This quarter AMD raised its full-year AI GPU revenue guidance by another $500M to above $5B.

AMD Q3 Earnings:

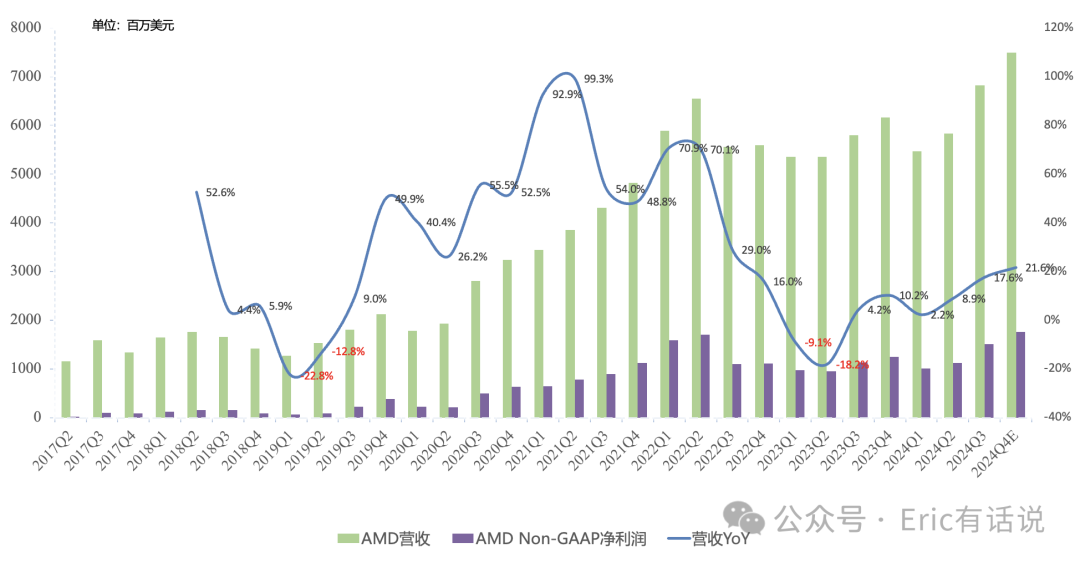

Revenue was $6.819B, up 18% year over year and 17% sequentially, slightly above the prior $6.7B guidance.

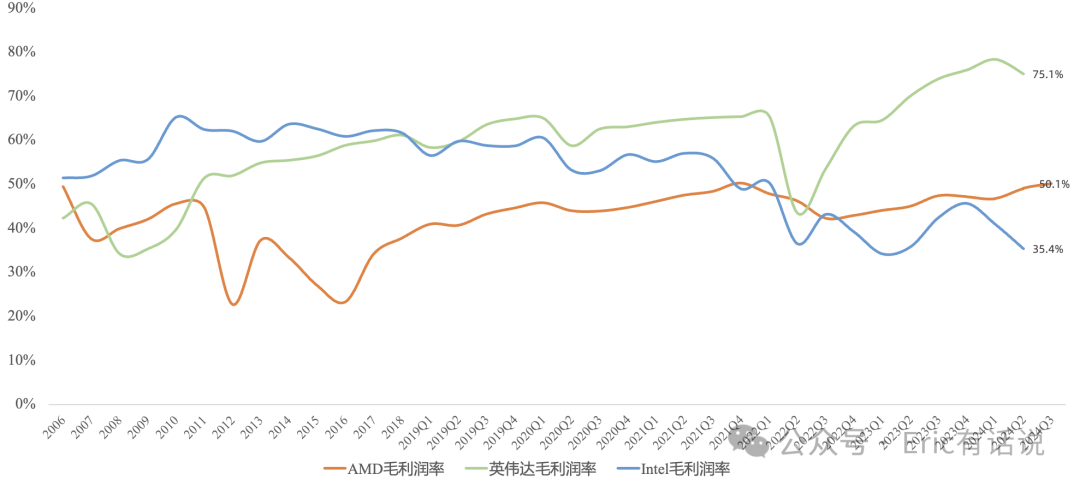

GAAP gross margin 50.1%, Non-GAAP gross margin 53.6%, both up modestly sequentially.

GAAP operating income $724M, highest since 2022 Q1. Non-GAAP operating income $1.715B, up 34% year over year. Q4 Non-GAAP operating income guided at $2B, up 42% year over year.

GAAP net income $771M, highest since 2022 Q1. Non-GAAP net income $1.504B, up 33% year over year. Q4 Non-GAAP net income guided at $1.755B, up 41% year over year, a new all-time high.

Operating cash flow $628M, up 49% year over year; prior historical high was $1B in 2022 Q2. Free cash flow $496M, up 63% year over year; prior historical high was $900M in 2022 Q1.

Q3 repurchased $250M; $4.9B remains under the authorization.

