As noted in the previous AMD earnings article:

This quarter AMD raised full-year AI GPU revenue by another $500M to $4.5B+.

AMD Q2 Earnings:

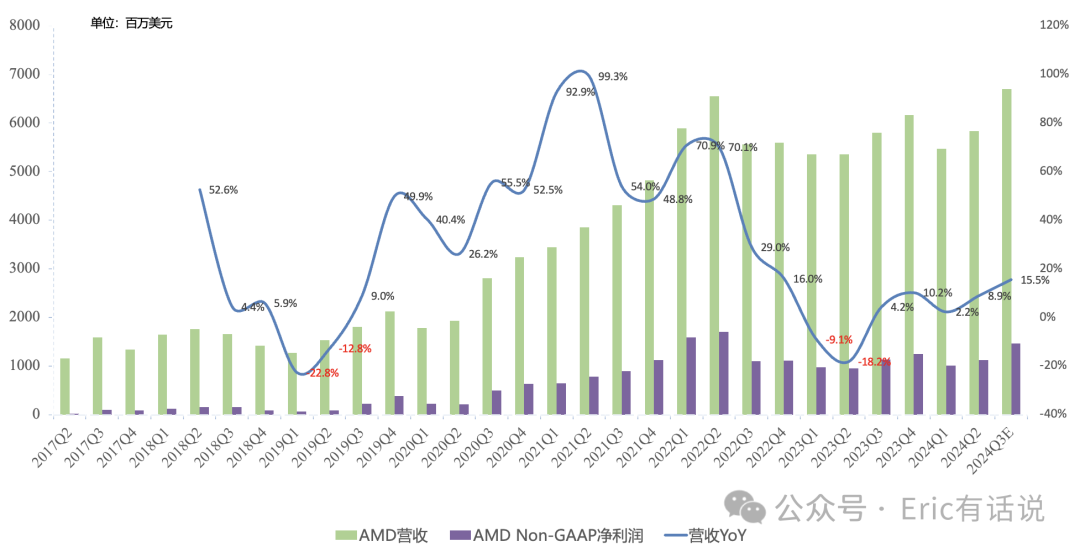

Revenue was $5.835B, up 9% year over year and 7% sequentially, modestly above the prior $5.7B guide.

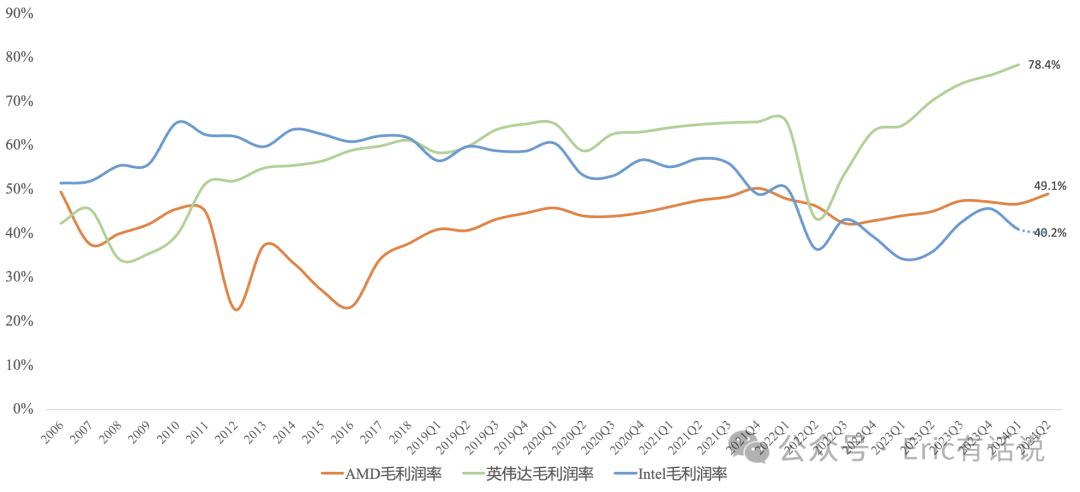

GAAP gross margin was 49.1%, Non-GAAP gross margin was 53.1%, both up sequentially.

