Since Intel officially announced Lip-Bu Tan as new CEO, all four US chip giants — NVIDIA, Broadcom, AMD, and Intel — now have Chinese-American CEOs; it appears only Chinese people can run semiconductors well.

Intel Q1 Earnings:

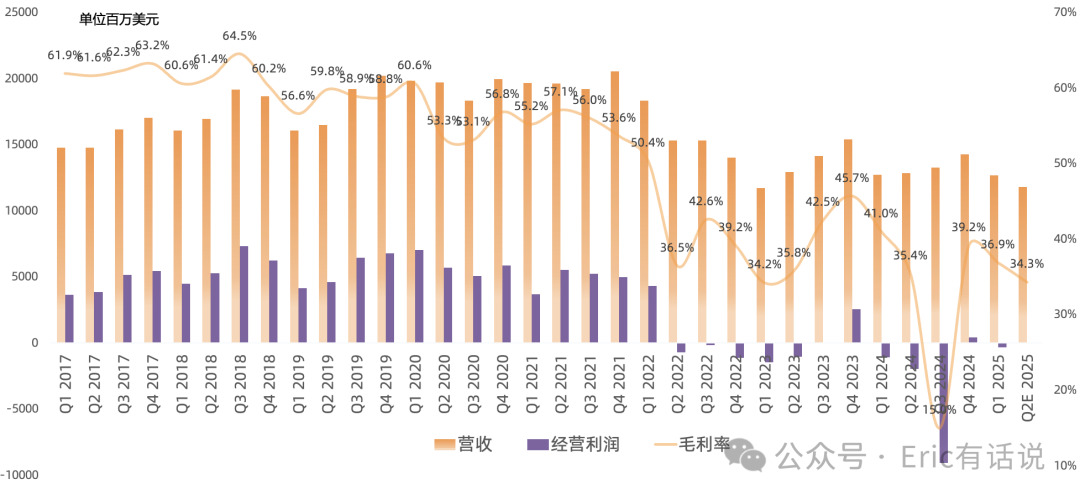

Revenue $12.667B, down 0.4% year over year, the 4th consecutive quarter of year-over-year decline, down 11% sequentially; Guiding next quarter revenue $11.8B, down 7% year over year, the 5th consecutive quarter of year-over-year decline;

GAAP gross margin 36.9%, down 4.1 percentage points year over year, down 2.3 percentage points sequentially; Guiding next quarter GAAP gross margin 34.3%, down 1.1 percentage points year over year;

GAAP operating loss $301M, back in the red; Guiding next quarter operating loss to widen;

GAAP net loss $887M, 5th consecutive quarter of losses; Guiding next quarter net loss of $1.39B, loss widening;

Non-GAAP net income $580M, down 24% year over year, 2nd consecutive quarter of profitability; Guiding next quarter Non-GAAP breakeven;

Adjusted free cash flow -$3.68B;

As of quarter-end, company net assets $99.76B;

Q1 Business Breakdown (yes, reporting segments changed again):

New structure: NEX edge business moved to CCG, NEX network business moved to DCAI, IMS business moved from Intel Foundry to All Other, automotive business moved from All Other to CCG; the result is that both CCG and DCAI numbers look better.

