This quarter AMD did not provide full-year AI GPU revenue scale guidance.

AMD Q1 Results:

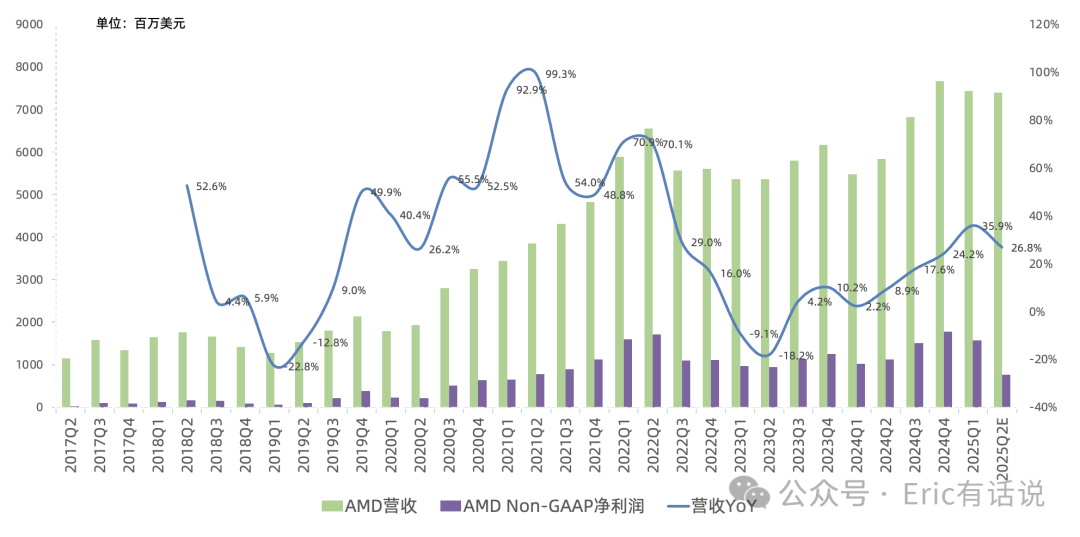

Revenue $7.438B, up 36% year over year, down 3% sequentially, slightly above prior guidance of $7.1B; expecting Q2 revenue $7.4B, up 27% year over year, down slightly sequentially;

GAAP gross margin 50.2%, Non-GAAP gross margin 53.7%, both down slightly sequentially;

GAAP operating income $806M, Non-GAAP operating income $1.779B, up 57% year over year; expecting Q2 Non-GAAP operating income $882M, down 30% year over year, due to MI308 export restriction impact;

GAAP net income $709M, Non-GAAP net income $1.566B, up 55% year over year; expecting Q2 Non-GAAP net income $763M, down 32% year over year;

Operating cash flow $939M, up 80% year over year; free cash flow $727M, up 92% year over year;

Q1 repurchased $749M, with $4B remaining under the authorization;

ZT acquisition completed; for the ZT design team, quarterly operating expense increase is approximately $50M;

MI308 export restriction results in an $800M charge next quarter and reduces next quarter revenue by $700M, Non-GAAP gross margin declining to 43%, excluding this impact Non-GAAP gross margin 54%; MI308 restriction reduces full-year revenue by $1.5B (vs. 2024 AI revenue of $5B, China exposure proportion relatively high), primarily impacting Q2 and Q3, with minimal Q4 impact;

