0%. Top customer 22%, second 15%, third 13%, fourth 11%, all shares declining. Customer base is increasingly diversified, no longer dictated by a handful of hyperscalers.

Rubin platform's seven chips are on track to begin shipping in Q3 next year. The long useful life of CUDA GPUs is a significant TCO advantage versus other AI chips. CUDA compatibility and the massive installed base extend NVIDIA AI chip lifetimes far beyond initial estimates.

Previously noted: the unexpected 10-for-1 split implies management expects annualized net income to exceed $100B. If quarterly EPS returns to $1, that implies $25B quarterly net income, a $100B run rate, likely achievable this year with Blackwell's help. A milestone moment where net income surpasses Apple to become the world's most profitable company is probable this year.

Overall, NVIDIA's results provide a strong rebuttal to the AI bubble argument and address investor concerns about older-GPU depreciation and declining gross margin, reinforcing the U.S. AI investment narrative. Current guidance implies full-year non-GAAP net income of $114.2B, with net income potentially exceeding $200B next year.

During the earnings call, Wall Street finally raised the fact that almost every major AI model has been trained on older Hopper GPUs or earlier TPUs. Even the GPT-5 family was trained on H100 and H200. The market has not yet seen a major model trained on Blackwell, whose specifications remain promising as scaling laws continue to hold.