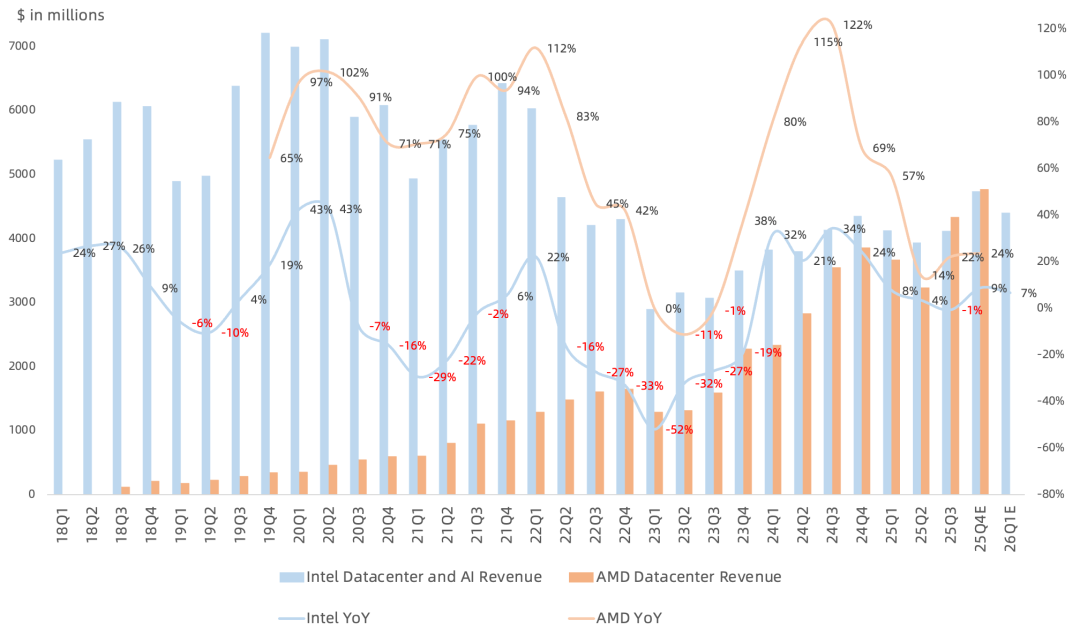

Early this year the market began focusing on surging CPU demand in the AI inference era potentially causing a memory-like shortage in server CPUs. Reality: server CPU demand is strong and Intel capacity constraints are real, but prices have not spiked like memory.

Intel Q4 Earnings:

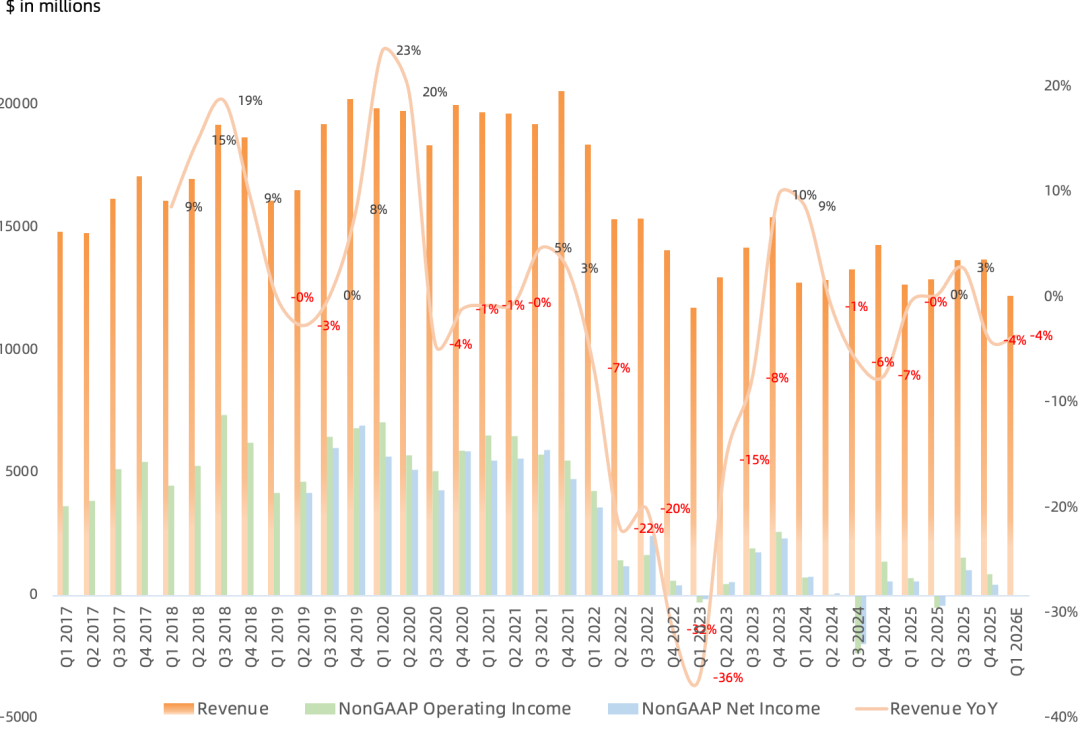

Revenue of $13.67B, down 4% year over year, up 0.2% sequentially, at the upper end of prior guidance range of $12.8-13.8B. Projected next quarter revenue midpoint of $12.2B, down 4% year over year, down 11% sequentially.

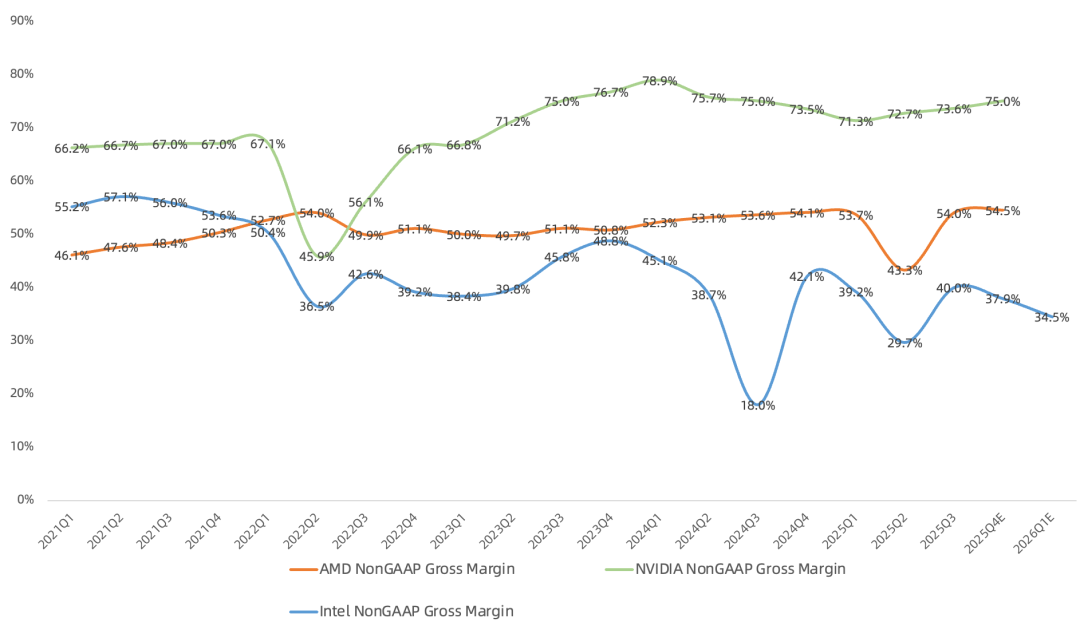

GAAP gross margin 36.1%, down 3.1 pp year over year, down 2.1 pp sequentially. Non-GAAP gross margin 37.9%, down 4.2 pp year over year, down 2.1 pp sequentially. Projected next quarter Non-GAAP gross margin 34.5%, down 3.4 pp sequentially.

