Early this morning after hours, NVIDIA reported Q2 earnings: Mellanox-inclusive data center revenue grew 168% year over year, surpassing the traditional gaming business. The company also gave very strong Q3 guidance, with single-quarter revenue set to hit another record high.

After the crypto crash, NVIDIA entered its darkest hour in early 2019. Since then, riding the data center explosion and strong PC growth, it seized the era's opportunity. This quarter NVIDIA formally shed its "gaming company" label; the AI king title is well deserved.

Q2 earnings: focus on Non-GAAP

NVIDIA Q2 Earnings Summary:

Revenue $3.866B, up 50% year over year and 26% sequentially, a record high.

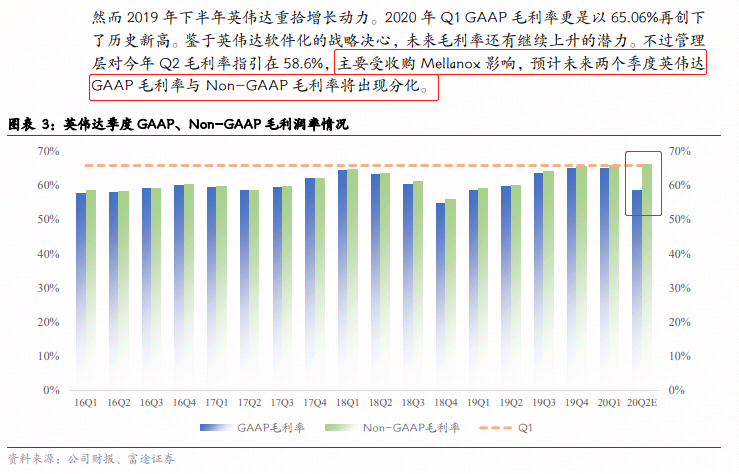

GAAP gross margin 58.8%, down 0.95 ppt year over year and 6.26 ppt sequentially, a one-year low.

Non-GAAP gross margin 66%, up 1.4 ppt year over year and down 0.2 ppt sequentially, near a record high.

GAAP net income $622M, up 13% year over year and down 32% sequentially, a one-year low.

Non-GAAP net income $1.366B, up 79% year over year and 22% sequentially, a record high.

The gap between GAAP and Non-GAAP is wide this quarter, primarily due to the Mellanox acquisition.

Per the filing, $245M of Mellanox acquisition-related costs were booked to COGS, pressuring gross margin. On the profit side, beyond the gross margin hit, a large portion stemmed from the humane advance wage payments during the pandemic. NVIDIA's Q2 operating expenses were $627M, up 136% year over year.

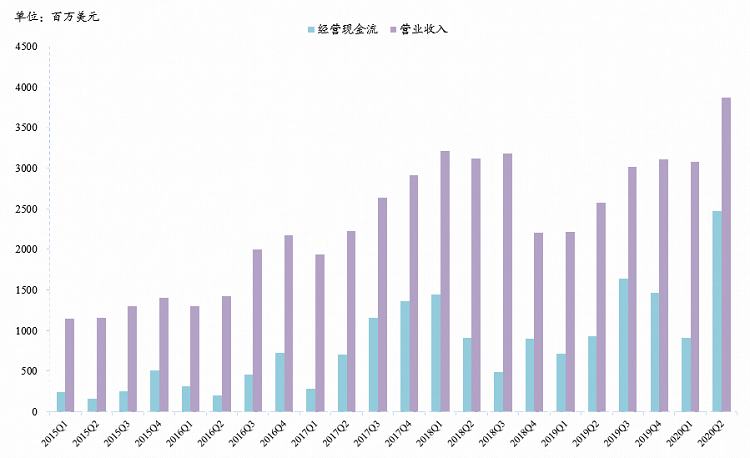

By contrast, record-high operating cash flow better reflects the quarter's strong performance.