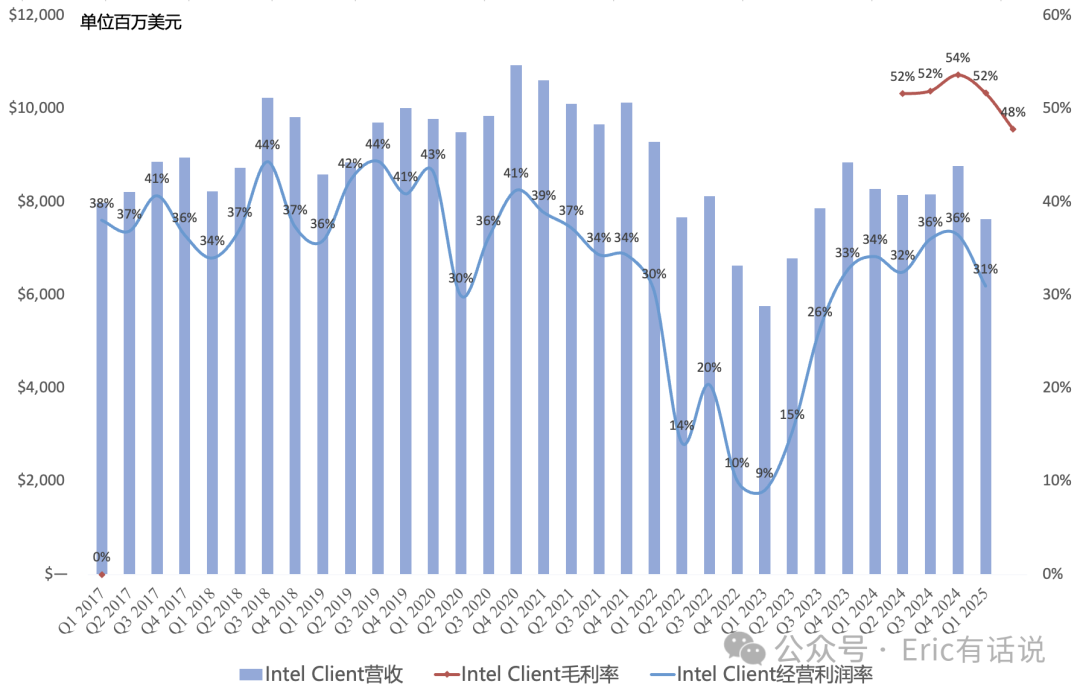

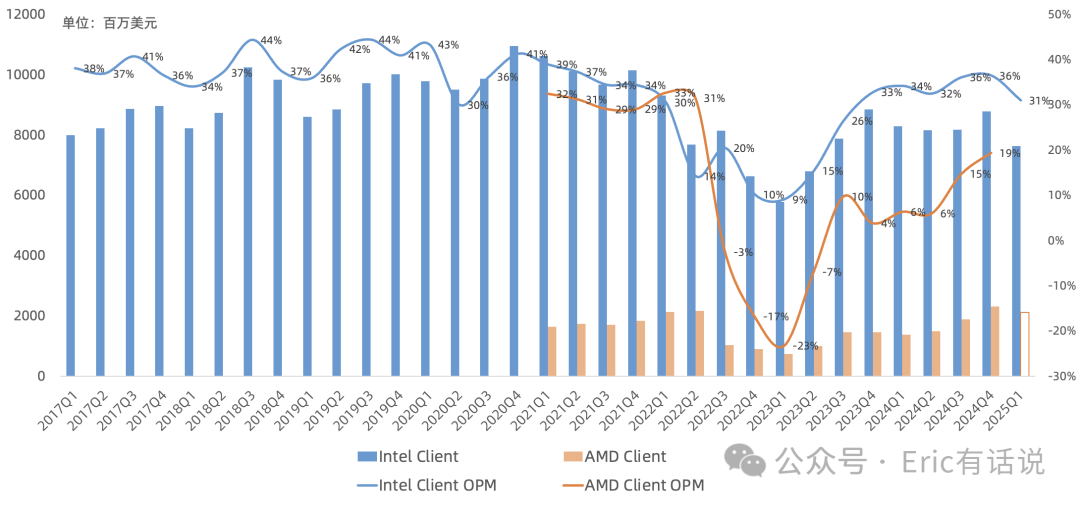

CCG revenue was $7.629B, down 8% year over year, the second consecutive quarter of year-over-year decline, and down 13% sequentially; revenue share was 60%. Gross margin was 48%, down 3.8 percentage points year over year. Operating income was $2.361B, down 16% year over year and 26% sequentially; operating margin was 31% (vs. AMD 24Q4 19%), remaining Intel's most profitable business.

PC revenue $6.5B, down 8% year over year due to intensifying competition; shipments down year over year; ASP roughly flat year over year; Raptor Lake shipments outperformed Lunar Lake, lifting gross margin; N-1 and N-2 generation CPU demand strong (recently RTX 50-series value-tier laptops frequently feature 13th/14th gen CPUs, and with China subsidies they are more attractive to consumers); Notebook Panther Lake (RibbonFET+PowerVia, first 18A) expected to enter volume production late this year, mass shipments early next year; Panther Lake ~70% internal production; next year desktop Nova Lake >70% internal; AI PC growth below expectations;