GAAP operating income $580M, up 41% year over year, down 15% sequentially. Non-GAAP operating income $1.21B, down 12% year over year, down 21% sequentially.

GAAP net loss of $330M, loss widened year over year, swung from profit to loss sequentially. Non-GAAP net income $770M, up 35% year over year, down 25% sequentially. Projected next quarter GAAP net loss of $1.02B, Non-GAAP net income breakeven, down sharply both year over year and sequentially.

Operating cash flow $4.29B, adjusted free cash flow $2.22B. As of quarter-end, total equity attributable to shareholders $114.28B.

Q4 Business Details:

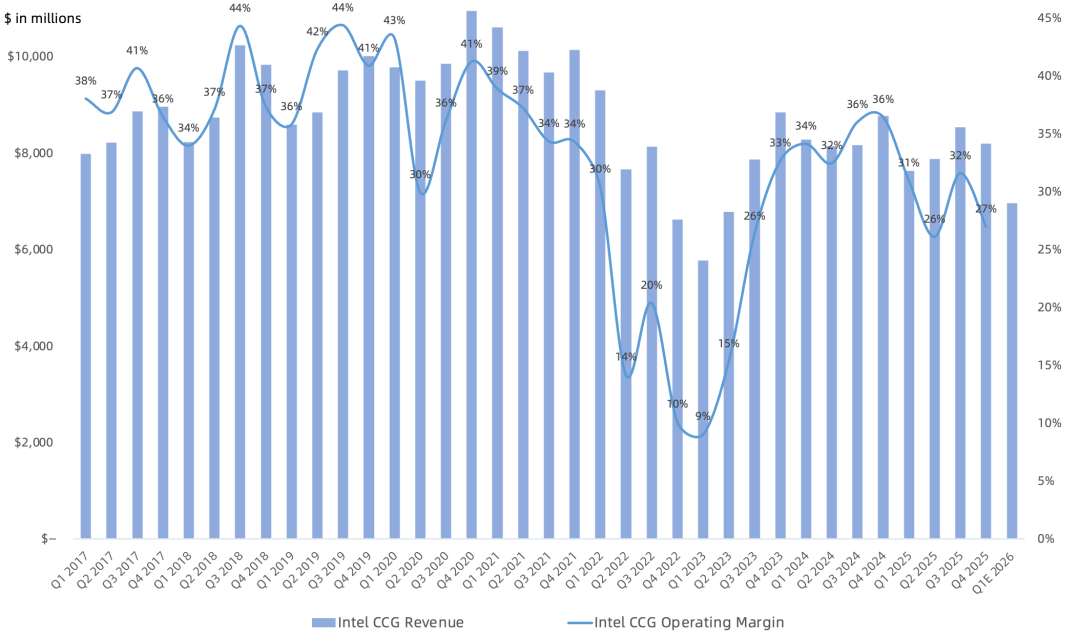

