Haven't written about Intel in a while; the last piece was the 2021 Q3 earnings 'Earnings Review | Intel Data Center Flash in the Pan, Notebook Business Weak, May Imply AMD Beat.' Intel's performance over these two years has been unspeakable; endured Pat's endless pie-in-the-sky promises, got used to Pat being repeatedly slapped in the face. But this Q3 did beat expectations somewhat, mainly due to PC beating expectations.

Intel Q3 Earnings:

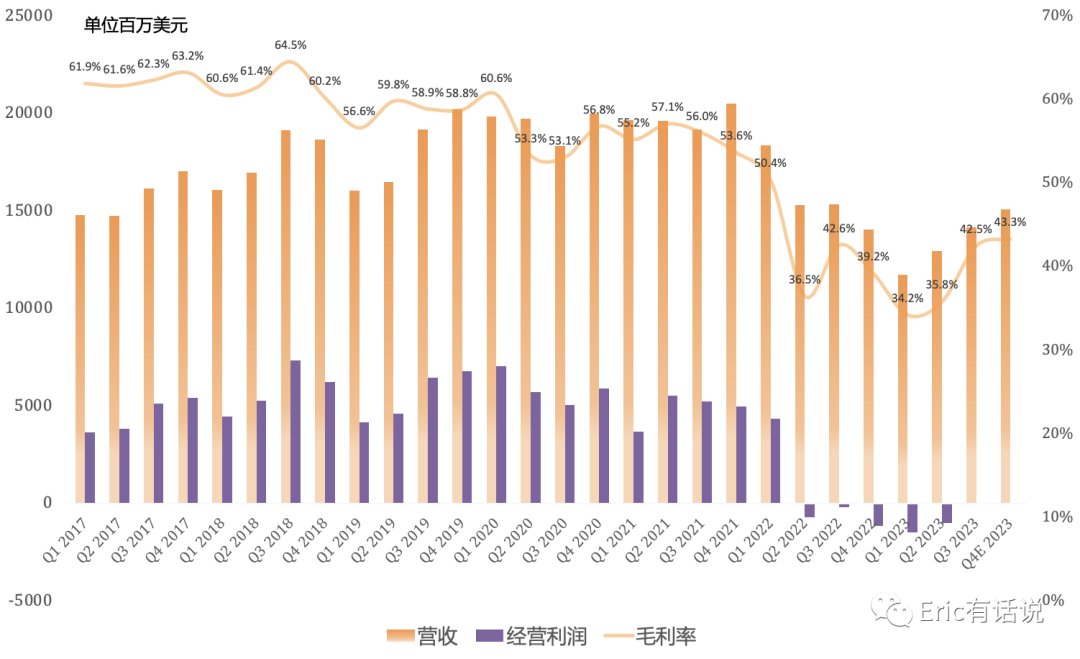

Revenue $14.158B, down 8% year over year, up 9% sequentially, seventh consecutive quarter of year-over-year decline.

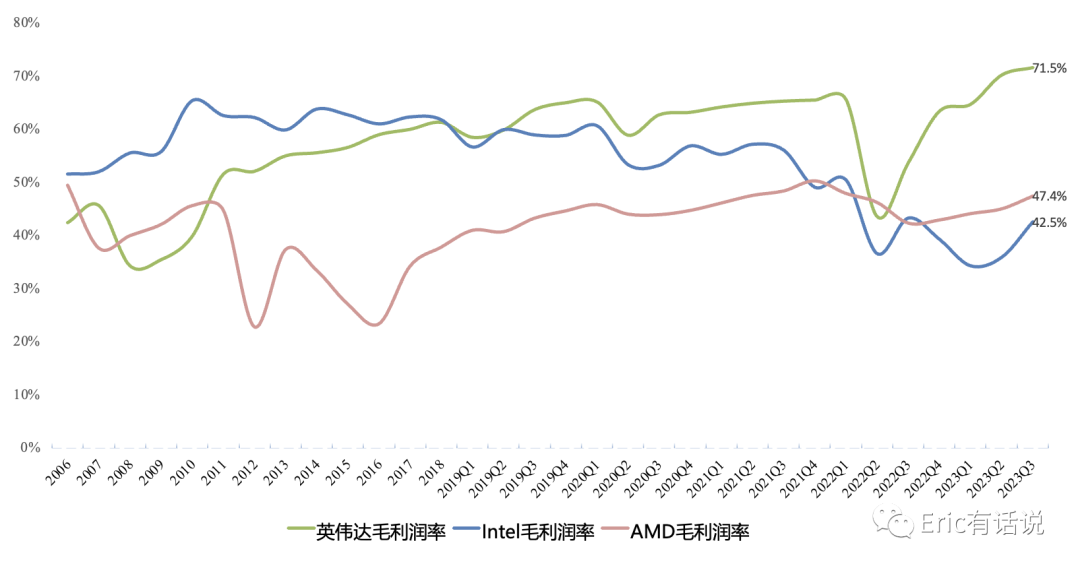

GAAP gross margin 42.5%, down 0.1 percentage points year over year, up 6.7 percentage points sequentially; previously gross margin had been below 40% for three consecutive quarters.

GAAP operating loss $8M, sixth consecutive quarter of operating loss, but loss has narrowed significantly; next quarter likely to break even.

