In the previous quarter's earnings postscript I mentioned:

Intel Q1 Earnings:

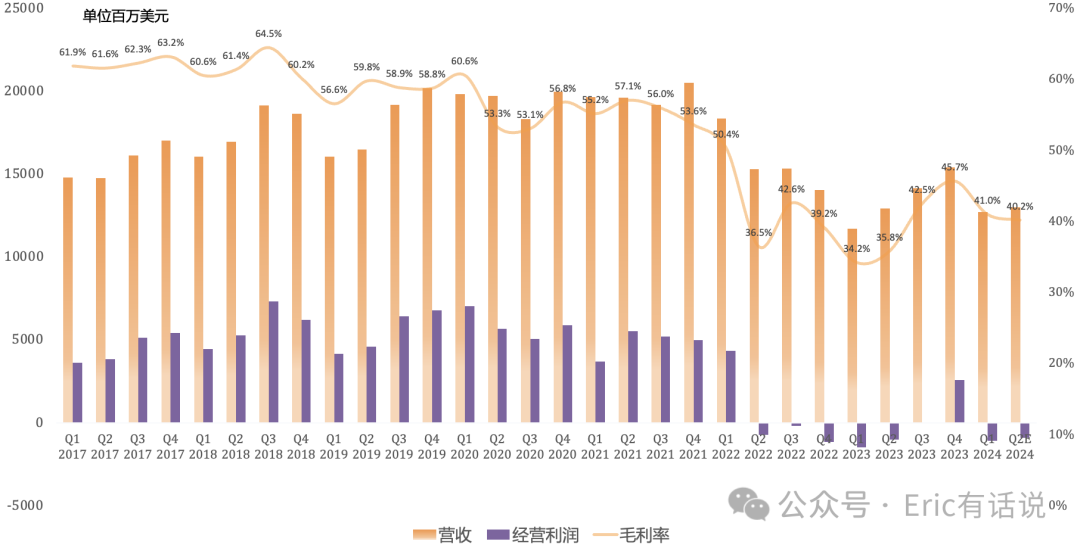

Revenue $12.724B, up 9% year over year, second consecutive quarter of year-over-year growth, down 17% sequentially; guided next quarter revenue $13B, flat year over year.

GAAP gross margin 41%, up 6.8 percentage points year over year, down 4.6 percentage points sequentially; guided next quarter GAAP gross margin 40.2%, continuing to decline sequentially.

GAAP operating loss of $1.069B; guided next quarter to continue losing money.

GAAP net loss $437M, swung to loss sequentially, ending three consecutive profitable quarters; guided next quarter GAAP loss of $212M.

Non-GAAP net income was $759M, swinging from a loss year over year, down 67% sequentially. Next-quarter non-GAAP net income is guided to $424M, down 22% year over year and 44% sequentially.

Free cash flow was -$6.178B; full-year free cash flow last year was -$3.1B.

