In the previous quarter's earnings postscript I noted:

Intel Q2 Earnings:

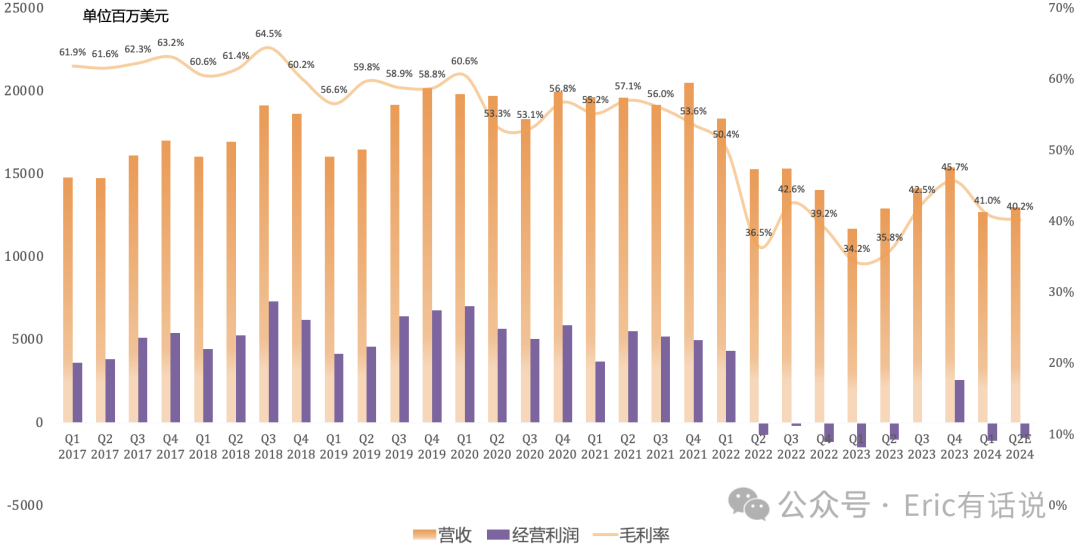

Revenue was $12.833B, down 1% year over year, ending two consecutive quarters of year-over-year growth, and up 1% sequentially; next quarter revenue is guided at $13.0B, down 8% year over year.

GAAP gross margin was 35.4%, down 0.6 percentage points year over year and 5.6 percentage points sequentially; next quarter GAAP gross margin is expected to decline further.

GAAP operating loss was $1.964B, the second consecutive quarterly loss; next quarter is expected to remain in an operating loss.

GAAP net loss was $1.654B, the second consecutive quarterly loss; next quarter is expected to remain in a net loss.

Non-GAAP net income was $83M, down 85% year over year and 89% sequentially; next quarter Non-GAAP net loss is guided at $128M, the first loss in six quarters.

Adjusted free cash flow was $8.155B; full-year free cash flow is expected to be negative, with a return to positive in 2025.

Q2 Business Details:

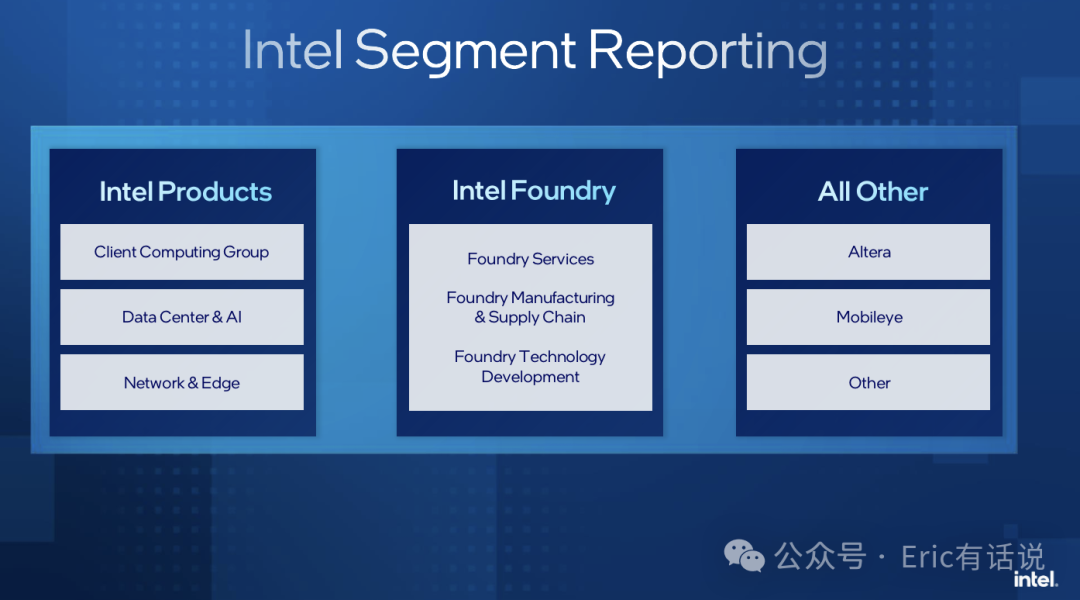

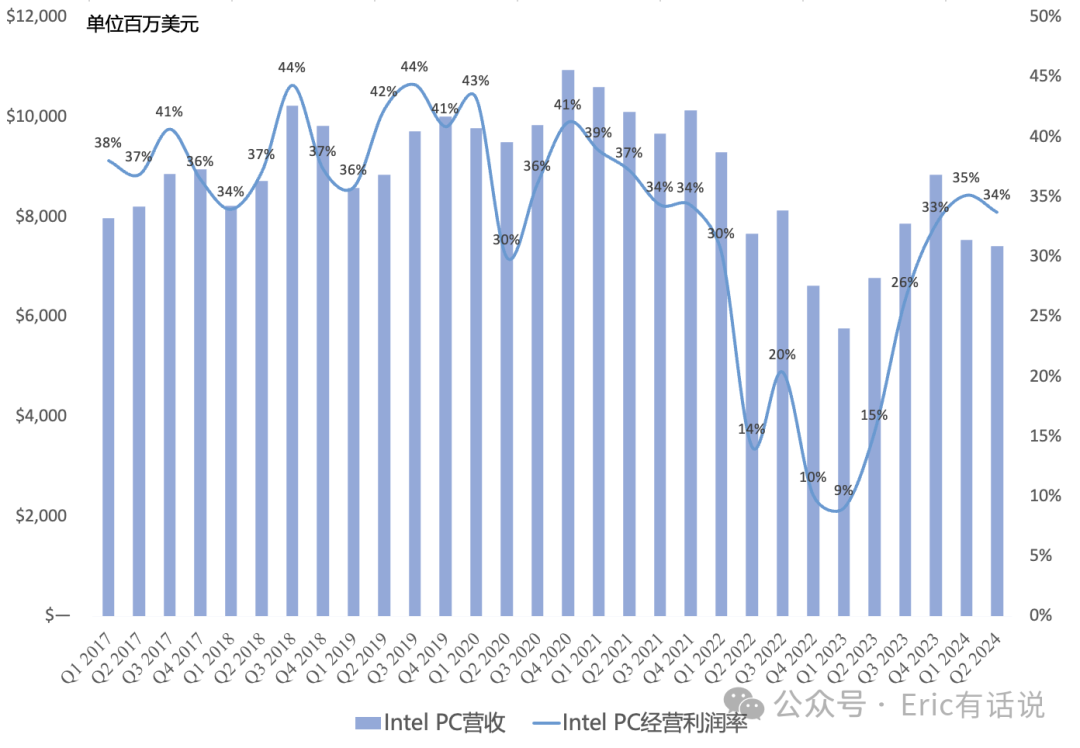

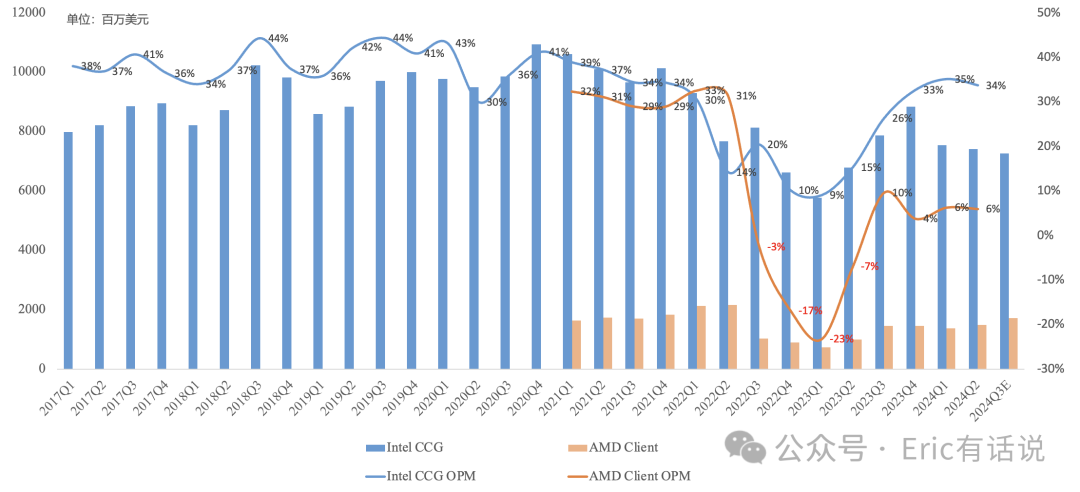

CCG revenue was $7.41B, up 9% year over year, the third consecutive quarter of year-over-year growth, down 2% sequentially, the second consecutive sequential decline, accounting for 58% of revenue; operating income was $2.497B, up 140% year over year and down 6% sequentially, representing 469% of Intel's total operating income.

Intel 4-based Meteor Lake Core Ultra Q2 shipments doubled sequentially, with cumulative shipments exceeding 15M, helping gross margin; the company expects 2024 AI PC shipments to exceed 40M, with cumulative shipments surpassing 100M by end of 2025; 2024 PC TAM is expected to grow low single digits year over year; TSMC 3nm-based Lunar Lake for notebooks begins shipping in Q3, and Arrow Lake for desktops in Q4; Lunar Lake carries lower gross margins due to integrated high-cost external memory and TSMC 3nm; second-half PC shipments are primarily constrained by elevated inventory.

