Investors began pricing in memory-like shortages for server CPUs as AI inference demand surged, sending Intel, AMD, and Arm shares sharply higher.

Intel Q1 Earnings:

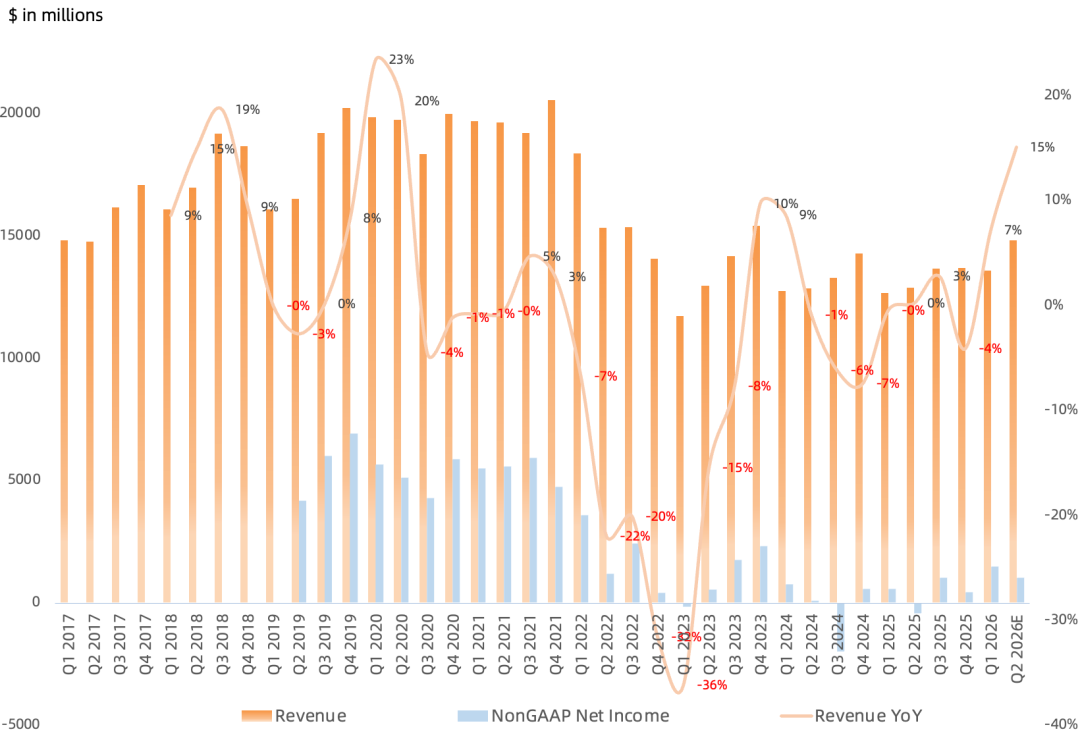

Revenue $13.58B, up 7% year over year, down 1% sequentially, above prior guidance range of $11.7-12.7B; next quarter revenue midpoint guided at $14.3B, up 11% year over year, up 5% sequentially;

