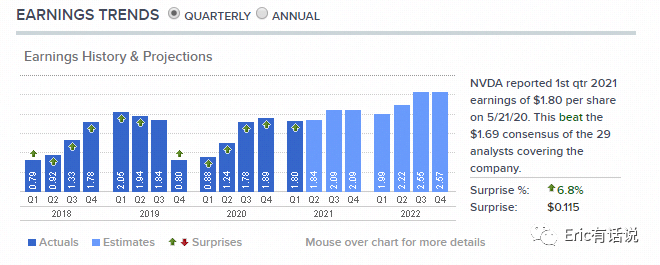

NVIDIA's FY2021 Q1 (referred to as calendar 2020 Q1 below) earnings arrived as expected, with EPS once again beating estimates. Overall, Q1 revenue met high-growth expectations, and Q2 guidance was also optimistic.

Source: CNBC

Against the pandemic backdrop, this morale-boosting report gave NVIDIA a strong start to 2020.

In this report, NVIDIA broke with its traditional GPU & Tegra segment reporting, switching to a two-segment structure: Graphics and Compute & Networking. This highlights the strategic importance of AI and HPC and adds Mellanox networking technology to the mix.

Source

Source: Company Filing

Q1 Earnings Overview

Earnings Summary:

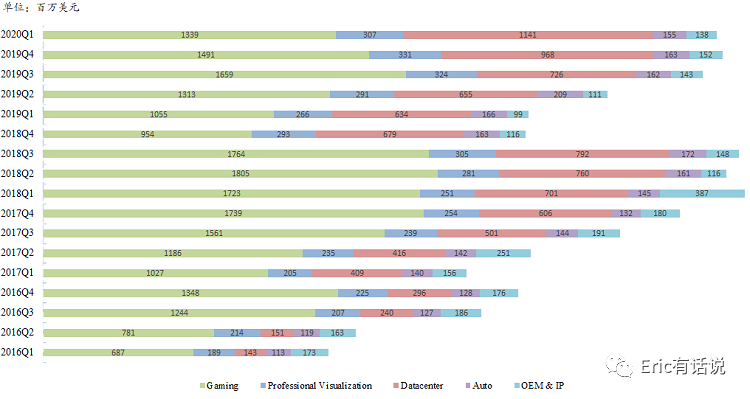

Q1 revenue $3.08B, up 39% year over year, down 1% sequentially, slightly above prior guidance.

GAAP net income $917M, up 133% year over year, down 3% sequentially.

Non-GAAP net income $1.12B, up 106% year over year, down 4% sequentially.

GAAP gross margin 65.8%, up 680 bps year over year and 40 bps sequentially, a new record high.

Data source

Overall, revenue slightly beat expectations while profit significantly exceeded them. After a cold start to 2019, NVIDIA fully recovered in the second half. For the first time in two years, NVIDIA posted three consecutive quarters of revenue above $3B.

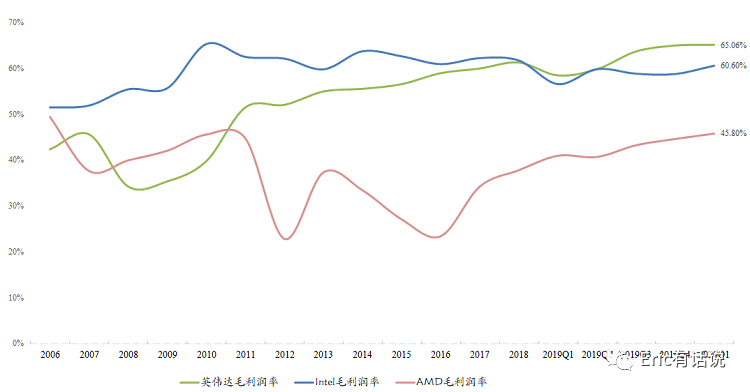

Compared to Intel and AMD, NVIDIA's gross margin leads by a wide margin. Given NVIDIA's software-centric strategy, gross margin has further upside. However, due to the Mellanox acquisition, GAAP and Non-GAAP gross margins will diverge for the next three quarters, with Non-GAAP continually setting new records.

