AMD still has not provided a 2026 AI revenue scale guide; guiding 2026 data center revenue up 60%+ year over year.

AMD Q4 Results:

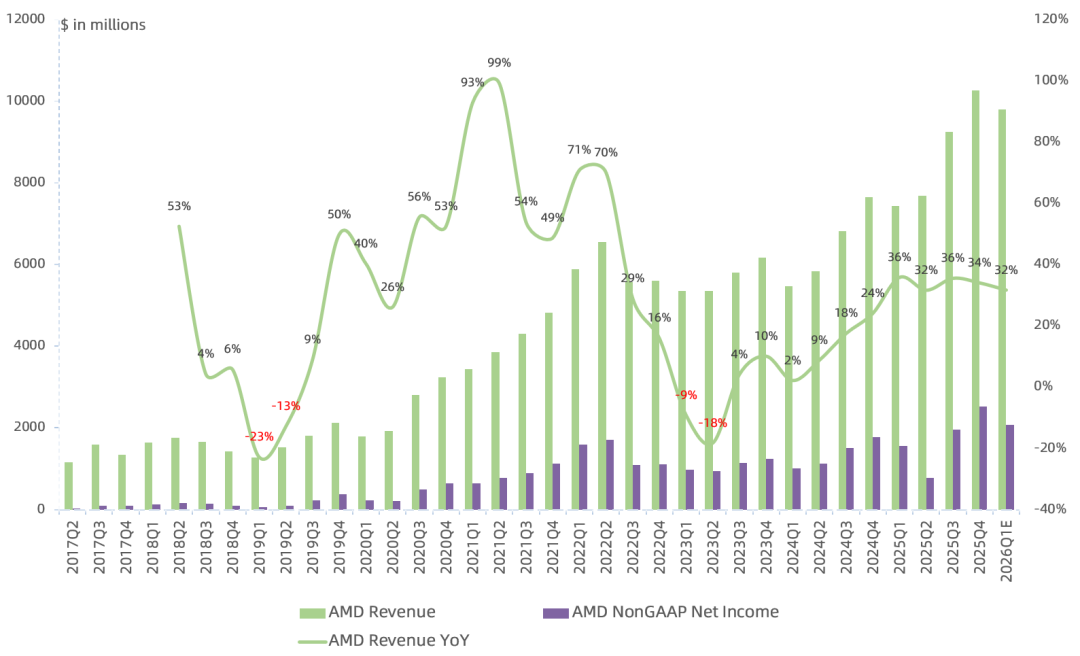

Revenue $10.27B, up 34% year over year and 11% sequentially, including $390M recognized China MI308 revenue; ex-China revenue $9.88B, also above consensus $9.65B; guiding Q1 revenue $9.8B (including $100M China MI308), up 32% year over year but down 5% sequentially.

