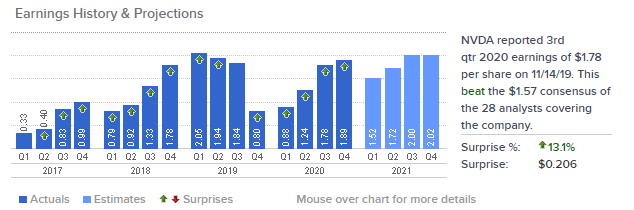

NVIDIA's FY2020 Q4 (referred to as calendar 2019 below) earnings arrived late; as expected, EPS beat again. Overall Q4 revenue met expectations, and the stock jumped 5% after hours to a 52-week high.

Source: CNBC

This morale-boosting report swept away the gloom from the 2018 crypto crash.

Q4 Earnings Overview

Earnings Summary:

Q4 revenue $3.105B, up 40.8% year over year, up 3% sequentially, slightly above prior-quarter guidance;

GAAP net income $950M, up 67.5% year over year, up 5.7% sequentially;

Non-GAAP net income $1.172B, up 136.3% year over year, up 6.3% sequentially;

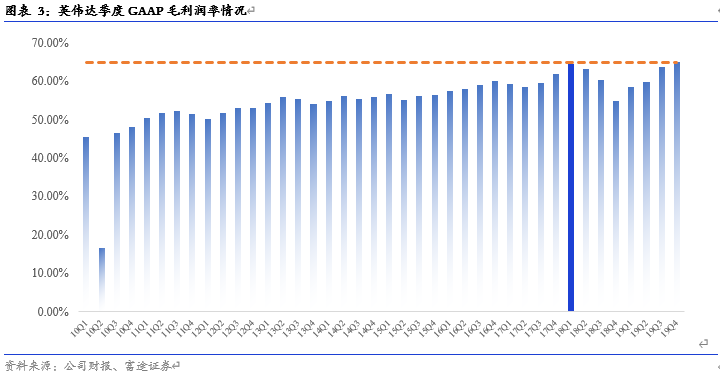

GAAP gross margin 64.9%, up 10.2 pct year over year, up 1.3 pct sequentially.

Data Sources:

Company filing

Overall, revenue slightly beat expectations while profits beat by a wide margin. After a cold start to 2019, NVIDIA fully warmed up in the second half. For the first time in a full year, NVIDIA posted back-to-back quarters of revenue above $3B.

Gross margin and cash flow hit records; Huang's execution is masterful

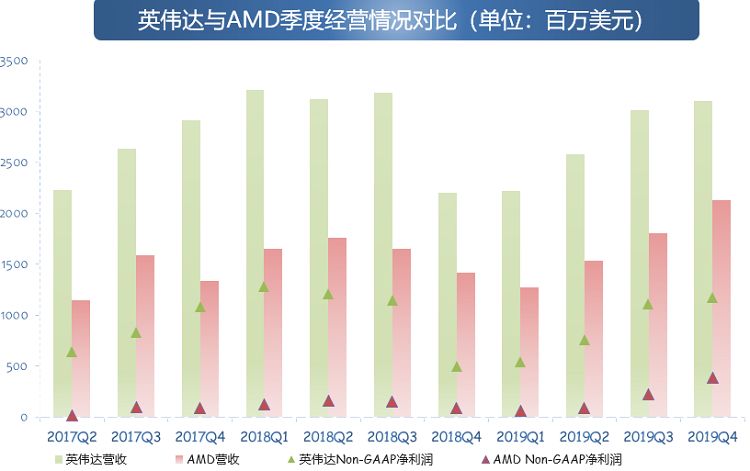

2018 Q4 was NVIDIA's darkest hour: high inventory from the crypto bust drove revenue and gross margin to multi-year lows. AMD narrowed the revenue gap to $800M and the non-GAAP net income gap to $400M.

But 2019 Q4 saw NVIDIA announce its return with 40% year-over-year growth. Single-quarter revenue set a Q4 record, and gross margin hit an all-time NVIDIA high of 64.9%.

