Previously in the Intel earnings post I noted:

Now it appears spot on. The market still has high expectations for AMD AI GPU revenue ($3.5B raised to $4B vs market expectation of $6B), and everyone still wants to take a swing at NVIDIA.

AMD Q1 Results:

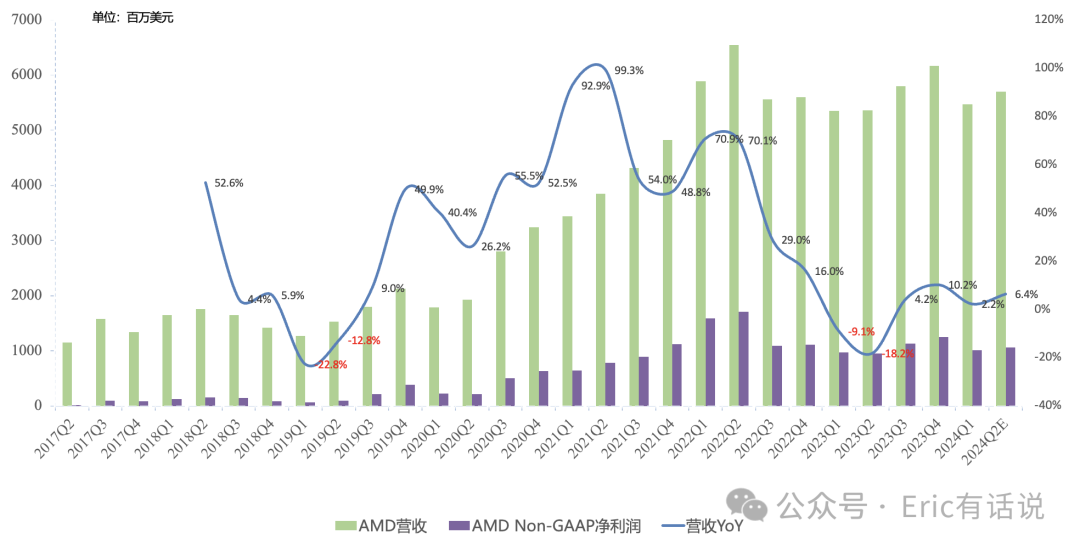

Revenue was $5.473B, up 2% year over year, down 11% sequentially, slightly above prior guidance of $5.4B.

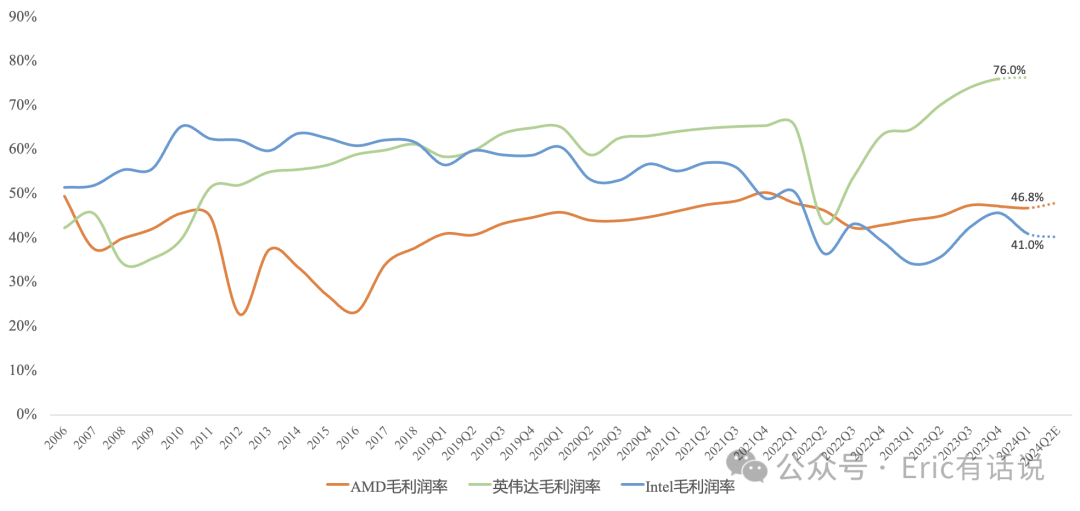

GAAP gross margin 46.8%, Non-GAAP gross margin 52.3%, up slightly sequentially.