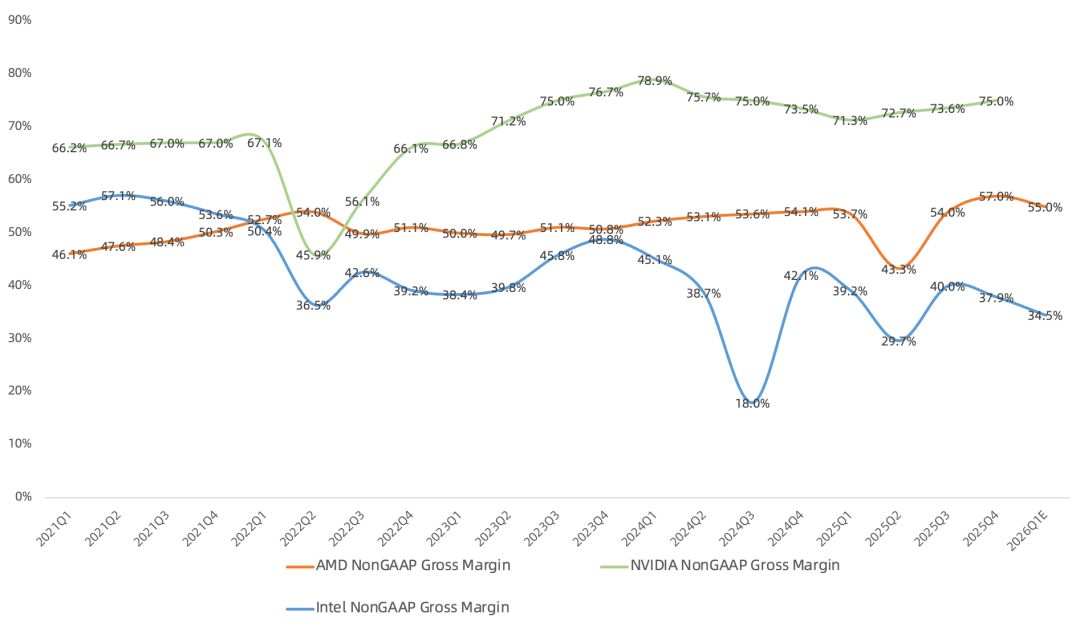

GAAP gross margin 54.3%, Non-GAAP gross margin 57%, up 2.9 percentage points year over year and 3 percentage points sequentially, above consensus 54.5%, primarily due to China MI308 revenue and prior inventory reserve reversals; ex-items Non-GAAP gross margin 55%; guiding Q1 Non-GAAP gross margin 55%.

GAAP operating income $1.75B, up 101% year over year; Non-GAAP operating income $2.85B, up 41% year over year; guiding Q1 Non-GAAP operating income $2.34B, up 32% year over year, down 18% sequentially.

GAAP net income $1.51B, up 213% year over year; Non-GAAP net income $2.52B, up 42% year over year; guiding Q1 Non-GAAP net income $2.07B, up 32% year over year, down 18% sequentially.

No repurchases in Q4; $9.4B authorization remaining.

By Segment Q4:

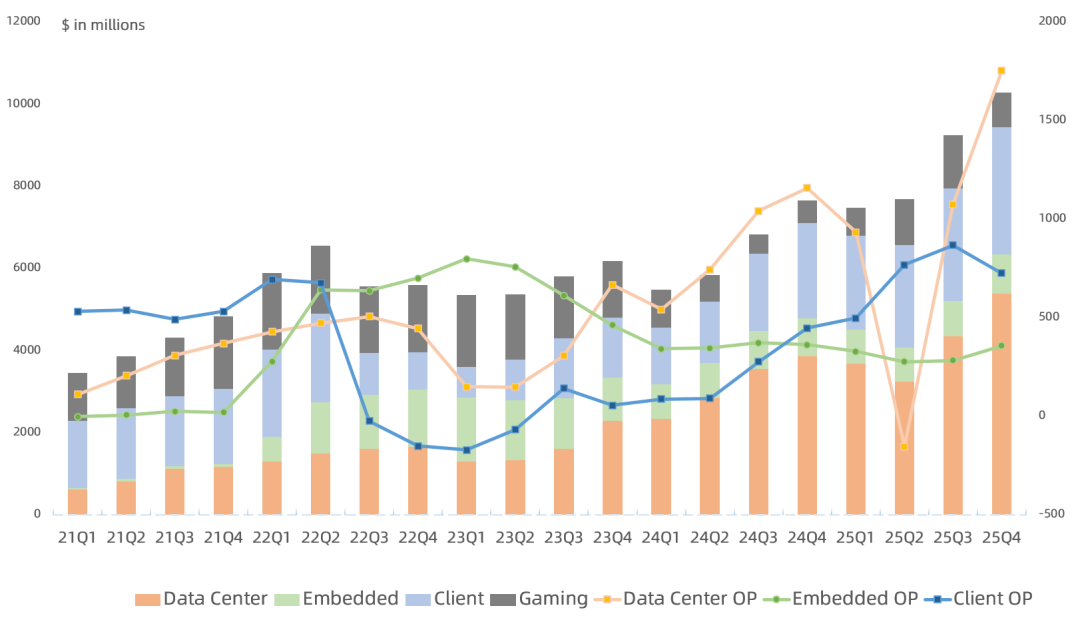

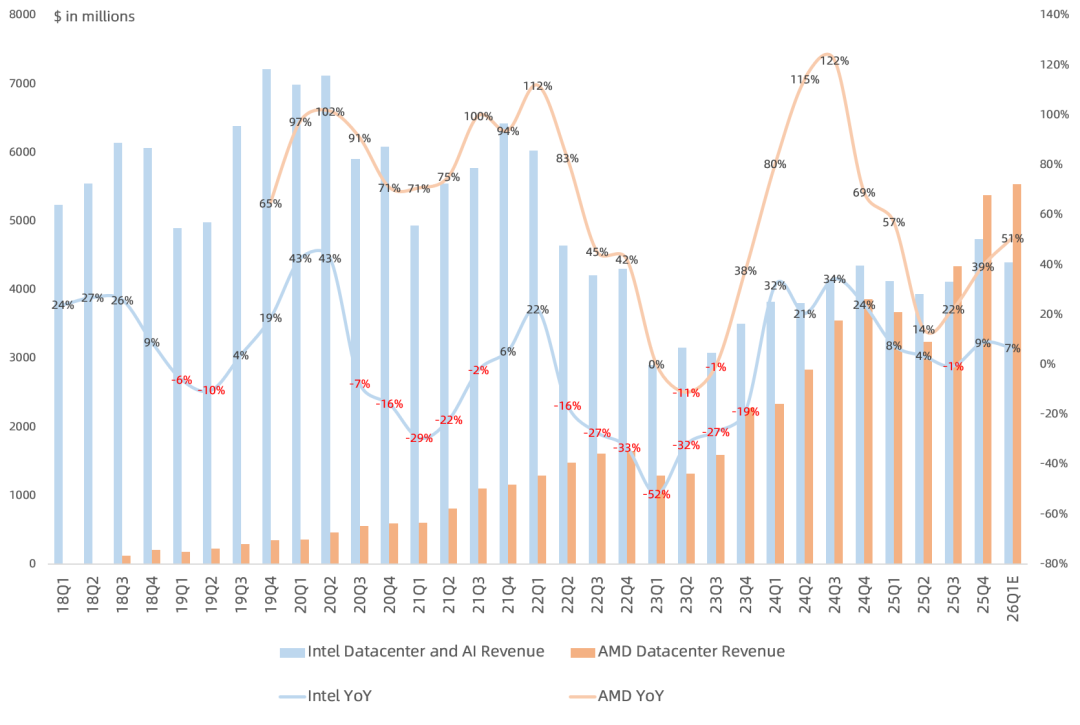

Data Center revenue $5.38B, up 39% year over year, 52% of revenue; operating income $1.75B, operating margin 33% aided by China MI308, making it AMD's most profitable segment this quarter.

CPU: Data center driven primarily by server CPU this quarter, with server CPU growing more; EPYC revenue hits new high, ASP rising; Zen 5 EPYC Turin adoption accelerated this quarter, accounting for over half of server CPU revenue (~$1.5B); Zen 4 EPYC Genoa demand also strong; record server CPU revenue from both cloud and enterprise customers, market share at new high; enterprise on-prem EPYC deployments by large enterprises more than doubled in 2025; strong demand for 2nm Zen 6 EPYC Venice CPU slated for production this year; management believes 2026 overall server CPU TAM will see strong double-digit growth, confirming market views of robust server CPU demand.

GPU: Data center GPU driven by MI350 series ramp this quarter, including $390M China MI308 revenue; ex-MI308 still grew sequentially; beyond multi-gen partnership with OpenAI (6 GW GPU), actively discussing large-scale multi-year deployments based on Helios and MI450 starting later this year with other customers.

H2 MI450 becomes a key inflection; related revenue starts in Q3 but ramps significantly in Q4; MI500 series expected 2027 production with HBM4E, CDNA 6 architecture, 2nm process.

Embedded revenue $950M, up 3% year over year, ending nine consecutive quarters of decline, 9% of revenue; operating income $360M, down 1% year over year, still AMD's highest operating margin segment; test, measurement & simulation demand notable; design wins growing, 2025 exceeded $17B, up nearly 20% year over year.