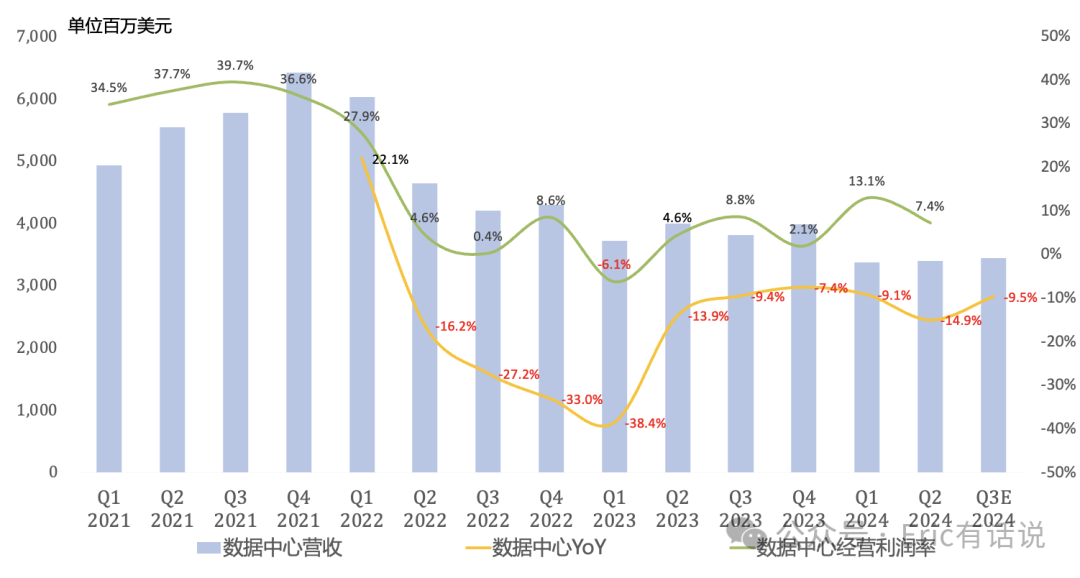

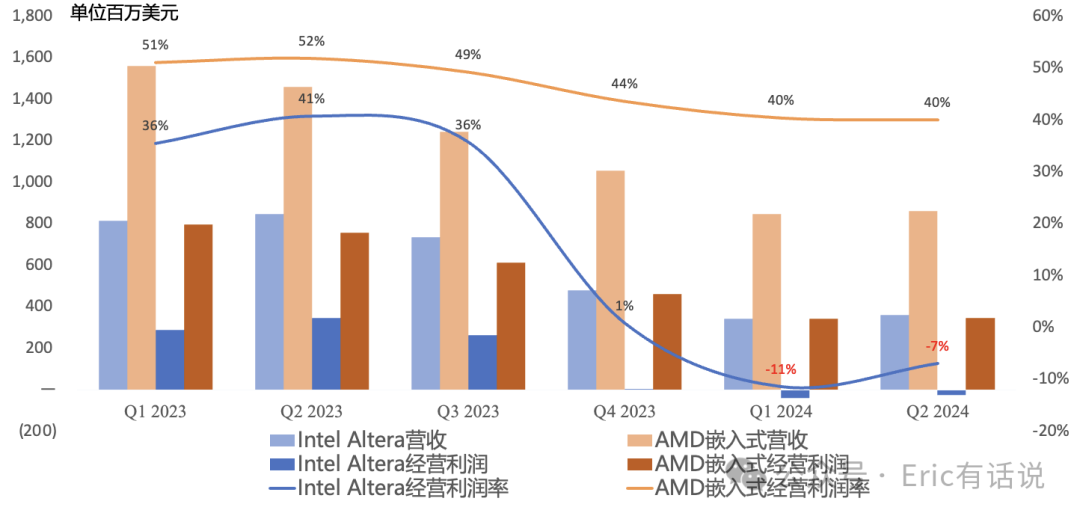

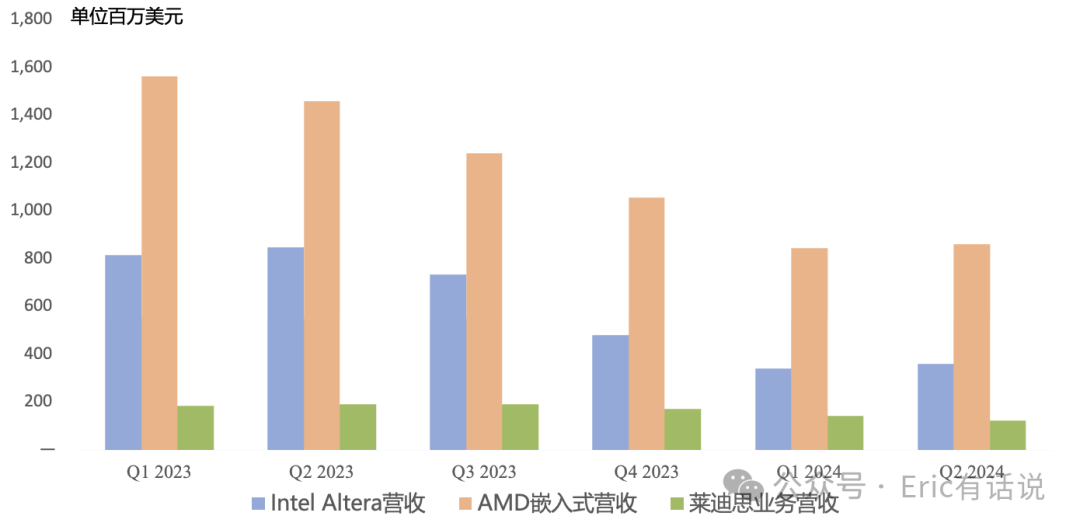

DCAI revenue was $3.045B (Intel has excluded Altera from disclosed figures since 24Q1), down 4% year over year, continuing its slump, and roughly flat sequentially; operating income was $276M, down 43% sequentially, with operating margin plummeting to 9% (chart below adds Altera back).

Over 130M Xeon CPUs are installed in data centers globally; the first Intel 3-based Sierra Forest (E-cores for cloud) is in volume production, with Granite Rapids (P-cores for enterprise) and Gaudi 3 expected to begin volume production in Q3; the traditional server market is recovering moderately, weighed down by domestic demand.

On AI, the company no longer cited the scale of full-year AI revenue to be driven by Gaudi 3 shipping in the second half; recall that in Q4 last year Intel claimed a 2024 Gaudi portfolio pipeline of over $2B, in Q1 it said only $500M+ had materialized, and in Q2 it stopped citing a specific figure—draw your own conclusions.

