AMD sharply raised its 2030 CPU market TAM, reinforcing investor expectations for strong server CPU demand, tight supply, and higher pricing.

AMD Q1 Results:

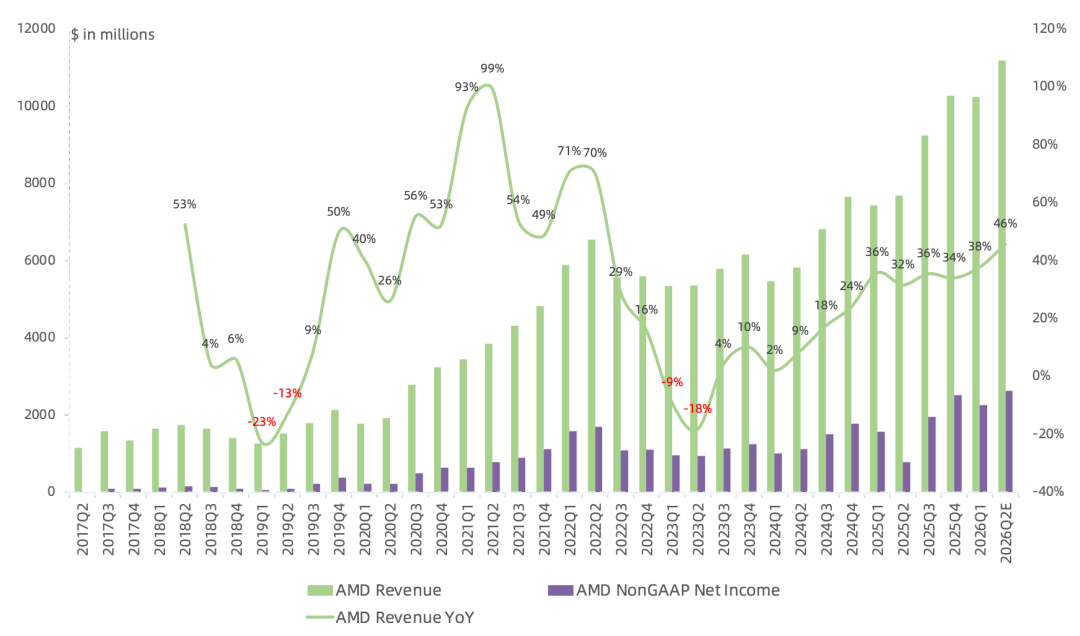

Revenue reached $10.25B, up 38% year over year and down 0.2% sequentially. AMD expects Q2 revenue of $11.2B, up 46% year over year and 9% sequentially.

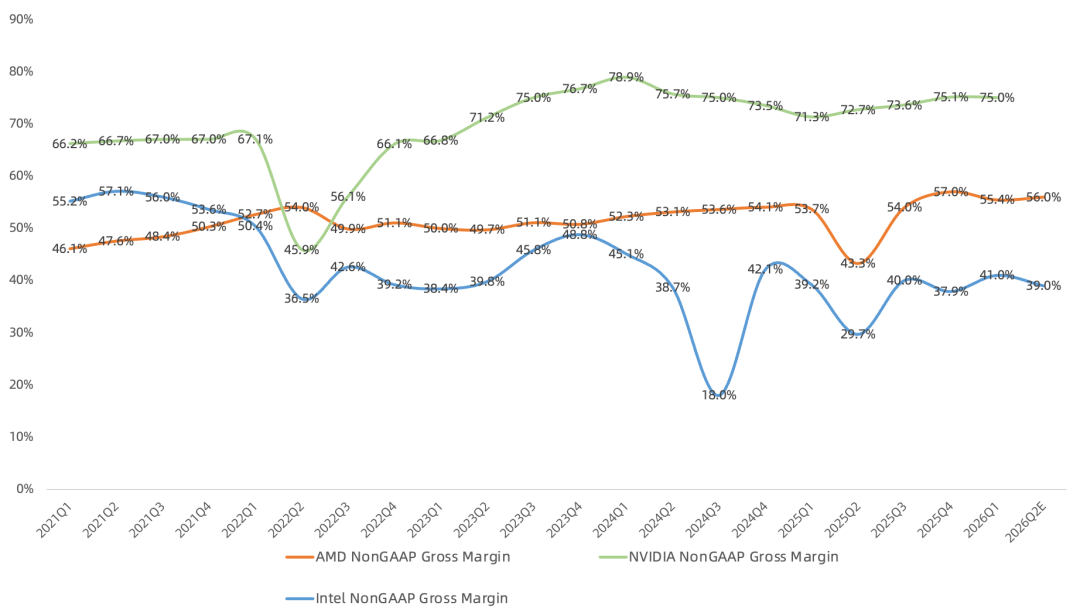

GAAP gross margin was 52.8%. Non-GAAP gross margin reached 55.4%, up 1.7 percentage points year over year and down 1.6 points sequentially. Q2 non-GAAP gross margin is expected to be 56%.

