When NVIDIA reported, headlines uniformly screamed 'miss.' That's the media for you. In reality, Q1 significantly exceeded both guidance and Street estimates; the only shortfall was Q2 guidance failing to extend the prior streak of sequential growth, which triggered a sharp sell-off. In today's jittery market, the slightest ripple becomes a storm.

Note that NVIDIA's Q1 fiscal quarter covers February, March, and April.

Q1 Sets New Records Again

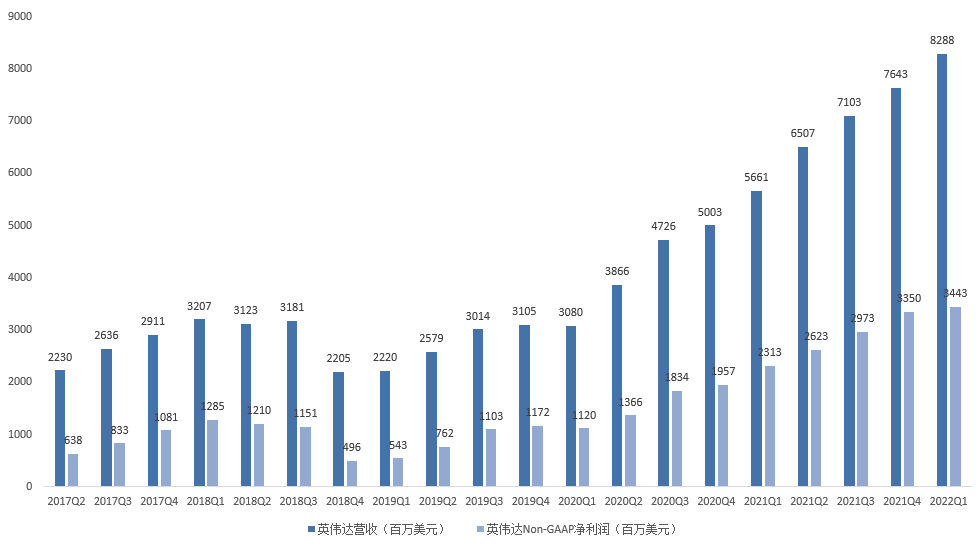

NVIDIA Q1 revenue was $8.29B, up 46.4% year over year, the eighth consecutive quarterly record.

GAAP gross margin was 65.5%, a new record. Non-GAAP gross margin was 67.1%, a new record.

GAAP net income was $1.618B, down 15% year over year, due to a $1.35B charge related to Arm. Adding that back extends the record streak to seven consecutive quarters.

Non-GAAP net income was $3.443B, up 48.9% year over year, the eighth consecutive quarterly record!

