Gaming business rebound arrived on schedule.

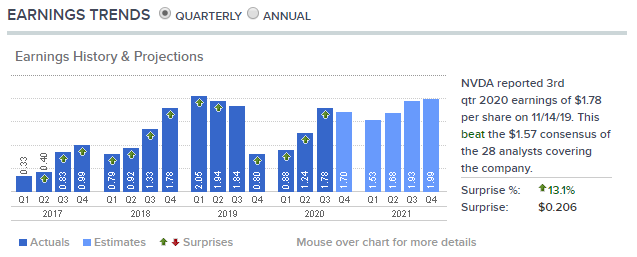

NVIDIA's Q3 earnings arrived late; as expected, EPS beat again. After all, CEO Jensen Huang's expectation management is masterful. Notably, the stock gyrated after hours, partly because Q4 guidance missed expectations. So, per the usual pattern, 'does guidance missing mean Q4 will likely beat?'

Source: CNBC

Setting aside 'conspiracy theories,' this report held plenty of surprises.

Q3 Earnings Overview

Earnings Summary:

Q3 revenue $3.014B, down 5.3% year over year, up 16.9% sequentially; prior-quarter guidance $2.9B;

GAAP net income $899M, down 26.9% year over year, up 62.9% sequentially;

Non-GAAP net income $1.1B, down 4.2% year over year, up 44.8% sequentially;

GAAP gross margin 63.6%, up 3.2 pct year over year, up 3.8 pct sequentially;

Non-GAAP gross margin 64.1%, up 3.1 pct year over year, up 4 pct sequentially.

Overall, revenue and gross margin beat expectations; sequential improvement confirms NVIDIA's recovery. For the first time in a full year, quarterly revenue topped $3B again.

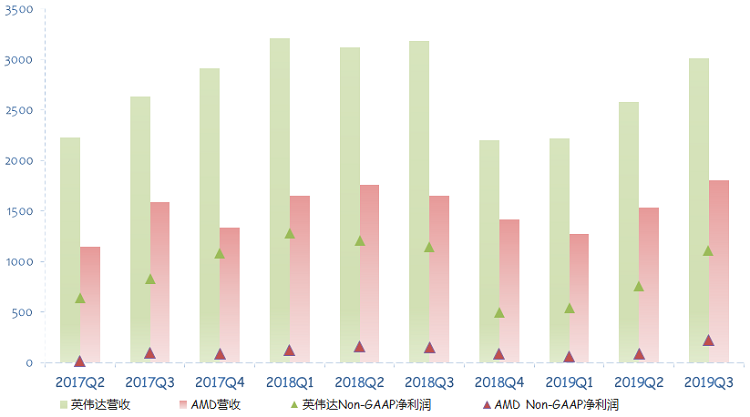

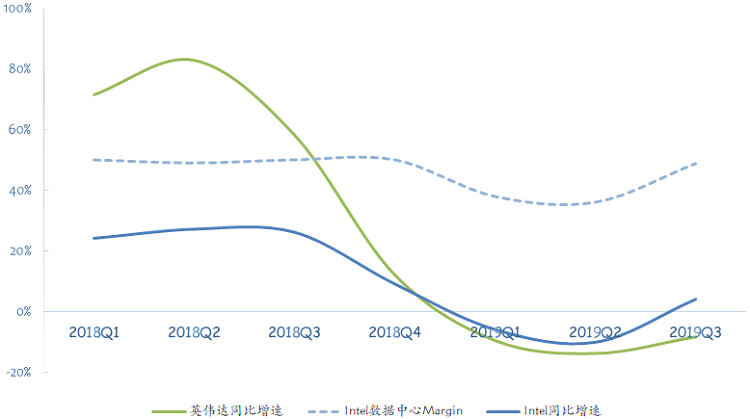

At NVIDIA's nadir (2018 Q4), AMD narrowed the revenue gap to $800M and the non-GAAP net income gap to $400M. But as NVIDIA recovered in 2019, both gaps widened again.

