Although AMD's stock has historically fallen more often than risen on earnings days, that should change now — thanks entirely to Intel. Intel's surprise assist likely has Lisa Su smiling ear to ear.

Q2 Earnings Snapshot

AMD 2020 Q2 Earnings:

Revenue $1.932B, up 26% year over year and 8% sequentially; prior guidance $1.85B

GAAP gross margin 44%, up 3 ppt year over year, in line with prior guidance

Operating income $173M, up 193% year over year

GAAP net income $157M, up 349% year over year

AMD Q2 revenue hit a record second-highest quarter; profits also at historic highs. AMD continues its core PC + data center (Ryzen + EPYC) growth logic.

Notebook CPU explodes as expected, becoming AMD's next comeback battleground

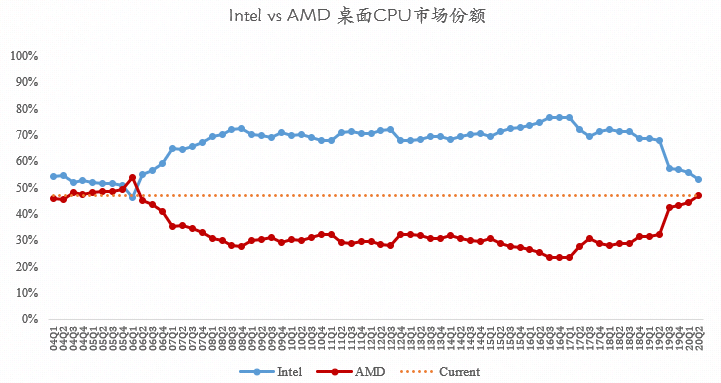

This quarter AMD desktop CPU revenue hit a 12-year high, and market share rose for an 11th consecutive quarter. But notebooks play an increasingly critical role in PC; notebooks will be AMD's next comeback battleground.

Data

Source

:

PassMark

Our most-watched AMD notebook business exploded on schedule in Q2. Ryzen 4000 series mobile CPUs delivered staggering gains; AMD Q2 notebook CPU revenue set another record, continuing to double year over year with high double-digit sequential growth. But PC GPU only grew in notebooks; desktop was weak with RDNA2 not yet launched, ASPs down both year over year and sequentially — very bullish for NVIDIA.

On CPUs, market observation shows Intel's grip on OEMs remains very strong, especially on high-end SKUs. Most brands pair AMD Ryzen 4000 high-end models with low-end GPUs; high-end GPUs are only configurable with Intel CPUs. If Intel loses its OEM leverage, the consequences are unimaginable.

AMD remains humble, consistently likening its pursuit of Intel to a marathon. We see the following primary notebook opportunities for AMD this year:

AMD shipments are still weighted toward the consumer market, leaving a vast commercial opportunity. A large volume of commercial Ryzen 4000 Pro series units will ship in the second half, expected to contribute significant profit.

Brands like Huawei, Xiaomi, and Hasee have not yet fully stocked Ryzen 4000 models in Q2, leaving significant H2 upside.

Per the call, AMD management is very bullish on H2 notebooks, aligning with our view: "Last year watch desktop, this year watch notebook."

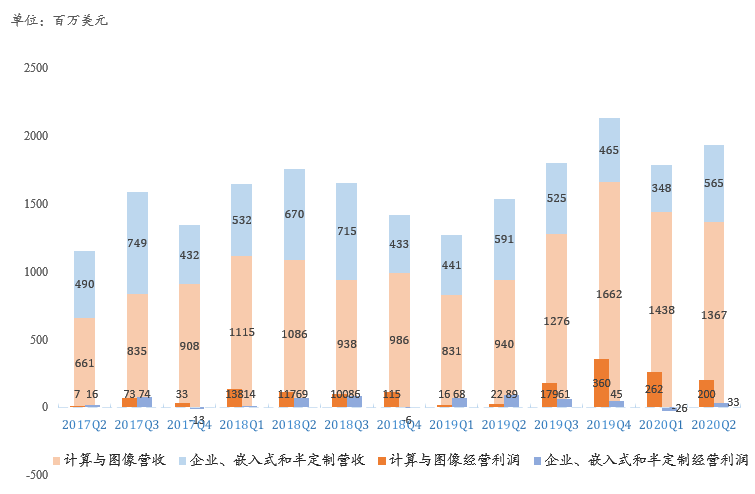

Data center EPYC stands alone; GPU still weak

On data center, AMD's growth driver is EPYC CPU; GPU remains disappointing — a refrain we've repeated for several quarters.

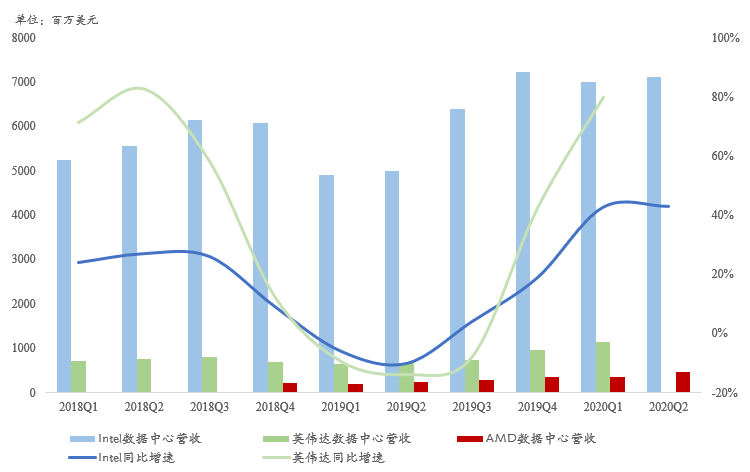

AMD Q1 EPYC shipments grew double-digits sequentially and >3x year over year. Q2 EPYC again doubled year over year with significant sequential growth. Lisa Su proudly announced the 10% server share target achieved. Per the call, Q2 data center revenue mix exceeded 20%, all from EPYC. We estimate EPYC revenue now exceeds $400M; though far below Intel's $7B+ run rate, the upside is larger.