GAAP operating income was $269M, swinging from a loss year over year and up sharply sequentially; Non-GAAP operating income was $1.264B, up 18% year over year; Q3 Non-GAAP operating income is guided at $1.685B, up 32% year over year.

GAAP net income was $265M, up sharply both year over year and sequentially; Non-GAAP net income was $1.126B, up 19% year over year, but still below the 2022Q2 peak of $1.7B; Q3 Non-GAAP net income is guided at $1.466B, up 29% year over year.

Operating cash flow was $593M, up 56% year over year, below the prior peak of $1.0B in 2022Q2; free cash flow was $439M, up 73% year over year.

Q2 share repurchases were $352M, with $5.2B remaining under the authorization.

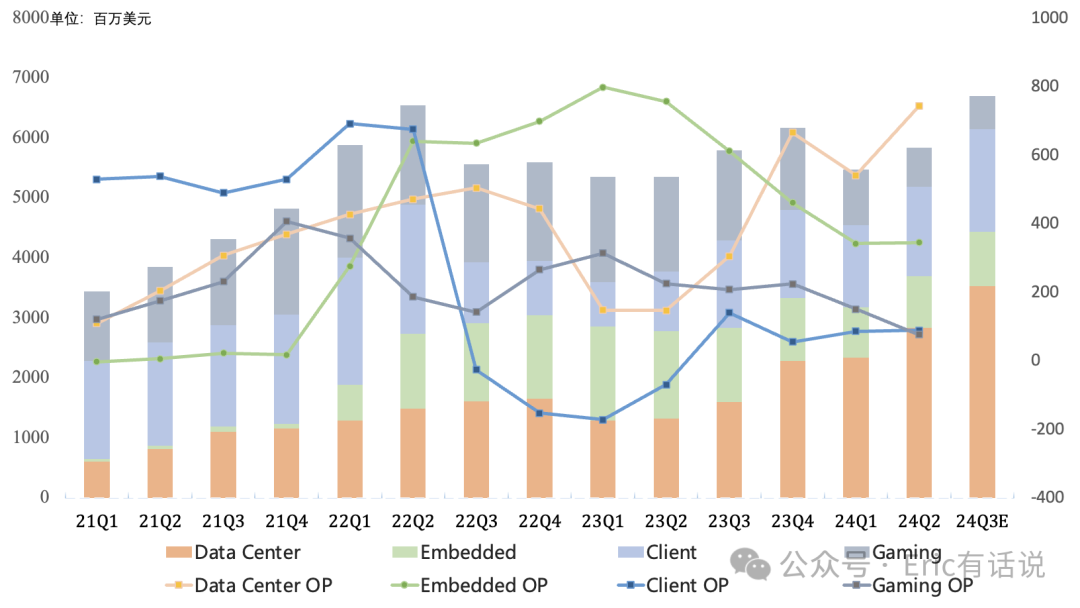

Q2 by Segment:

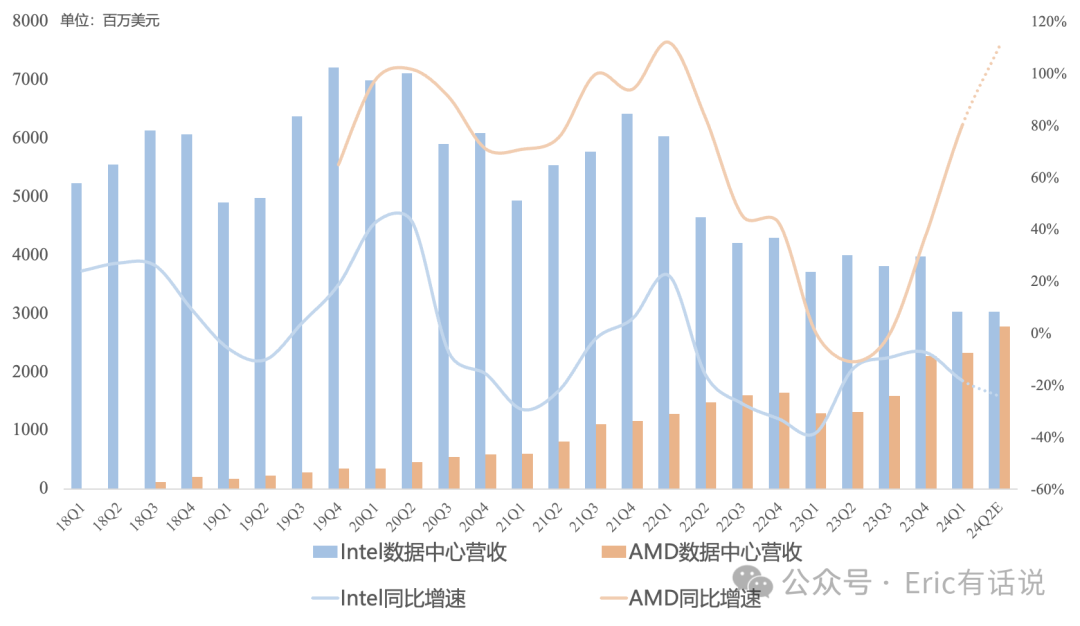

Data Center revenue was $2.834B, up 115% year over year, accounting for 49% of revenue; operating income was $743M, up 405% year over year, remaining AMD's highest-margin business.

EPYC revenue continued double-digit year-over-year growth; cloud demand is strong, with hyperscalers continuing to procure Zen 4 EPYC; public cloud instances running EPYC exceeded 900, up 34% year over year; enterprise revenue grew double digits sequentially, with over one-third of new enterprise wins coming from first-time EPYC customers; next-gen Zen 5 Turin began shipping to lead cloud customers in Q2, contributing revenue in the second half; the traditional server CPU market shows signs of recovery, and server CPU share is expected to keep rising.

Data Center GPU revenue set a new quarterly record for the third consecutive quarter; MI300 series quarterly revenue exceeded $1B; Microsoft became the first hyperscaler to deploy MI300X this quarter; enterprise and cloud AI customer pipeline for the MI300 series expanded; this quarter, data center GPU revenue was predominantly from AI customers, with supercomputing a small share; going forward, data center GPUs will refresh annually; the large-memory MI325X launches later this year, contributing revenue in Q4; 2025 H2 MI350 series with CDNA 4 architecture delivers a 35x performance uplift over CDNA 3; 2026 MI400 with CDNA Next architecture.

Q3 Data Center GPU revenue is expected to grow by over $200M sequentially; 2024 full-year revenue is raised from $4.0B to $4.5B+.

Embedded revenue was $861M, down 41% year over year (Lattice revenue was $124M, down 35% year over year), accounting for 15% of revenue; operating income was $345M, down 54% year over year (Lattice operating income was $22M, down 58% year over year); customers are still destocking; Q1 was the revenue trough, with early signs of recovery; a slow recovery is expected in the second half, with sequential quarterly growth; first-half design wins exceeded $7B, up 40% year over year, including hundreds of millions from adaptive and x86 compute products.