Gaming business to explode in Q3! Auto and visualization hit hard by pandemic

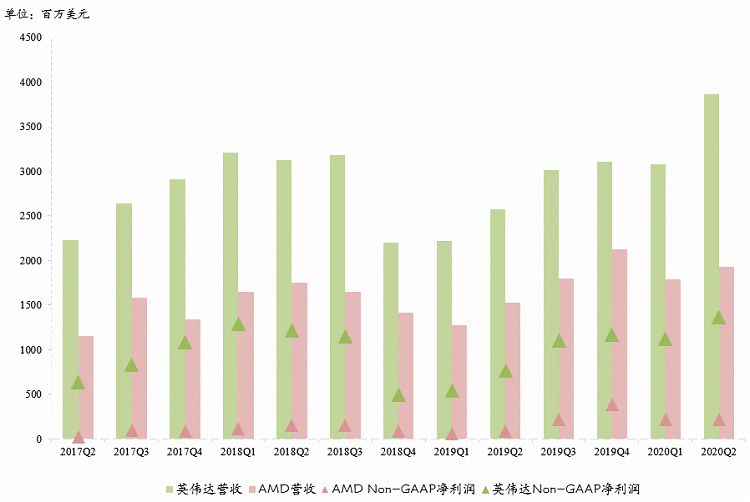

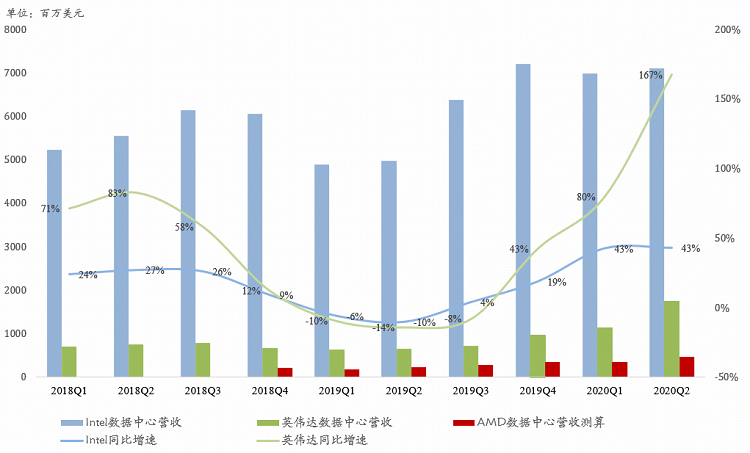

This quarter NVIDIA decisively widened its lead over AMD, on both revenue and profit.

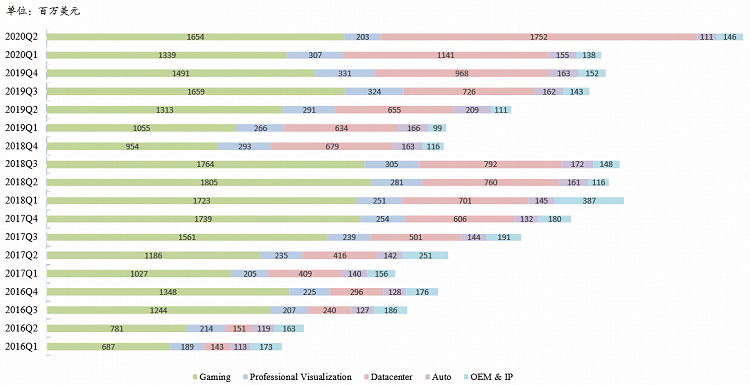

By segment: first, the pandemic-hit auto and professional visualization businesses. Auto guidance was for a 40% sequential decline; actual was -28%, roughly on par with Intel Mobileye's struggles. Professional visualization had grown year over year for 17 straight quarters; Q2 unexpectedly fell 30%, as its customers cluster in film and engineering, sectors hit hard by the pandemic — understandable.

NVIDIA's core gaming business remained king in Q2, with Switch and laptops taking off during the pandemic. Q2 gaming revenue $1.654B, up 26% year over year and 24% sequentially, far exceeding the company's single-digit sequential guidance.

Gaming benefited mainly from surging notebook and Switch shipments, detailed in our prior piece "Earnings Preview | NVIDIA Q2 Revenue May Hit Record High! Data Center Revenue Poised to Surpass Gaming." With AMD's RDNA2 desktop cards not yet launched and notebook RDNA2 products nowhere in sight, NVIDIA effectively monopolized the notebook discrete GPU market during this window.

The most shocking part of this report was gaming's Q3 guidance. Per the call, NVIDIA is extremely bullish on the PC gaming market in the second half, guiding 25% sequential growth in Q3, with single-quarter revenue breaking $2B for the first time.

NVIDIA noted that while PS5 and Xbox X use AMD SoCs, the trend of next-gen console games being ported to PC will drive a PC gaming explosion. That's good news and bad news: it means Q3 gaming will overtake data center.

NVIDIA formally becomes a data center company; Mellanox purchase was a steal

When people mention NVIDIA, most still think of a GPU vendor. But this quarter NVIDIA finally earned its rebranding moment.

