This quarter AMD still did not provide full-year AI GPU revenue guidance, only painting a pie of future annual revenue exceeding tens of billions.

AMD Q2 Earnings:

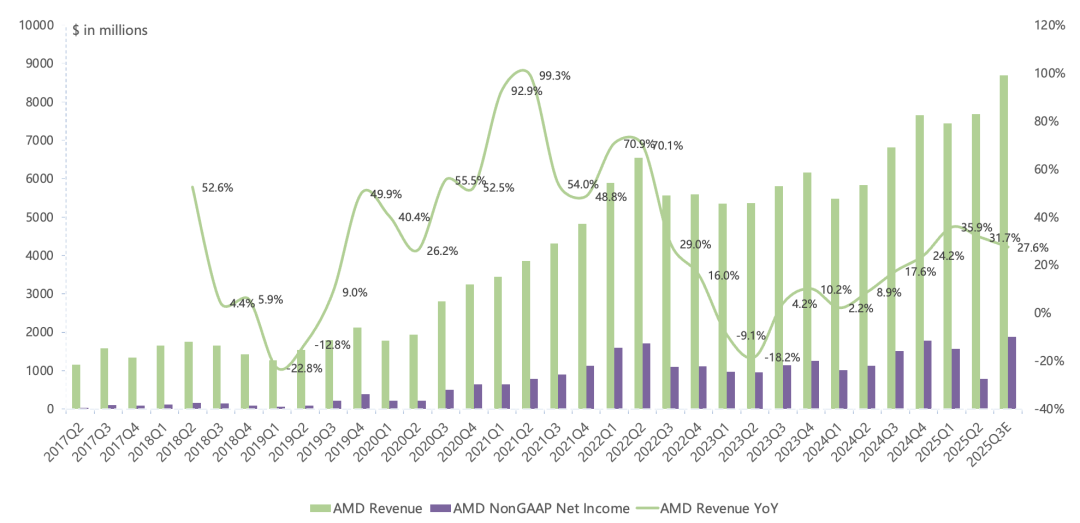

Revenue $7.685B, up 32% year over year, up 3% sequentially, slightly above prior guidance of $7.4B. Q3 revenue guided $8.7B, up 28% year over year, up 13% sequentially.

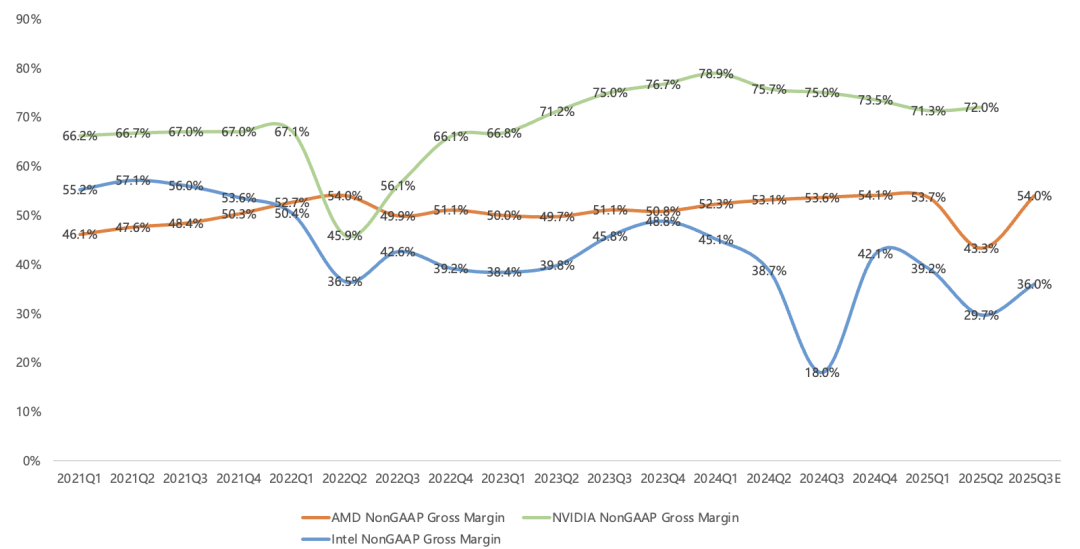

GAAP gross margin 39.8%, non-GAAP 43.3%, both down significantly year over year and sequentially, primarily due to prior MI308 ban impact. Excluding that impact, non-GAAP gross margin 54%, guided similar for Q3.

GAAP operating loss $134M. Non-GAAP operating income $897M, down 29% year over year due to MI308 ban impact. Q3 non-GAAP operating income guided $2.158B, up 26% year over year.

