As I mentioned at the end of the last earnings report:

On December 1, 2024, Pat announced his retirement and resigned from the board.

Intel Q4 Earnings:

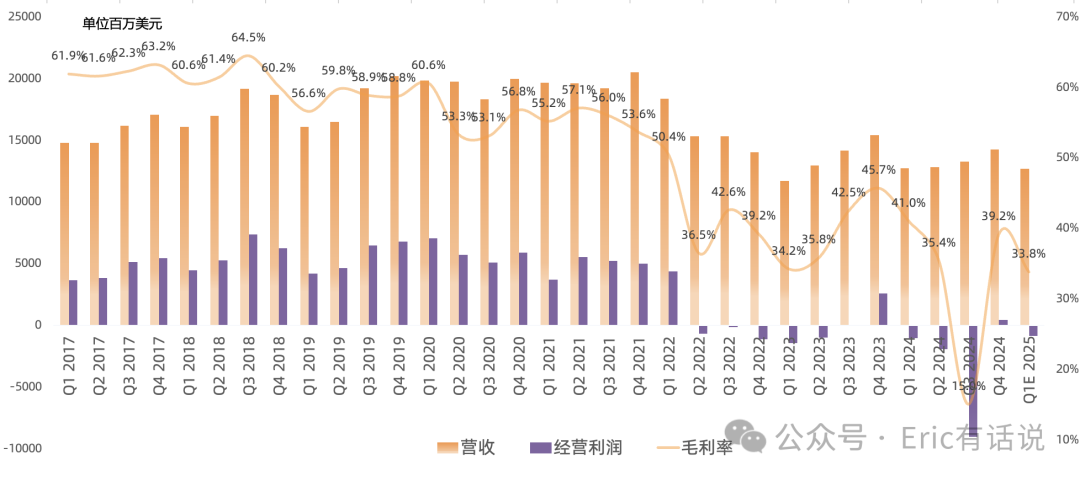

Revenue was $14.26B, down 7% year over year, the third consecutive quarter of year-over-year decline, and up 7% sequentially. Full-year 2024 revenue was $53.1B, down 2% year over year. Next quarter revenue is guided to $12.7B, down 0.2% year over year, marking the fourth consecutive quarter of year-over-year decline.

GAAP gross margin was 39.2%, down 6.5 percentage points year over year and 24.2 percentage points sequentially. Next quarter GAAP gross margin is guided to 33.8%, down 7.2 percentage points year over year.

GAAP operating income was $412M, ending three consecutive quarters of operating losses. Next quarter is expected to return to an operating loss.

GAAP net loss was $153M, the fourth consecutive quarter of net losses. Next quarter is expected to remain in a net loss. Full-year 2024 GAAP net loss was $19.233B.

Non-GAAP net income was $568M. Next quarter non-GAAP is guided to breakeven. Full-year 2024 non-GAAP net loss was $566M.

Adjusted free cash flow was -$1.503B. Full-year 2024 adjusted free cash flow was -$2.228B. 2025 free cash flow is expected to turn positive.

As of quarter-end, the company's net assets were $99.27B.

Full-year 2024 top customer revenue share was 19%, second was 14%, third was 12%. Full-year 2024 mainland China revenue share was 29%, U.S. 24%, Singapore 19%, Taiwan 15%.