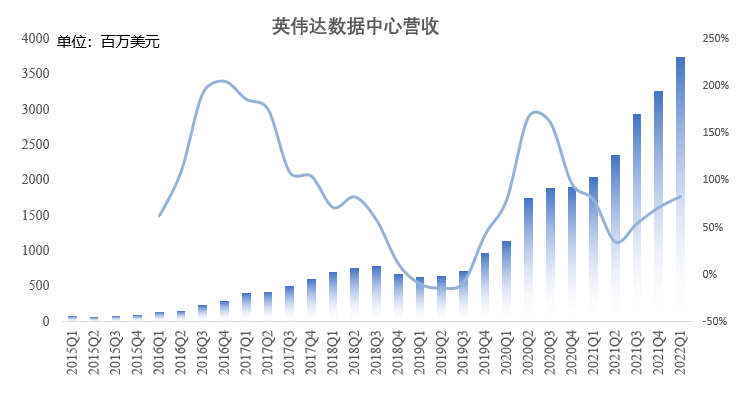

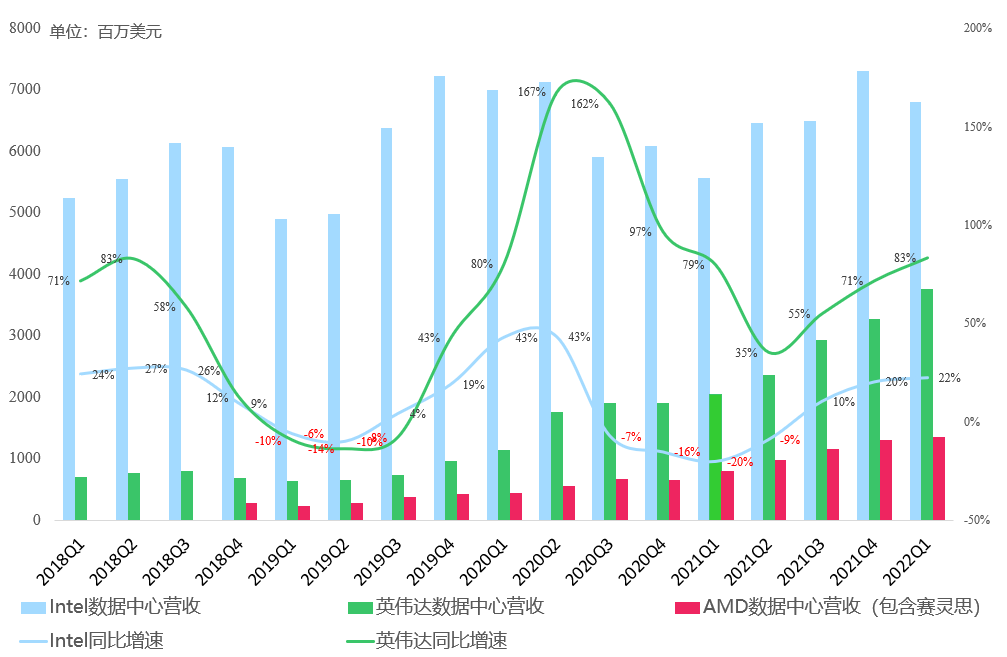

Data Center Q1 revenue was $3.75B, up 83.1% year over year and 14.9% sequentially, the tenth consecutive quarterly record, becoming NVIDIA's largest segment. Hyperscale and cloud demand was robust, with revenue doubling year over year again. Verticals continued high double-digit growth, driven by consumer internet, financial services, and telcos. The A100 maintains dominant performance in both training and inference. The Data Center CPU Grace is slated for H1 next year. Networking chip demand is strong; supply remains constrained but is improving.

The new H100 enters volume production in Q3 and ramps in Q4. At Computex, NVIDIA announced liquid-cooled A100 for Q3 shipment and liquid-cooled H100 for early 2023. The company expects Data Center to grow sequentially every quarter this year. The Data Center CPU ships in H1 next year; Computex unveiled a roster of OEM partners. 2023 could see a Data Center inflection.

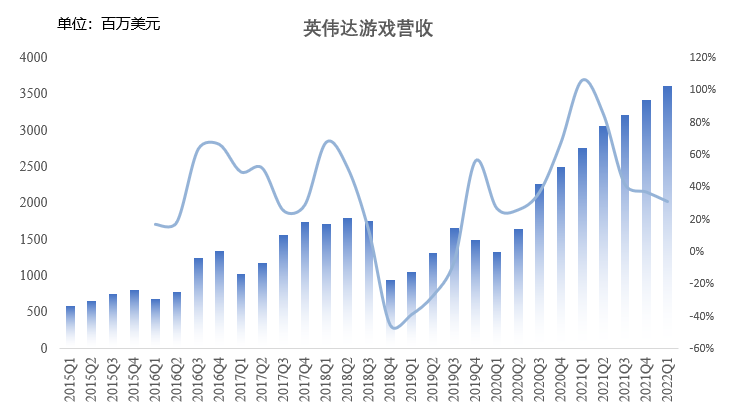

Gaming Q1 revenue was $3.62B, up 31.2% year over year and 5.8% sequentially, the seventh consecutive quarterly record. Gaming laptop revenue continued to set records; Switch performed well, but desktop discrete GPUs were soft. RTX penetration reached 33%. The RTX 30 series, launched in fall 2020, is the most successful series to date. However, with RTX 40 launching in Q3, Q2 sits at the tail end of the transition cycle.

The market has fretted over PC demand. Jensen said overall end-market demand is stable; Europe and China face near-term headwinds from war and lockdowns, but North America is strong. Despite the official guidance calling for a 15% sequential decline in Gaming, management remains confident in the second half.

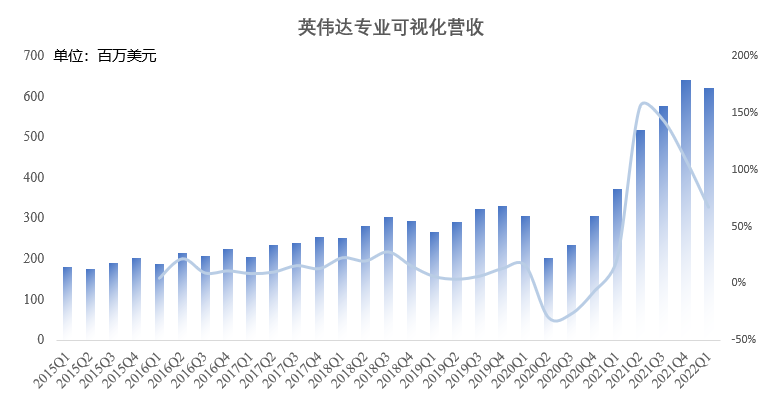

Professional Visualization Q1 revenue was $620M, up 67.2% year over year but down 3.3% sequentially. Mobile workstation demand was strong; desktop workstations declined. Among the global top 100 enterprises, 10 have signed Omniverse deals; 700 companies are evaluating it; cumulative downloads reach 200K.