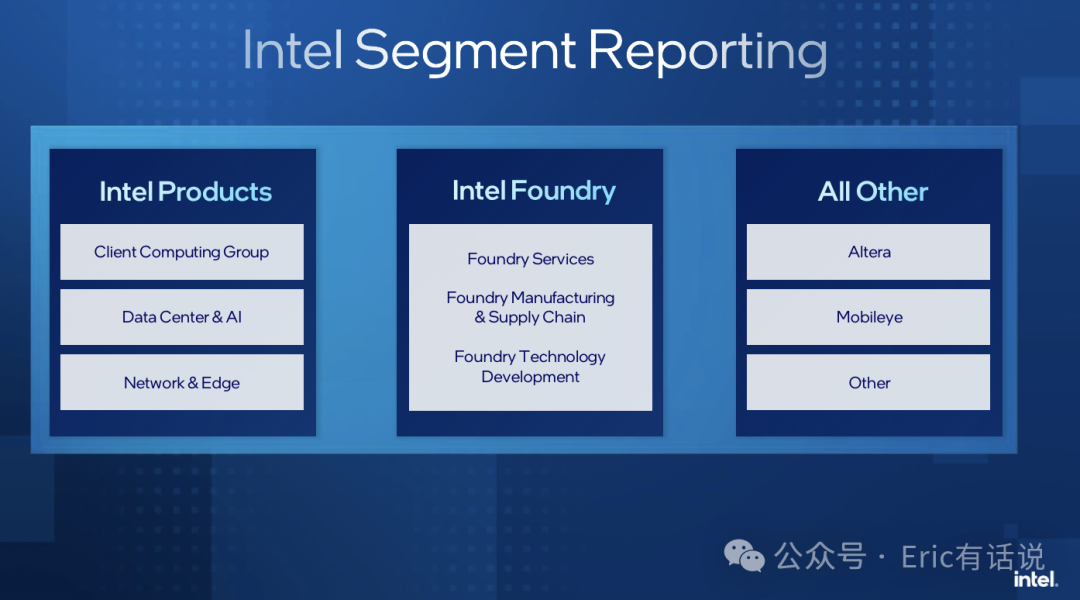

Q1 Business Breakdown (Intel changed reporting segments again this quarter):