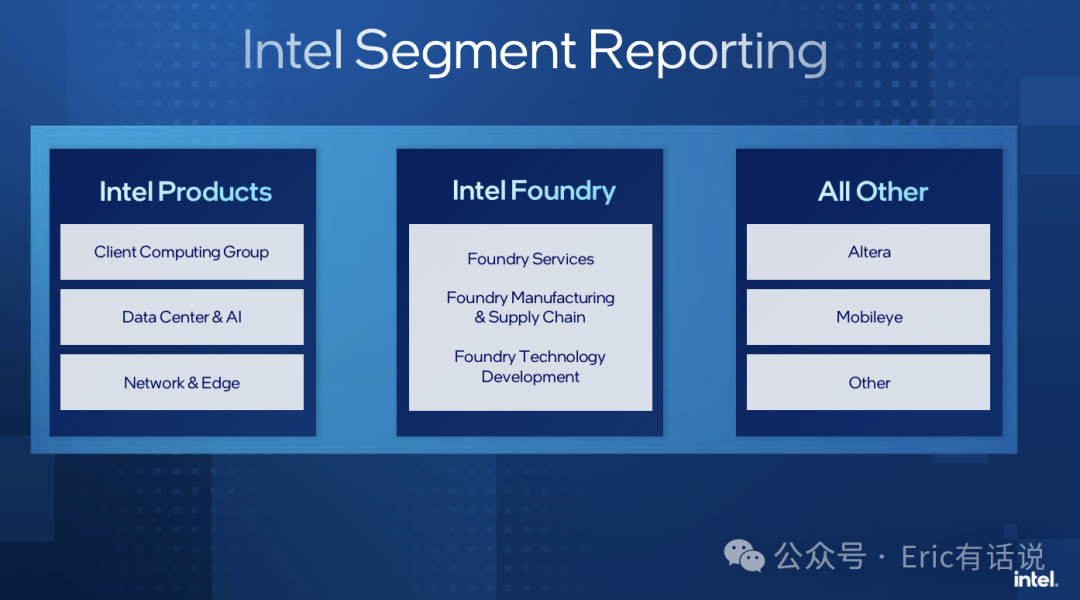

Q4 Business Details:

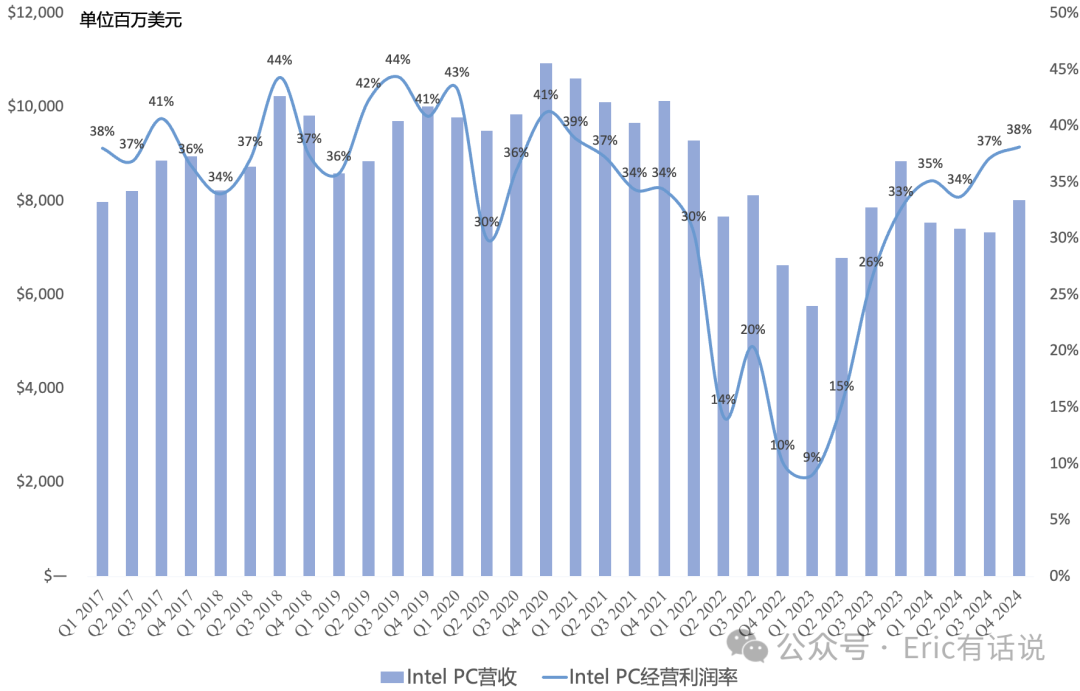

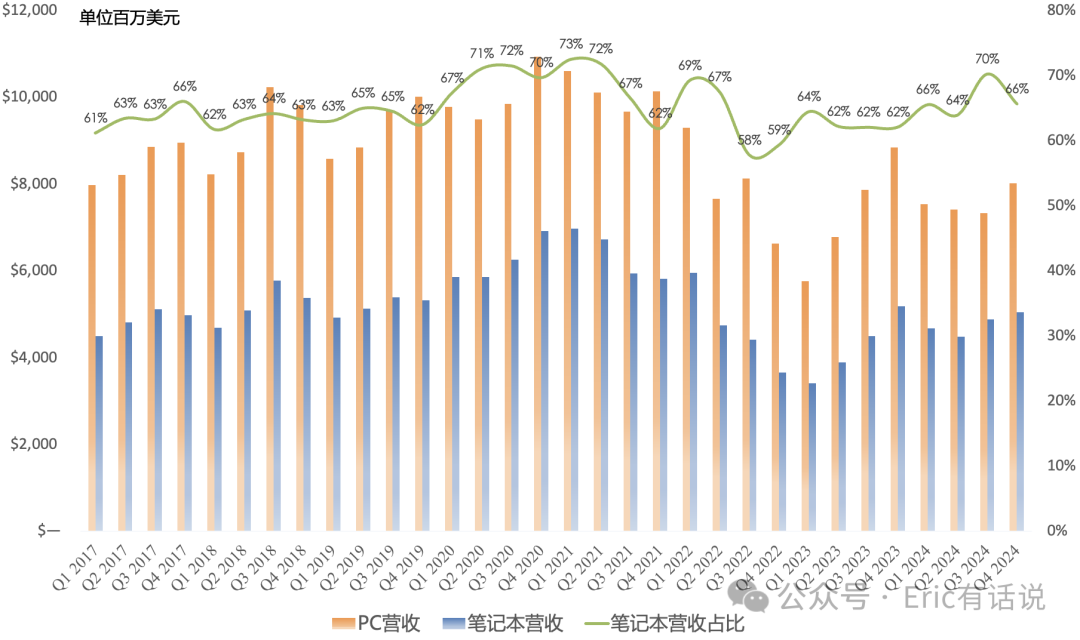

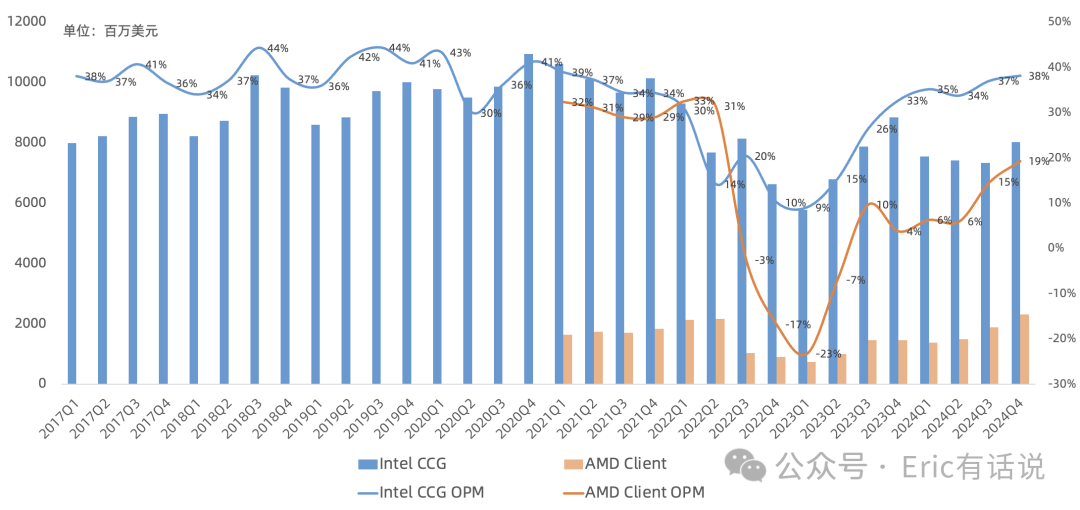

CCG revenue was $8.02B, down 9% year over year, the second consecutive quarter of year-over-year decline, and up 9% sequentially, ending three consecutive quarters of sequential decline, accounting for 56% of revenue. Operating income was $3.06B, up 6% year over year and 12% sequentially, with an operating margin of 38% (AMD 19%), returning to Q2 2021 levels, and remains Intel's most profitable business.

Intel's PC CPU market share is approximately 70%. The target of over 100M AI PC units shipped by end of 2025 is on track. Part of the sequential