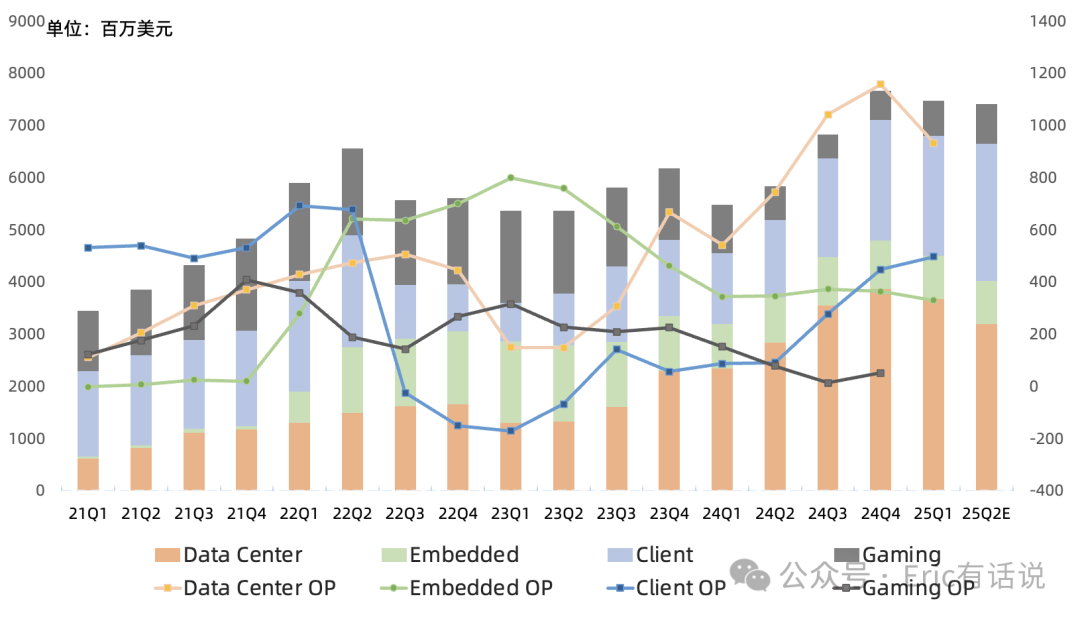

Q1 Segment Results:

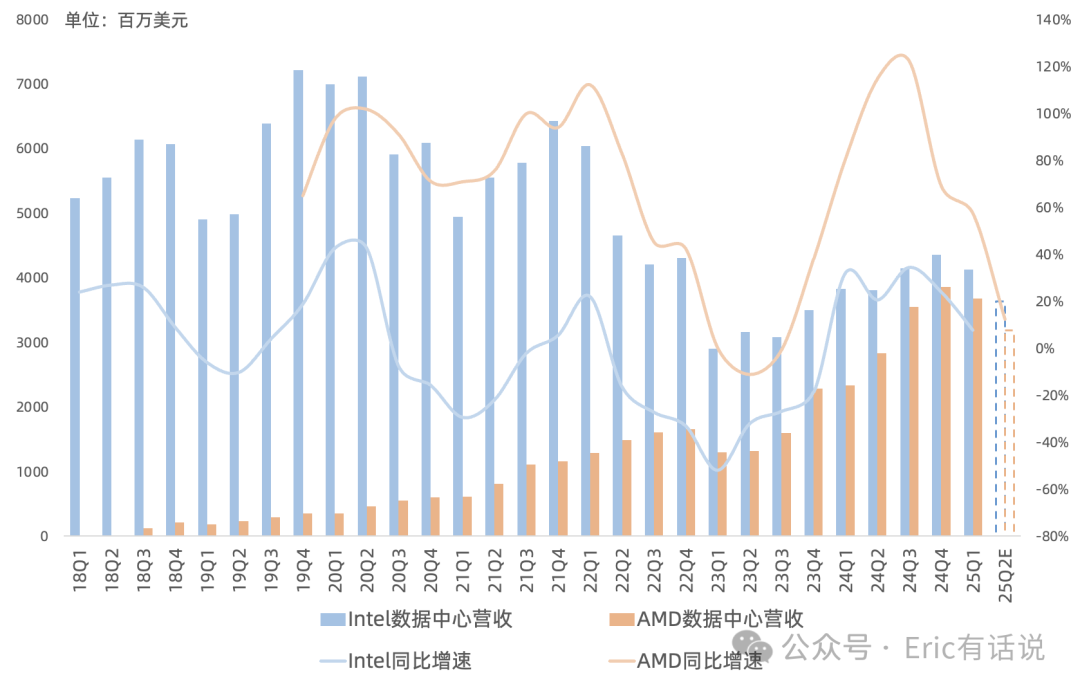

Data Center revenue $3.674B, up 57% year over year, accounting for 49% of revenue; operating income $932M, up 72% year over year, remains AMD's highest-margin business;