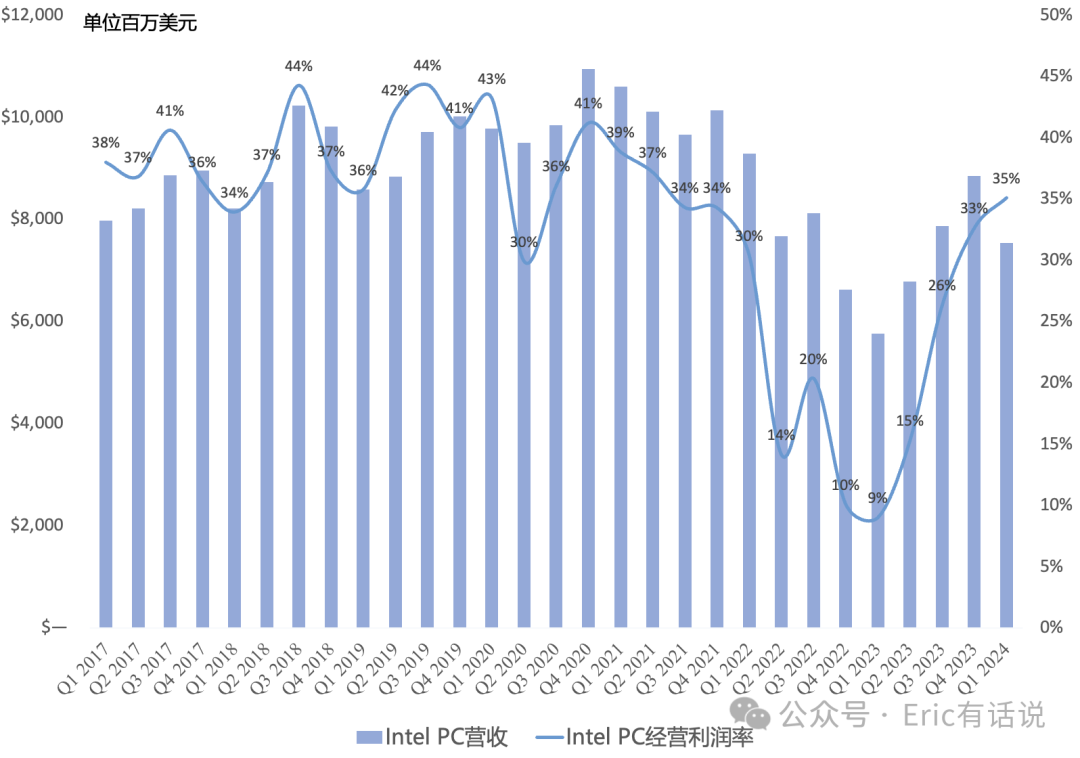

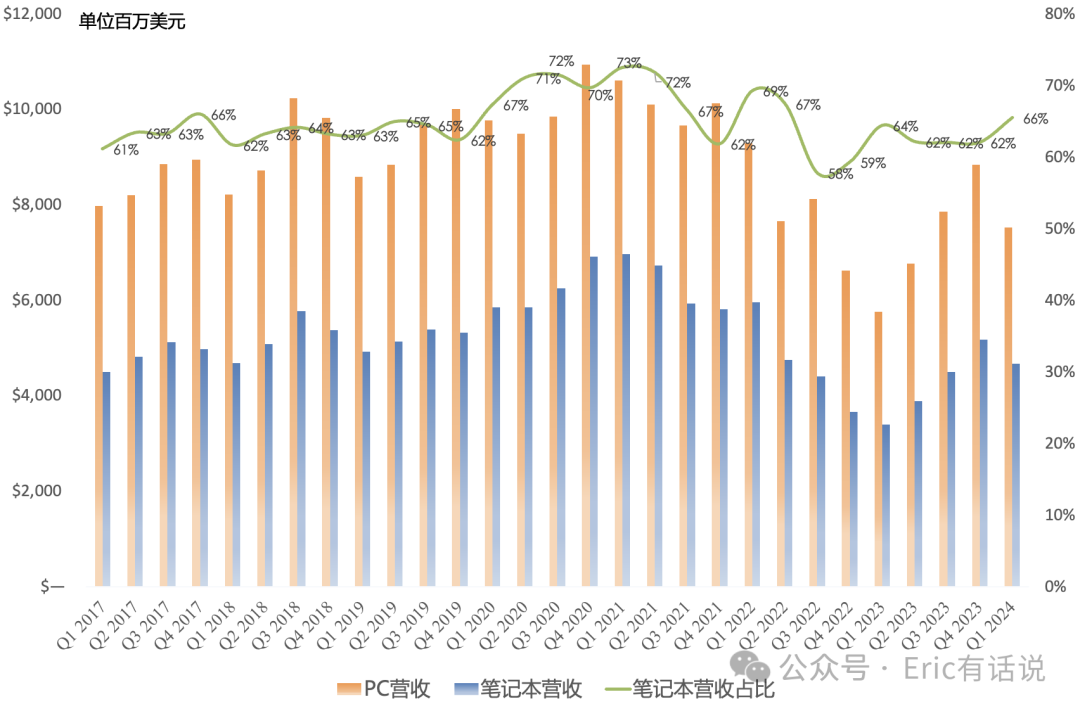

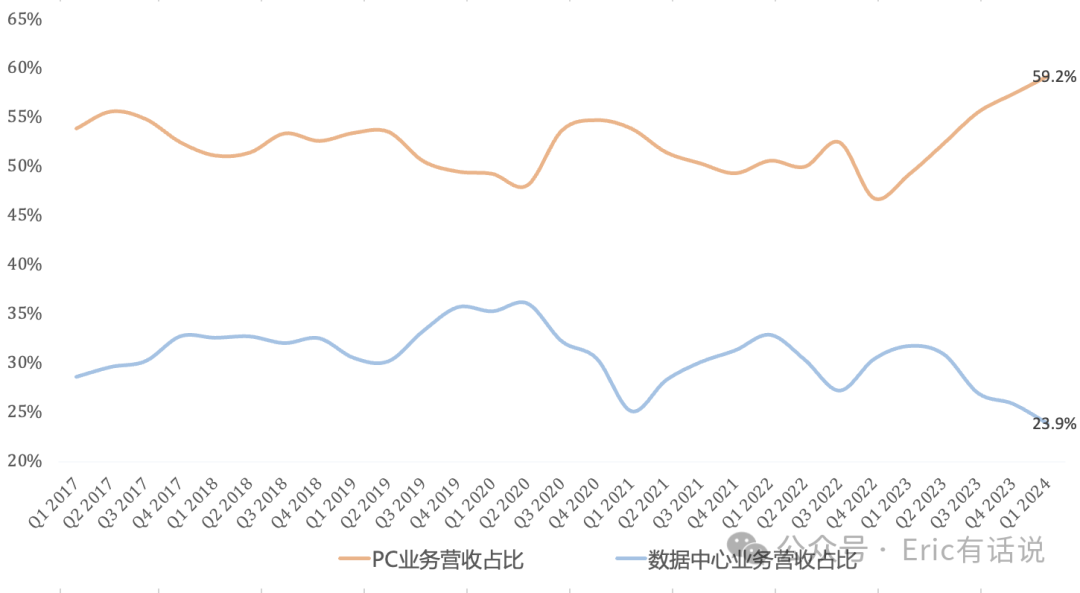

CCG revenue was $7.533B, up 31% year over year for the second consecutive quarter, down 15% sequentially, with revenue share of 59%, a high since Q4 2014; operating income was $2.645B, up 409% year over year, down 8% sequentially, accounting for 167% of Intel's operating income.

Expect commercial PC market refresh in H2; Intel 4 process Meteor Lake Core Ultra Q2 shipments to double sequentially, currently constrained by packaging capacity; with Lunar Lake/Arrow Lake launching in H2, expect 2024 AI PC shipments to exceed 40M units.