PC revenue growth this quarter was due to customers pulling in orders to avoid tariffs. Notebook Panther Lake (RibbonFET + PowerVia, 18A client) is expected to enter volume production in 2H 2025, driving margin improvement. Desktop Nova Lake (Intel 18A + TSMC) is slated for 2026 volume production.

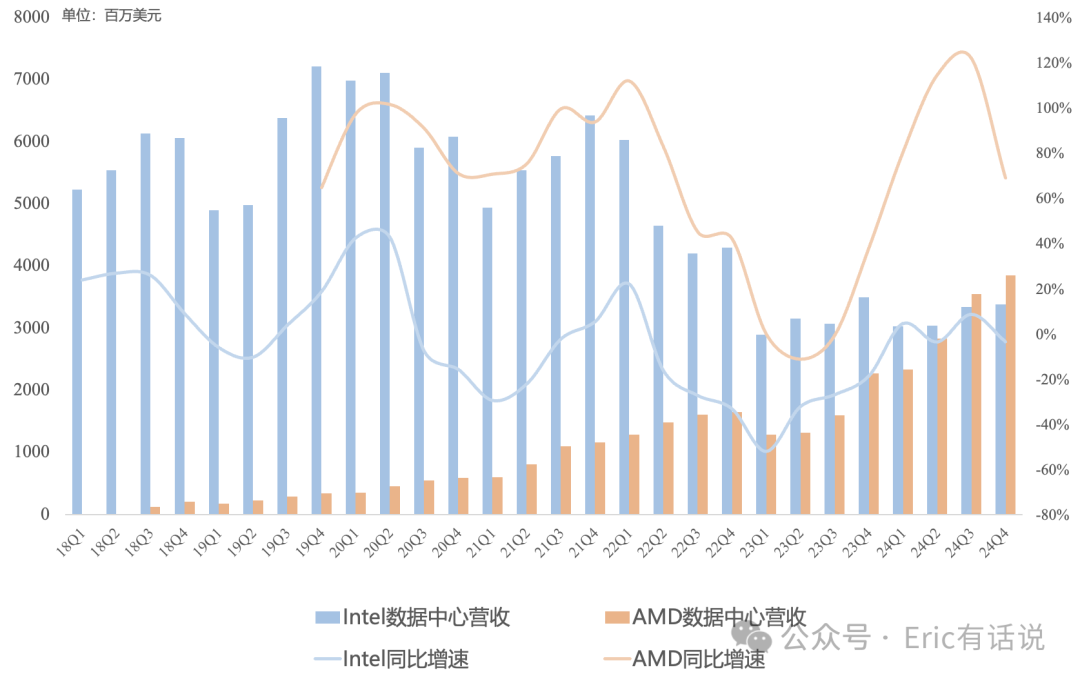

DCAI revenue was $3.387B (since Q1 2024, DCAI reporting excludes Altera; AMD Q4 data center revenue was $3.859B), down 3% year over year and roughly flat sequentially, marking the second consecutive quarter of being overtaken by AMD data center. Operating income was $233M, down 33% sequentially, with an operating margin of 7%.