GAAP operating income was $36M, swinging from a loss year over year, down 89% sequentially; Non-GAAP operating income was $1.133B, up 3% year over year, down 20% sequentially; guided Q2 Non-GAAP operating income of $1.221B, down 14% year over year.

GAAP net income was $123M, swinging from a loss year over year, down 82% sequentially; Non-GAAP net income was $1.062B, up 12% year over year, but still below the 2022 Q2 peak of $1.7B; guided Q2 Non-GAAP net income of $1.062B, up 12% year over year.

Operating cash flow $521M, up 7% year over year, up 37% sequentially, previous peak was 2022 Q2 at $1B; free cash flow $379M, up 16% year over year.

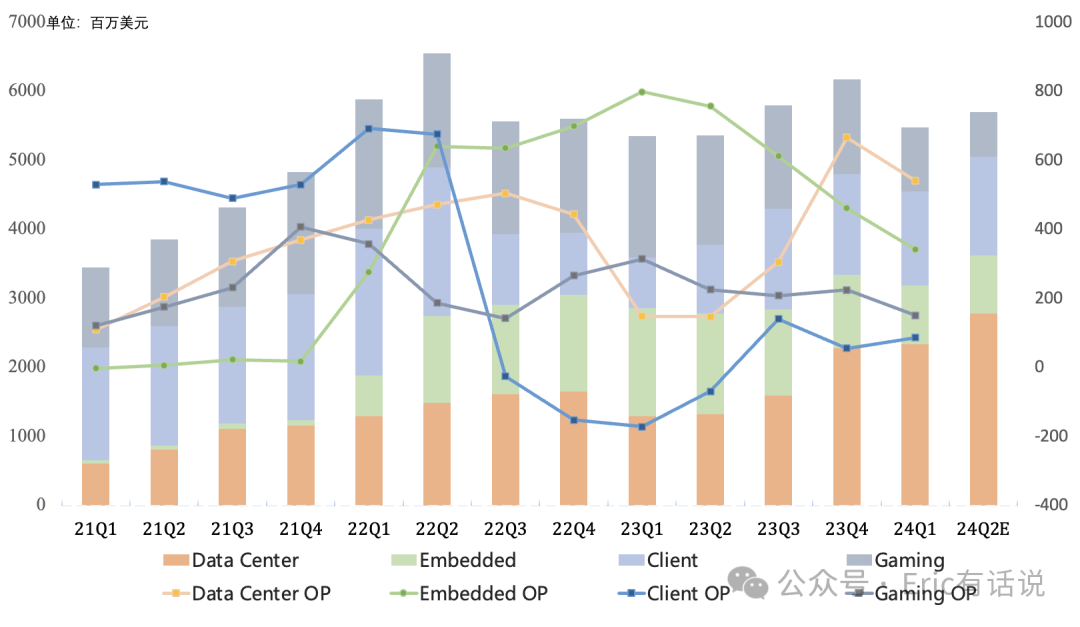

Q1 Segment Results:

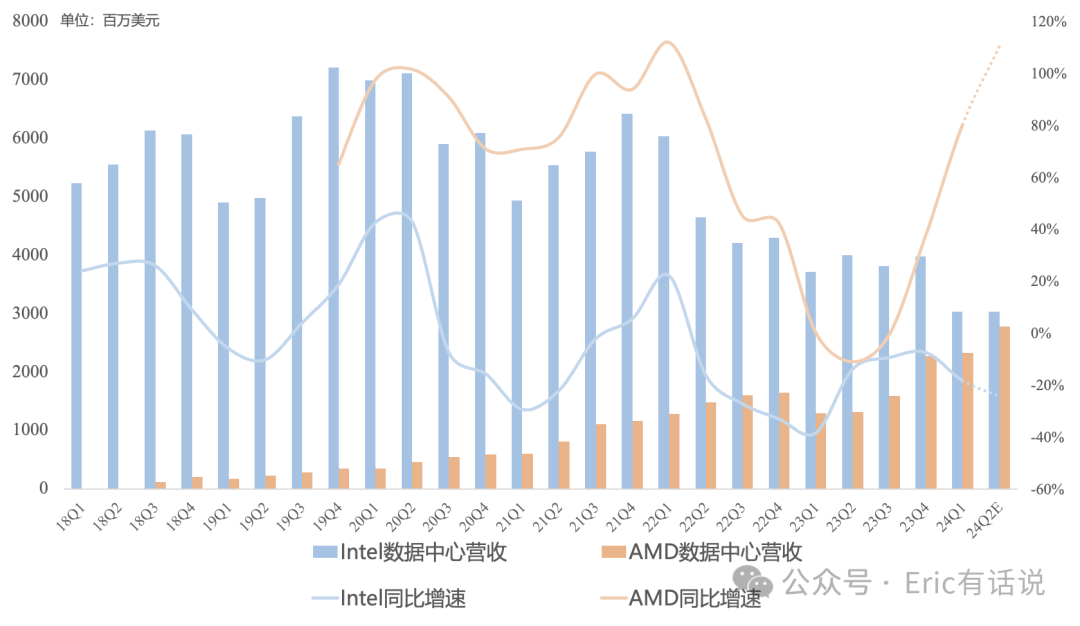

Data Center revenue was $2.337B, up 81% year over year, accounting for 43% of revenue; operating income $541M, up 266% year over year, down 19% sequentially, still AMD's highest-margin business.

EPYC revenue continued double-digit year-over-year growth, down sequentially due to seasonality; overall server CPU share continues to rise; Enterprise demand recovering; despite Cloud demand divergence, hyperscalers continue purchasing Zen4 EPYC; next-gen Zen5 Turin sampling, server partners on Zen5 platform to be 30% more than Zen4, launching late this year.

Data Center GPU revenue set a record for the second consecutive quarter; MI300X ramping rapidly, cumulative revenue >$1B; >100 enterprise and AI customers deploying or planning to deploy MI300X.

Guided 2024 Q2 Data Center GPU revenue up >$200M sequentially, but margin still below Data Center average; 2024 revenue raised from $3.5B to >$4B.

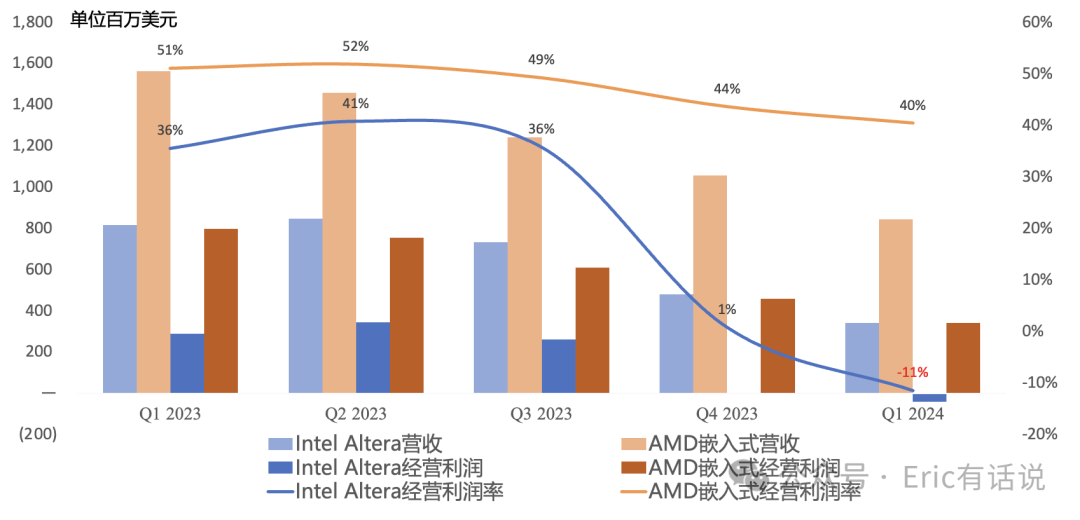

Embedded revenue was $846M, down 46% year over year (Intel Altera revenue $342M, down 58% year over year), accounting for 15% of revenue. Operating income was $342M, down 57% year over year (Intel Altera operating loss $39M). Customers are still destocking; communications market is weak; industrial and automotive are soft. Q2 is expected to be flat sequentially, with recovery in the second half.