Source:

Our research report screenshot

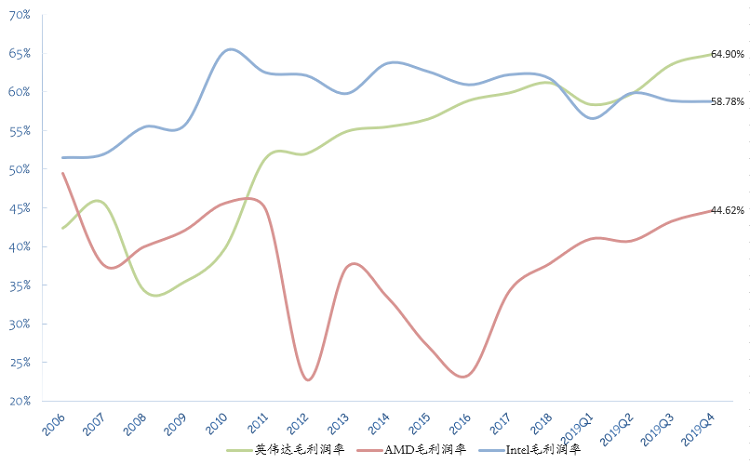

Compared with Intel and AMD, NVIDIA's gross margin now leads by a wide margin. The sharp margin expansion reflects higher gaming GPU ASPs, improved raw-material costs, and a broader product portfolio. Given NVIDIA's software-centric strategy, gross margin has further upside.

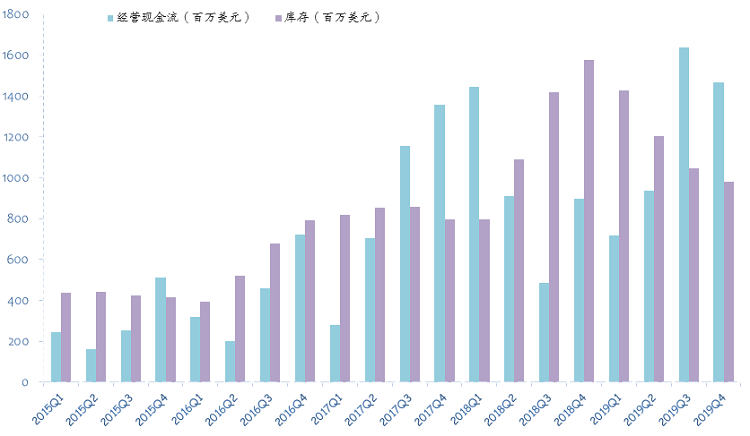

To see how sharp Huang's execution is, just look at inventory.

As early as the Q3 report, NVIDIA showed raw-material inventory fell $358M in the first three quarters of 2019, down nearly 58%. Because RTX Super and GTX 16 series used existing core designs — mainly changing memory bandwidth, bus width, and shader counts — raw-material consumption dropped sharply. Full-year 2019 raw-material data is not yet available as the 10-K has not been filed with the SEC.

Data source: Company filing

The most direct payoff from destocking is the change in operating cash flow. Thanks to inventory management, NVIDIA generated $4.761B of operating cash flow in 2019, a record high; free cash flow also hit a record $4.272B.

Turing inventory is now largely cleared; perhaps the next-gen Ampere architecture will arrive soon.

Q4 Segment Overview

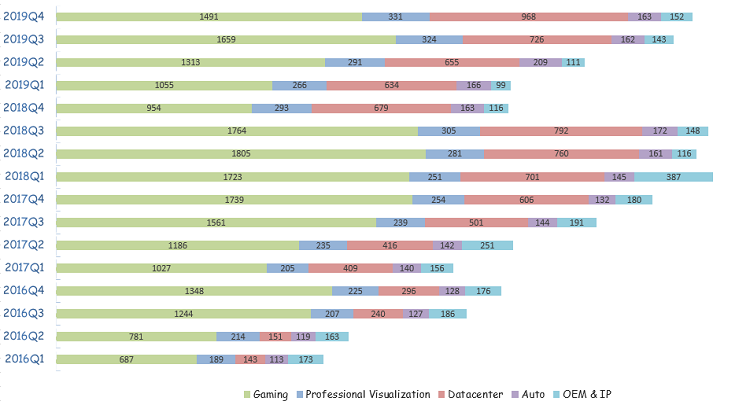

By segment, this quarter marked the first time in a year that all four major businesses grew year over year simultaneously.