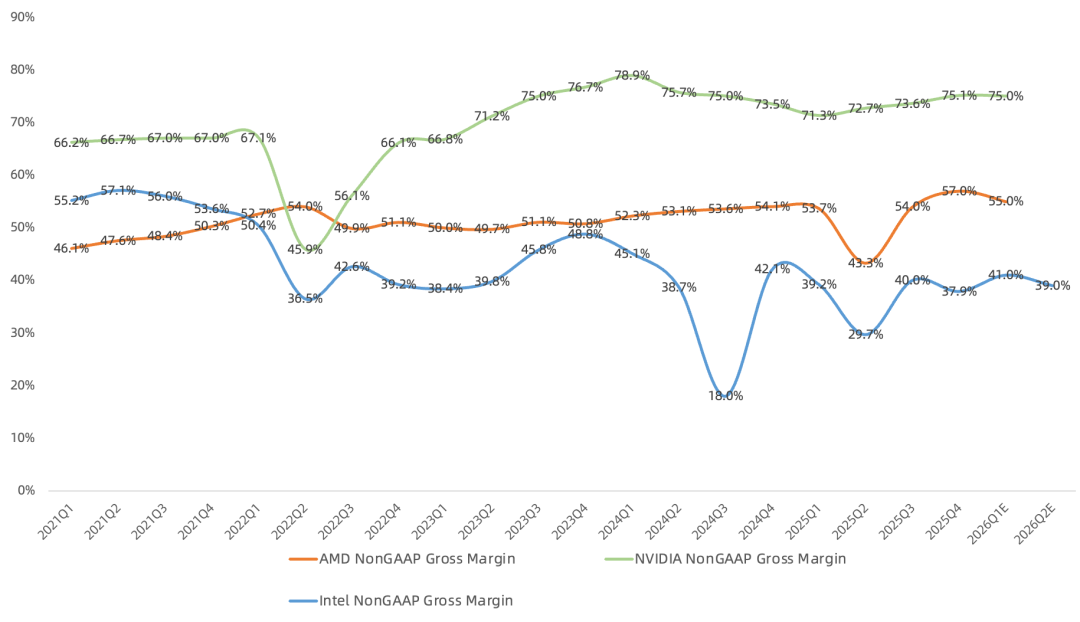

GAAP gross margin 39.4%, up 2.5 percentage points year over year, up 2.7 percentage points sequentially; non-GAAP gross margin 41%, up 1.8 percentage points year over year, up 3.1 percentage points sequentially; next quarter non-GAAP gross margin guided at 39%, down 2 percentage points sequentially;

GAAP operating loss $3.14B, non-GAAP operating income $1.67B, up 142% year over year, up 38% sequentially;

GAAP net loss $4.28B, non-GAAP net income $1.49B, up 156% year over year, up 94% sequentially; next quarter GAAP net income guided at $410M, non-GAAP net income guided at $1.02B;

Operating cash flow $1.1B, adjusted free cash flow negative $2.02B; as of quarter-end, total equity attributable to shareholders $111.4B;

Q1 Business Details:

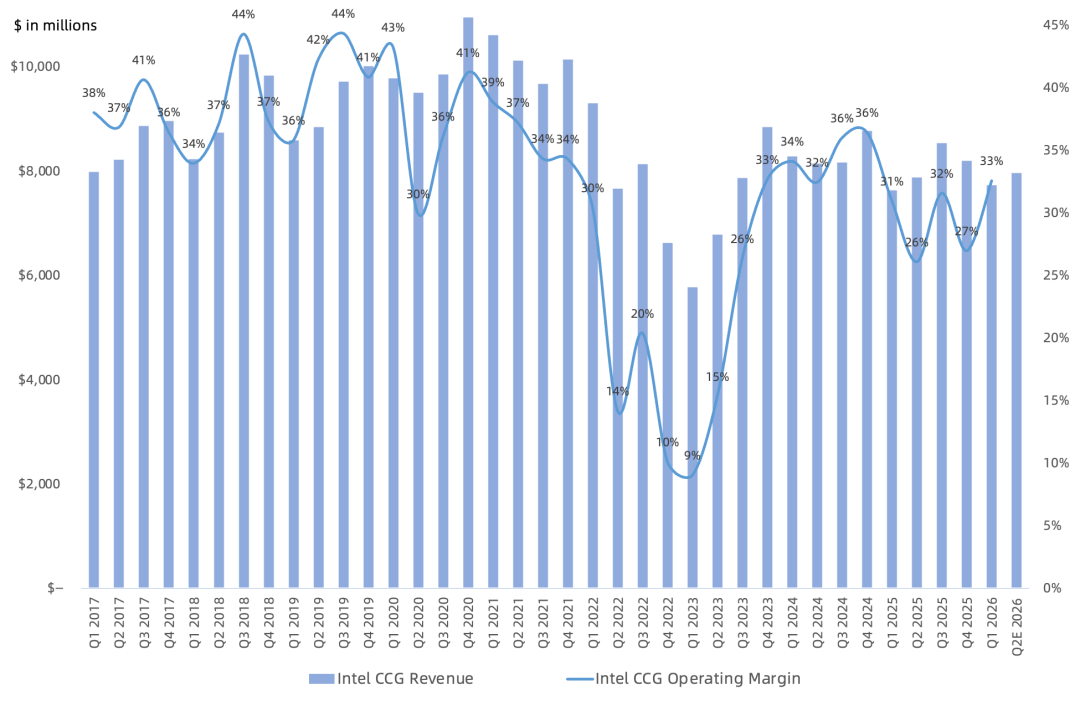

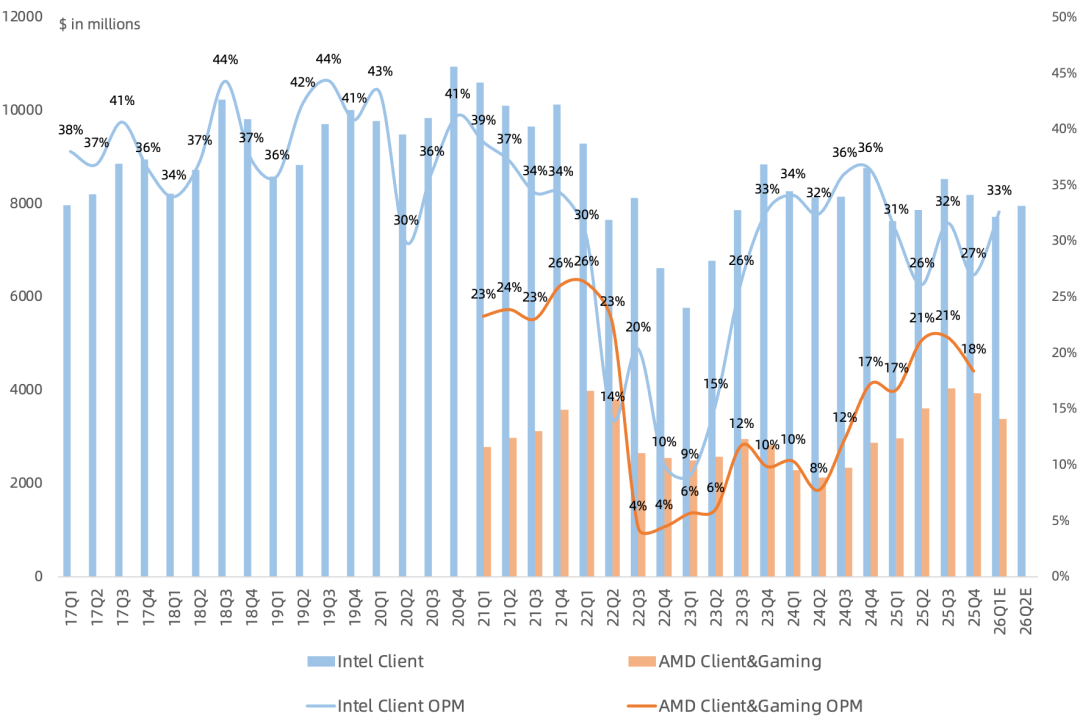

CCG revenue $7.73B, up 1% year over year, down 6% sequentially, 57% of revenue mix; operating income $2.52B, up 7% year over year, operating margin 33% (AMD 25Q4 18%), remains Intel's most profitable business;

AI PC revenue up 8% sequentially, 60%+ of client CPU mix; PC demand expected to weaken in H2, full-year PC shipments to decline low double-digits year over year, but PC revenue relatively flat in H2 due to customer inventory build; 18A Panther Lake ramps next quarter, share in product mix rises sharply, severely dragging down margins;