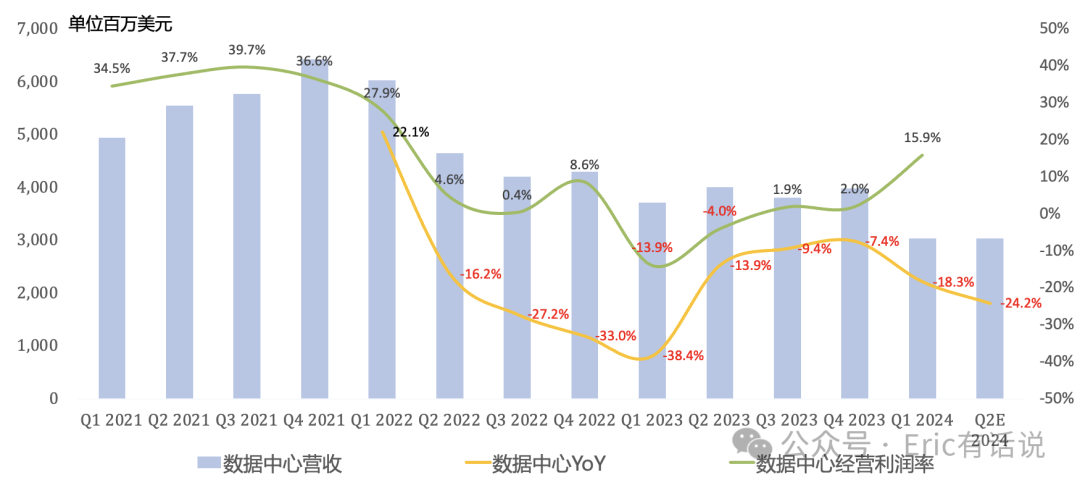

DCAI revenue was $3.036B, down 18% year over year, eighth consecutive quarter of year-over-year decline, down 24% sequentially; operating income $482M, third consecutive profitable quarter, operating margin back to 16%.

Server CPU ASP kept growing, but share gains must wait until late this year or next year with Clearwater Forest (GAA 18A E-cores server); expect traditional server market recovery in H2, full-year server CPU revenue up mid-20% year over year.

AI: H2 Gaudi 3 shipments to drive full-year AI revenue >$500M, 2025 to continue growing; Falcon Shores late next year; recall last quarter Intel claimed 2024 Gaudi portfolio pipeline >$2B, now only $500M+ landed? Understandable.

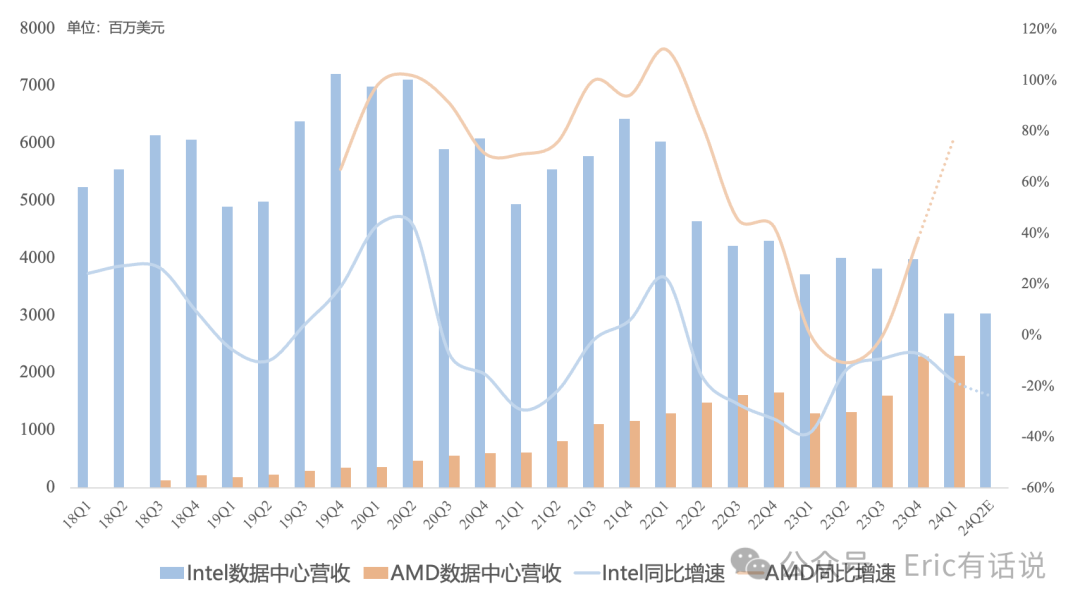

Q2 data center revenue is expected to be flat sequentially, and the gap between AMD and Intel data center revenue will narrow further. AMD will likely overtake Intel in 2024, possibly even earlier than I predicted last quarter.