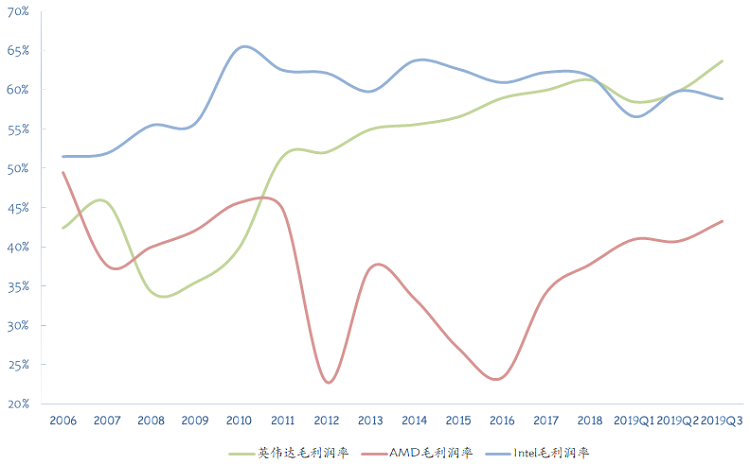

Besides AMD's heavy interest-bearing debt, gross margin is the other key driver of the net income gap. The most surprising figure in this report was the sharply higher gross margin.

Q3 GAAP gross margin hit 63.6%, near the company's historical peaks of 64.48% in 18Q2 and 63.87% in 18Q3, well above the 62% guided in Q2. This margin level now leads Intel and AMD.

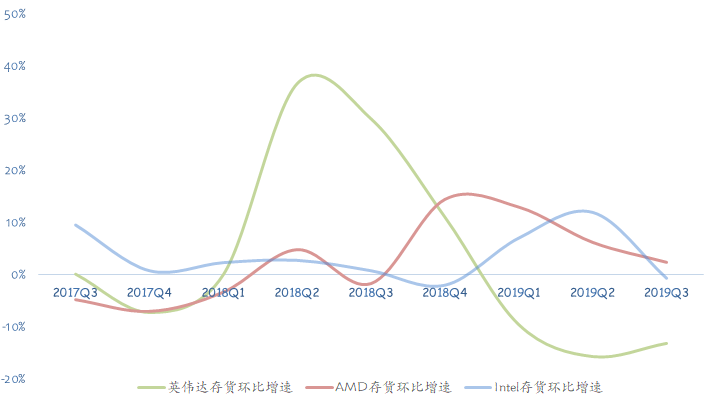

In Q1 the market still worried about NVIDIA and AMD 'destocking' progress; by Q2 mining inventory was largely cleared, so tracking sequential inventory changes mattered less. But interestingly, all three companies launched many new products in the first half, yet NVIDIA's inventory was digested remarkably fast — a testament to Huang's 'blade work.'

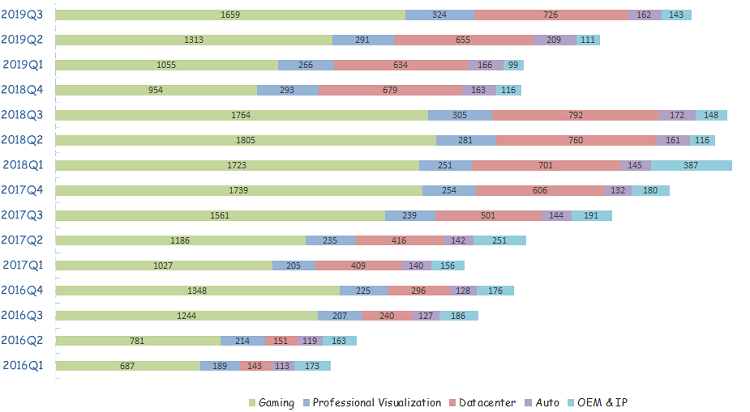

Q3 Segment Performance

Q3 Filing:

Gaming recovery was faster than we expected: single-quarter revenue $1.659B, up 26% sequentially.

Visualization revenue $324M, a record. NVIDIA Quadro RTX workstations and Quadro RTX professional GPUs shone in their niches;

Data center, like Intel, recovered sequentially: single-quarter revenue $726M, up 11% sequentially. Supercomputing stood out, proving the issue isn't data center GPU demand but AMD's data center GPU competitiveness;

The Q2 auto deal was a one-time revenue recognition, so Q3 auto decline was inevitable.

Gaming business erupts on schedule

While the market reveled in AMD's process-node coup, it overlooked NVIDIA's masterful 'blade work' and the 'price-cut lure.' We published research in early September bullish on NVIDIA's gaming recovery.

Our core thesis: 'Gaming laptops will become the new global PC growth driver; a Switch refresh will revive the long-weak Tegra business. Beyond that, we remain bullish on ray tracing; NVIDIA's bet on ray tracing aligns with current market demand. We are confident in NVIDIA's recovery and look forward to Q3 bringing more hope.'

NVIDIA's gaming business delivered as hoped this quarter. Single-quarter gaming revenue $1.659B, reaching 92% of the historical peak (2018 Q2).