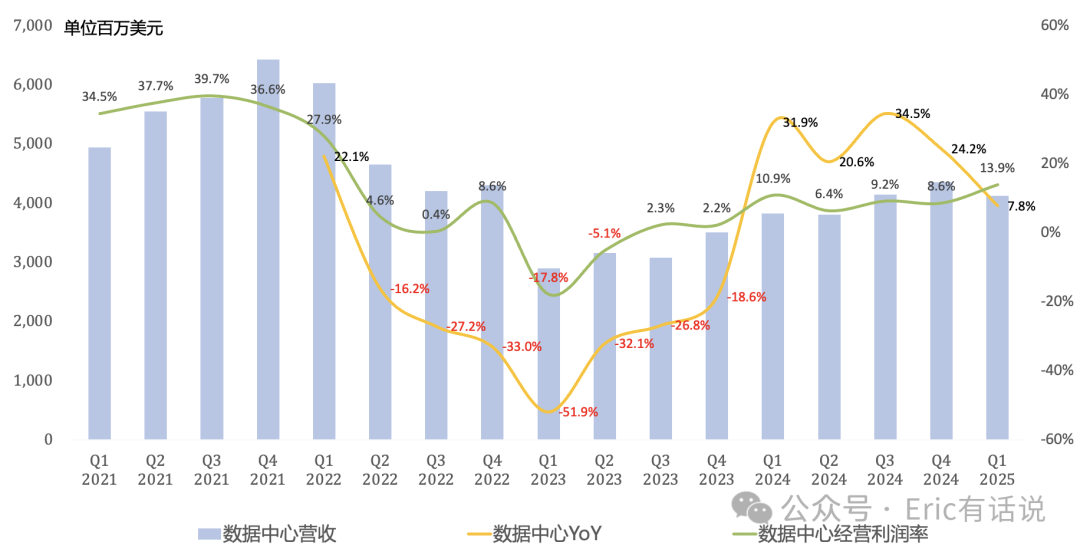

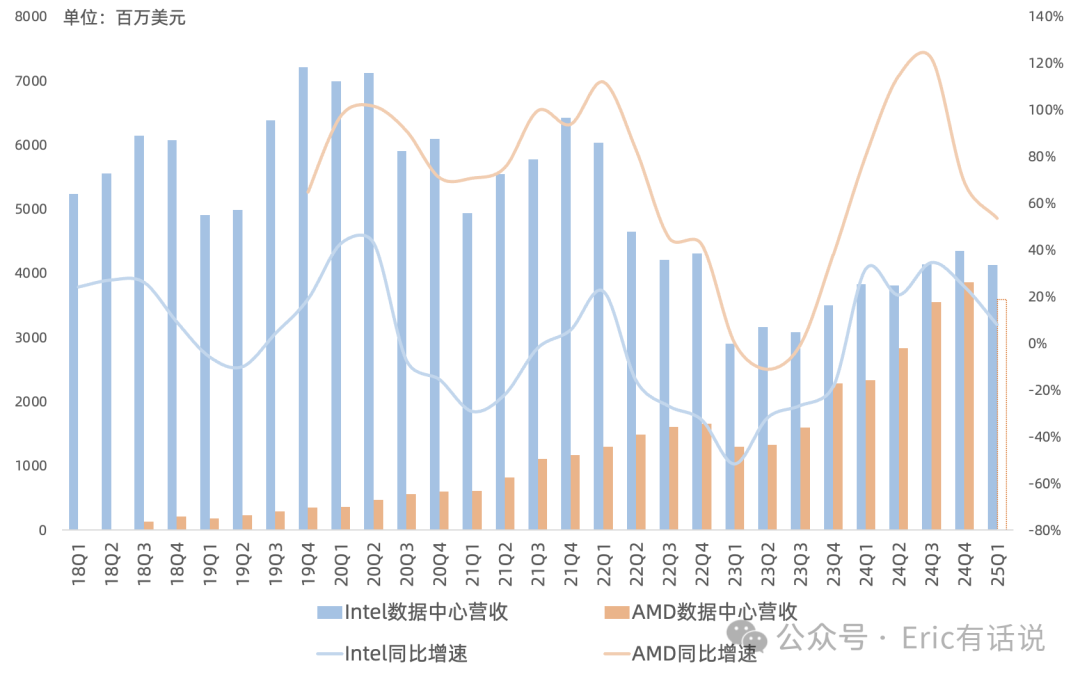

DCAI revenue $4.126B (surpassed AMD data center revenue after segment change), up 8% year over year, down 5% sequentially; Gross margin 43%, down 11.6 percentage points year over year; Operating income $575M, up 38% year over year, up 54% sequentially; Operating margin 14%;