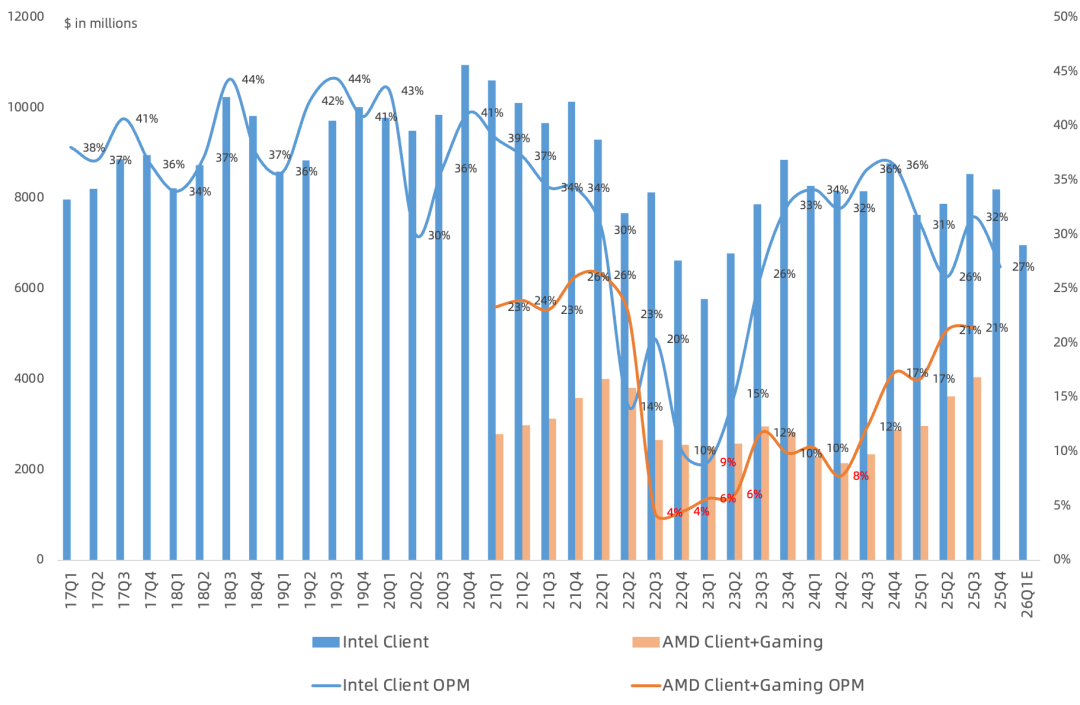

CCG revenue $8.19B, down 7% year over year, down 4% sequentially, 60% of revenue. Operating income $2.21B, down 31% year over year, operating margin 27% (AMD 25Q3 21%), remains Intel's most profitable business.

2025 PC consumer TAM exceeds 290M units. This quarter AI PC revenue grew double digits sequentially. Panther Lake current margin below company average. On Lunar Lake, memory secured per current forecast is sufficient, but Lunar Lake margin is indeed low. Management acknowledges surging memory and storage prices will suppress PC market demand. Desktop CPU Nova Lake (Intel 18A + TSMC) targeting volume production by end of 2026.