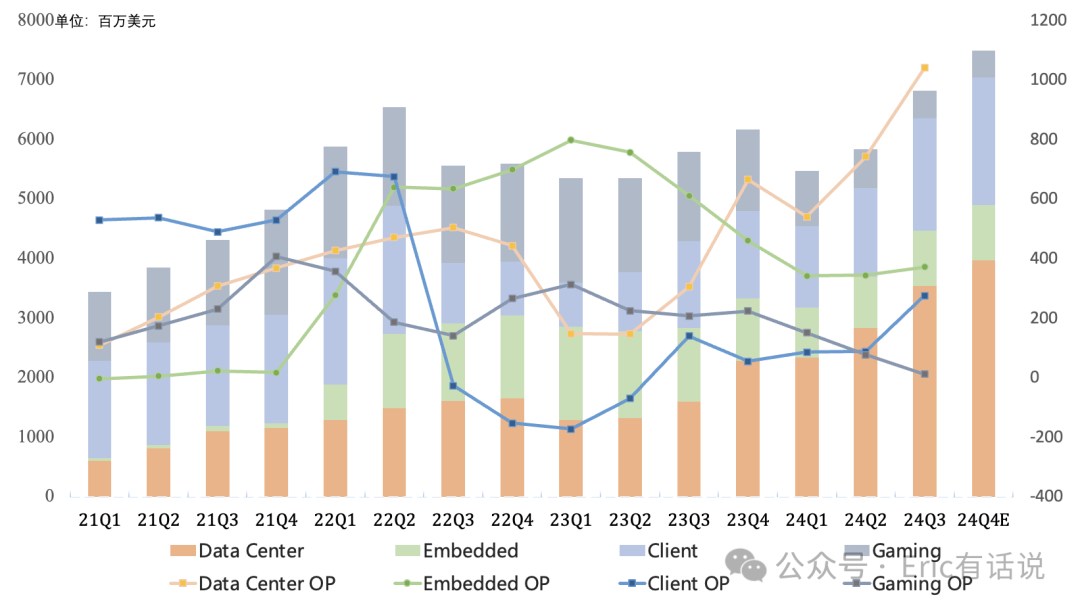

Q3 by Segment:

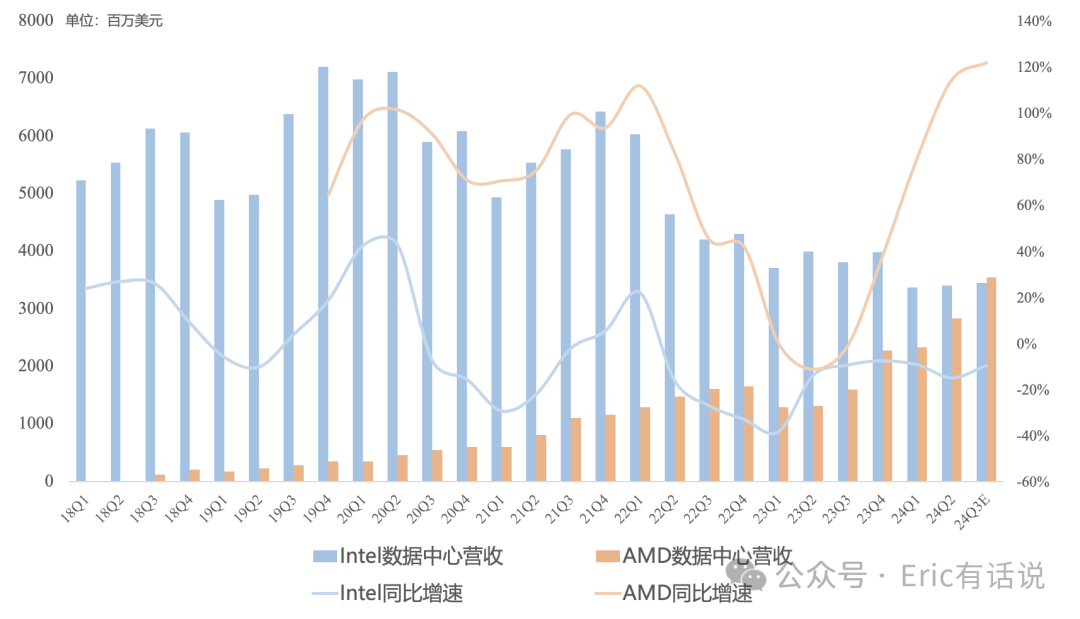

Data center revenue was $3.549B, up 122% year over year, accounting for 52% of revenue. Operating income was $1.041B, up 240% year over year, remaining AMD's most profitable segment.

On CPU, Zen 4 EPYC Genoa/Bergamo demand was strong this quarter, and server CPU share continued to rise. Meta has cumulatively deployed 1.5M EPYC CPUs. Public cloud instances powered by EPYC reached 950+, up 20% year over year. Enterprise revenue grew double digits year over year for the fifth consecutive quarter.