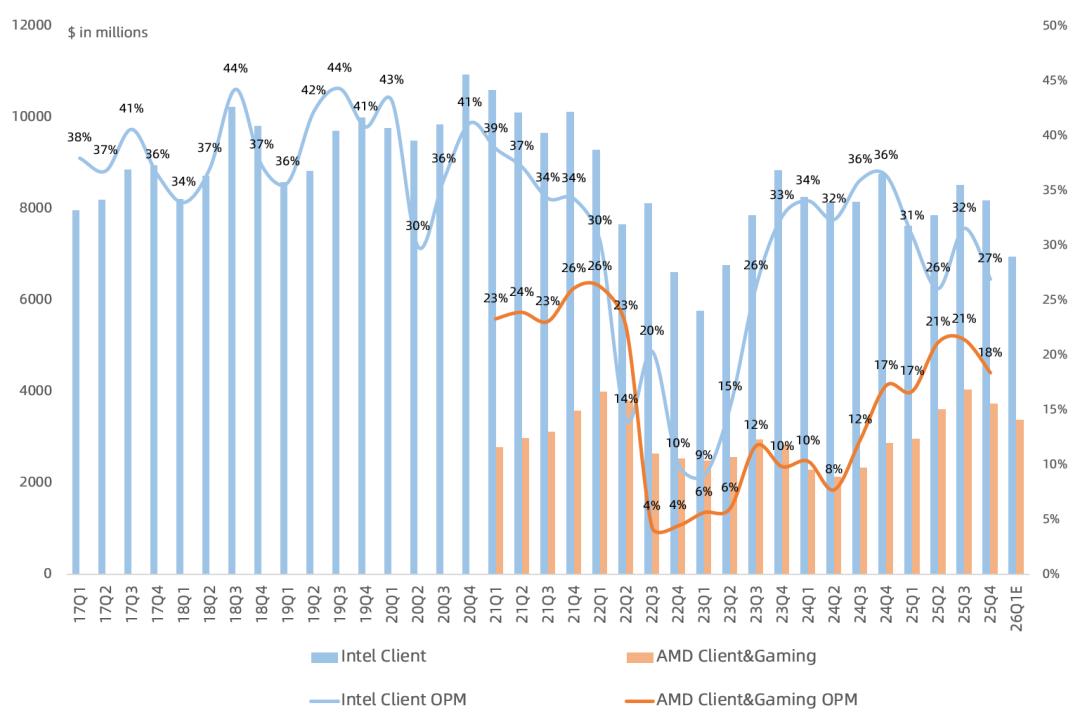

Client revenue $3.1B, up 34% year over year, 30% of revenue; Gaming revenue $840M, up 50% year over year, third consecutive quarter of growth, 8% of revenue; Client & Gaming combined operating income $730M, up 46% year over year, operating margin 18%, still below Intel's 27%.

Client growth driven primarily by desktop CPU; desktop CPU revenue has set records for four consecutive quarters; mobile Ryzen notebook shipments hit record this quarter; commercial notebook and desktop Ryzen CPU shipments up >40% year over year.

Gaming: Semi-custom revenue up year over year, down sequentially; Gaming GPU revenue up year over year; guiding 2026 semi-custom revenue to see significant double-digit decline as current console cycle enters year 7; next-gen Microsoft Xbox expected 2027.

Guiding 2026 Q1 revenue $9.8B, up 32% year over year, down 5% sequentially; guiding Q1 Data Center up year over year and sequentially, both server CPU and GPU up sequentially; Client and Gaming up year over year, down seasonally sequentially; Embedded up slightly year over year, down seasonally sequentially.

This quarter's China MI308 shipments were from early 2025 orders; license application submitted for MI325 but still awaiting result.

Memory price increases will cause 2026 PC TAM to dip slightly, H2 relatively weaker vs H1 in a "non-seasonal" manner; even in a declining PC market, company believes PC business can grow by focusing more on enterprise.