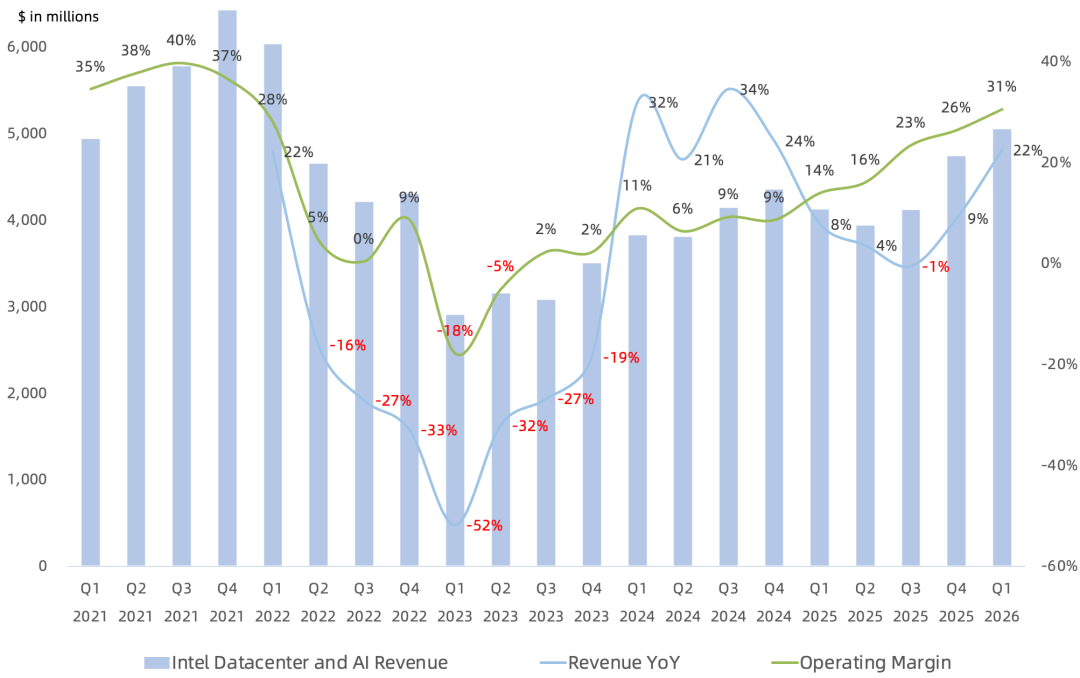

DCAI revenue $5.05B, up 22% year over year, up 7% sequentially, 37% of revenue mix; operating income $1.54B, up 168% year over year, up 23% sequentially, operating margin 30.5%, up for 6th consecutive quarter, highest since 2022 Q1;

DCAI signed multiple long-term agreements, including with Google, Xeon 6 selected as host CPU for NVIDIA DGX Rubin NVL8 systems, co-designing next-gen heterogeneous AI inference architecture with SambaNova; due to Xeon's industry-leading position in memory, security, and network orchestration, it remains the most widely deployed host CPU; full-year CPU server industry and company shipments both expected to achieve strong double-digit growth, and momentum to extend through 2027; server CPU per-core ASP to increase;

Customers seeking custom silicon for AI, networking, and cloud workloads; company ASIC design services (IPU) revenue up 30%+ sequentially, nearly doubled year over year, run-rate revenue exceeds $1B;