Data source: Company Filing

Data center knows no bounds! Q2 set to become largest segment

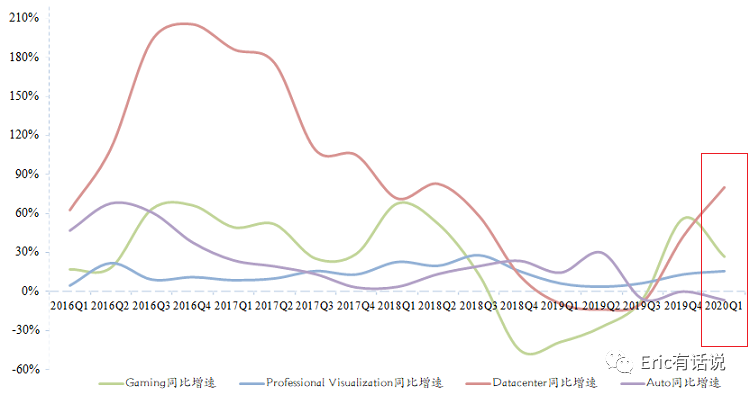

NVIDIA Q1 data center revenue $1.141B, again far exceeding expectations. Up 80% year over year and 18% sequentially, a new quarterly record — and this still excludes Mellanox, which NVIDIA plans to consolidate in Q2 and include in data center.

Data source: Company filing

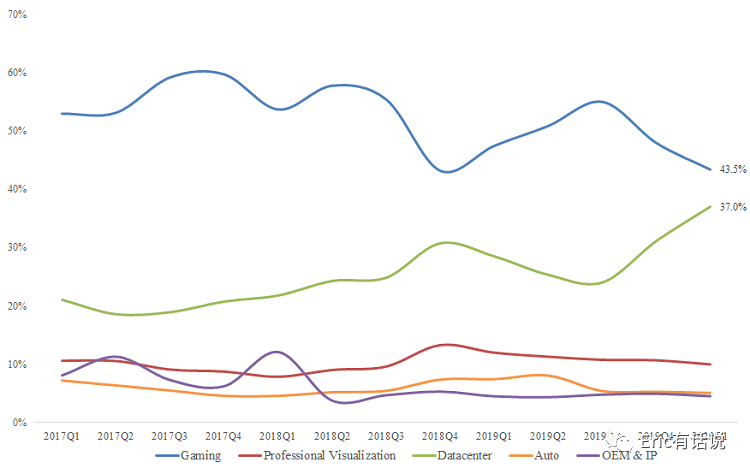

Notably, Q1 data center accounted for 37% of revenue, also a record. Given Mellanox's high growth, we expect Q2 data center to surpass gaming and become NVIDIA's largest segment.

Data source: Company Filing

Since 2015, data center revenue has compounded at 54.5% annually. From under $340M in 2015 to $2.983B in 2019, the growth is staggering.

Management's Q2 data center outlook is also bullish, citing strong hyperscale and vertical demand. The Ampere A100 GPU, unveiled at GTC with 20x performance gains, has begun shipping and contributed revenue in Q1. Combined with Mellanox's high growth, data center revenue should continue to set records.

In short, we believe AMD's main data center rival remains Intel, while NVIDIA now possesses an end-to-end hardware and software moat in data center. Overall, the data center TAM defies boundaries; NVIDIA, Intel, and AMD are in a win-win, not zero-sum.

Gaming meets expectations; professional visualization still promising

Gaming steady; gaming laptop growth hits record high!

NVIDIA Q1 gaming revenue $1.339B, up 27% year over year, down 10% sequentially, roughly in line with expectations.

Last quarter's call guided for seasonal declines in Q1 notebook GPU and Switch. The sudden pandemic instead boosted gaming, with Switch growing both year over year and sequentially.

The strongest performer in gaming remains gaming laptops. Gaming laptops have posted double-digit year-over-year growth for nine straight quarters. Q1 gaming laptop growth hit a six-quarter high. As we've emphasized in external research, "gaming laptop business has high certainty; Max-Q writes the laptop future." Max-Q balances performance and thin-and-light, and the future of gaming laptops is the unification of performance and portability.

The primary future growth driver for NVIDIA gaming remains gaming laptops; the graphics technology direction continues to favor ray tracing. Also looking forward to the RTX 3000 series.

Professional visualization "accumulates grains into a tower," beneficiary of the "everyone a creator" era

Another segment to watch is professional visualization. We previously argued "professional design and visualization market outlook bright; GPU adds color to creativity."

