NVIDIA Q1 slightly beat, but Q2 guidance is perhaps the most stunning in recent tech years (Q2 revenue guide $11B vs consensus $7.2B), Wall Street up all night revising models. I previously optimistically predicted Q4 single-quarter revenue could hit $10B; didn't expect AI revenue to materialize this fast.

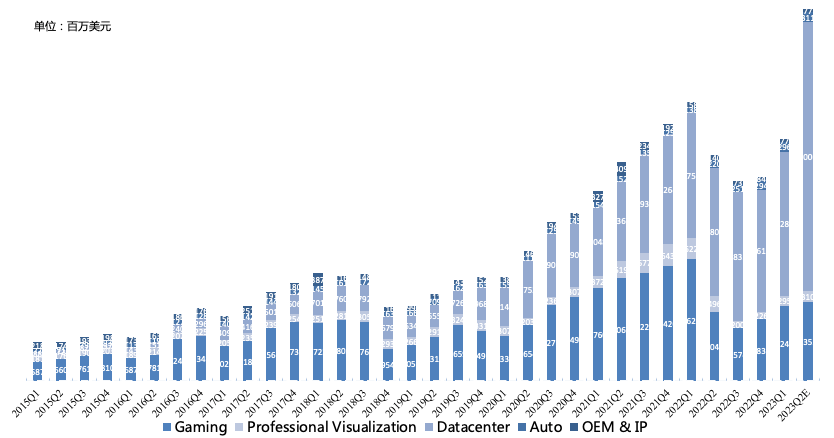

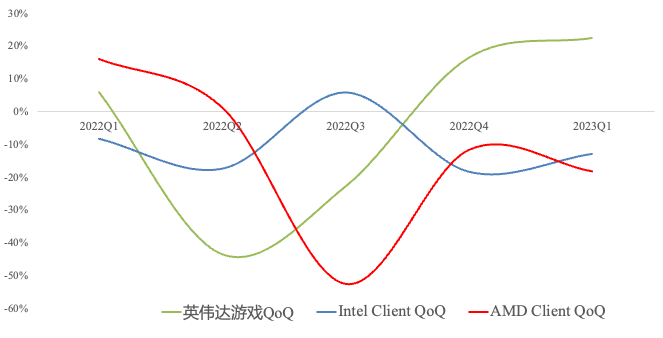

On Q1, two points: gaming rebounded for two consecutive quarters after bottoming in Q3 last year, now near the 2020 Q3-2022 Q2 mining peak range floor; from Q2 last year's blowup (reflections on NVIDIA Q2 blowup) to now, recovery speed in semiconductor ToC is nearly unmatched. And this is still the semiconductor cycle bottom; Intel and AMD PC businesses haven't rebounded yet.

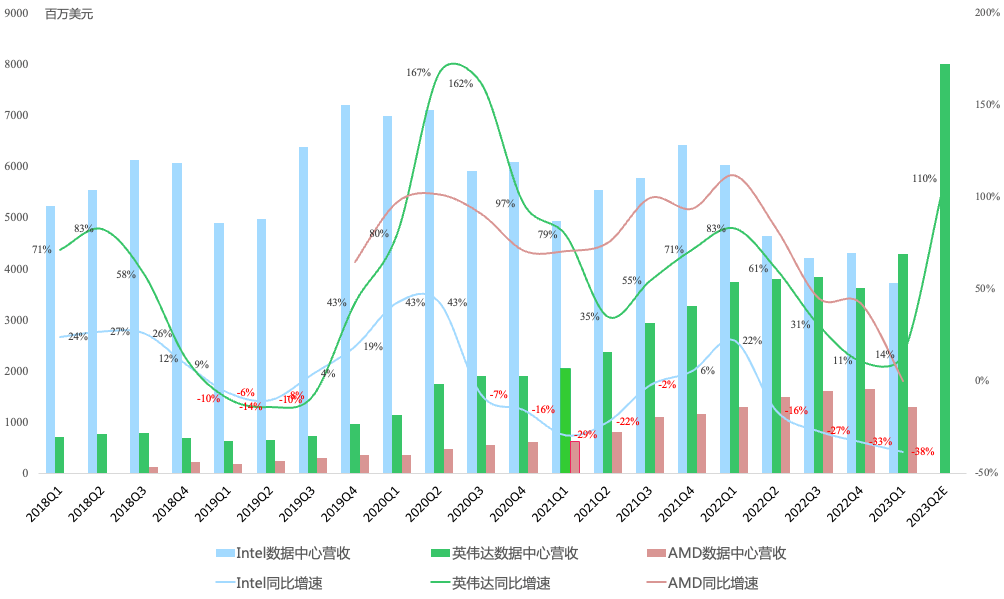

Second, data center hit a milestone: data center revenue surpassed Intel for the first time. This marks the formal transformation of data center; traditional CPU influence formally yields to GPU.

