Key Takeaways:

AMD's Q3 earnings may be the best in its history, with notebooks and data center firing on all cylinders and a perfect next-gen console launch.

EPYC begins to threaten Intel's data center; AMD's data center outlook remains optimistic.

Acquiring Xilinx's "money printer," AMD starts learning from NVIDIA.

A few years ago, data center rebuilt Intel. Now, NVIDIA and AMD formally counterattack the incumbent Intel, carving out an independent data center narrative.

AMD, which typically reports after hours, suddenly pre-announced the Xilinx acquisition before the open, capturing the market's attention. The spotlight seemed to shift from what was an exceptionally bright Q3 report. The report shows AMD steadily eating into Intel's share, in both PC and data center.

Possibly the best earnings report in AMD's history

AMD Q3 Earnings Summary:

Revenue $2.801B, up 56% year over year and 45% sequentially, a record high. Prior guidance $2.55B.

GAAP gross margin 44%, flat versus prior guidance.

Operating income $449M, up 141% year over year and 160% sequentially, highest since 2010.

GAAP net income $390M, up 225% year over year and 146% sequentially, highest since 2011.

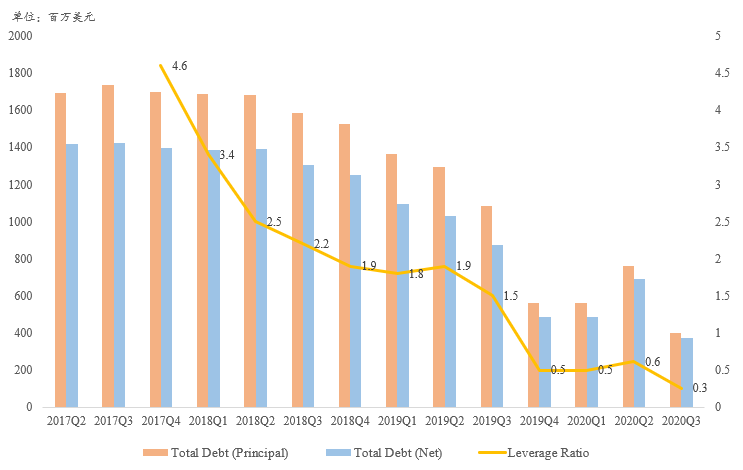

Notably, AMD's leverage further declined this quarter, with interest-bearing debt principal down 48% sequentially, fully shedding its historical baggage. This deleveraging underpins the Xilinx acquisition.

Notebook business sets another record! Next-gen console business off to a perfect start

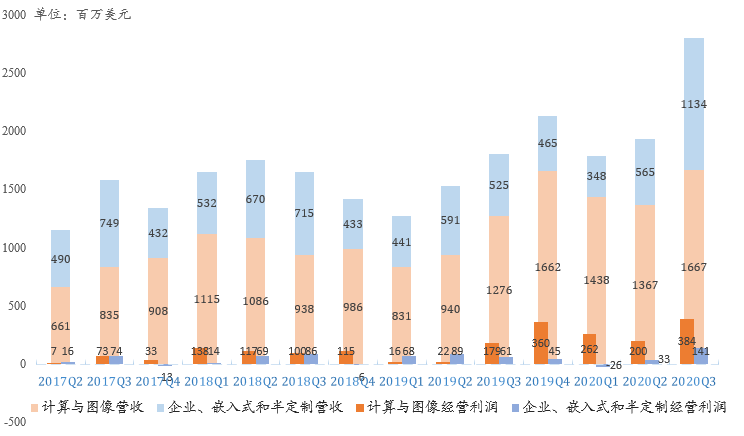

AMD Q3 Computing & Graphics revenue $1.667B, up 30.6% year over year and 21.9% sequentially; operating income $384M, up 114.5% year over year.

The notebook business we have long favored continues to deliver. This quarter notebook CPU shipments and revenue both hit record highs, driving total PC CPU revenue to a record. AMD has gained PC CPU share versus Intel for 12 consecutive quarters. "Ruthless" is that AMD's desktop and notebook ASPs both rose sequentially, in sharp contrast to Intel.

On graphics, with no new desktop GPUs yet, revenue was driven mainly by Apple notebook shipments, down year over year but up sequentially, with limited impact.

Notebook CPU accounts for a large share of the Computing & Graphics segment.

After seven years, the next-gen consoles PS5 and Xbox Series X have arrived. PS5 pre-orders are red-hot, with units impossible to find; some Wall Street analysts even think PS5 lifetime sales could set a record.