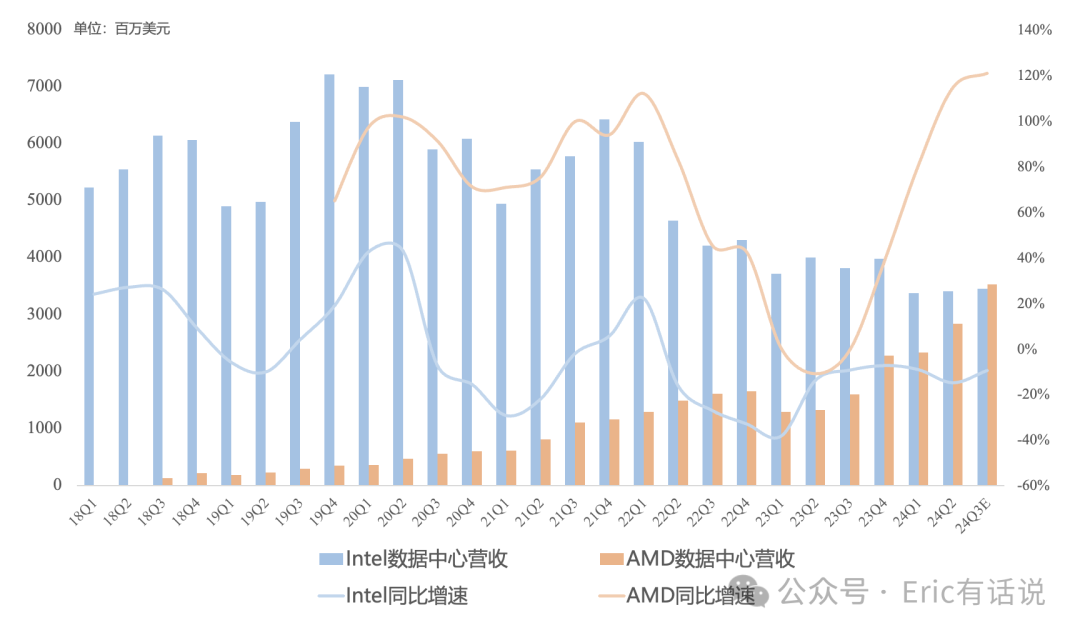

Q3 data center revenue is expected to grow modestly sequentially; AMD's data center revenue will formally surpass Intel's.

NEX revenue was $1.344B, down 2% year over year, the seventh consecutive quarterly decline, and down 2% sequentially; operating income was $139M; excluding the communications market, NEX first-half revenue and operating income grew 10% year over year; all non-communications segments are recovering, and IPU is expected to become a 2025 growth driver for NEX.

Intel Foundry revenue was $4.32B, up 3% year over year; operating loss was $2.83B, a new record; Q3 Foundry operating loss rate is expected to be consistent with Q2, as 85% of wafers remain pre-EUV, driving high costs; a second High-NA EUV tool is preparing to move into the Oregon fab; IFS (external) revenue was $66M, down 72% year over year.