GAAP operating income reached $1.48B, up 83% year over year, while non-GAAP operating income rose 43% to $2.54B. AMD expects Q2 non-GAAP operating income of $3.03B, up 238% year over year and 19% sequentially.

GAAP net income reached $1.38B, up 95% year over year, while non-GAAP net income rose 45% to $2.27B. Q2 non-GAAP net income is expected to reach $2.64B, up 238% year over year and 16% sequentially.

AMD repurchased $221M of stock in Q1, leaving $9.2B under its authorization.

Q1 Segment Results:

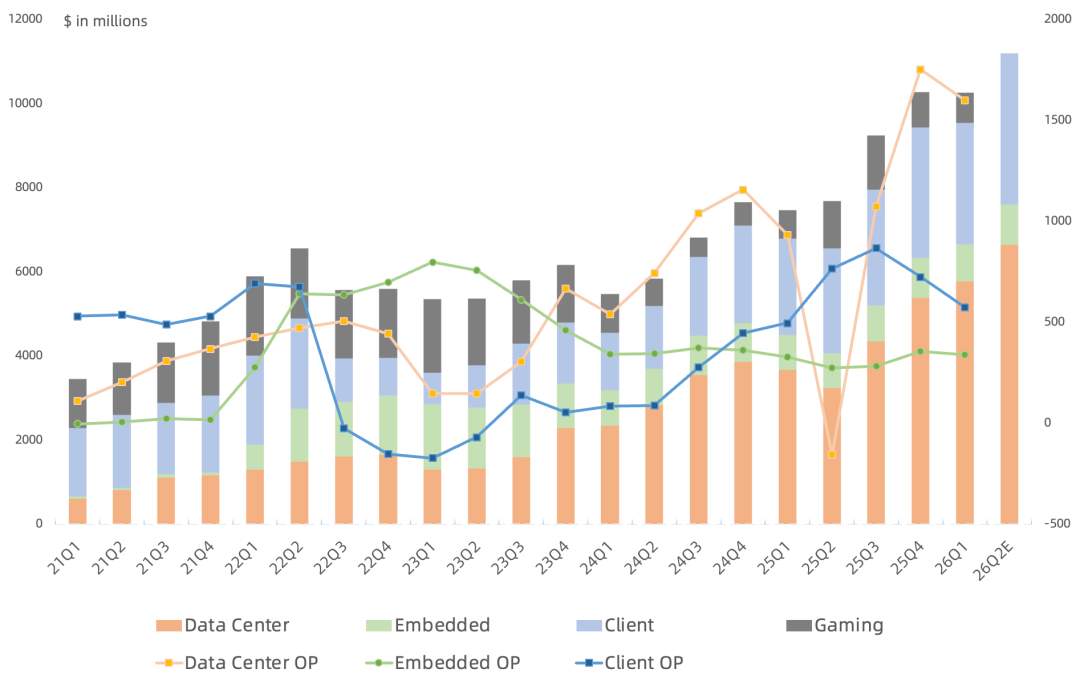

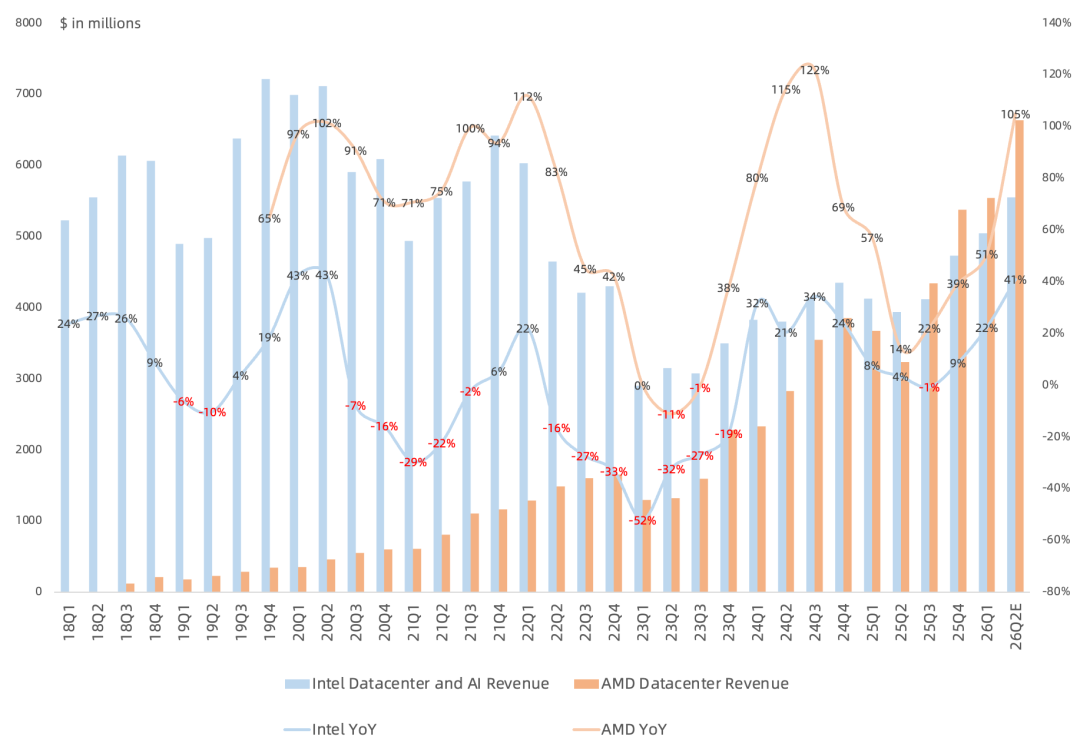

Data Center revenue reached $5.78B, up 57% year over year and representing 56% of total revenue. Segment operating income was $1.6B, while operating margin declined sequentially to 28%.

On CPUs, server processors were the main Data Center growth driver this quarter. EPYC revenue set a record for a fourth consecutive quarter. Zen 5 Turin accounted for more than half of EPYC revenue, or roughly $1.7B, while demand for Zen 4 Genoa also remained strong. The number of EPYC-powered cloud instances increased nearly 50% year over year to more than 1,600. In enterprise, both EPYC revenue and sell-through reached records. The 2nm Zen 6 Venice family, scheduled to ship by the end of 2026, includes processors optimized for throughput, performance per watt, and performance per dollar. It also includes Verano, the first EPYC CPU designed specifically for AI infrastructure. Customer demand is exceptionally strong, with more customers validating and ramping Venice platforms at this stage than for any previous EPYC generation.

On GPUs, Data Center GPU revenue declined slightly sequentially because of the transition in China. Revenue still grew at a strong double-digit rate year over year as Instinct adoption accelerated across cloud, enterprise, sovereign AI, and supercomputing customers. Meta plans to deploy up to 6 GW of AMD GPUs across several product generations, including a custom GPU based on the MI450 architecture, with shipments still scheduled to begin in the second half of 2026. AMD has started sampling the MI450 family to leading customers and remains on track to ramp volume shipments of the Helios rack-scale platform in the second half. That ramp will pressure gross margin in Q4.

Demand for the MI450 GPU family continues to strengthen. Management remains confident that annual Data Center AI revenue can reach tens of billions of dollars in 2027 and grow by more than 80% over the following several years.

Embedded revenue reached $870M, up 6% year over year for a second consecutive quarter of growth and representing 9% of total revenue. Operating income increased 3% to $340M, leaving Embedded as AMD's highest-margin segment. Demand was particularly strong in test, measurement, and simulation. Design-win momentum grew at a double-digit rate, with several billion dollars of new wins across multiple markets.