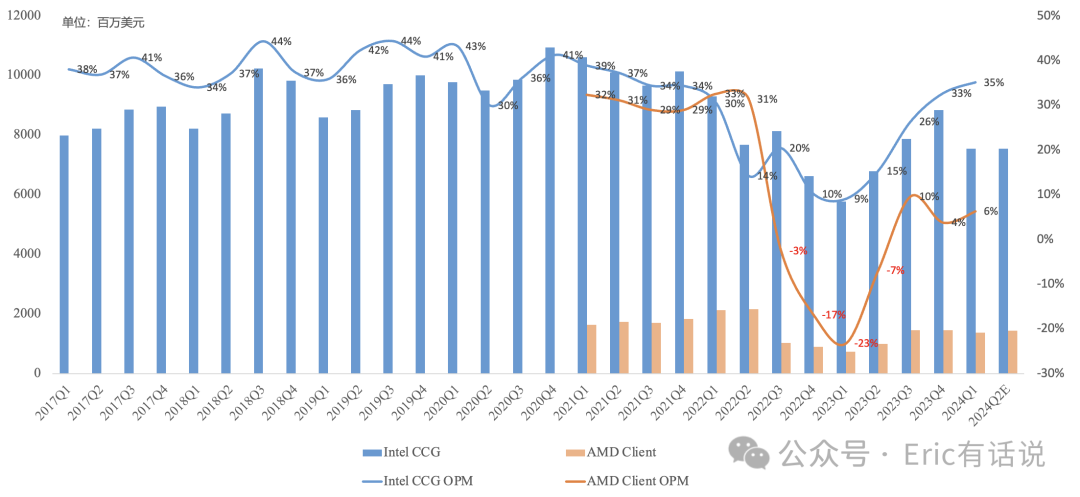

Client revenue was $1.368B, up 85% year over year, down 6% sequentially, accounting for 25% of revenue; operating income was $86M, profitable for the third consecutive quarter, but operating margin remained far below Intel's (6% vs 35%); Q1 Ryzen 8000 series demand was strong, desktop revenue up high double digits year over year, notebook revenue nearly doubled year over year; commercial Ryzen Pro series poised to continue gaining share; Zen5 notebook AI PC product Strix launching later this year, expected to continue gaining full-year PC CPU share with volume and price rising in H2.

Gaming revenue was $922M, down 48% year over year, sixth consecutive quarterly decline, down 33% sequentially, accounting for 17% of revenue; operating income $151M, down 52% year over year; semi-custom revenue down year over year; game consoles in year 5 of this generation; Gaming GPU revenue down year over year and sequentially; Gaming margin remains below company average; guided Q2 Gaming revenue down 30% sequentially, H2 to continue declining vs H1.

Guided Q2 revenue of $5.7B, up 6% year over year, up 4% sequentially; Data Center revenue expected to grow double digits sequentially, with Data Center GPU contributing over $200M of sequential growth; Embedded revenue expected to be flat sequentially; Client revenue expected to grow sequentially; Gaming revenue expected to decline 30% sequentially.

Guided full-year 2024 company revenue to grow year over year.

Overall, 2024 is a major opportunity for AMD's fundamentals to improve; I believe revenue will likely surpass the 2022 record high, but whether margins can sustain improvement in H2 remains the key valuation driver; Non-GAAP annual net income near-term expectation lowered to $6-7B.

Regarding the most-watched AI GPU, full-year revenue guidance was raised to $4B+; assuming server CPU revenue grows modestly year over year, 2024 Data Center revenue would be ~$11B; at a 25% margin that implies $2.8B profit, a very significant contribution to AMD's own growth, and could even unlock the milestone of Data Center quarterly revenue surpassing Intel for the first time in history as early as Q3, but the market wants more, and AMD still isn't firing on all cylinders.

Good news: EPYC Enterprise demand recovering, Xilinx margins holding; bad news: Gaming weaker than expected, AI GPU margins clearly constrained.

Back to my longstanding concerns on AMD:

1) Whether Arm-based server CPUs, led by NVIDIA, can disrupt the incumbent x86 server CPU market (under observation).

2) Xilinx significantly slowing (continuing to slow)

3) Process technology bottleneck, Intel outsourcing to TSMC (Qualcomm Win on Arm challenging x86, watching)

Now may need to add: Gaming weaker than expected.