Intel's new CEO Lip-Bu Tan has overturned several major prior strategies, making significant adjustments to the controversial Intel Foundry business and planning a thorough restructuring of Intel; whether this massive ship can set sail again remains to be seen.

Intel Q2 Earnings:

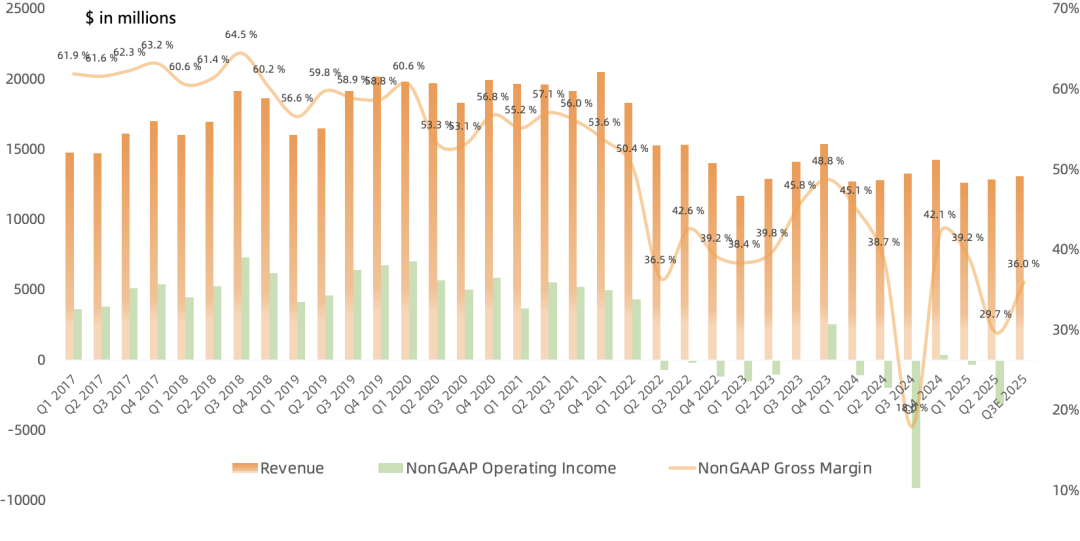

Revenue of $12.86B, up 0.2% year over year, ending 4 consecutive quarters of year-over-year declines, and up 1.5% sequentially, slightly above the prior guidance range of $11.2-12.4B; guiding Q3 revenue midpoint of $13.1B, down 1% year over year and up 2% sequentially.

GAAP gross margin of 27.5%, down 7.9 percentage points year over year and 9.4 percentage points sequentially; Non-GAAP gross margin of 29.7%, down 9 percentage points year over year and 9.5 percentage points sequentially, well below the prior guidance of 36.5%, primarily due to incremental costs related to expense reduction plans, including approximately $800M in non-cash impairment and accelerated depreciation, plus approximately $200M in one-time period costs; excluding these impacts, Non-GAAP gross margin would be 37.5%, slightly above prior guidance; guiding Q3 Non-GAAP gross margin of 36%, down sequentially.

GAAP operating loss of $3.18B, impacted by $1.89B in one-time restructuring charges; Non-GAAP operating loss of $500M, swinging from profit to loss both year over year and sequentially; guiding Q3 Non-GAAP operating breakeven.

GAAP net loss of $3.02B, the 6th consecutive quarterly loss; guiding Q3 net loss of $1.05B, with the loss narrowing.

Non-GAAP net loss of $440M, swinging from profit to loss both year over year and sequentially; prior guidance was breakeven, ending 2 consecutive quarters of profitability; still guiding Q3 Non-GAAP breakeven.

Q2 operating cash flow of $2.1B, total capex of $4.5B, net capex of $3.1B, resulting in adjusted free cash flow of -$1.1B, the 4th consecutive quarter of negative adjusted FCF.

As of quarter-end, company net assets stood at $97.88B.