Data source: Company filing, units in millions of dollars

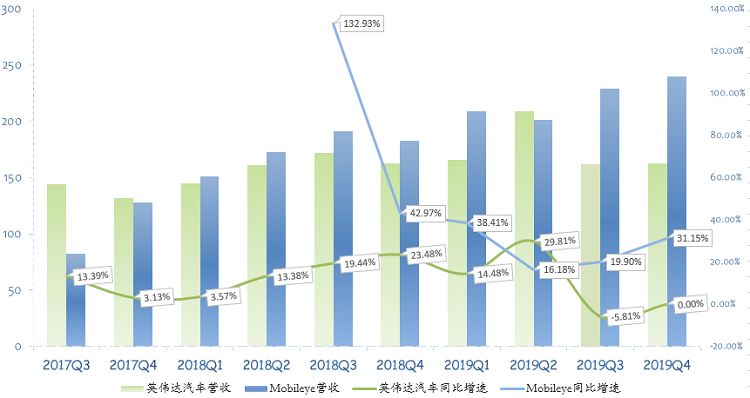

First, the auto business, where growth nearly stalled. NVIDIA signed a one-time revenue-recognition auto deal with Toyota and others in Q2, making that quarter a record.

But Q3 and Q4 auto revenue essentially flatlined, far behind Intel's Mobileye. No matter how powerful the Orin autonomous-driving chip is, it needs automotive industry adoption.

With the global auto market clearly trending down and L3+ autonomous deployment stalled, we think NVIDIA's auto business is unlikely to surprise in the near term; it remains focused on ecosystem building. Stockpile grain, delay coronation.

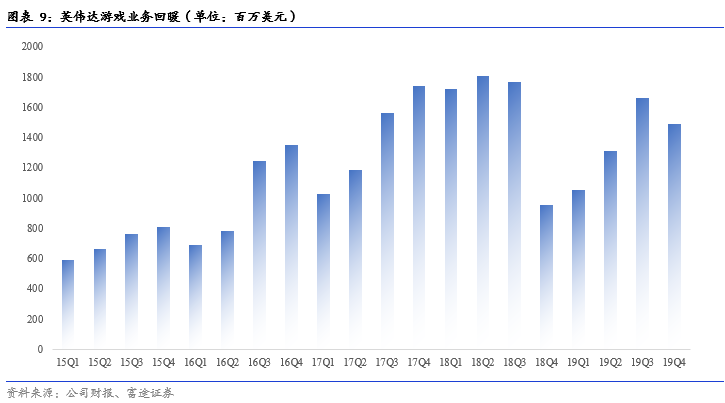

Gaming laptops stay strong; cloud gaming still has room to imagine

NVIDIA Q4 gaming revenue was $1.491B, up 56.3% year over year, about $250M shy of the Q4 record, down 10.1% sequentially. Full-year 2019 gaming revenue was $5.518B, the second-highest ever, trailing only 2018 when the GTX 1060 dominated crypto.

Overall gaming GPU business: RTX Super exceeded expectations; GTX Super played a clear fill-in role.

This quarter NVIDIA cut prices repeatedly and launched several GTX 16-series mid-range cards with good effect. Per Steam, the recently launched GTX 1660/1650 share rose quickly; Super series also performed well. The top 10 GPUs on Steam are all NVIDIA, including RTX 2060.

The strongest performer remains gaming laptops. Gaming laptops have logged eight consecutive quarters of double-digit year-over-year growth. As we've emphasized in external research, 'gaming laptops offer high certainty; Max-Q writes the future of notebooks.' Max-Q balances performance and thin-and-light, and the future trend is unifying performance with portability.

On consoles, Switch was steady. Tegra revenue was $331M, up 47.1% year over year, down 26% sequentially. With auto revenue flat sequentially, the Tegra sequential decline largely reflects Switch. This aligns with management's Q3 call commentary on Switch.

On cloud gaming, GeForce Now launched overseas at $4.99/month, well below Google Stadia. The company claims 80% of users access GeForce Now on Mac or Android devices.

The service does not support China; NVIDIA's cloud gaming strategy in China centers on GPU technology cooperation with Tencent Cloud.

Going forward, we still see gaming laptops as the primary gaming growth driver, and ray tracing as the key graphics technology direction. We also look forward to the RTX 3000 series.