NEX revenue was $1.364B, down 8% year over year, marking the sixth consecutive quarter of year-over-year decline, and down 7% sequentially; operating profit was $184M. The 5G market is weak, while network/edge revenue grew 10% year over year. NEX overall channel inventory is near normal levels, and the business is expected to grow quarter by quarter going forward.

Intel Foundry revenue was $4.369B, down 10% year over year due to declines in backend services, sample revenue, and the impact of the IMS divestiture; operating loss was $2.474B, a new record high. Wafer shipments grew slightly, while ASP declined slightly, dragged down by mature-node pricing. This year wafer shipments will still be led by Intel 7, with Intel 4/Intel 3 ramping next year. Full-year Intel Foundry loss pressure is expected to remain high, with depreciation increasing by $2B.

Previously, IFS (external) revenue was $16M, down 86% year over year and 95% sequentially, which explains why internal and external results were combined for disclosure.

Microsoft is the fifth Intel 18A customer; the sixth is an aerospace and defense company. Intel 18A now has six customers in total, encompassing 50 test chips. Intel 14A will be the first process node to use High-NA EUV. Intel Foundry lifetime deal value exceeds $15B, up $5B sequentially. Future Intel Foundry wafer ASP growth is expected to be three times the cost growth, which will drive rapid gross margin improvement.