On GPU, data center GPU revenue this quarter approached CPU ($1.5-1.7B), exceeding company expectations. Early in the year the mix was primarily inference; training is now growing quickly. Q4 shipments are still expected to be led by the MI300 series. MI325X (vs. H200) enters volume production in Q4, with volume shipments in 2025 Q1. MI350 series (vs. Blackwell) launches in H2 2025. CDNA Next-based MI400 series (vs. Blackwell Ultra/Rubin) launches in 2026. Due to capacity constraints, the timeline from sampling to volume ramp for GPUs is lengthy. Currently, both the MI300 and MI325 series carry gross margins below the corporate average.

Q4 data center GPU revenue is guided to grow sequentially. Full-year revenue raised from $4.5B to above $5B. The company projects the 2028 AI chip TAM at $500B, exceeding the entire semiconductor industry's 2023 market size.

Embedded revenue was $927M, down 25% year over year, 14% of revenue. Operating income was $372M, down 39% year over year. Embedded customer demand continues a slow recovery into 2025. Test and simulation demand is strong; communications and industrial remain weak. Full-year design wins grew 20%+ year over year; the company will outperform the industry average.

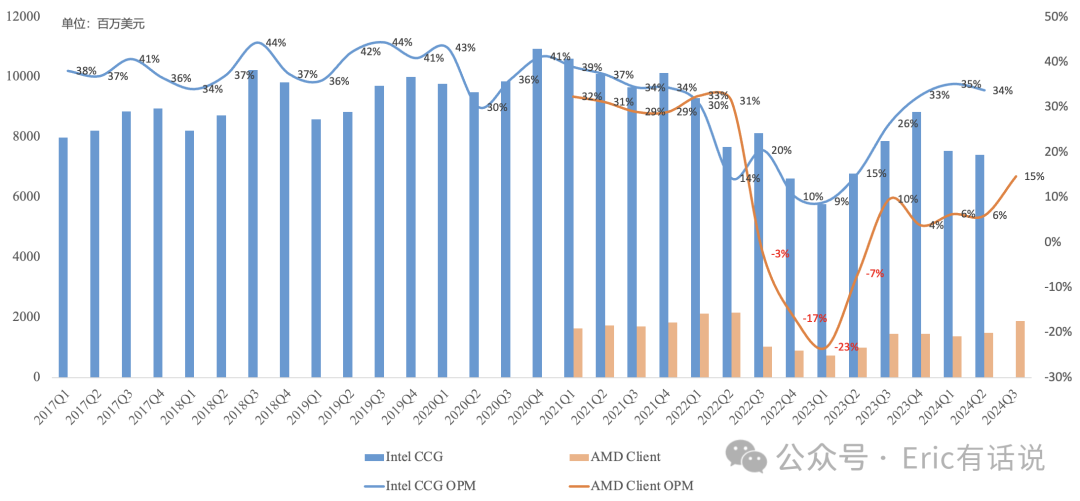

Client revenue was $1.881B, up 30% year over year, 28% of revenue. Operating income was $276M, operating margin 15%, up 9 percentage points sequentially, though still below Intel.

Zen 5 Ryzen desktop revenue grew double digits year over year, driven by Ryzen 9000 series demand, reaching a record market share. Notebook Ryzen AI 300 series is ramping quickly; the company expects over 100 commercial PC platforms shipping Ryzen AI Pro in 2025. However, the notebook business is increasingly consumer-facing, which will keep PC gross margin below the corporate average. 2025 PC shipments are guided to grow mid-single digits year over year, but ASP depends on product mix.

Gaming revenue was $462M, down 69% year over year, the eighth consecutive quarterly decline, 7% of revenue. Operating income was $12M, down 94% year over year. Semi-custom revenue fell sharply year over year as Sony and Microsoft consoles continue inventory drawdown. Gaming GPU revenue declined year over year. First RDNA 4 GPU expected in early 2025.

Guides Q4 revenue at $7.5B, up 22% year over year and 10% sequentially. Sequential growth is mainly driven by data center and Client; Gaming and Embedded are guided to grow modestly sequentially.

Revisiting the Previous Quarter's View:

Full-year revenue is tracking around $25.6B, but full-year net income guidance is only $5.4B, below the expected $6B. A key highlight this quarter was the PC business margin improving as expected; we look for continued repair.

On the market's top focus, AI GPU, full-year revenue guidance was raised to above $5B. Given EPYC's momentum, 2024 data center revenue could reach ~$12.7B. At a 25% operating margin that implies ~$3.2B in operating income — already very impressive for AMD's own growth trajectory. Q3 will almost certainly mark the first time data center quarterly revenue historically surpasses Intel.

Overall, this earnings report was mediocre. Aside from Lisa raising guidance by $500M each quarter still not satisfying the market, the lower gross margins on the MI300/MI325 series have raised concerns about long-term margin levels.