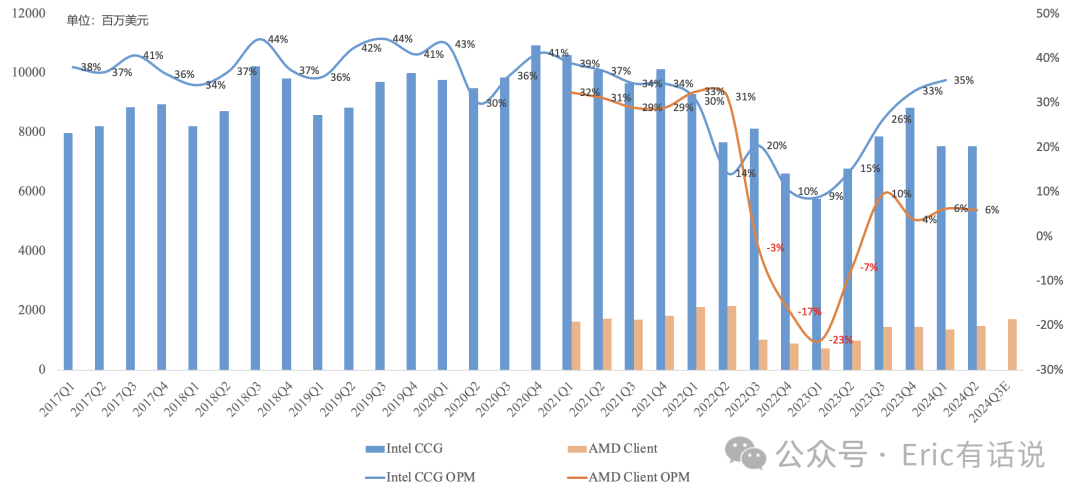

Client revenue was $1.492B, up 50% year over year, accounting for 26% of revenue; operating income was $89M, profitable for the fourth consecutive quarter, but operating margin was only 6%, still far below Intel; Ryzen 8000 series demand is strong; desktop Zen 5 Ryzen 9000 series and notebook Zen 5 Ryzen AI 300 series begin volume shipping in Q3, with the latter spanning premium, gaming, and commercial platforms; full-year PC CPU share is expected to keep rising, with above-typical seasonality in the second half.

Gaming revenue was $648M, down 59% year over year, the seventh consecutive quarterly decline, accounting for 11% of revenue; operating income was $77M, down 66% year over year; semi-custom revenue declined year over year; the current console generation is in its fifth year; gaming GPU revenue grew year over year; Q3 gaming revenue is expected to decline double digits sequentially; the second half will be worse than the first.

Q3 revenue is guided at $6.7B, up 16% year over year and 15% sequentially; Data Center and Client revenue are expected to grow double digits sequentially, Embedded to grow single digits, and Gaming to decline double digits.

Revisiting the Previous Quarter's View:

Overall, 2024 is a significant fundamental improvement opportunity for AMD; revenue is very likely to surpass the 2022 all-time high, but whether margins can sustainably expand in the second half remains the key valuation driver; near-term Non-GAAP full-year net income expectations are revised to $6B-$7B.

Full-year revenue hitting a new all-time high looks assured, with a shot at $25B. The bigger issue is the pace of margin improvement—first three quarters Non-GAAP net income is only ~$3.6B, so full-year net income may need to be lowered to ~$6B. AMD still has a latent profit inflection point that has yet to materialize: the Client business, i.e., PC—not AI PC per se, but the 6% operating margin versus Intel's 30%+ and AMD's own ~30% in 2021 leaves enormous upside.

On the market's top concern, AI GPU, full-year revenue guidance is now $4.5B+; combined with EPYC momentum, 2024 Data Center revenue could reach ~$13B; at a 25% operating margin that implies ~$3.3B of operating income, a very respectable contribution to AMD's own growth; Q3 also has a shot at unlocking the milestone of Data Center quarterly revenue surpassing Intel's for the first time.

Overall, the positives—strong EPYC and AI GPU demand, stable PC growth, Xilinx stabilizing—outweigh the negative of gaming being weaker than expected.

Returning to my longstanding concerns on AMD:

1) Whether Arm-based server CPUs, led by NVIDIA, can disrupt the incumbent x86 server CPU market (under observation).

2) Xilinx deceleration (now stabilizing).

3) Process technology bottleneck, Intel outsourcing to TSMC (Qualcomm Windows on Arm challenging x86, under observation).