NVIDIA Q1 professional visualization revenue $307M, up 15% year over year, down 7% sequentially; Turing products neared 50% of shipments in Q1.

Professional visualization is the only NVIDIA segment with 17 consecutive quarters of year-over-year revenue growth since 2016. In the 5G era, we are bullish on GPU adoption in professional rendering, video creation and editing, and engineering design. NVIDIA's GPU optimization for video software can multiply efficiency, often several times over traditional CPU. Professional visualization may become NVIDIA's next stable earnings contributor after data center.

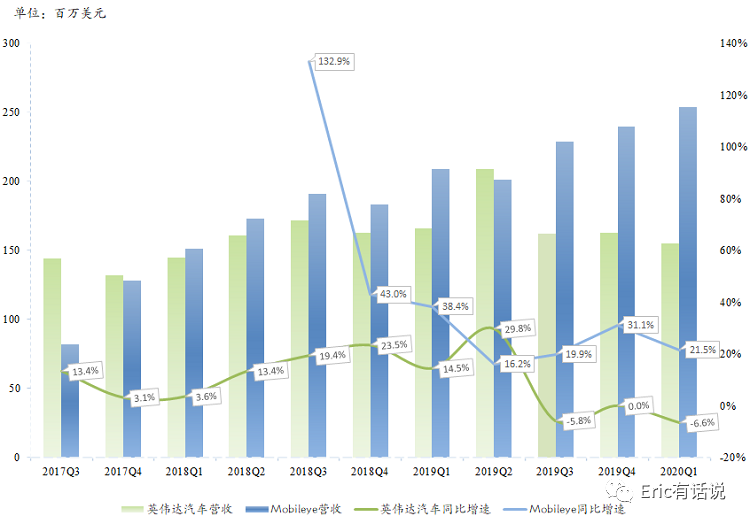

Auto weak; Q2 guidance down 40% sequentially

Of NVIDIA's four segments, only auto declined this quarter; the rest all posted double-digit year-over-year growth.

On NVIDIA auto, our view has been that despite deep tech reserves, near-term upside is limited; the focus remains on ecosystem building. Stockpile grain, delay coronation.

NVIDIA signed a one-time revenue recognition auto deal with Toyota and others in Q2 last year, driving a record quarter. But Q3 and Q4 auto revenue essentially flatlined. In 2020, Q1 auto revenue was $155M, down 6.6% year over year, gradually falling behind Intel's Mobileye. Q2 guidance calls for a 40% sequential decline, confirming the downtrend.

Data Sources:

Company Fil

ing

Traditional infotainment still accounts for over half of NVIDIA auto revenue; autonomous driving chips remain a small share — only the future imagination space is large.

Conclusion

Over the past year, NVIDIA delivered a satisfying scorecard. Gaming roared back, data center fully recovered, and overall results returned to 2018 peaks. The sudden pandemic could not stop NVIDIA from posting its best-ever performance.

NVIDIA CEO Jensen Huang noted on the call that the pandemic brought four structural impacts:

Enterprise digitalization is irreversible; accelerated "move to cloud" is a done deal.

Humanity needs compute-intensive health defense systems for the next pandemic.

AI and robotics will become indispensable.

Working from home has become a trend, and the status of gaming entertainment remains unshakable.

NVIDIA guided FY2021 Q2 revenue of around $3.65B, a record high, implying roughly 41.5% year-over-year growth. GAAP gross margin guidance is 58.6%, while non-GAAP gross margin will reach an unprecedented 66%.

Hearteningly, NVIDIA — the company with the second-highest average compensation globally — not only gave across-the-board raises during the pandemic but also disclosed on the earnings call that it pre-funded employee salaries four months early, causing a sharp jump in Q2 opex guidance.

On the business front, Q2 gaming is expected to be driven by continued growth in notebook GPUs and Switch, up about 5% sequentially. Data center should remain strong, with the company extremely optimistic on A100 shipments.

The U.S.-China tech conflict also became a focal point for analysts. NVIDIA CEO Jensen Huang stated that China's high-performance computing market is primarily served by domestic supply chains, so the overall impact on NVIDIA's data center business is limited.

The gaming company NVIDIA is gone, replaced by the AI company NVIDIA. Defining NVIDIA's boundaries is truly difficult.