MI450 series to contribute revenue from Q3 in H2, with significant ramp in Q4; MI450 ramp in Q4 may pressure gross margin; management says longer-term each generation should deliver higher gross margins.

MI450 series includes MI455X and Helios for AI superclusters; MI430X for HPC and sovereign AI; 8-GPU MI440X server for enterprise; multiple OEMs publicly announced plans to launch Helios systems in 2026, vast majority to be delivered as rack-level solutions this year.

Continues to project 2027 AI business revenue could reach tens of billions annualized run rate, but avoids guiding 2026 AI revenue; only guiding 2026 data center revenue up 60%+, though market understands this still blurs CPU and GPU growth; management emphasizes 60%+ CAGR for data center over next 3-5 years.

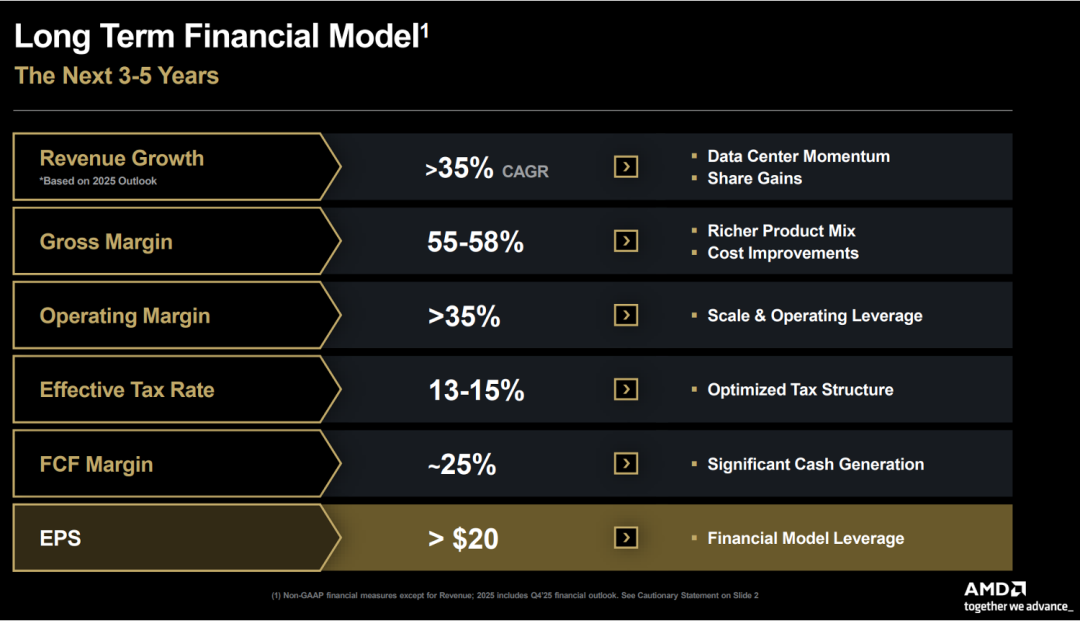

Prior Analyst Day targets: 3-5 year revenue CAGR 35%+, Non-GAAP gross margin 55-58%, Non-GAAP operating margin 35%+, Non-GAAP EPS $20+; Data Center CAGR 60%+, AI CAGR 80%+, non-Data Center CAGR 10%+.

Revisiting the Previous Quarter's View:

Market expectations for AMD were previously too high, hoping for NVIDIA-style or memory-style sequential AI ramp, but that still awaits H2 OpenAI/Oracle MI450 series ramp; market currently underestimates AMD's reliance on OpenAI orders.

EPYC's continuing share gains against Intel remain the foundation of AMD's results. Intel's own capacity constraints have created an unusually favorable opportunity, and EPYC's performance will help determine whether AMD can navigate the earnings gap before the MI450 family reaches volume production.

Simple modeling based on current guidance: assuming Data Center up 60% year over year, Embedded and PC & Gaming up 10%, FY revenue ~$46B+; applying current Q1 21% net margin guide (H2 MI450 ramp to pressure margins) implies FY net income ~$10B; current market cap ~40x P/E.