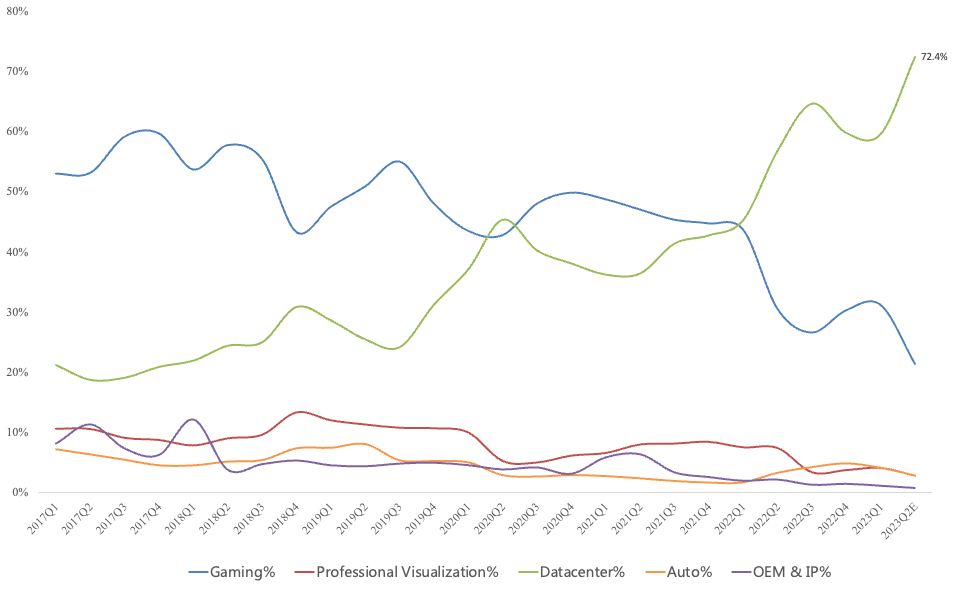

Q2 guidance is the bombshell. Most of the massive sequential revenue growth comes from data center, implying Q2 data center revenue could hit $8B, exceeding Intel+AMD data center combined — isn't that creating another NVIDIA? Who still calls NVIDIA a gaming GPU company? Q2 data center share can exceed 70%.

Per guidance, Q2 revenue is $11B, up 64% year over year; GAAP net income $4.2B, up 546% year over year; non-GAAP net income $5.1B, up 292% year over year. Management expects H2 data center product supply to grow significantly vs. H1 sequentially. Linearly extrapolating Q2 results, FY2023 full-year non-GAAP net income is at least $18B. Applying NVIDIA's long-term 50x–70x P/E midpoint yields a market cap of $900B–$1.26T.

Of course, AI sustainability remains to be seen; views differ. Jensen emphasizes installed data center base of $1T and growing, but mostly CPU-based; this will convert to AI data centers, GPU necessity may eventually rival CPU, but penetration is still very low.

FY24 Q1 Call Highlights:

Gaming sequential growth driven by RTX 40 series strength, RTX 40 notebook and desktop growth; GFN library >1,600 titles; DLSS games/apps >300.

Data center CSP demand for H100 very strong; internet customers like Meta also strong H100 demand; auto/financial/healthcare/telecom vertical AI demand strong; DGX on-prem or DGX Cloud both available; Grace CPU sampling; H2 data center capacity up significantly, order visibility multiple quarters, expect H2 supply up significantly sequentially vs H1.

Visualization workstations recovering, desktop and mobile demand warming up, inventory digestion complete; Omniverse Cloud available in H2.

Networking demand strong from CSPs and enterprises; BlueField-3 in production; InfiniBand revenue record; new roadmap at Computex.

Next 6 years auto pipeline $14B backlog (Qualcomm $30B); this quarter auto growth driven by Orin ramp; China NEV production/sales below expectations; 2024 BYD next-gen Dynasty and Ocean series to use Orin.

I wrote in two 2021 pieces "Earnings Review | AI King NVIDIA: Microsoft of Semiconductors" and "Earnings Review | New Semiconductor King Blows Out, Another NVIDIA in 5 Years?": envisioning 2023 as the year NVIDIA formally joins Apple and Microsoft. Hope it comes true.

I'm still very curious about H2 Grace CPU performance, whether it can break Intel/AMD's data center CPU duopoly.