Q2 Business Details:

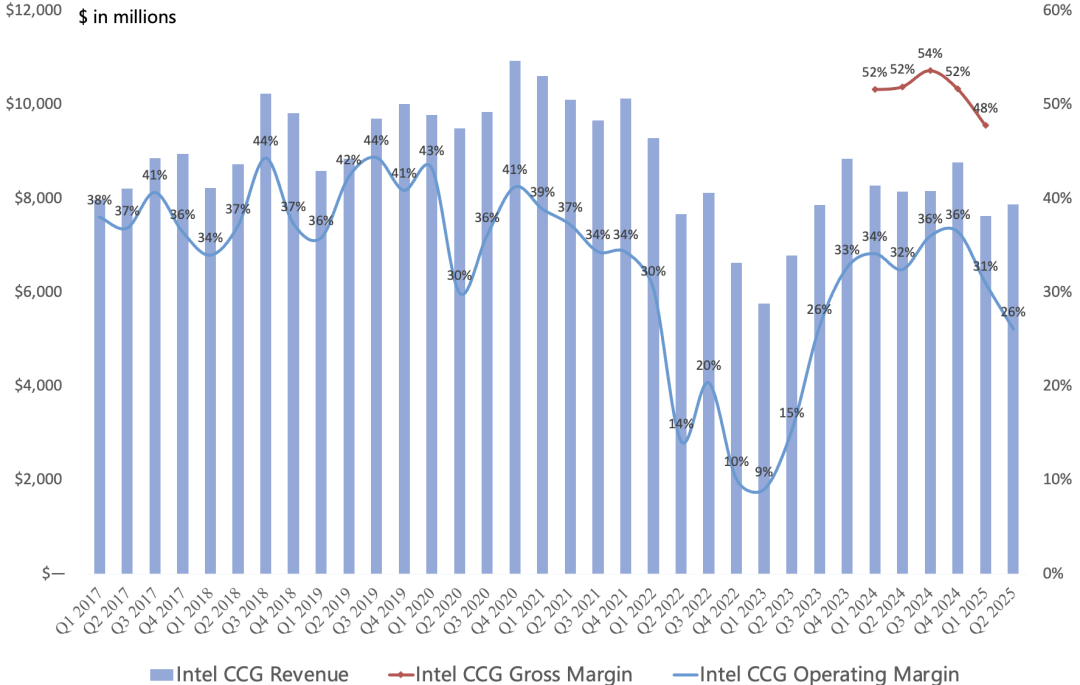

Starting in 25Q1, Intel NEX Edge moved to CCG, NEX Network moved to DCAI, IMS moved from Intel Foundry to All Other, and Automotive moved from All Other to CCG. The result is that CCG and DCAI numbers look better.