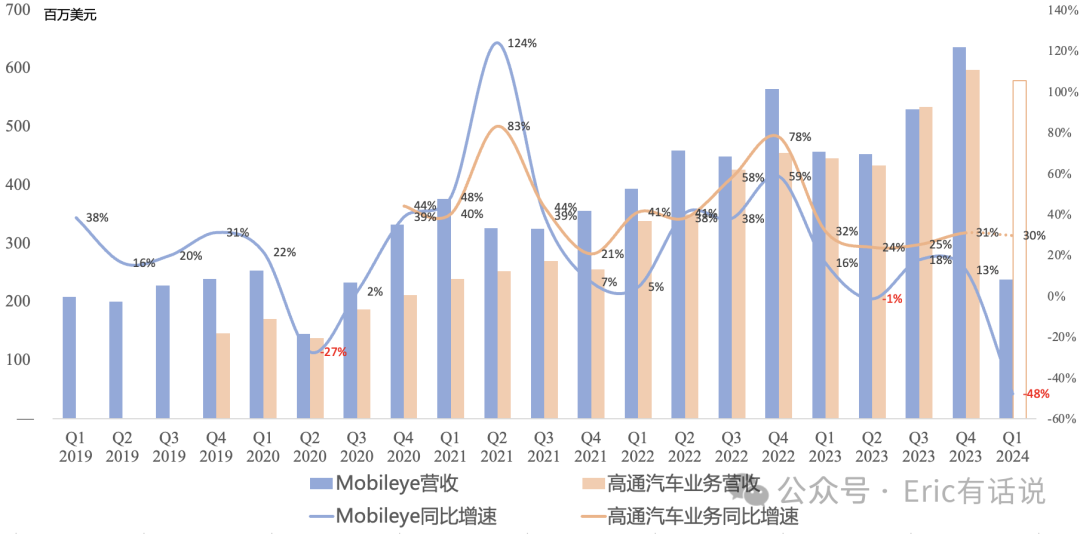

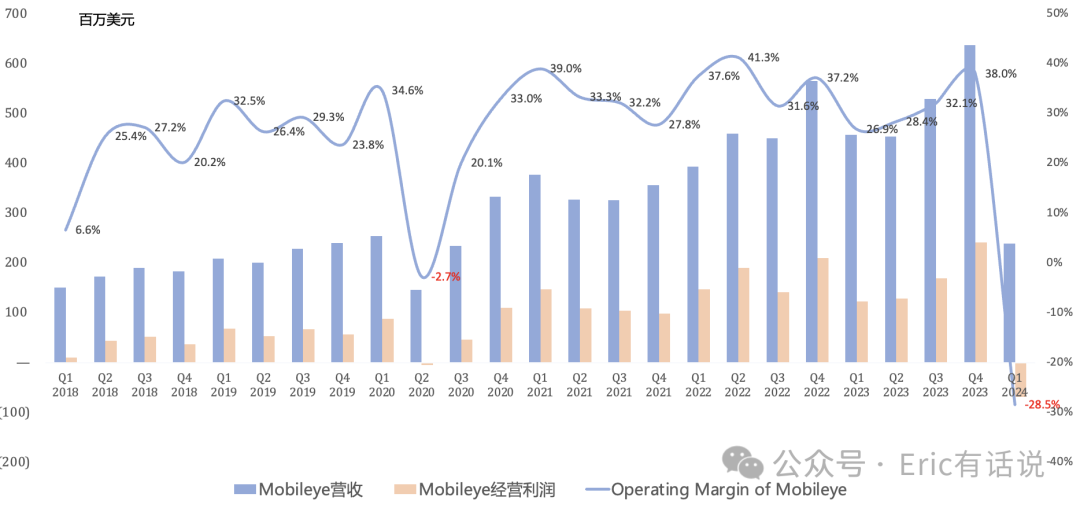

Mobileye revenue was $239M, down 48% year over year and 63% sequentially; operating loss was $68M, the first loss since 2020 Q2. Revenue scale will likely be overtaken by Qualcomm again. Mobileye FY2024 revenue is projected at $1.895B, down 9% year over year, with an operating loss of $423M.

This quarter the FPGA business Altera was carved out of DCAI. Altera revenue was $342M, down 58% year over year and 29% sequentially. Year-end Altera revenue run rate is expected to reach $2B, implying full-year revenue down 31% year over year, with Q4 revenue up 4% year over year.

Call Highlights:

Q2 revenue midpoint is guided at $13B, flat year over year and up 2% sequentially. PC and data center revenue are expected to be flat sequentially, while Mobileye/Altera/IFS revenue grows sequentially. PC is impacted by insufficient Core Ultra packaging capacity. All businesses are expected to resume growth in the second half, with full-year gross margin up 2 percentage points versus last year.

Intel 18A manufacture ready in 24H2; Clearwater Forest (GAA 18A E-cores server) / Panther Lake (18A client) ramp in 25H1 on track. First Intel 3 process Sierra Forest (E-cores clouds) already launched; next-gen Granite Rapids (P-cores enterprise) launching 24Q3.

Intel Foundry's 2030 target is to become the world's second-largest foundry. Intel claims to be the only non-Asian company capable of manufacturing advanced processes.

The global foundry market is expected to grow from $110B today to $240B by 2030, with 90% of the growth coming from EUV and advanced packaging.

As its own technology advances, products currently outsourced to TSMC will return to internal production; the next two years will be the peak of outsourcing to TSMC.

CEO Pat stated that the databases required for LLM with RAG currently all run on x86 CPUs.

FY2024 capex as a percentage of revenue is expected in the mid-30s; FY2024 free cash flow is expected to break even.

The U.S. announced in March up to $8.5B in grants and $11B in loans to Intel, plus tax incentives and other forms totaling $45B.

Overall, this earnings report continues to rely on PC to maintain appearances. PC contributed 59% of Intel revenue and 167% of operating profit. However, subsequent PC demand is not that optimistic; Microsoft's Windows business growth guidance is weak, and Qualcomm is adding disruption.

Pat's vision-painting is clearly not on par with Musk's. Intel's years-long diversification strategy has been thoroughly crushed; PC share has returned to a decade ago, and performance is even worse than a decade ago. Management pins hopes for high growth on next year. Ironically, the to-be-spun Altera and the already-spun Mobileye both blew up simultaneously, and Intel Foundry's disclosure format makes one wonder if it's also preparing for a future spin. Don't let Intel end up as a pure PC company.

Regarding next week's AMD earnings, near-term data center CPU share appears intact for AMD, but weakness in the console market is concerning. The market is most focused on whether the full-year $3.5B AI revenue guide can be raised again, and whether the 'silent' MI300 has truly seen order cuts.