On the CPU side, driven by Zen 5 EPYC Turin and Zen 4 EPYC demand, EPYC revenue (~$2B) achieved double-digit year-over-year growth for the seventh consecutive quarter, down slightly sequentially; server CPU market share continues to rise; hyperscale and enterprise customer demand remains strong; Forbes Global 2000 enterprise customer EPYC cloud instance count grew more than 2x year over year; Zen 5 EPYC began validation production at TSMC Arizona Fab in April, first products expected to ship in H2; Zen 6 EPYC Venice to debut on TSMC 2nm HPC process; Lisa noted EPYC enterprise market share is still relatively low, with significant room for growth;

On the GPU side, this quarter Data Center GPU revenue grew only double digits year over year, down significantly sequentially ($1.3B), missing market expectations, primarily composed of MI325 and MI300 series; expecting excluding export restriction impact, H1 Data Center GPU revenue flat year over year, but full-year Data Center GPU revenue to grow high double digits year over year as MI350 series ramps in H2; 2028 AI Accelerator chip market TAM $500B, long-term CAGR 60%; Lisa believes GPU is more competitive than ASIC in inference;

Embedded revenue $823M, down 3% year over year, seventh consecutive quarter of decline, accounting for 11% of revenue; operating income $328M, down 4% year over year; embedded demand continues to recover gradually, book-to-bill continues to improve, demand improvement in test, communications, and aerospace will drive a return to growth in H2 2025, while industrial remains weak;

Client revenue $2.294B, up 68% year over year, accounting for 31% of revenue; Gaming revenue $674M, down 27% year over year, tenth consecutive quarter of decline, accounting for 9%; combined Client and Gaming operating income $496M, Gaming likely operating at a loss, Client operating margin ~22%, still below Intel's 31%;

Lisa stated that Q1 Client revenue growth was unrelated to preemptive pull-forward orders to avoid tariffs (unlike Intel); PC revenue share has grown for five consecutive quarters.

Revenue

Half of the sequential revenue growth came from ASP improvement.

,

CPU unit volume actually declined double-digits sequentially.

But ASP hit a new high.

;

Desktop Ryzen channel shipments up over 50% year over year; notebook Ryzen AI 300 series revenue up over 50% sequentially; commercial Ryzen Pro PC unit shipments up over 30% year over year; HP, Lenovo, Dell, and ASUS launched AMD commercial models up 80% vs. 2024; company growth will exceed industry average;

In Gaming, semi-custom revenue continues to decline year over year; game console channel inventory has normalized; 2025 demand signals have strengthened; Gaming GPU revenue grew year over year; RDNA4 Radeon RX 9070 series demand strong; FSR4 now supports over 30 games, expecting 75 games by year-end; merging Client and Gaming reporting can mask Gaming weakness on one hand, and enable better comparison with Intel's Client business on the other;

Expecting 2025 Q2 revenue $7.4B, up 27% year over year, down 1% sequentially; expecting Q2 Data Center down sequentially, but Data Center CPU up sequentially, Client and Gaming up double digits sequentially, Embedded flat sequentially;

Expecting 2025 revenue up high double digits year over year; Data Center and Client businesses up high double digits year over year; semi-custom business to achieve full-year growth; Embedded business to return to year-over-year growth in H2;

Revisiting the Previous Quarter's View:

Overall, this quarter's performance was primarily driven by the PC and Server CPU businesses, with export controls weighing on the already weak AI performance in H1. H2 becomes more interesting: the long-weak Gaming and Embedded businesses begin to contribute growth, the consistently strong PC business begins to plateau, and the AI GPU business takes over from Server CPU as the primary growth driver for Data Center.

Management continues to indicate that H2 MI350 series shipment performance can drive full-year AI revenue high double-digit growth; a simple calculation implies H2 quarterly AI revenue above $2B. Given the export control impact (did not expect AMD's China AI exposure proportion to be this much higher than NVIDIA's), H1 Non-GAAP net income is only ~$2.3B, temporarily lowering Non-GAAP net income expectation to $6-7B.