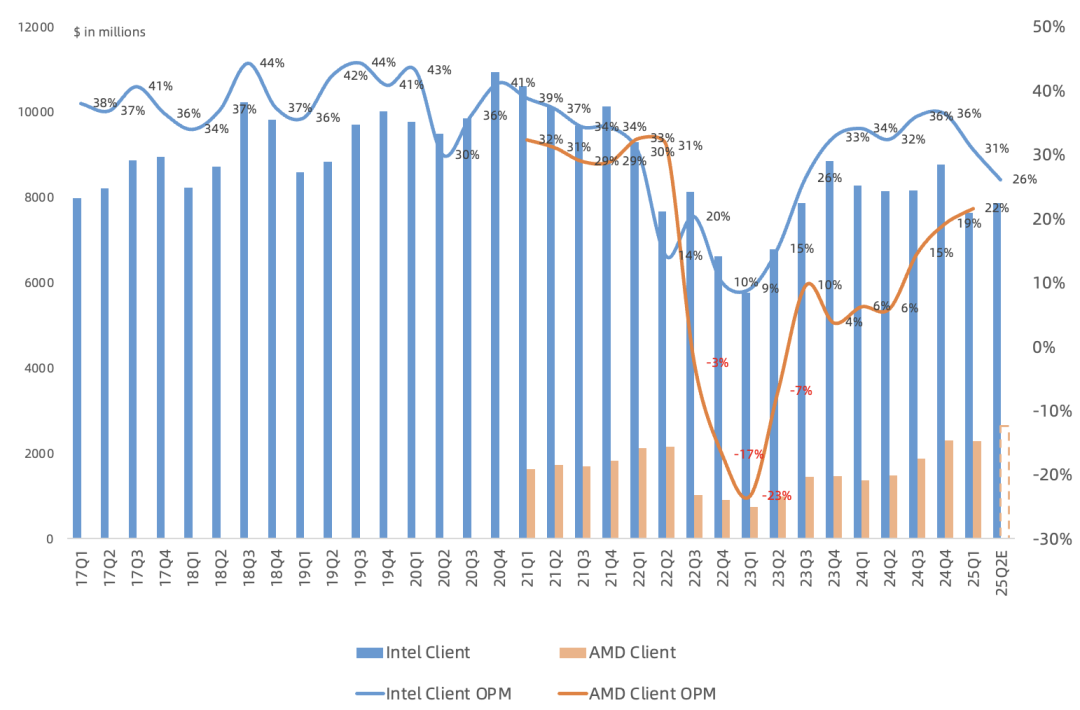

CCG revenue of $7.87B, down 3% year over year, the 3rd consecutive quarterly decline, up 3% sequentially, representing 61% of revenue; operating income of $2.05B, down 22% year over year, operating margin of 26% (vs. AMD 25Q1 22%), remaining Intel's most profitable business.

PC revenue of $6.6B, down 6% year over year due to intensifying competition; shipments down year over year, ASP roughly flat; as in the prior quarter, desktop Raptor Lake shipments outperformed notebook Lunar Lake, lifting margins; N-1 and N-2 generation CPU demand remains strong (recently RTX 50-series value-tier notebooks frequently feature 13th/14th gen CPUs, which, combined with government subsidies, are more attractive to consumers).

For Q3, Lunar Lake is expected to ramp very significantly, pressuring margins, while Raptor Lake shipments exceed expectations, leaving Intel 7 capacity constrained in the second half; continuing to advance notebook Panther Lake (RibbonFET + PowerVia, 18A client) toward year-end volume production, aiming to win back consumer and commercial notebook share; acknowledging a significant gap versus AMD in the high-end desktop market that needs to be closed; betting on Nova Lake (Intel 18A + TSMC) for volume production by end of 2026.