The 2025 data center CPU target is share stabilization. Data center GPU roadmap adjusted: Falcon Shores will not be sold externally, replaced by rack-scale Jaguar Shores. The one-size-fits-all approach does not work in AI data centers, acknowledging customers prefer full-scale rack solutions. Traditional server demand is stable.

Granite Rapids (Intel 3 P-cores enterprise) has narrowed the gap with AMD. Future Diamond Rapids (GAA 18A P-cores server) will narrow it further. Clearwater Forest (GAA 18A E-cores server) is expected to enter volume production in 1H 2026 (delayed from the original 2H 2025).

NEX revenue was $1.623B, up 10% year over year and 7% sequentially. Operating income was $340M. Edge market customer purchasing intent is recovering. Q1 architecture reorganization: edge business moves from NEX to CCG, network business moves from NEX to DCAI, NEX will focus on communications.

Intel Foundry revenue was $4.502B, down 13% year over year. Operating loss was $2.26B. Q4 Foundry operating loss rate is expected to be consistent with Q3. IFS (external) revenue was approximately $191M, down 34% year over year. Intel Foundry sequential growth was mainly driven by higher EUV wafer mix (20231% to 20245%+) and higher IMS equipment sales. EUV wafer mix will increase further in 2025, significantly lifting gross margin. Currently 30% of Intel products are externally manufactured; this will gradually decrease but external foundry will not stop. Subsequently, the IMS business will move from Intel Foundry to All Other.

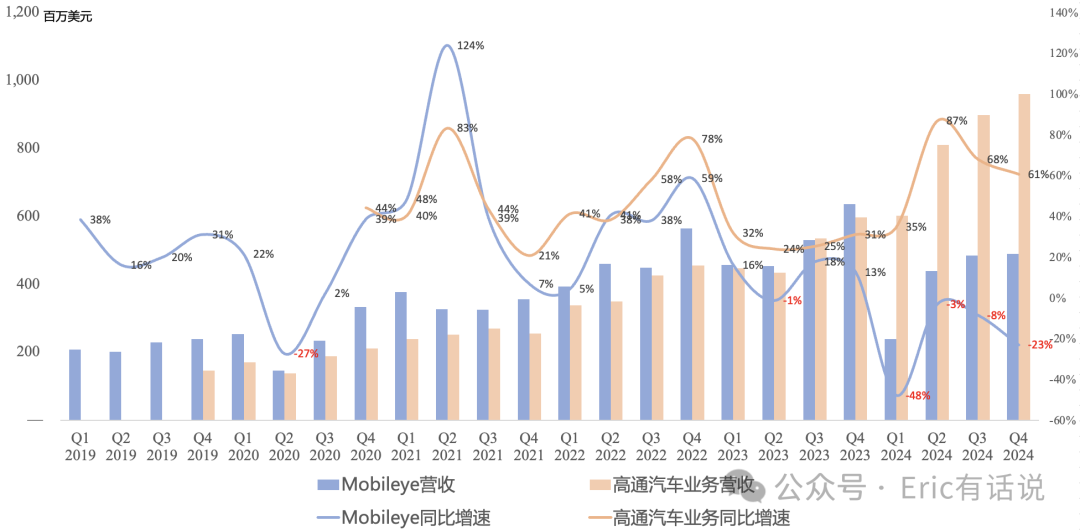

Mobileye revenue was $490M, down 23% year over year, the fourth consecutive quarter of year-over-year decline, and up slightly sequentially. The revenue gap with Qualcomm will widen further. Operating income was $103M, down 58% year over year. Subsequently, the automotive business will move from All Other to CCG.