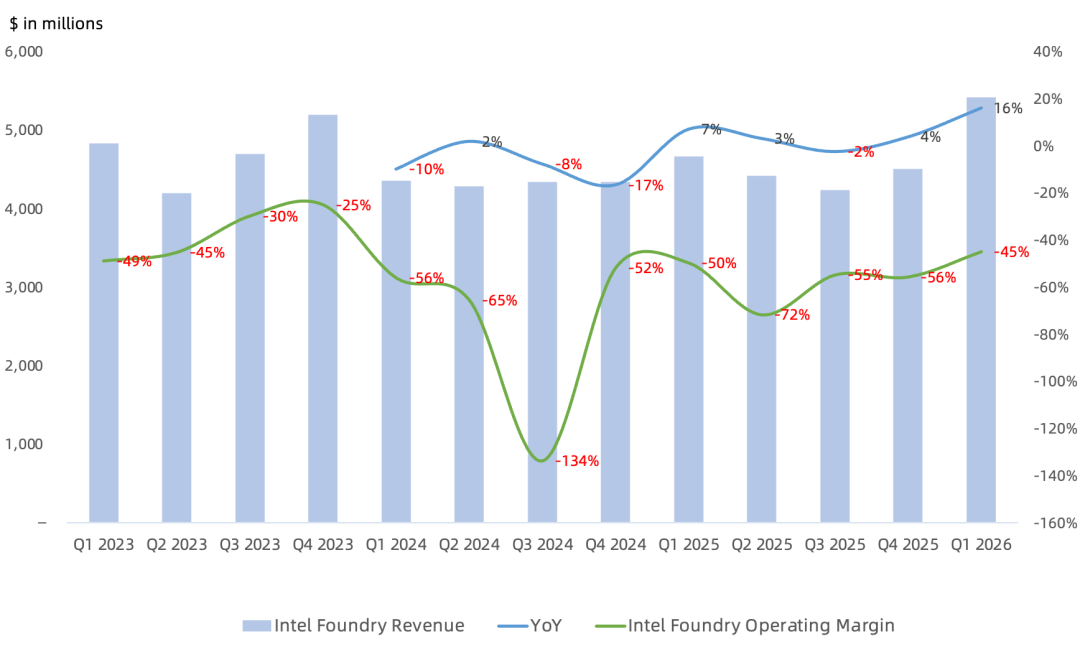

Intel Foundry revenue $5.42B, up 16% year over year, up 20% sequentially, mainly driven by increased EUV wafer mix from Intel 3 and significant growth from 18A; external foundry revenue $174M, down 22% sequentially; operating loss $2.44B, loss widened year over year, narrowed sequentially, operating loss rate 45%;

Intel 3 Xeon 6 and Intel 18A Core Series 3 now in full volume production ramp; 18A yield now above internal forecast; external customers still engaging on 18A-P and 14A; 14A maturity, yield, and performance exceeding 18A at same time point, co-developing PDKs with multiple customers, intentionally increased 14A investment; expect earlier design commitments to emerge from H2 this year and further expand in H1 2027;

Advanced packaging customer backlog grew this quarter, announced multi-year expansion of backend facilities in Malaysia; this demand to convert to revenue starting 2027; expect advanced packaging future market to reach billions annually; over time, advanced packaging gross margin to reach at least foundry industry average, or foundry average gross margin.

Call Highlights:

Management guides Q2 revenue $13.8-14.8B, midpoint implies 11% year over year, 5% sequential, two consecutive quarters of year-over-year growth, driven mainly by data center CPU business;

Expect Q2 DCAI and CCG revenue both up sequentially; CCG up low single-digits sequentially, DCAI up double-digits sequentially; Foundry revenue no guidance given;

Expect Q2 non-GAAP gross margin 39%, down 2 percentage points sequentially, mainly dragged by 18A ramp;

Expect 2026 revenue by halves to follow past decade's seasonality, with server outperforming seasonality, PC underperforming seasonality;

2026 gross capex target raised from "flat to slightly down" to "flat," and spending more skewed to equipment/tools; 2026 equipment investment to grow 25% to address supply shortages;

Increasing wafer starts on three nodes: Intel 7, Intel 3, and Intel 18A; also continuing to use external foundry (TSMC); expect Intel Foundry operating loss to improve gradually through the year, but several more quarters needed to reach foundry average gross margin, though progress better than expected;

Management believes Intel has three strategically important assets to benefit from AI demand: x86 CPU franchise, advanced packaging technology, vast manufacturing network; CPU becoming indispensable foundation of AI era again, customers deploying server CPUs and AI chips at increasingly CPU-heavy ratios;