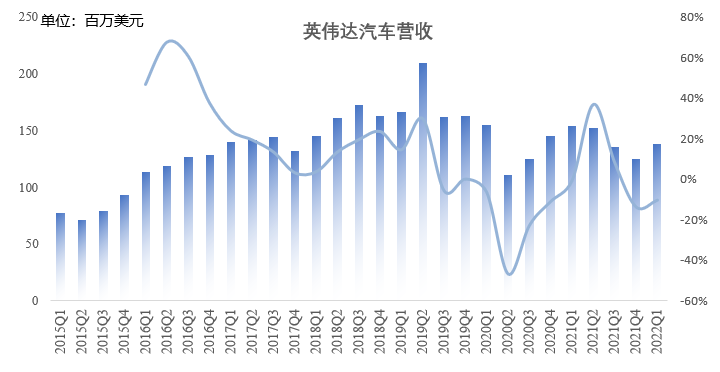

Automotive Q1 revenue was $140M, down 10.4% year over year but up 10.4% sequentially, the second consecutive quarter of year-over-year decline. The Orin autonomous driving chip will contribute in Q2; legacy cockpit business continues to decline.

CMP mining chip revenue was negligible in Q1. Entry-level notebook discrete GPU revenue also declined, driving OEM & IP revenue down to $160M. No material impact on the overall company.

As we noted last time, Q1 included a $1.357B Arm-related charge, which virtually guaranteed a GAAP net income decline year over year. The media loves a sensational headline, harping on this charge to claim NVIDIA's profits are failing, but they ignore that this payment secures a 20-year Arm license — effectively front-loading the expense.

How to Interpret the Weak Q2 Gaming Guidance?

NVIDIA guided Q2 revenue of $8.1B, up 24.5% year over year but down 2.3% sequentially; the Street expected $8.45B. The last sequential decline was Q1 2020; the market responded with a sharp sell-off. NVIDIA cited a $500M revenue hit from exiting Russia and China lockdowns, of which $400M was Gaming and $100M Data Center. Adding back the $500M would put guidance above expectations, but the macro impact is real.

At the segment level, Gaming is guided down 15% sequentially and roughly flat year over year, driven by 1) the Russia-Ukraine war, 2) China lockdowns, 3) the impending RTX 40 launch. Data Center and Automotive are guided to continue strong growth both year over year and sequentially. Knowing Jensen's guidance style, Q2 will likely still deliver sequential growth, but this year's extreme macro is affecting many tech companies.

Amid high inflation and recession fears, NVIDIA's Q1/Q2 OpEx grew 32%/39% year over year, well above the historical 25% norm. NVIDIA attributed this to preparing for Q3 new products and over-hiring earlier; to protect current employee benefits, hiring will slow. Some media spun this as a sign of weakness. Jensen said Q3 will be the biggest product launch wave in NVIDIA's history, evidenced by a 66% year-over-year increase in supply-chain prepayments and continued inventory builds. The company expects OpEx to normalize in the second half, with full-year Non-GAAP OpEx growth returning to the normal 25% level.

NVIDIA also unusually repurchased $2B in Q1, with shareholder approval for $15B in buybacks through December 2023. The market shrugged and kept selling.

By contrast, AMD's guidance was more optimistic: Q2 revenue ex-Xilinx also grows sequentially. Intel's guidance was more pessimistic, and that was before the Shanghai lockdown intensified.

Q2 may be NVIDIA's slowest growth quarter of the year, but the second-half product cadence should restore high growth in Gaming. Data Center remains NVIDIA's core long-term growth engine.

We estimate NVIDIA FY2022 revenue of $36.8B, up 37% year over year, and Non-GAAP net income of $15.2B, up 35% year over year. The current market cap implies a Non-GAAP P/E of 28x on this year's estimates.

Even with extremely bearish sentiment, tracking exceptional tech companies remains worthwhile, because we believe technology is the primary productive force.