Semiconductor giant Intel released Q1 earnings after hours:

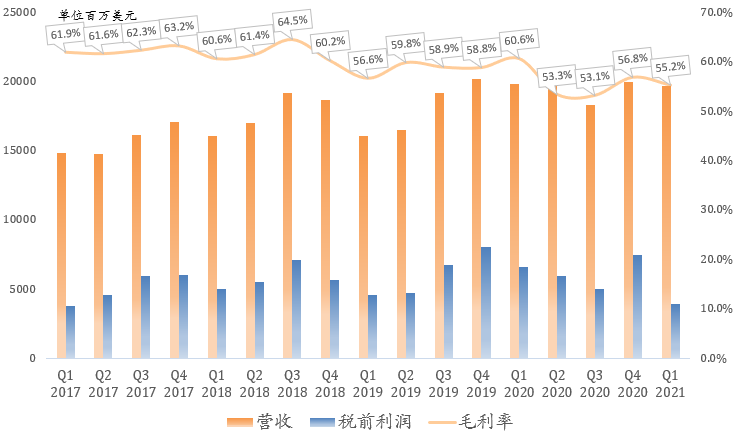

Revenue $19.67B, down 1% year over year; gross margin 55.2%, down 5.4 ppt year over year; net income $3.361B, down 41% year over year.

Excluding the NAND sale to SK hynix, revenue $18.57B, flat year over year; gross margin 58.4%, down 6 ppt year over year; net income $5.7B, down 6% year over year.

Intel's overall earnings were much as previewed yesterday; Intel has become the semiconductor "underperformer." Whether or not NAND is excluded, Intel may be the only giant to miss out on the semiconductor supercycle.

Data center down 20% year over year, operating margin hits new low

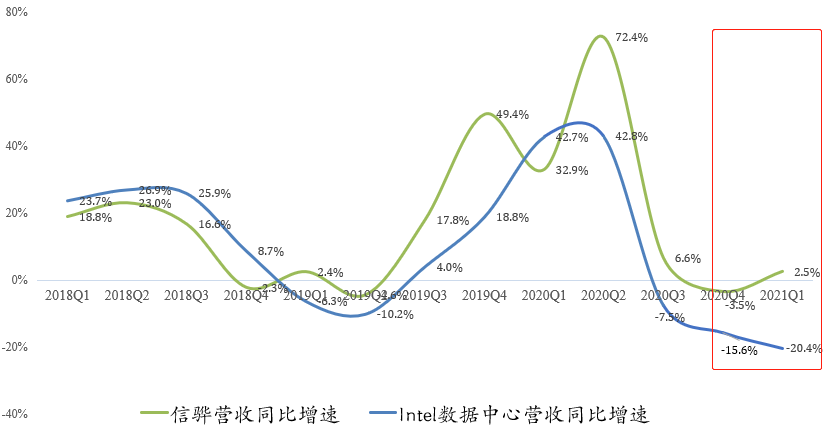

We previously used Cinno Research revenue data to judge that Intel's data center should also be slowly recovering, with Q1 decline within 10%. The reality: even with Optane folded in, Intel Q1 data center still fell 20.4% year over year! Two consecutive quarters of disappointment.

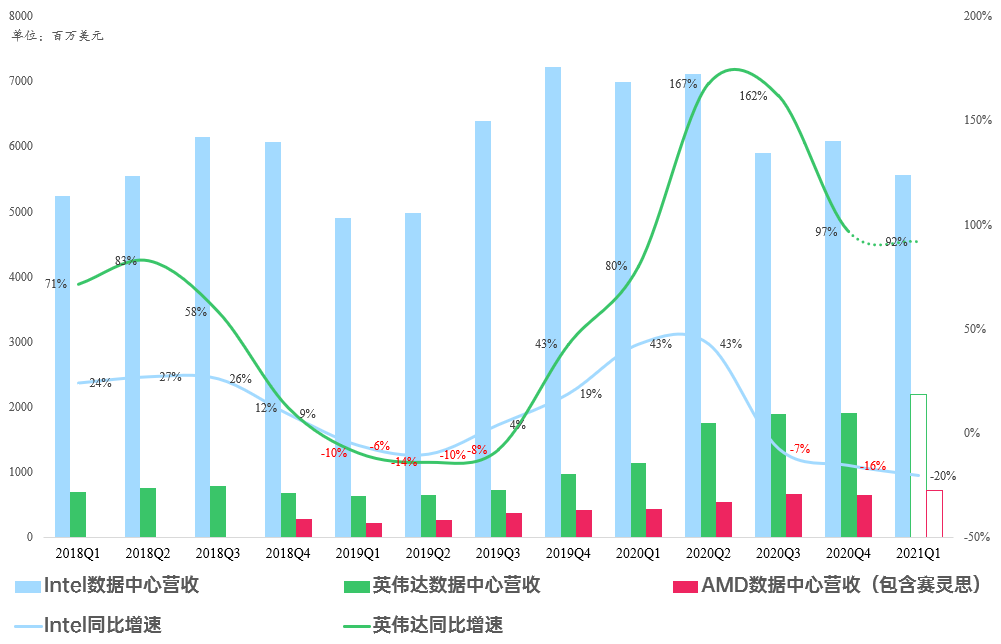

We previously judged that because NVIDIA DGX data centers deeply bind AMD EPYC with NVIDIA A100, EPYC would further erode Intel Xeon share. The earnings now confirm that.