Based on history and management commentary, consoles typically need 4-6 quarters to ramp meaningfully, so we have been cautious. But given the explosive PS5 pre-orders and NVIDIA RTX 30 pre-orders, the gaming industry is entering its best-ever period, and AMD's console business is off to a far stronger start than expected.

AMD Q3 Enterprise, Embedded & Semi-Custom revenue $1.134B, up 116% year over year and 101% sequentially. Operating income $141M, up 131% year over year. Management says Q4 console demand is explosive and will grow sequentially.

EPYC begins to threaten Intel's data center; AMD outlook remains optimistic

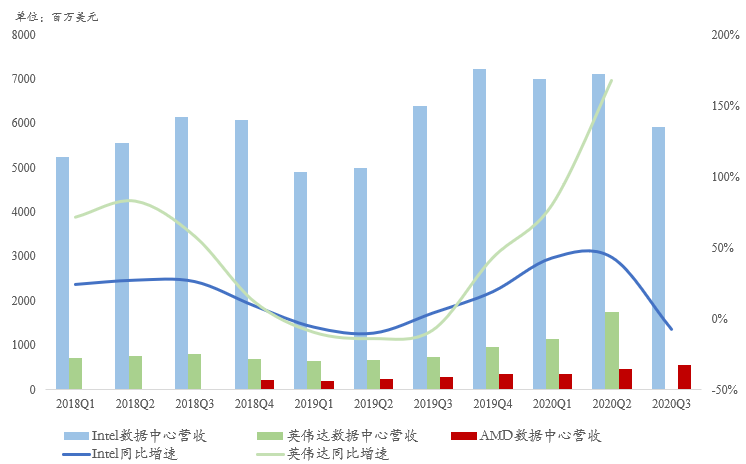

Intel's Q3 miss was driven mainly by a sharp data center shortfall. We previously viewed Intel's data center as a bellwether for AMD and NVIDIA. Does that mean AMD and NVIDIA data center will also miss? The answer is no.

Intel's data center ASP and shipments have now fallen sequentially for two consecutive quarters, with Q3 ASP down 14% sequentially. Intel's data center operating margin fell to 32.2%, a record low.

By contrast, AMD's EPYC revenue set another record, doubling year over year with double-digit sequential growth. But data center GPU remains soft, only growing sequentially — consistent with our view that AMD's data center benchmark is Intel. We estimate EPYC Q3 revenue around $490M, with data center GPU around $60M.

Intel's Q4 data center outlook was deeply pessimistic, guiding broad data center down 25% year over year. Yet memory giants Micron and SK Hynix were uniformly upbeat on data center. AMD likewise: while raising Q4 guidance strongly, it expressed strong optimism on data center. The next-gen EPYC Milan is expected to ship in Q4 and ramp broadly in Q1, going head-to-head with Intel's new Ice Lake server CPUs.

Acquiring Xilinx's money printer, AMD starts learning from NVIDIA

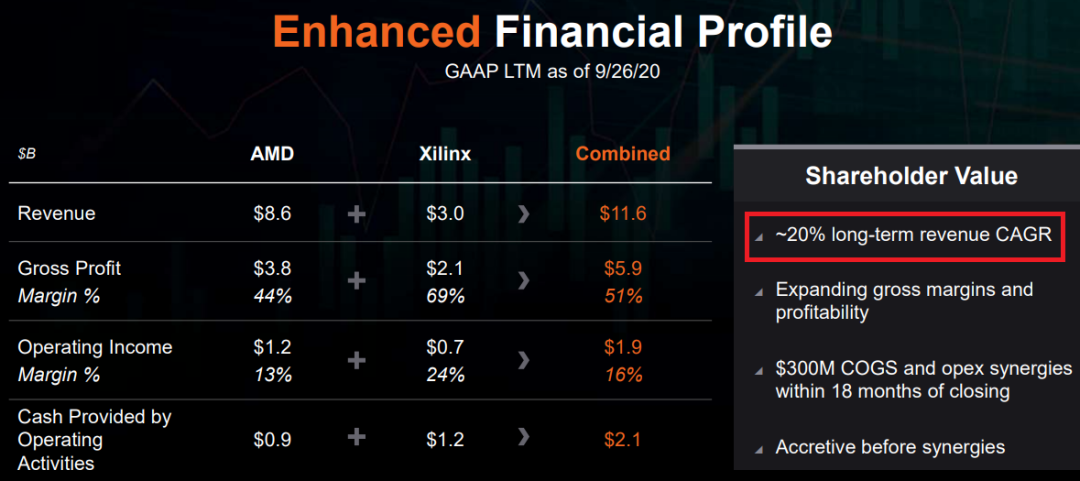

AMD pre-announced a $35B all-stock acquisition of FPGA leader Xilinx before the open yesterday, expected to close by end of 2021.

