I noted at the end of the 23Q4 earnings:

AMD's data center revenue officially overtook Intel's in 2024 Q3. On November 2, Intel, a Dow component for 25 years, was removed from the index.

Intel Q3 Earnings:

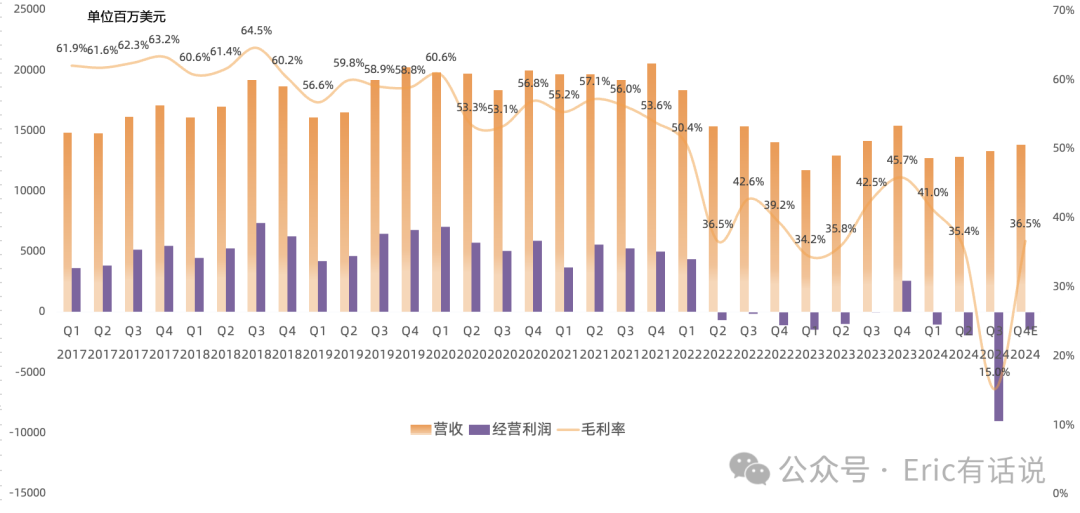

Revenue was $13.284B, down 6% year over year, the second consecutive quarterly year-over-year decline, but up 4% sequentially. Next-quarter revenue is guided at $13.8B, down 10% year over year.

GAAP gross margin was 15%, down 27.5 percentage points year over year and 20.4 percentage points sequentially. Next-quarter GAAP gross margin is guided at 36.5%, down 9.2 percentage points year over year.

GAAP operating loss was $9.057B, the third consecutive quarterly loss. Next quarter is also guided to a loss.

GAAP net loss was $16.989B, the third consecutive quarterly loss. Next quarter is also guided to a loss.

Non-GAAP net loss was $1.976B. Next-quarter Non-GAAP net income is guided at $515M.

Adjusted free cash flow was -$2.702B. Full-year free cash flow is expected to be negative; 2025 free cash flow is expected to turn positive.

This quarter's impairment and restructuring charges totaled $18.5B, including a $3.1B impairment of Intel 7-related equipment and facilities, a $2.6B Mobileye goodwill impairment, $2.2B in severance, and a $9.9B deferred tax asset impairment. Q4 will still incur substantial restructuring charges.

As of this quarter, the company's net assets stood at $104.864B.