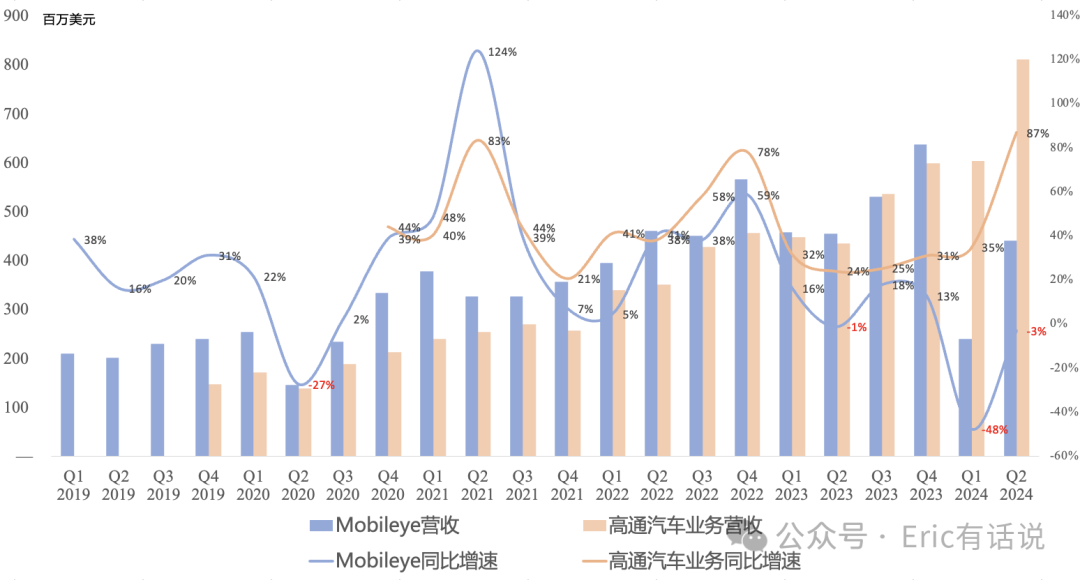

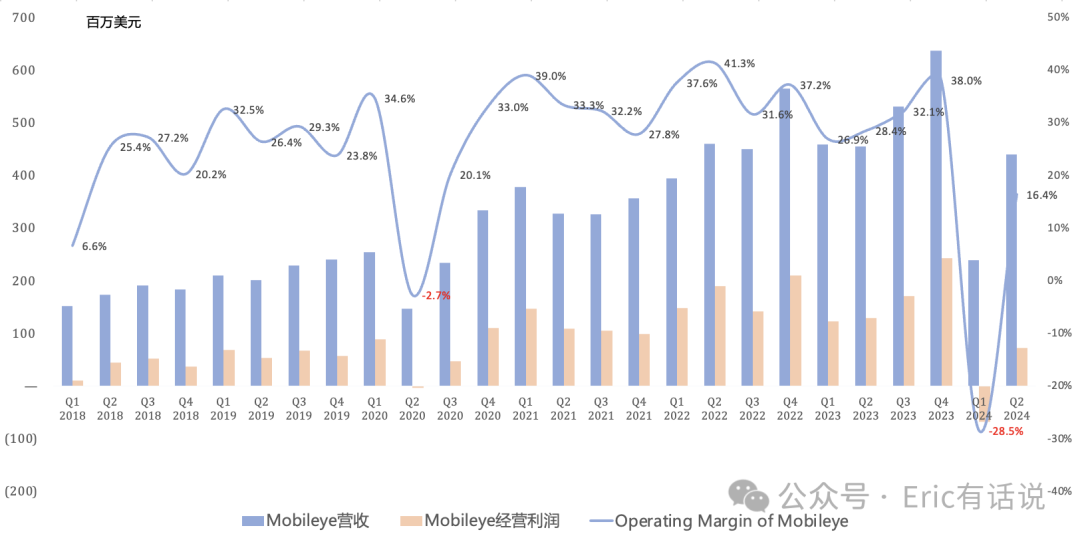

Mobileye revenue was $440M, down 3% year over year and up 84% sequentially; operating income was $72M; revenue gap with Qualcomm has widened; full-year revenue and profit guidance were lowered due to European OEM weakness in the domestic auto market; Mobileye 2024 full-year revenue is now expected at $1.64B, down 21% year over year, with Non-GAAP operating income lowered to $180M.

Altera revenue was $361M, down 58% year over year and up 6% sequentially; customers are still destocking; orders are expected to recover in the second half with double-digit sequential revenue growth; Agilex 5 & 7 pipeline is strong; Agilex 3 is on track; Altera is expected to be fully operationally independent by year-end, with an IPO next year.

Call Highlights:

Q2 margin decline was primarily due to rapid ramp of Ultra AI CPUs, accelerated Intel 4/Intel 3 process transitions at the Ireland fab, and some idle capacity.

The second half of 2024 is expected to show sequential quarterly improvement, but the recovery pace is below expectations; Q3 results will be impacted by CCG/DCAI inventory digestion and NEX/Altera/Mobileye underperformance; Q4 revenue is expected to grow sequentially at the upper end of the 0-5% range; Q3 revenue midpoint is guided at $13.0B, down 8% year over year and up 1% sequentially; Client revenue is expected to be flat to down slightly sequentially, while data center and edge markets grow modestly; gross margin is expected to decline modestly sequentially, pressured by TSMC foundry costs.

Clearwater Forest (GAA 18A E-cores server) / Panther Lake (RibbonFET+PowerVia, 18A client) ramp in 25H1 remains on track, with launch expected in 25H2, at which point external foundry reliance will decrease; Intel 14A and Intel 10A will use High-NA EUV.

2024 gross capex is lowered to $25B-$27B, net capex $11B-$13B; 2025 gross capex $20B-$23B, net capex $12B-$14B; adjusted free cash flow is expected to turn positive in 2025, with gross margin improving modestly, and a significant gross margin uplift in 2026 as TSMC outsourced orders return in-house.

The company plans to reduce headcount by 15%+ by end of 2025; 2024 opex is expected to decline to $20B, 2025 to $17.5B, and 2026 to $15B.

Dividends will be suspended starting in Q4.

Previously noted at the end of the last earnings report:

This Intel report couldn't even preserve the PC fig leaf, paling against AMD's guidance for an even stronger PC seasonal peak; notebook newcomer Lunar Lake faces margin pressure, data center is on the cusp of a historic overtaking by AMD, while Pat continues to serve up visions of a great 2026.