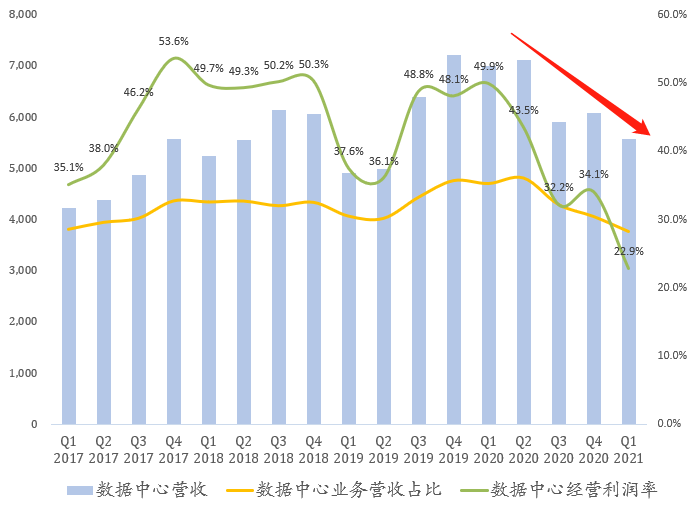

Intel Q1 data center revenue was $5.564B, down 20.4% year over year, even including Optane. Intel's data center revenue share hit a new low since 2017 at just 28.3%. Even more alarming, Q1 data center operating margin reached 22.9%, a new low. The company blamed the 10nm Xeon ramp and higher R&D spending.

However, Intel's 5G business did indeed shine as we expected. Data center adjacent businesses represented by 5G SoC grew 33% year over year in Q1, but could not reverse the data center slump.

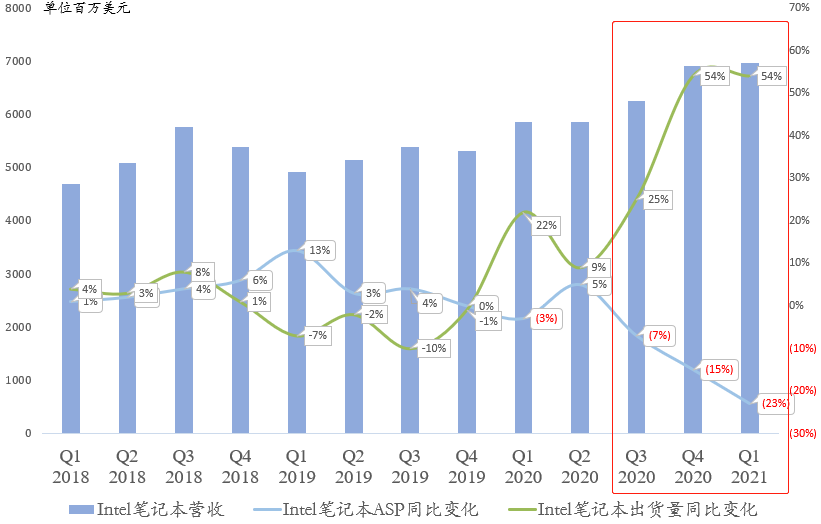

Notebook revenue hits record, but ASP falls year over year for third straight quarter

Intel Q1 PC revenue was $10.605B, up 8.5% year over year. Notebook revenue was around $6.97B, accounting for 72.5%, hitting a record high.

But this performance is par for the course given the PC explosion. IDC shows total PC shipments up 55.2% year over year. Beats from Intel, AMD, and NVIDIA PC were all but guaranteed. Notably, behind Intel's strong notebook results lies a severe divergence between shipments and ASP, with ASP falling year over year for three consecutive quarters at an accelerating pace! This means Intel's shipments are dominated by entry-level Chromebooks, suggesting its mainstream market may be seriously threatened by AMD.

Intel's long-term thesis broken, urgently needs new technology to rescue it

Intel's other businesses like Mobileye posted record revenue and operating profit, but the ADAS approach has been abandoned by the mainstream market, which has shifted to NVIDIA. Mobileye's future MaaS prospects are questionable.

In short, Intel may benefit somewhat from the global semiconductor supercycle in the near term, but its long-term logic is broken, especially its growth pillar—the data center business.

With AMD aggressively blocking in PC and server markets ahead, and NVIDIA, the pioneer of Arm in data center, chasing furiously from behind, Intel's road ahead will be rocky, and the contrast with AMD and NVIDIA will only grow starker.