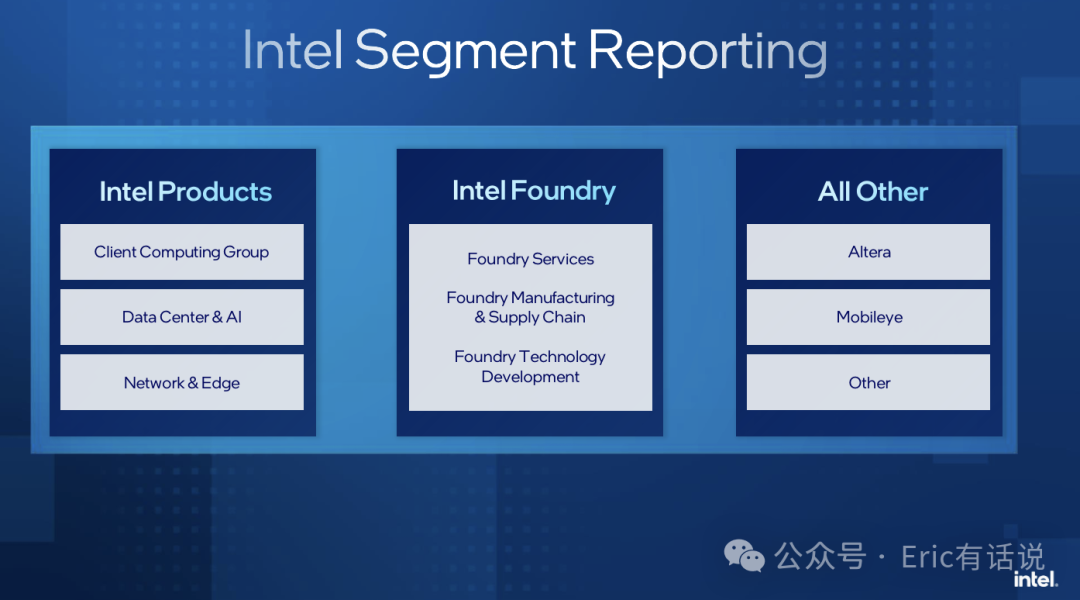

Q3 Segment Details:

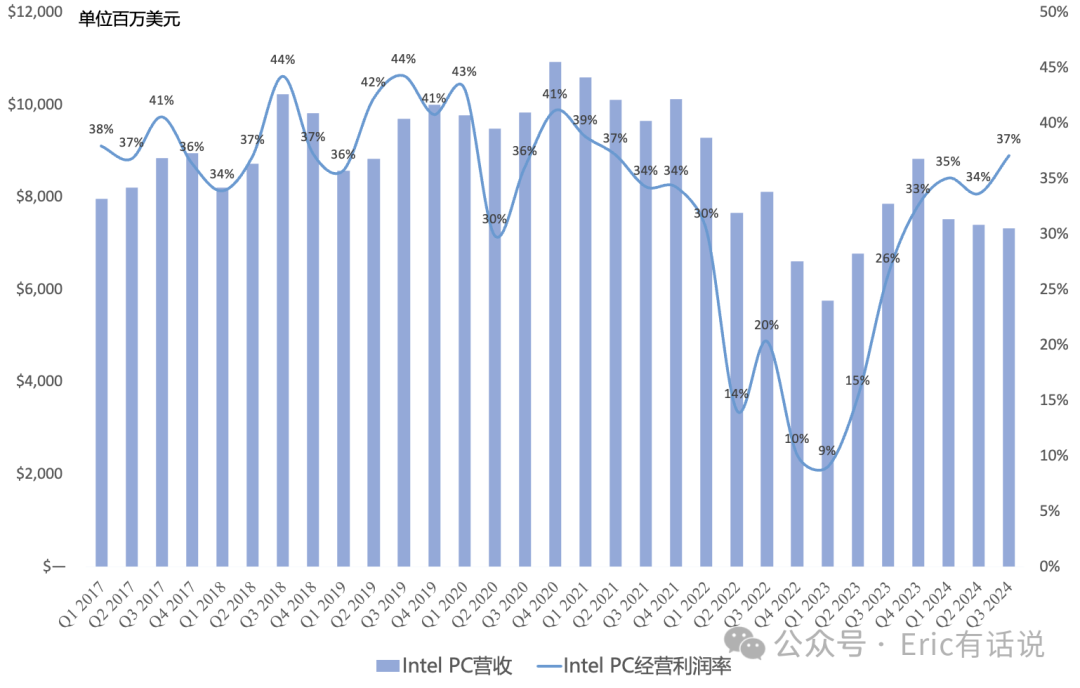

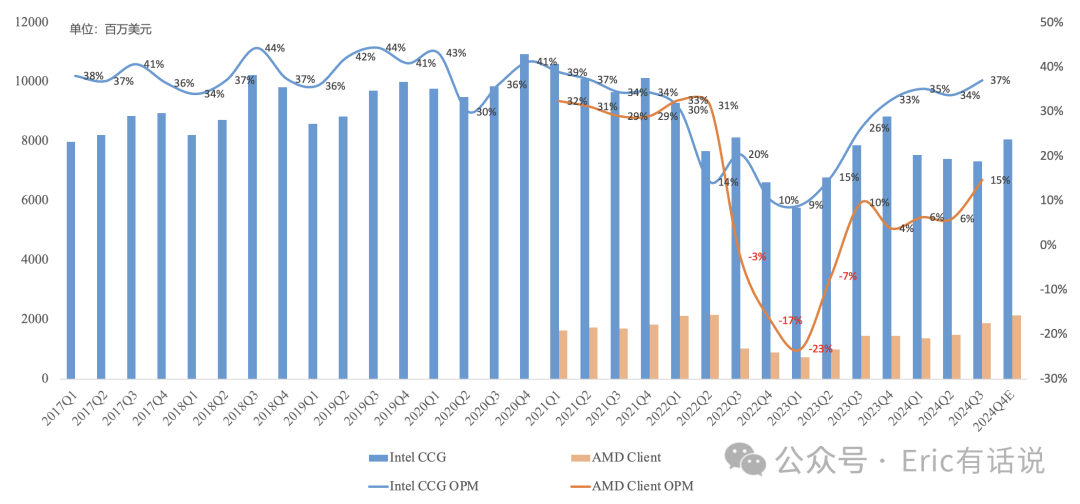

CCG revenue was $7.33B, down 7% year over year, ending three consecutive quarters of year-over-year growth, and down 1% sequentially, the third consecutive quarterly sequential decline. Revenue share was 55%. Operating income was $2.722B, up 31% year over year and 9% sequentially, with an operating margin of 37% (vs. AMD's 15%), returning to 21Q2 levels. It remains Intel's most profitable business.

PC shipments were mainly affected by high inventory. Notebook Panther Lake (Intel 18A) is expected to reach volume production in 25H2, with over 70% of die area internally fabricated. Successor Nova Lake is still expected to partially use TSMC foundry. The company expects cumulative AI PC shipments to exceed 100M by end of 2025. Lunar Lake's ramp next year will pressure company gross margin.