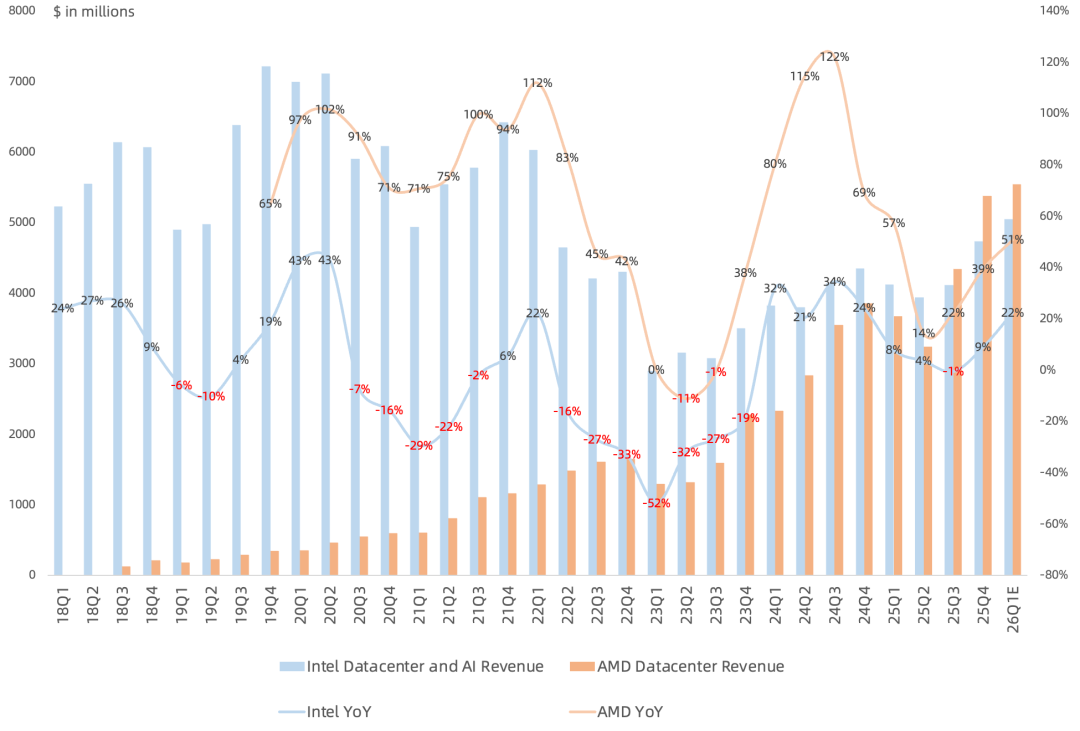

Management did not directly address whether TeraFab collaboration is a foundry contract or process licensing; supply constraints costing billions in revenue; responding to Wall Street questions on Arm and AMD CPU competition, Lip-Bu Tan said CPU demand very strong now, everyone will benefit;

Excluding Fab 34 JV repurchase impact, still expect full-year adjusted free cash flow positive; financed Fab 34 JV repurchase with ~$7.7B cash and $6.5B new debt, still committed to repay all $2.5B debt maturing this year and all $3.8B maturing in 2027;

Expect non-controlling interest (NCI) ~$250M per quarter on average this year, ~$1.1B full year in 2027/2028 (GAAP basis);

Previously Noted at End of 2025Q3 Earnings:

After overturning the IDM 2.0 strategy last quarter, this quarter Lip-Bu Tan does a 180-degree reversal and revives Pat's IDM 2.0 foundry dream; with backing from big-name investors and positive 18A progress, Intel's short-term surge is huge, completely breaking free from its prior valuation framework.

At last quarter's earnings, we noted that the market's short-term hype around server CPU shortage narratives and betting on 18A volume to turn Foundry around are not things that can materialize in earnings anytime soon; they need time to settle. But now the market's hype speed and sentiment don't need to wait for time to settle. From an event perspective, management's announcement to repurchase the Ireland Fab 34 JV is a major inflection point.

As for the media's over-hyped "AI training typically ~7-8 GPUs per 1 CPU, AI inference may move to 3-4 GPUs per 1 CPU, as we enter agentic and multi-agent it could become 1:1, even potentially flip," this statement is somewhat misleading, especially combined with Google's just-released TPU 8i/8t using Google's homegrown Axion CPU for the CPU header for the first time, NVIDIA Vera CPU rack, and Arm itself stepping in to make chips; last year Arm still said 2025 hyperscaler new server CPU chips nearly 50% Arm architecture.

So from a long-term view, how should Intel be valued? Logic may be sum-of-the-parts: PC business (reference Qualcomm valuation), data center business (reference growth stock valuation), foundry business (foundry P/B valuation); you can run the numbers yourself.