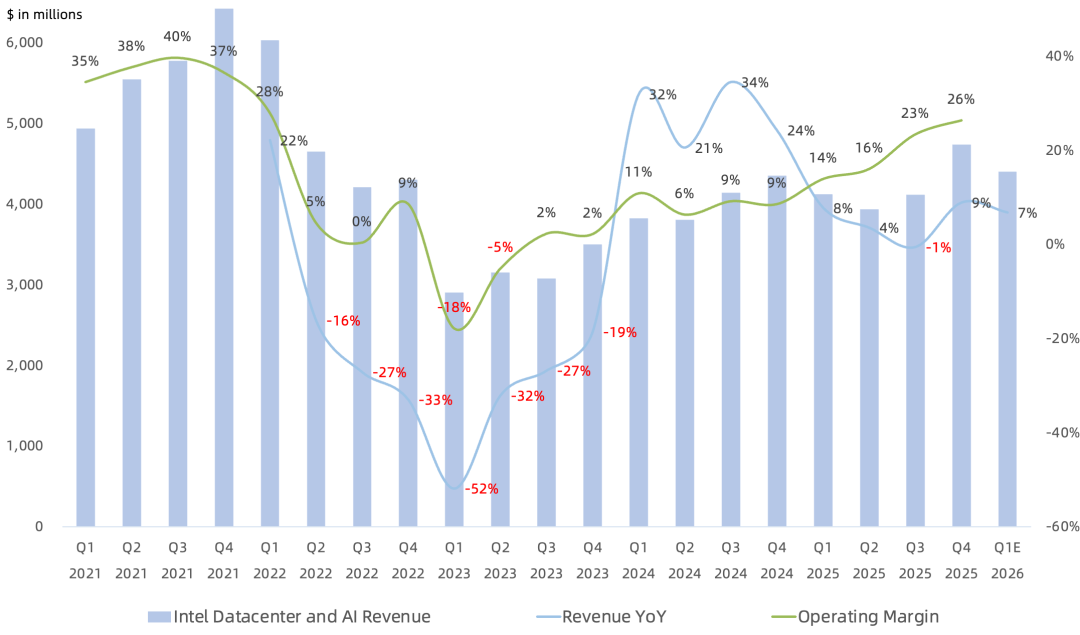

DCAI revenue $4.74B, down 9% year over year, up 15% sequentially, 35% of revenue. Operating income $1.25B, up 234% year over year, up 30% sequentially, operating margin 26.4%, up for five consecutive quarters, highest since 2022 Q2. Traditional server and networking revenue grew double digits both year over year and sequentially. Traditional server demand remains very strong, benefiting mainstream server CPU products: 4th Gen Xeon Scalable Sapphire Rapids (Intel 7) and 5th Gen Emerald Rapids (Intel 7). New product 6th Gen Granite Rapids (Intel 3 + Intel 7 P-cores) continues to ramp.

Future simplification of server CPU roadmap, concentrating resources on 7th Gen Xeon Diamond Rapids (Intel 18A P-cores) supporting 16-channel DDR with MRDIMM Gen2, and accelerating development of 8th Gen Coral Rapids supporting hyper-threading return where possible. Close collaboration with NVIDIA on custom server CPU with NVLink.

Intel 7 / Intel 3 / 18A three-node wafer starts continue to increase, seeing 7-8% yield improvement monthly. Management believes Q2 supply will definitely improve, but will not immediately fully exit capacity constraints. CEO disappointed at inability to fully meet market demand; while yields meet internal plan, they remain below CEO's target. Prioritizing internal wafer supply to data center, and increasing external wafer procurement share for PC. Entering 2026, buffer inventory exhausted, and the structural shift of 'wafers tilted to server' begun in 25Q3 will not yield factory output until end of 2026 Q1; internal supply constraints most acute in Q1.

Customers seeking custom silicon for AI, networking, and cloud workloads; company's ASIC design services division 2025 revenue up >50%, Q4 run-rate revenue >$1B. Future ASIC TAM $100B.