Data center GPU, dependent on software ecosystem, has never been a match for NVIDIA, declining year over year and sequentially for multiple quarters. Management says the year-end CDNA architecture data center GPU will turn the tide. Amusingly, in its earnings deck AMD accidentally promoted NVIDIA's new DGX A100 while touting EPYC.

We maintain our view: "AMD's data center should benchmark Intel, not NVIDIA; NVIDIA's data center GPU has a deep moat."

Source: AMD official website

On gaming consoles, Q1 console business bottomed with negligible revenue and a large profit drag. Q2, with next-gen console SoC shipments starting, Enterprise, Embedded & Semi-Custom revenue reached $565M, up 62% sequentially, swinging to profit. As next-gen consoles ramp, H2 console business should improve.

Don't overestimate AMD's next-gen console business: its gross margin is below the corporate average of 45%. And per history and management, consoles need 4-6 quarters to meaningfully contribute.

Three Questions, Three Answers

In our prior "Earnings Preview" (link in original) we posed three questions:

Can EPYC Q2 share reach double digits?

Lisa Su voluntarily noted on the call that server share finally reached double digits. We don't fixate on the exact share number because EPYC's high growth is plain to see; the reason share lagged 10% is simply that the total market pie kept expanding — look at Intel's data center. We've always believed the data center TAM is huge, and the red, green, and blue vendors are in a win-win, not zero-sum.

Will full-year guidance be raised?

AMD did raise full-year guidance, from 25% year-over-year revenue growth to 32%. The Q1 cut was due to pandemic uncertainty. This raise reflects management's optimism on H2 PC and data center. That optimism is the most direct driver of AMD's stock surge. By contrast, Intel's expectation management has been poor. Currently Micron, SK Hynix, AMD, and other semis are all bullish on H2 data center; only Intel is bearish — very strange.

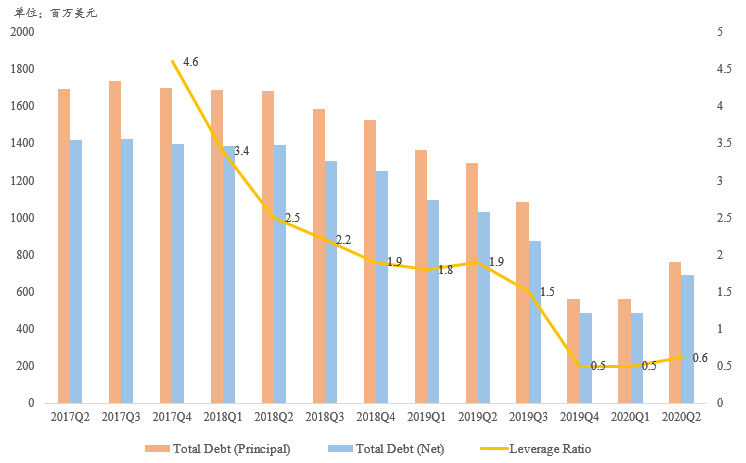

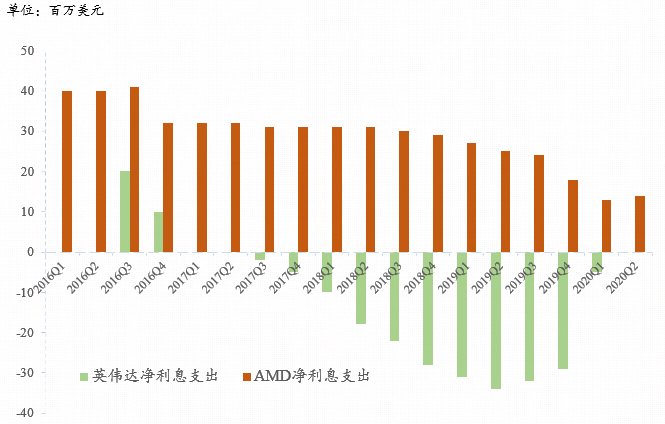

Did deleveraging continue in Q2?

AMD improved cash flow significantly last year, with 2019 operating and free cash flow hitting highs since 2007. We previously noted that massive interest-bearing debt, causing interest expense multiples of peers, was a heavy burden.

In 2020 Q2, interest-bearing debt principal ticked up slightly, understandable given the pandemic. But net interest expense stayed relatively low, and net cash hit a new high.

On the call, a Deutsche Bank analyst asked if AMD, now flush with cash, would consider M&A. Lisa Su perhaps still felt some purse-string shyness, saying the focus remains on organic development. The benefits of low leverage are increasingly evident; whether AMD's debt principal continues to fall is worth watching.

In sum, our long-standing PC + data center core growth thesis keeps being validated. With Intel's strategic focus on data center, AMD's PC market is enjoying its best window: last year watch desktop, this year watch notebook.

Perfect timing: Intel just handed AMD a massive gift package; we hope Ryzen 4000 mobile can replicate last year's desktop comeback myth.