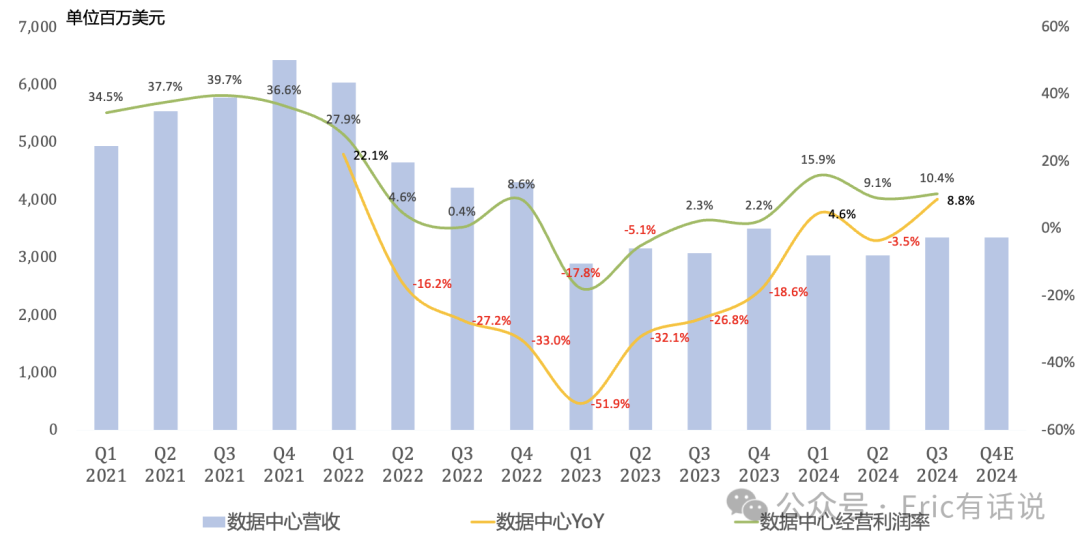

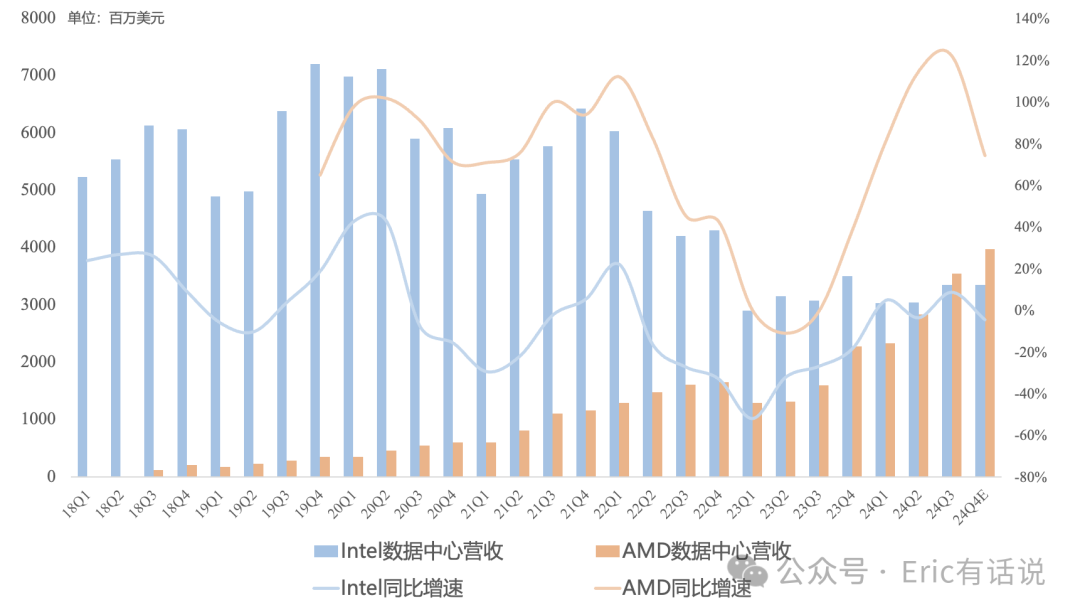

DCAI revenue was $3.349B (since 24Q1, DCAI disclosure excludes Altera; AMD Q3 data center revenue was $3.549B), up 9% year over year and 10% sequentially. Operating income was $347M, up 26% sequentially, with an operating margin of 10%.

This quarter's DCAI revenue growth came mainly from a modest recovery in traditional servers. Over 70% of the installed server base still uses Xeon CPUs.

On AI, Gaudi 3, unmentioned in the Q2 earnings, finally resurfaced and fell far short of company expectations. Recall that in Q4 last year Intel claimed a 2024 Gaudi portfolio pipeline above $2B; in Q1 it said booked revenue was only $500M+; Q2 stopped citing specific numbers; and in Q3 it admitted the full-year Gaudi GPU sales target of $500M would not be met (vs. AMD's full-year AI GPU guidance of $5B+). Q3 saw a $300M inventory write-down on Gaudi GPUs.

AMD's Q3 data center revenue officially surpassed Intel's in scale. Intel's Q4 data center revenue is guided roughly flat sequentially, while AMD will challenge $4B in revenue, further widening the gap.

NEX revenue was $1.511B, up 4% year over year, ending seven consecutive quarters of year-over-year decline, and up 12% sequentially. Operating income was $268M, as the segment's end markets begin to recover.

Intel Foundry revenue was $4.35B, down 7% year over year. Operating loss was $5.84B, a new record. Q4 Foundry operating loss rate is guided in line with Q3. IFS (external) revenue was about $55M, down 82% year over year. In Q3, Intel signed a multi-billion-dollar foundry letter of intent with AWS, including custom Intel 3 Xeon 6 and Intel 18A AI chips. Beyond AWS, Q3 secured two 18A design wins. Q3 was awarded a $3B Secure Enclave program order from the US government.

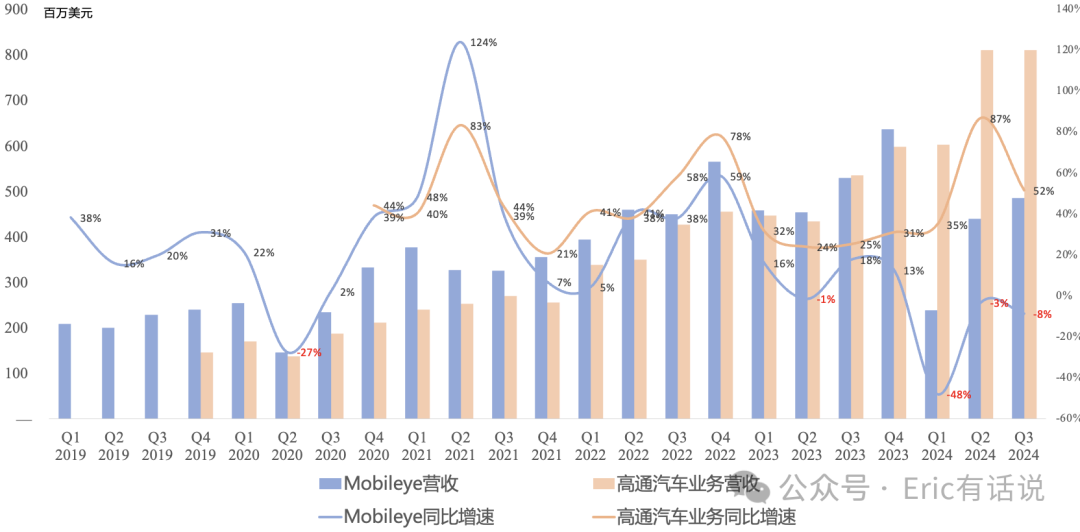

Mobileye revenue was $490M, down 9% year over year, the third consecutive quarterly year-over-year decline, but up 10% sequentially. Operating income was $78M, down 57% year over year, mainly due to a >50% shipment decline in China. Revenue will be pulled further away from Qualcomm. Full-year revenue guidance midpoint is $1.64B, down 21% year over year; Non-GAAP operating income midpoint is $177M, down 73% year over year.