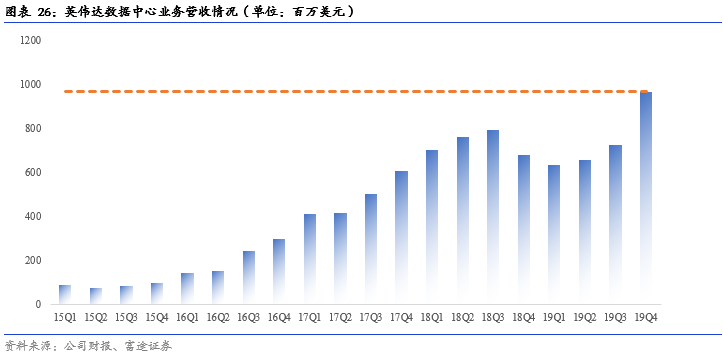

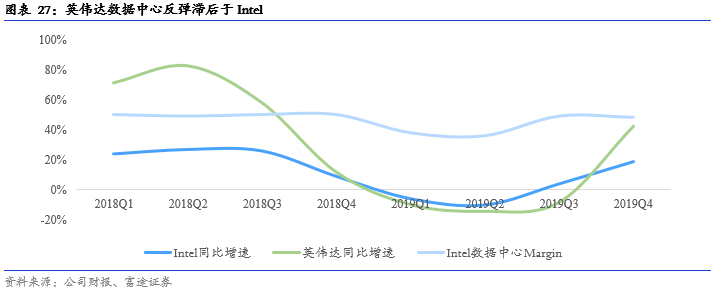

Data center flies high; AI revolution far from over

NVIDIA Q4 data center revenue was $968M, beating all expectations. Up 42.56% year over year, up 33.3% sequentially! Single-quarter record. Full-year 2019 data center revenue was $2.983B, also a record.

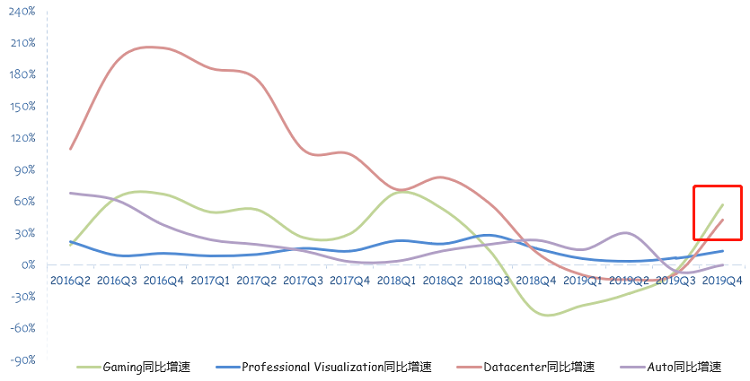

Notably, Q4 data center share of revenue hit 31%, a record. Since 2015, data center revenue has compounded at 54.5% annually! From under $340M in 2015 to $2.983B now — simply staggering.

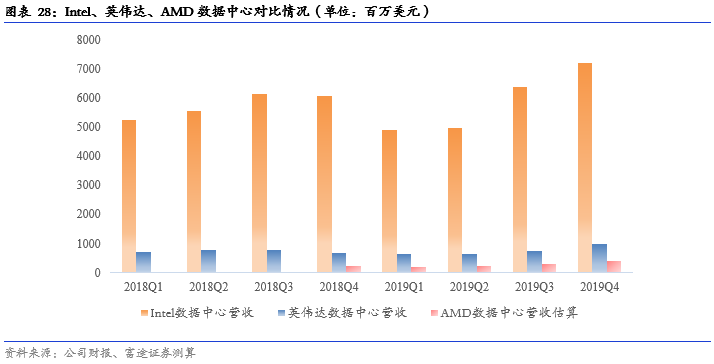

We believe NVIDIA's position in the GPU data center market is solid. By revenue scale, NVIDIA's data center business still trails Intel significantly. Our estimates put AMD's data center quarterly revenue near $400M, but AMD's GPU data center business remains weak.

Source: Our research report screenshot

Specifically, full-year data center strength came from a rebound in large-scale computing and more verticals adopting AI. NVIDIA T4 and V100 GPU shipments and revenue set records again in Q4. T4, used mainly for inference, saw shipments jump 4x year over year!