Server CPU revenue up year over year driven by strong hyperscaler demand; shipments up 16% year over year; ASP down 10% year over year; Clearwater Forest (GAA 18A E-core server) expected to enter volume production H1 2026;

Intel Foundry revenue $4.667B, up 7% year over year, up sequentially mainly due to Intel 7 process pull-ins and advanced packaging growth; Gross margin -27%; Operating loss $2.32B; Intel Foundry external revenue $31M, up 138% year over year;

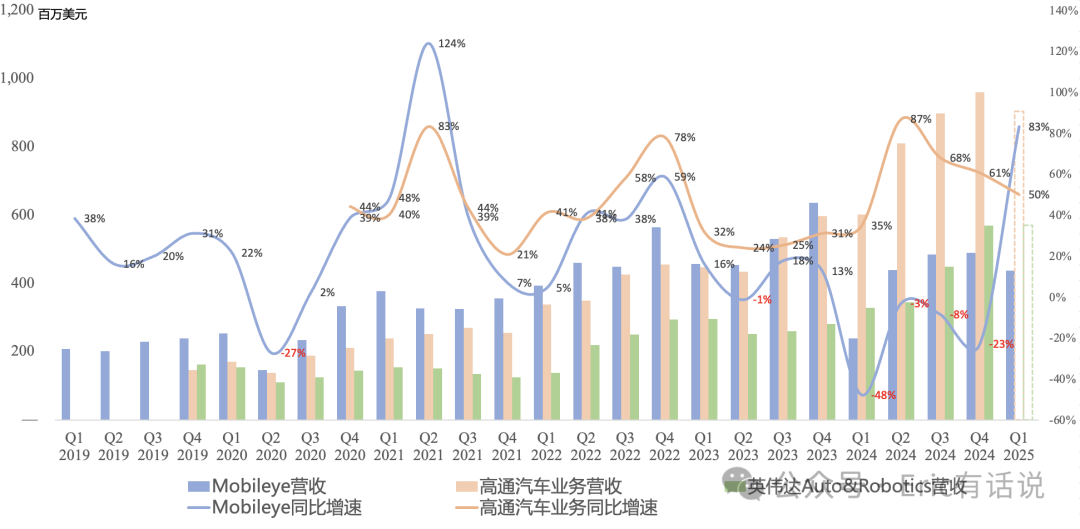

Mobileye revenue $438M, up 83% year over year, ending 4 consecutive quarters of year-over-year decline, down 11% sequentially; Revenue gap vs. Qualcomm widened further, even overtaken by NVIDIA; Operating income $59M, swung to profit year over year; Average system price $49, a multi-year low; FY25 revenue guidance midpoint $1.75B, up 6% year over year; operating income guidance midpoint $218M, up 18% year over year;

Altera revenue $368M, up 8% year over year, down 14% sequentially; Silver Lake previously announced acquisition of 51% of Altera at an $8.75B enterprise valuation (Intel acquired Altera for $16.7B in 2015; AMD acquired Xilinx for $35B in 2020); Intel retains remaining 49%; transaction expected to close H2 this year;

Call Highlights:

Q1 received $1.1B CHIPS Act grant and $1.9B final payment from SK hynix for NAND business sale; subsequent subsidies uncertain;

Due to macro uncertainty including tariffs, guiding Q2 revenue $11.2-12.4B, down year over year, down 2%-12% sequentially; DCAI sequential decline larger than CCG; Intel Foundry sequential decline due to continued Intel 7 capacity constraints;

Guiding Q2 Non-GAAP gross margin 36.5%, down 2.2 percentage points year over year; Guiding 2025 opex $17B (reduced), 2026 $16B;

Guiding 2025 gross capex $18B (reduced), net capex $8-11B (unchanged); cost discipline is a key priority;

Guiding Q2 NCI near zero, full year $500M, 2026 $1.3-1.5B, growing thereafter;

Previously noted at the end of the last earnings report:

This was Lip-Bu Tan's first earnings call as Intel CEO; he didn't paint many grand visions, focusing instead on cost-cutting measures; the previous Foundry target of operating profitability by end of 2027 was not reiterated. The make-or-break 18A volume production timeline remains at year-end, with no acceleration. Management repeatedly emphasized the impact of tariffs and macroeconomics on results; in the near term, Intel has little good news and needs time.