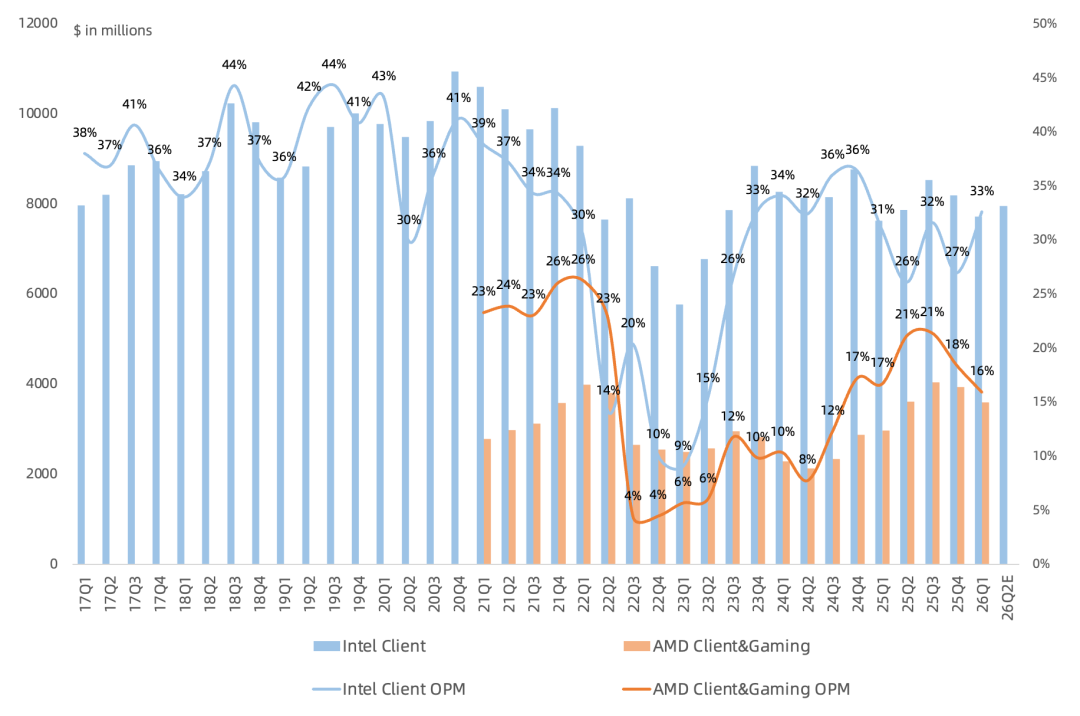

Client revenue reached $2.89B, up 26% year over year and representing 28% of total revenue. Gaming revenue rose 7% to $720M, marking a fourth consecutive quarter of growth and representing 7% of revenue. Combined Client and Gaming operating income increased 16% to $580M. Operating margin was 16%, down 2 percentage points sequentially and still well below Intel's 33%.

Client growth was driven primarily by notebook CPUs as Ryzen 400 laptop shipments ramped and commercial adoption increased. Ryzen PRO PC sell-through grew more than 50% year over year. Desktop demand was softer and more exposed to rising memory and component costs.

Within Gaming, semi-custom revenue declined year over year while gaming GPU revenue increased. As in the PC market, management expects higher memory and component costs to weigh on demand in the second half of 2026. Gaming revenue is expected to fall more than 20% from the first half to the second half.

AMD expects Q2 2026 revenue of $11.2B, up 46% year over year and 9% sequentially. Data Center should grow strongly year over year and at a double-digit rate sequentially. Server CPU revenue is expected to rise more than 70% year over year and remain strong through the second half of 2026 and into 2027 as the next EPYC generation ramps. Data Center AI revenue should grow at a double-digit rate sequentially. Client and Gaming are expected to increase modestly both year over year and sequentially, while Embedded should grow at double-digit rates on both comparisons. Ryzen CPU demand should remain healthy in Q2. Higher memory and component costs are expected to reduce PC shipments in the second half, although AMD's Client revenue should still grow year over year. Gaming revenue is expected to decline more than 20% from the first half to the second half.

AMD plans to share more about its next-generation Instinct GPUs, EPYC processors, Helios rack-scale platform, and expanding customer partnerships at the Advancing AI event in July 2026.

At its Financial Analyst Day in November 2025, AMD estimated that the server CPU market would grow at an 18% compound annual rate over the following three to five years. It has now raised that estimate to 35%, putting the 2030 addressable market above $120B, and remains confident in its goal of 50% CPU market share. However, AMD did not raise its corresponding long-term financial targets and still expects EPS above $20 within three to five years and gross margin of 55%-58%.

Lisa Su framed the CPU opportunity in three layers: general-purpose computing, head nodes that support AI accelerators, and CPUs for agentic AI workloads. Management views growth in agentic-computing CPU demand as incremental to the existing market.

Revisiting the Previous Quarter's View:

EPYC's continuing share gains against Intel remain the foundation of AMD's results. Intel's own capacity constraints have created an unusually favorable opportunity, and EPYC's performance will help determine whether AMD can navigate the earnings gap before the MI450 family reaches volume production.

AMD's long-term EPS target of $20 remains the key reference point. In a bullish market, investors will price it in well ahead of delivery; in a bearish market, it becomes the valuation anchor.