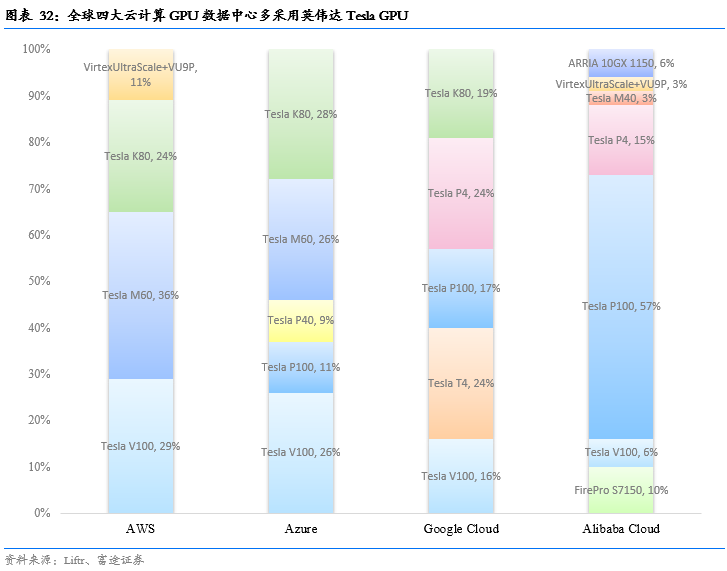

Large-scale computing customers are the major cloud providers. For example, Azure and AWS deployed large volumes of NVIDIA V100 GPUs and DGX servers in Q4. Vertical customers beyond internet firms include food-delivery and traditional retail companies, using algorithmic recommendation and conversational AI.

We think AMD's main data center rival is still Intel, while NVIDIA retains a deep software-and-hardware moat in data center GPUs. Overall, the data center TAM is huge; red, green, and blue vendors are in a win-win, not a zero-sum game.

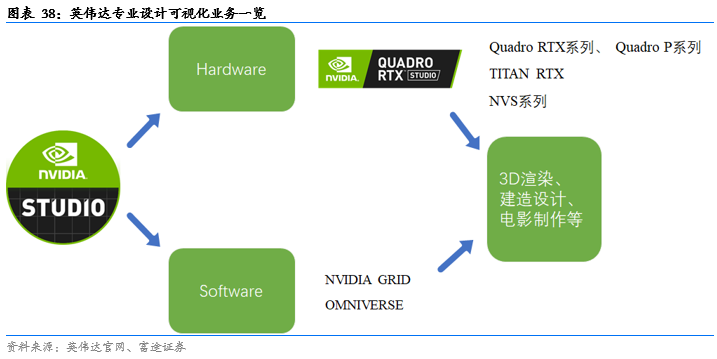

Overlooked professional visualization business has bright prospects

Another business to watch is professional design and visualization. We previously argued 'professional design and visualization market outlook bright; GPU adds color to creativity.'

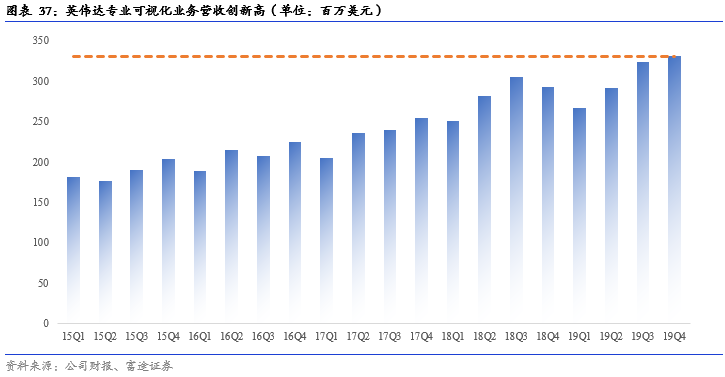

NVIDIA Q4 professional visualization revenue was $331M, up 12.97% year over year, up 2% sequentially, setting another quarterly record.

This business is primarily a hardware-plus-software platform. On hardware, the flagship is the Turing-based Quadro RTX GPU, which supports ray tracing for more stunning rendering; its ASP is roughly 80% above the prior generation.

Professional visualization is the only NVIDIA segment with 16 consecutive quarters of revenue growth since 2016. In the 5G era, we are bullish on GPU adoption in professional rendering, video creation, and engineering design. Professional visualization could become NVIDIA's next stable earnings driver after data center.

Conclusion

Overall, NVIDIA delivered a satisfying report card over the past year. Gaming rebounded strongly, data center fully recovered, and overall performance returned to 2018 peaks.

NVIDIA guided FY2021 Q1 revenue around $3B, lowered by $100M due to the pandemic but still at a high level, implying roughly 35% year-over-year growth. GAAP gross margin guidance reached an unprecedented 65%!

By segment, Q1 gaming expects seasonal declines in notebook GPUs and Switch, down about 5% sequentially. But data center should remain strong. On the Mellanox acquisition, only China antitrust approval remains; expected to close in the first half of this year.

In short, the once-and-future AI big brother NVIDIA is back.

This is an era of Intel, AMD, and NVIDIA winning together, not one rising at another's expense.