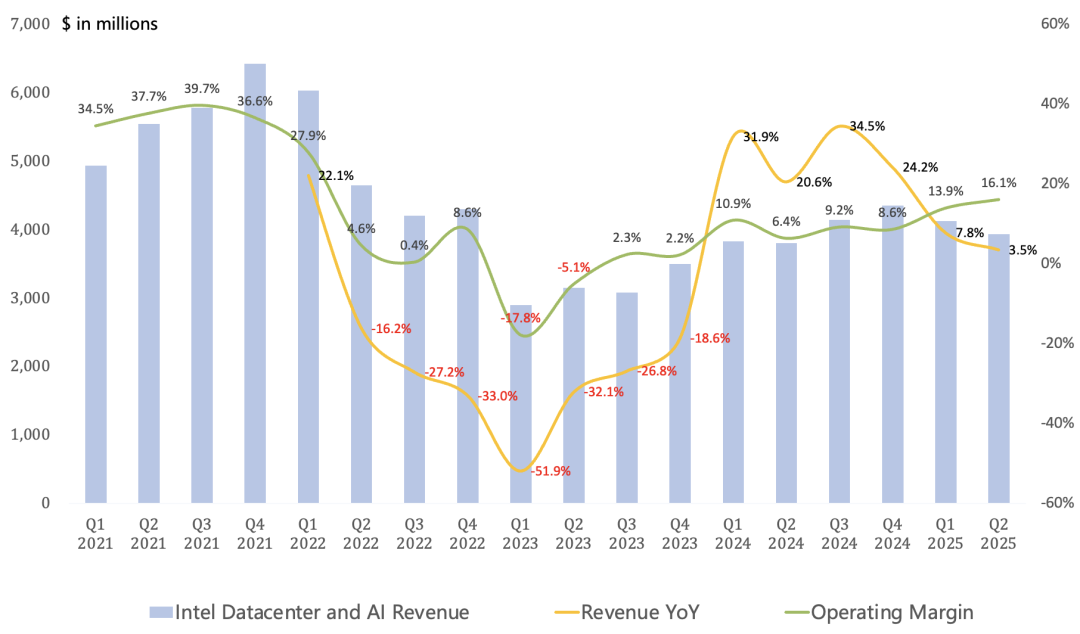

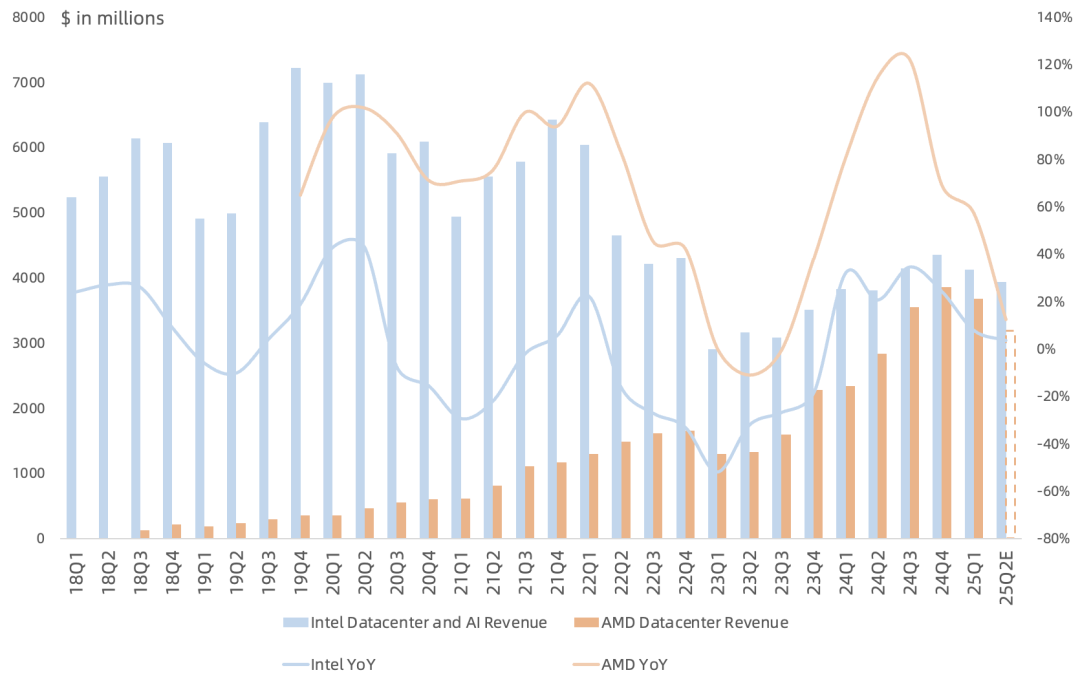

DCAI revenue of $3.94B (under revised reporting, surpassing AMD's data center revenue), up 4% year over year, down 5% sequentially, representing 31% of revenue; operating income of $630M, up 162% year over year and 10% sequentially, operating margin of 16%, improving for the 4th consecutive quarter.

Driven by strong hyperscaler demand and selection as the host CPU for NVIDIA DGX B300, Intel's Q2 server CPU revenue grew year over year; shipments up 13% year over year, but ASP down 8% year over year due to price competition with AMD; management acknowledges high-end product performance still lags AMD significantly and is playing catch-up; in the future, an ASIC approach for AI compute cards is not ruled out.

Intel Foundry revenue of $4.42B, up 3% year over year, down 5% sequentially, operating loss of $3.17B, with losses widening both year over year and sequentially, operating loss rate of 71.7%; Intel 7 wafer output better than expected and advanced packaging services grew, but an $800M impairment this quarter worsened the loss; second-half Intel 7 capacity constraints will lower external advanced packaging revenue expectations.