GAAP net income $872M. Non-GAAP net income $781M, down 31% year over year. Q3 non-GAAP net income guided $1.877B, up 25% year over year.

Operating cash flow $1.462B, up 147% year over year. Free cash flow $1.18B, up 169% year over year.

Q2 repurchased $478M. $9.5B remaining authorization.

In May, agreed to sell ZT manufacturing business to Sanmina for $3B in cash and stock. Expected to close by end of 2025, subject to regulatory approval.

Q3 guidance excludes MI308 shipments. US export license application still pending. Most MI308 inventory is WIP (unlike H20 finished goods), so shipments will still take time.

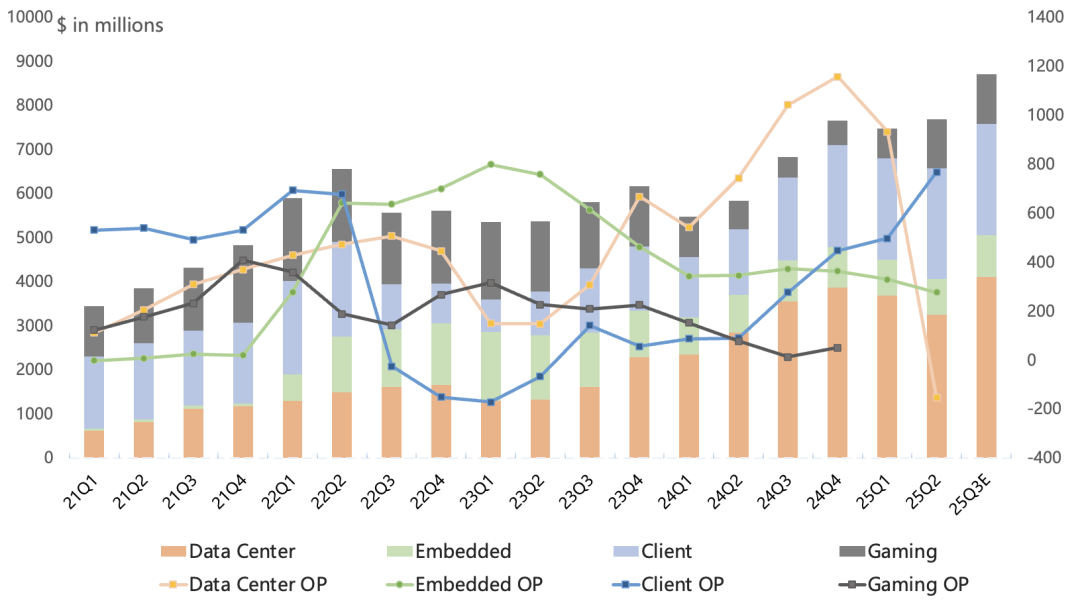

Q2 by Segment:

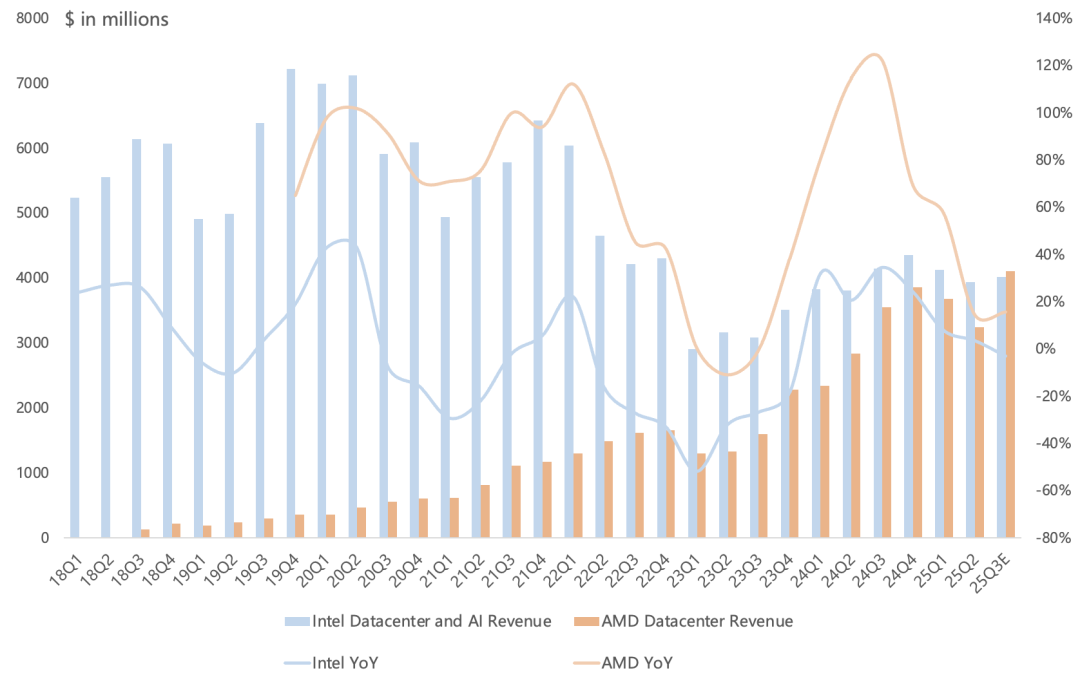

Data Center revenue $3.24B, up 14% year over year, 42% of revenue. Operating loss $155M.

CPU: Zen 5 EPYC Turin CPU shipments ramped significantly. Overall server CPU revenue hit records in cloud and enterprise. Market share grew for the 33rd consecutive quarter. >100 new EPYC-powered cloud instances launched this quarter, including multiple Turin instances from Google and Oracle Cloud. ~1,200 EPYC cloud instances available globally. EPYC enterprise deployments grew significantly QoQ, driven by new wins in large tech, auto, manufacturing, financial services, and public sector. Remain optimistic on server CPU business.

GPU: Data Center GPU revenue declined this quarter mainly due to MI308 export ban and MI325-to-MI350 transition. Partnered with Oracle to deploy a multi-billion-dollar large-scale cluster driven by MI355X + EPYC Turin + Polara 400 NIC, >27K nodes, 8-9 month delivery. MI350 series began volume production in June. Q3 capacity expected to ramp quickly. Announced multi-billion-dollar collaboration with Humane to build AI infrastructure entirely on AMD CPU, GPU, and software. MI400 series development on track for 2026 launch. Launched developer cloud, but not a meaningful revenue contributor. Data Center GPU gross margin still slightly below corporate average, expected to improve long-term.

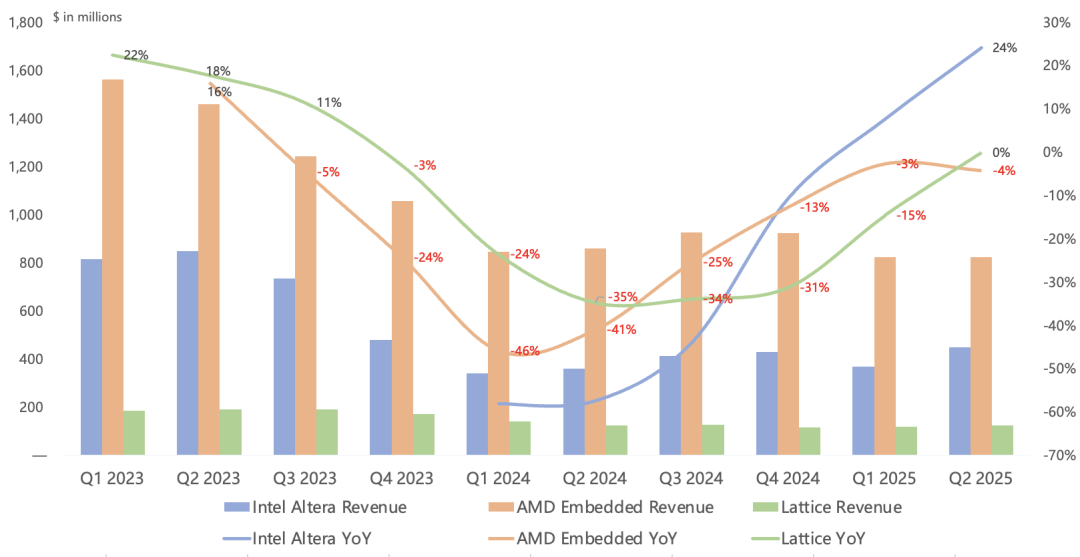

Embedded revenue $824M, down 4% year over year, eighth consecutive quarter of decline, 11% of revenue. Operating income $275M, down 20% year over year. Embedded demand recovering; Q2 shipments improved. Strong performance across most markets offset by industrial weakness and inventory digestion, underperforming Intel Altera and Lattice. Expect test & measurement, communications, and aerospace demand improvement to drive Embedded back to growth in 2025.2025 design wins may exceed 2024's record $14B.