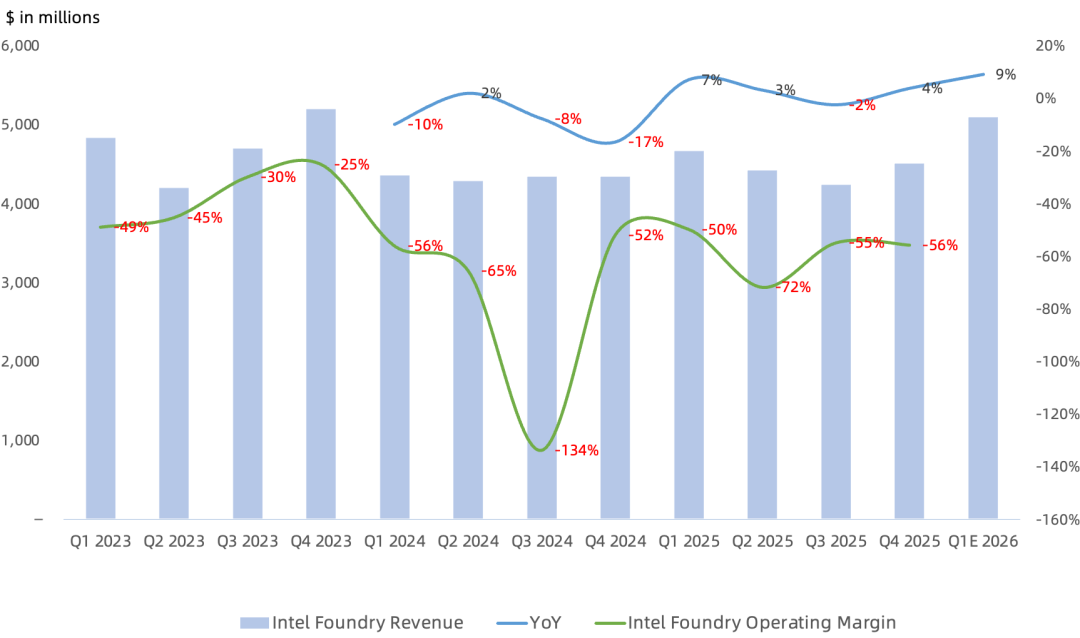

Intel Foundry revenue $4.51B, up 4% year over year, up 6% sequentially, of which external foundry revenue $220M, driven mainly by US government projects and deconsolidated Altera. Operating loss $2.51B, loss widened both year over year and sequentially, operating loss rate 55.7%. Intel Foundry EUV wafer revenue share rose from <1% in 2023 to >10% in 2025.

Intel Foundry becomes the world's only semiconductor manufacturer to have delivered 'GAA + backside power', ramping in Oregon and Arizona fabs. 14A will use High-NA EUV. Intel 18A-P progressing well, engaging internal and external customers on this node. Intel 14A development remains on track. Will not invest in 14A capacity before securing 14A customers, only willing to do 14A-related R&D. Expect 14A customers to make definitive supplier selections in H2 2026, extending into H1 2027. Project 14A risk production by end of 2027, true volume production in 2028. More details to be provided at H2 2026 analyst day.

Advanced packaging offers strong differentiation, especially EMIB and EMIB-T, supporting customer ramps starting H2 2026. Previously thought advanced packaging opportunity was 'hundreds of millions' while foundry was 'billions'; now from early customer engagements, scale on many advanced packaging opportunities will far exceed $1B, with several customers even willing to pay subscription-style upfront fees due to severe advanced packaging supply shortage.

Mobileye revenue $450M, down 9% year over year, down 12% sequentially, revenue falling further behind Qualcomm and NVIDIA. Operating income $41M, down 60% year over year. Average system price $50.8, up 2% year over year. Mobileye and IMS combined other businesses operating loss of $8M.

Call Highlights:

Management projects Q1 revenue of $11.7-12.7B; at midpoint, down 4% year over year, down 11% sequentially, second consecutive quarter of year-over-year decline, mainly due to seasonal slowdown in revenue pillar PC business.

Projected Q1 DCAI and CCG revenue both down sequentially; CCG decline more severe (double digits), DCAI possibly down high single digits; Foundry revenue up double digits sequentially.

Projected Q1 Non-GAAP gross margin 34.5%. Higher PC outsourcing mix and 18A ramp dragging margin. This year's first phase margin target is to pull back to 40%, then update subsequent targets.

2026 gross capex target changed from 'below $18B' to 'flat to slightly down', with spending more weighted to H1. Facility spending significantly reduced, believing cleanroom space is adequate; shifting more funds to equipment tools. Therefore 2026 equipment investment will increase significantly versus 2025 to address supply shortages.

Management sees server CPU demand as largely x86-related; does not believe supply constraints will benefit AMD share; key remains product. Believes delivering 16-channel Diamond Rapids and accelerating hyper-threading-enabled Coral Rapids return will determine share trajectory over the next few years. Intel server CPUs remain the preferred choice for AI head nodes.

NVIDIA's $5B investment closed in Q4. Plan to repay all $2.5B maturing debt on schedule in 2026.

Projected non-controlling interest (NCI) ~$325M in Q1, ~$1.2B for full year (GAAP basis). NCI expected to grow significantly again in 2027.

Previously noted at the end of the last earnings report:

After overturning the IDM 2.0 strategy last quarter, this quarter Lip-Bu Tan does a 180-degree reversal and revives Pat's IDM 2.0 foundry dream; with backing from big-name investors and positive 18A progress, Intel's short-term surge is huge, completely breaking free from its prior valuation framework.

Intel shares ran up into earnings, pricing in high expectations. The market desperately wanted to hear improving fundamentals and see a confirmed recovery trend. As for the near-term hype around server CPU shortages and betting on 18A ramp to turn Foundry around—neither will materialize in earnings anytime soon; they need time to settle.