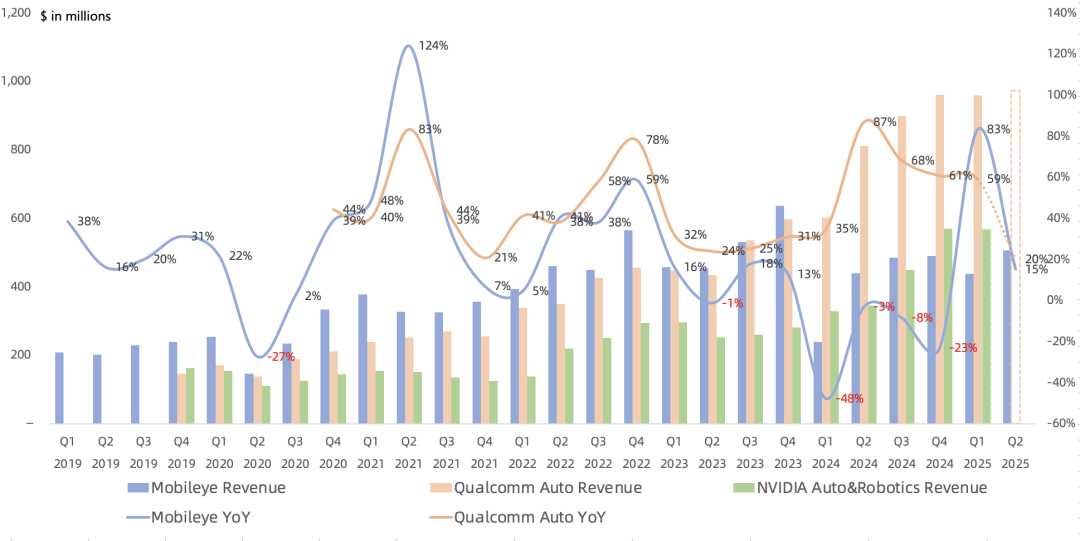

Mobileye revenue of $510M, up 15% year over year, the 2nd consecutive quarter of year-over-year growth, up 16% sequentially; revenue gap versus Qualcomm has widened further, and NVIDIA has now overtaken it; operating income of $110M, up 47% year over year; average system price of $49.7, down 9% year over year; full-year revenue guidance midpoint raised from $1.75B to $1.83B, up 10% year over year; operating income guidance midpoint raised from $218M to $248M, up 34% year over year; after selling 7% of Mobileye shares for $922M on July 11, Intel sold additional shares to Mobileye.

Altera revenue of $450M, up 24% year over year and 22% sequentially; FPGA demand beginning to recover; Silver Lake previously announced it would acquire 51% of Altera at an $8.75B enterprise valuation (Intel acquired Altera for $16.7B in 2015; AMD acquired Xilinx for $35B in 2020); Intel retains the remaining 49%, with the transaction expected to close in Q3 this year; per the adjusted agreement, approximately $4.4B in net cash proceeds are expected, of which $1B is deferred and will be paid in two equal $500M installments no later than December 31, 2026 and December 31, 2027.

Call Highlights:

As of Q2, Intel headcount stood at 96,400; target is 75,000 by year-end; management headcount to be cut by ~50%, implying roughly 22% more reductions in the second half.

Due to macro uncertainties including tariffs, management guides Q3 revenue of $12.6-13.6B, down 5% to up 2% year over year, down 2% to up 6% sequentially, driven primarily by the legacy PC business; historically Q3 revenue grows high single digits sequentially versus Q2; given potential tariff-driven pull-forward in the first half, the company's second-half outlook is conservative; guiding Q3 CCG revenue up sequentially, Intel Foundry revenue down sequentially.

Guiding Q3 Non-GAAP gross margin of 36%; guiding 2025 opex of $17B, 2026 opex of $16B (unchanged); major cash costs related to restructuring expected in Q3; guiding 2026 non-GAAP gross margin range of 40%-60%.

Guiding 2025 gross capex of $18B (unchanged), net capex of $8-11B (unchanged); only 50% of the current $18B capex is maintenance spending; guiding 2026 gross capex significantly above $9B but below $18B, impacting semiconductor equipment vendors such as ASML.

Management believes the past several years of capacity investment far exceeding demand was unwise and excessive; future capacity additions will be based entirely on customer capacity commitments, with absolutely no preemptive capex; management decided to halt manufacturing plant projects in Germany and Poland, plans to consolidate Costa Rica assembly/test operations into existing Vietnam and Malaysia factories, and will further slow the Ohio factory build-out.

Intel 18A Panther Lake products are slated for Arizona production; Intel 18A continues to make steady progress on yield and performance targets; Intel 18A and 18AP remain the key nodes for the company's next three product generations; management believes internal products alone can deliver a reasonable return on the Intel 18A investment, not ruling out the possibility of zero external customers; Intel 14A will be a foundry node from the start (2028/2029), but investment will only occur once orders are in hand (meaning no customers, no build).

Previously noted at the end of the last earnings report:

Overall, the new CEO has directly shattered Pat's IDM 2.0 foundry dream; the results will take time to validate, and near-term earnings impact may be limited; the near-term focus remains on Intel 18A progress. Intel's valuation has long hovered around 1x P/B, somewhat reminiscent of Samsung Electronics.