We previously noted that massive interest-bearing debt, causing interest expense multiples of peers, was a heavy burden for AMD, making debt a key metric to track. The ideal approach was therefore a stock deal for Xilinx.

The market's main refrain on AMD buying Xilinx is to compare it with Intel's acquisition of FPGA runner-up Altera, questioning the deal's prospects. But it's easy to overlook that despite a small, low-growth FPGA market, Xilinx maintains exceptionally high and stable profitability.

An interesting detail in AMD's deal deck: previously AMD guided a 20% 5-year revenue CAGR; the combined CAGR is still shown as 20%. Why?

The first analyst on the call asked this, but Lisa did not directly answer. We believe it's because Xilinx's performance has essentially plateaued at current levels. So is Xilinx worth it?

Yes.

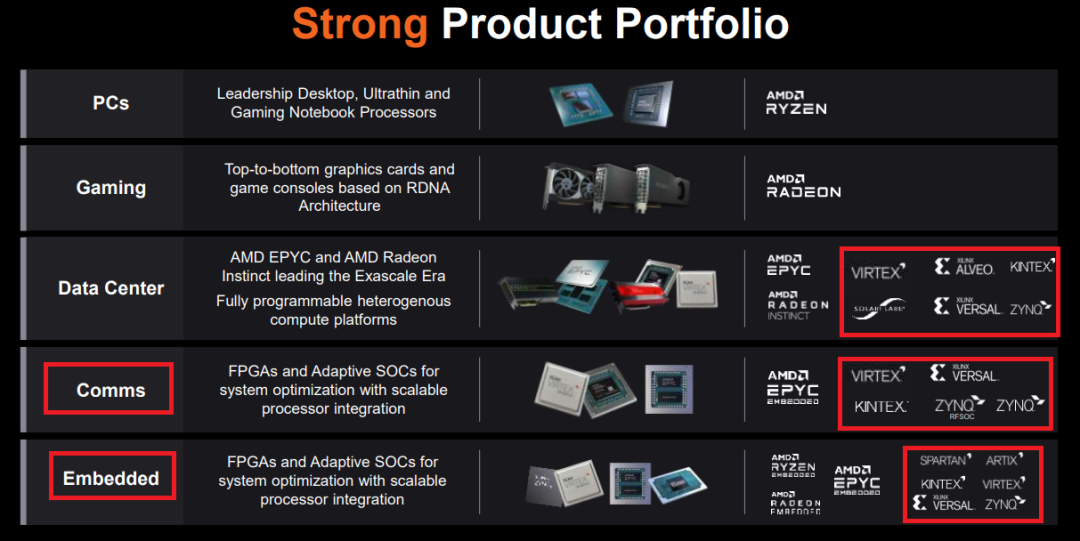

In recent quarters, Intel's data center 5G SoC has been a bright spot; NVIDIA's Mellanox acquisition brought DPU and a focus on 5G. Only AMD was distant from 5G. Buying Xilinx lets AMD enter the massive communications market and cross-sell its own data center CPUs.

Xilinx's automotive business is also highly attractive to AMD. Intel has Mobileye, NVIDIA has autonomous driving chips, while AMD has a blank slate.

Xilinx possesses advanced 2.5D/3D packaging technology, which combined with AMD's refined process design capabilities is a compelling picture.

Xilinx excels in software; AMD wants to learn from NVIDIA and enrich its software ecosystem.

In short, facing a Xilinx that barely grows but prints money like a mint, Lisa couldn't resist — especially in an all-stock deal.

Conclusion

This year the pandemic accelerated the explosion of the notebook, gaming, and data center markets. On top of that, next-gen consoles PS5 and Xbox Series X pre-orders were exceptionally hot, driving AMD's results to historic highs. The Xilinx acquisition fills out the product matrix, giving AMD's data center the confidence to compete head-to-head with Intel and NVIDIA.

A few years ago, data center rebuilt Intel. Now, NVIDIA and AMD formally counterattack the incumbent Intel, carving out an independent data center narrative. The tech world is that ruthless.