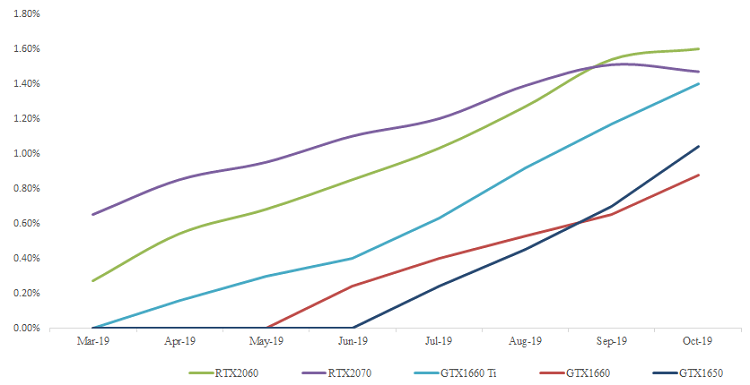

Examining the gaming mix, desktop GPU shipments fell year over year — understandable given the GTX 1060, the world's best-selling GPU, a year ago. But desktop GPU shipments still rose sequentially; the RTX series has now gained market acceptance.

This quarter NVIDIA cut prices repeatedly and launched several GTX 16-series mid-range cards with good effect. Per Steam, the recently launched GTX 1660/1650 share rose quickly; the top 10 GPUs on Steam are all NVIDIA, including RTX 2060.

Source: Steam

The main gaming growth drivers remain the gaming laptops and Switch SoC we favored. Market data shows the 2018 gaming laptop market reached $12B; 2019 is estimated to grow ~25% to $15B, with a 5-year CAGR of 20%. Gaming laptops' PC status is self-evident.

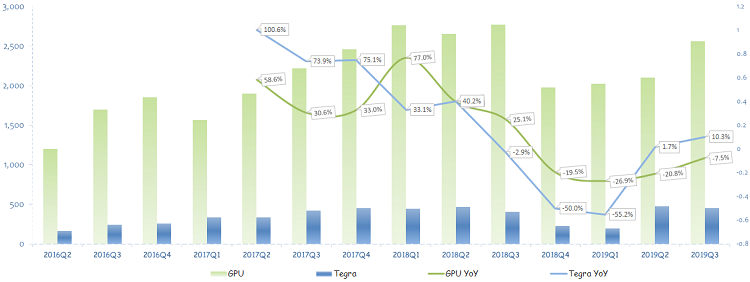

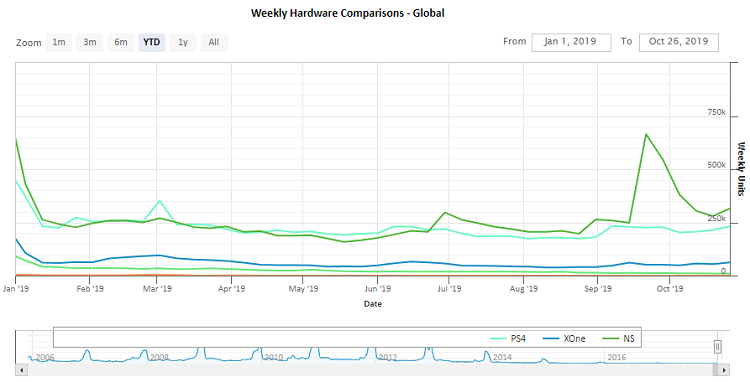

On consoles, Switch Lite and revised Switch shipments contributed significantly. Tegra revenue was $449M, up 10.3% year over year, down 5.5% sequentially. Last quarter included the one-time Toyota deal; with auto revenue down $47M sequentially, Tegra fell only $26M, implying Switch SoC and AI edge SoC held up well sequentially.

Source: VGChartz

Conclusion

Overall, this is the best report NVIDIA has delivered this year. Gaming rebounded strongly, data center began to recover, and full-year performance could be down only single-digits year over year, back to 2018 peaks. But Huang still threw cold water on investors, perhaps for 'expectation management': Q4 revenue guidance was conservative.

NVIDIA guided Q4 revenue of $2.891B-$3.009B, a sequential decline, mainly expecting seasonal drops in notebook GPUs and Switch. But GAAP gross margin guidance was very high at 64.1%, the second-highest in company history. The company also expects data center to continue sequential recovery. On the Mellanox deal, EU and China antitrust approvals remain; expected to close early next year.

In short, hoping for a rapid return to 2018 highs seemed unrealistic at the start of the year, but Q3 showed a full-year recovery to 90% of 2018 is very possible; perhaps the current 12x P/S isn't expensive.