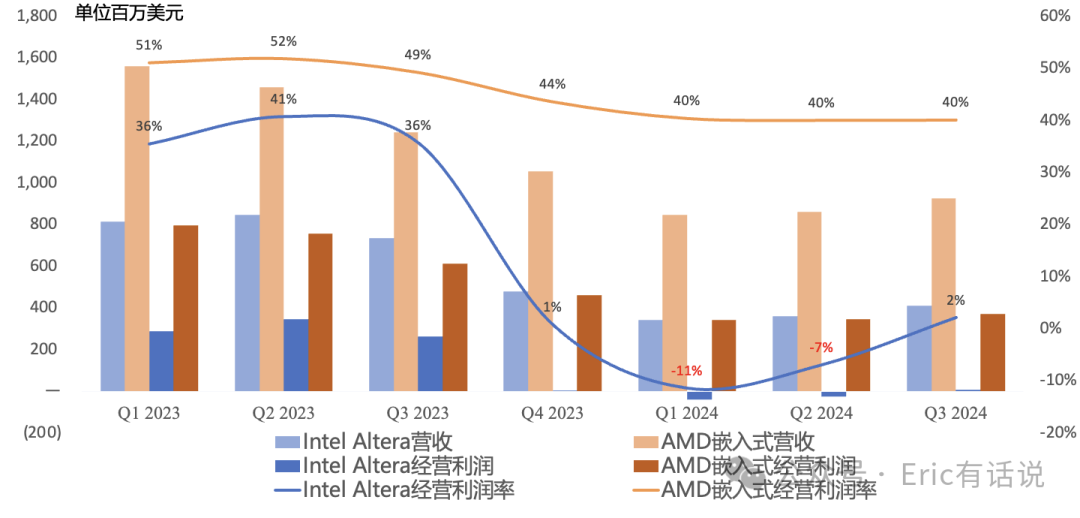

Altera revenue was $412M, down 44% year over year but up 14% sequentially. Q4 revenue is guided to grow high-single digits sequentially (implying no more than $450M). Recall Q1 Pat guided Q4 revenue at $500M — another miss. External strategic investment in Altera is expected to close in early 2025.

Call Highlights:

The company overall is impacted by weak downstream demand and high inventory. Inventory normalization is expected to persist through H1 next year. The plan is to invest for 3%-5% revenue growth next year, though that does not necessarily represent the actual growth rate.

Plans to move the edge business from NEX to CCG, with NEX focusing on networking and communications. Plans to re-segment business revenue reporting again in 2025 Q1 (truly exhausting).

Guides Q4 full-year revenue midpoint at $13.8B, down 10% year over year and up 4% sequentially. Sequential growth is mainly driven by seasonal PC strength, while data center and networking are guided flat. Non-GAAP gross margin 39.5%, down 9.3 percentage points year over year, pressured by Lunar Lake ramp and 18A R&D.

2025 gross margin is expected to be further pressured by Lunar Lake ramp and Intel 18A ramp, especially in H2.39.5% may be the midpoint level. 2026 gross margin is expected to improve significantly.

Intel Foundry's current external revenue comes mainly from advanced packaging, which turned profitable in Q3 and is expected to grow in 2025. Foundry's long-term revenue relies primarily on internal supply, with a target of $15B in external revenue by 2030.

2024 gross capex lowered to $25B, net capex lowered to $11B. 2025 gross capex $20-23B (unchanged), net capex $12-14B (unchanged). 2025 adjusted free cash flow expected to turn positive.

Previously noted at the end of the last earnings report:

Pat took a big bath this quarter, writing off everything possible, then continued to serve up pies to the market: a 2026 triumphant return, attempting to rescue the below-book stock price. Intel's future is now entirely bet on 18A — a high-stakes gamble, with all of Pat's big pies premised on 18A.

Intel's latest desktop Arrow Lake reveals two problems: TSMC's process leads Intel by a wide margin, and Intel's design capability lags Apple by a wide margin. Consequently, Arrow Lake has become a rare generational product where performance actually regressed.

Manchester United's Ten Hag has been fired. Wonder how long Pat can last.