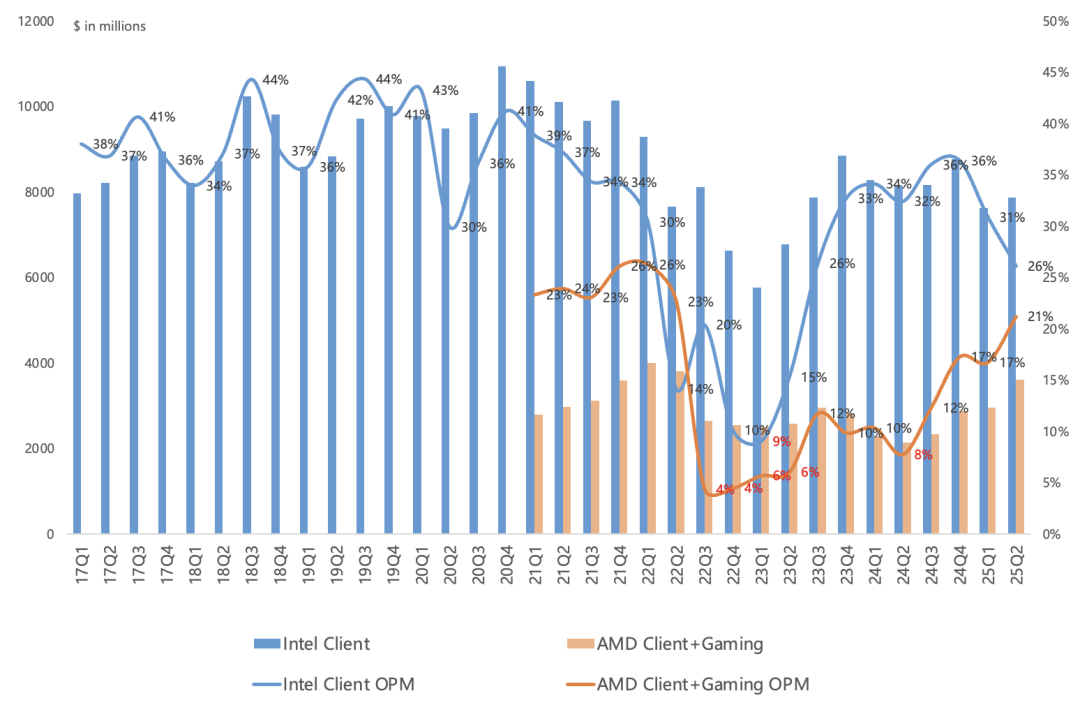

Client revenue $2.499B, up 68% year over year, 33% of revenue. Gaming revenue $1.122B, up 73% year over year, ending 10 consecutive quarters of decline, 15% of revenue. Combined Client & Gaming operating income $767M, up 362% year over year. Operating margin 21%, still below Intel's 26%, but trend suggests overtaking Intel is not far off.

Client growth driven by desktop CPUs. X3D series demand strong. Desktop channel CPU sales hit records. Ryzen CPUs held top spot on global major e-commerce bestseller lists all quarter. Notebook CPU shipments up double digits year over year, driven by commercial notebook share gains. ASP also rising. Expect PC growth to exceed industry average over next several quarters. Q2 saw little tariff-driven pull-forward.

Gaming: Semi-custom revenue up significantly year over year. Console channel inventory normalized. Customers building for holiday season. Q4 console business will actually decline double digits sequentially. Combining Client and Gaming reporting enables better comparison with Intel Client.

Q3 2025 revenue guided $8.7B, up 28% year over year, up 13% sequentially. Data Center guided up double digits sequentially. Client & Gaming guided up low single digits sequentially, with Client revenue growing and Gaming roughly flat. Embedded guided up sequentially.

2025 revenue guided high double-digit year-over-year growth. Data Center and Client high double-digit year-over-year growth. Semi-custom to grow for full year. Embedded to return to year-over-year growth in H2. (Unchanged)

Outlook: AI business revenue can reach annualized tens of billions scale, but no guess on exact timing.

Revisiting the Previous Quarter's View:

Overall, this quarter still relied on traditional PC and server CPU businesses. MI308 export controls eased but process incomplete; WIP inventory means shipments miss Q3. Lisa still unwilling to give full-year AI revenue guidance to reassure investors, only vaguely saying future can annualize to tens of billions. 2025 non-GAAP net income essentially locked at $6-7B. H2 MI350 unlikely to bring more surprises. Next year's MI400 rack product is the key focus.