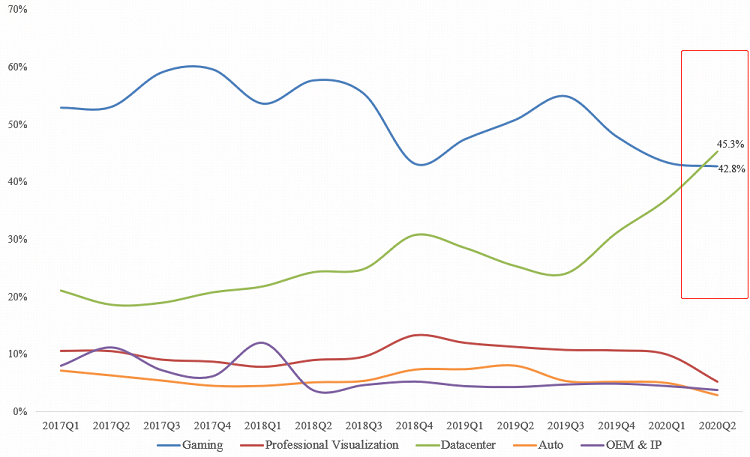

NVIDIA Q3 data center revenue $1.752B, up 168% year over year, above our 154% estimate, exceeding gaming revenue for the first time.

NVIDIA Revenue Mix by Segment

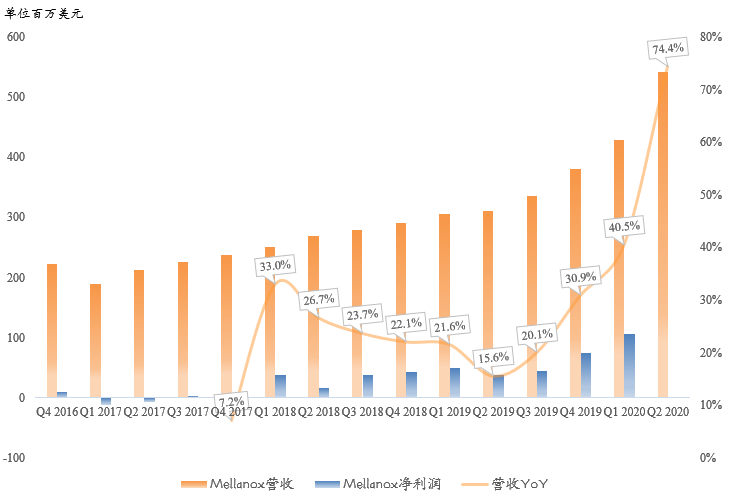

First-time consolidation of Mellanox is the top contributor. The $7.13B, year-long acquisition of Mellanox is absolutely worth it; one must admire Jensen Huang's vision. We previously noted Mellanox's customer base overlaps almost perfectly with NVIDIA's data center customers, implying powerful synergies — fully evident in Q2.

Per the filing, Mellanox contributed ~14% of company revenue and >30% of data center revenue this quarter. That implies Mellanox Q2 revenue of ~$541M, up 74.4% year over year. Ethernet shipments hit a record. In June, NVIDIA also acquired HPC software company Cumulus Networks; NVIDIA describes strong Mellanox-Cumulus synergy.

Looking at NVIDIA's acquisitions, one marvels at its eye. It also shows NVIDIA demands high profitability from targets; given Arm's poor financials, it may not pass Jensen's test.

Even excluding Mellanox, NVIDIA's data center revenue this quarter was $1.211B, up 85% year over year and 6% sequentially — also strong.

NVIDIA's new flagship A100, though early in its ramp, is shipping at a record pace. Amazon AWS, Microsoft Azure, Google Cloud, Alibaba Cloud, Tencent Cloud, and Baidu Cloud have all deployed A100. Management said A100 contributed ~25% of data center revenue in Q2, with vast remaining headroom.

For Q3 data center outlook, NVIDIA guided for single-digit sequential growth, a relatively optimistic view. Specifically, per the call, NVIDIA is bullish on hyperscale in Q3 and expects vertical industry mix to rise. GPU business led by A100 will outperform Mellanox.

NVIDIA may eventually reach a $1T market cap

NVIDIA's Q2 report was outstanding, but the market seemed more focused on the Arm deal, so the stock fell instead of rising. Arm is a bottomless pit under SoftBank; it needs a true semiconductor company to back it, but whether that company is NVIDIA is uncertain.

Everyone knows Arm's assets are good, but few understand its reality: bottomless investment, terrible profitability. More critically, this deal will almost certainly fail Chinese antitrust review.

Back to NVIDIA: Jensen Huang repeatedly emphasized on the call that NVIDIA's future is a software company; hardware is just the beginning. AI will bring profound change to software. Given NVIDIA's sky-high P/S, it already fits a software profile.

NVIDIA guides Q3 revenue of $4.4B, another record. Notably, a near-term catalyst: on September 1, NVIDIA will launch the RTX 30 series, which previews suggest will be the largest generational performance leap in NVIDIA's history.

Follow Jensen for frontier tech