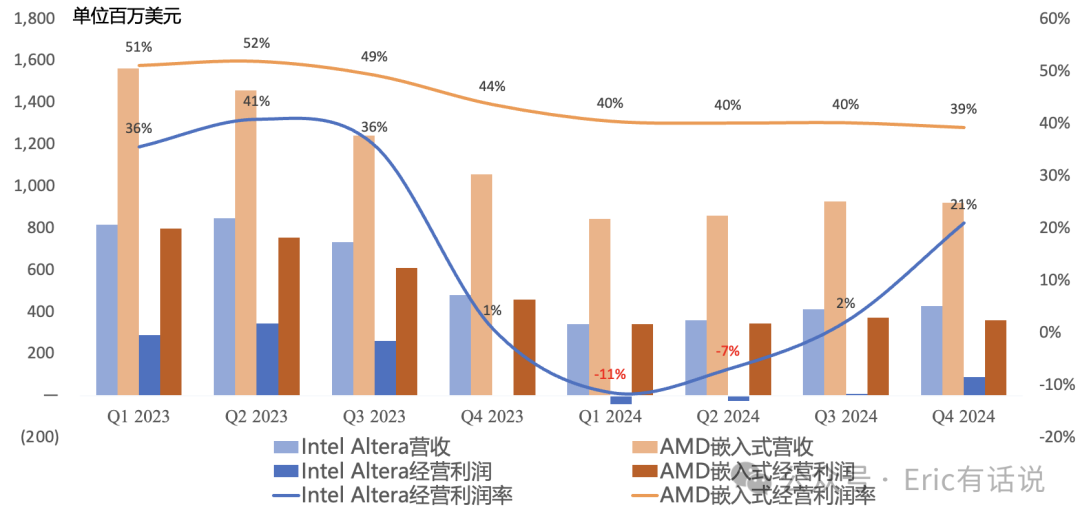

Altera revenue was $429M, down 11% year over year and up slightly sequentially. Operating margin improved to 21%. Altera continues to destock. Q1 Altera revenue is expected to decline sequentially, but by less than the overall company sequential decline (11%-18%). Altera external strategic investment and IPO efforts continue.

Call Highlights:

CHIPS Act: U.S. Department of Commerce awarded a $7.86B grant. $1.1B received in Q4, and another $1.1B received in January.

Due to intensifying competition, tariffs, and high PC inventory, Q1 revenue midpoint is guided to $12.2B, down 4% year over year and 14% sequentially. CCG, DCAI, and NEX sequential declines are similar. Intel Foundry is expected to be flat to slightly down sequentially.

Q1 non-GAAP gross margin is guided to 36%, down 9.1 percentage points year over year. Gross margin is expected to improve quarter by quarter thereafter (roughly 40%-60%). Intel product gross margin will be below 2024's 51%. Intel Foundry gross margin will continue to recover. 2025 opex is expected to be $17.5B, and will continue to decline in 2026. By 2026, as Panther Lake ramps and Intel Foundry margins recover, gross margin is expected to return to 60%.

The key to strong Intel products is a strong Intel Foundry. Intel Foundry's target is to achieve operating profitability by the end of 2027. Advanced packaging and partnerships with Tower Semi and UMC.

2025 gross capex is guided to $20B (reduced), net capex $8B-$11B (reduced). The top priority for 2025 remains reducing capex, improving operating cash flow, and unlocking non-core asset value. The 2025 adjusted free cash flow breakeven guide has been withdrawn.

Previously noted at the end of the last earnings report:

This time Pat took a big bath, writing off everything possible, while continuing to paint a rosy picture for the market: a triumphant return in 2026, attempting to rescue the below-book stock price. Intel's future is now entirely bet on 18A, a high-stakes gamble. All of Pat's big pie is premised on 18A.

Recent speculation on Intel's future is all over the place: Musk involvement in an acquisition, a merger with GlobalFoundries, and earlier Qualcomm acquisition talks that apparently fell through. This earnings call showed the interim management's attitude as relatively sincere, acknowledging roadmap and strategic errors without painting more big pies. As for the 18A that will decide Intel's fate, we'll have to wait until the second half of the year.