GAAP net income $310M, down 70% year over year, down 79% sequentially; Non-GAAP net income $1.739B, down 29% year over year, up 218% sequentially.

Free cash flow $943M; first three quarters cumulative free cash flow -$10.5B.

Q3 Segment Details:

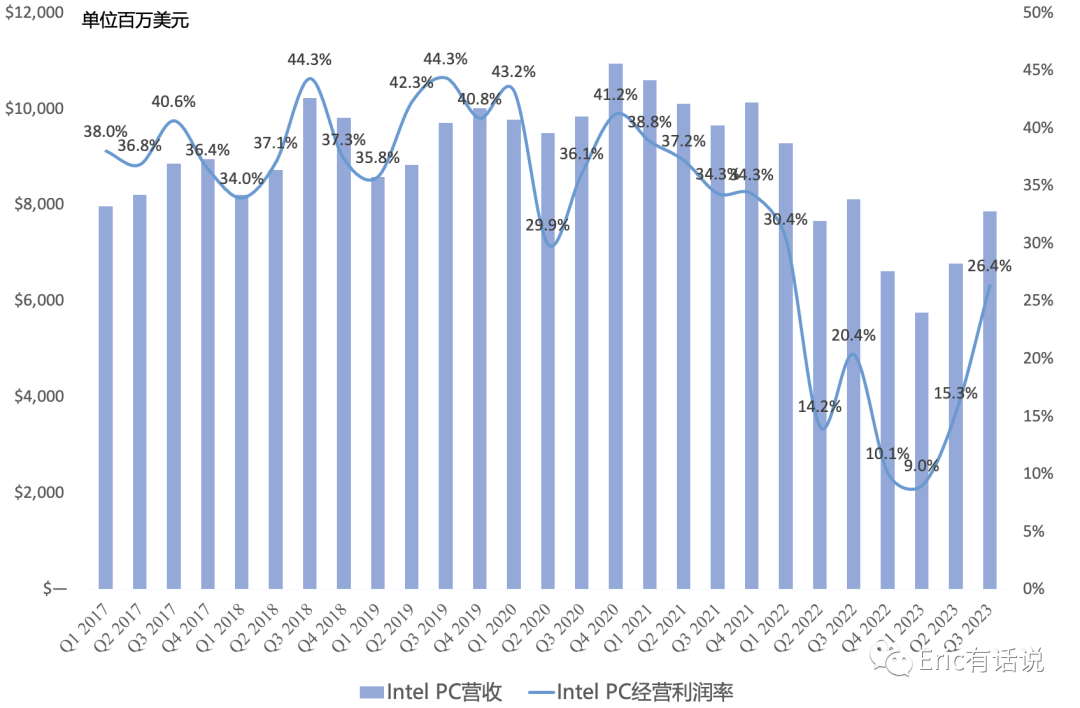

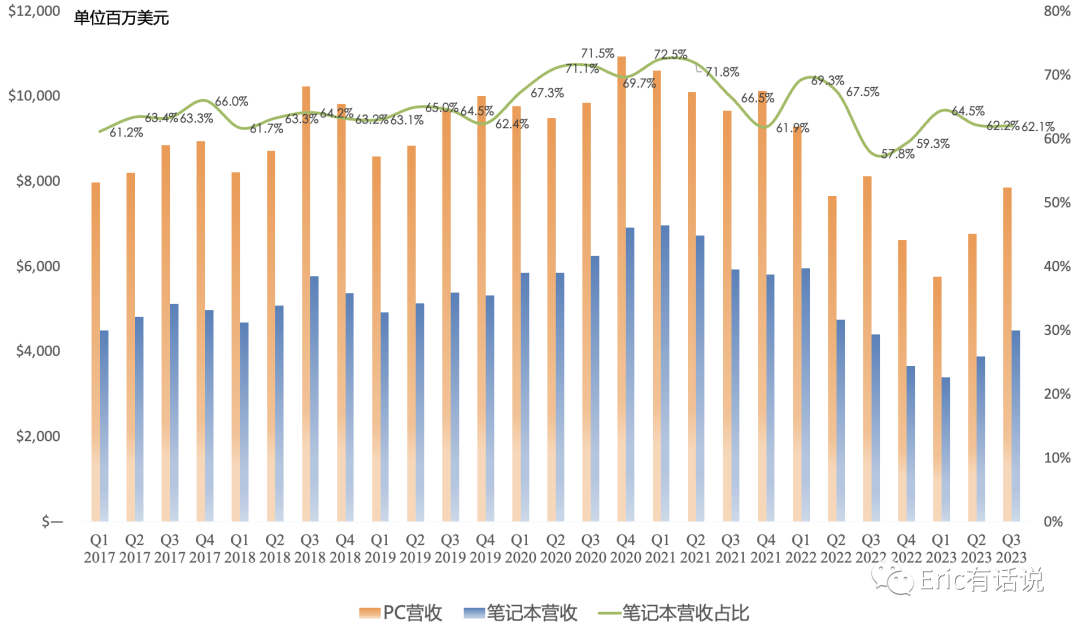

CCG revenue $7.867B, down 3% year over year, ninth consecutive quarter of year-over-year decline, but up 16% sequentially, second consecutive quarter of 16%+ sequential growth; revenue share 56%, highest since 2017 Q2; operating income $2.073B, up 25% year over year, doubled sequentially.

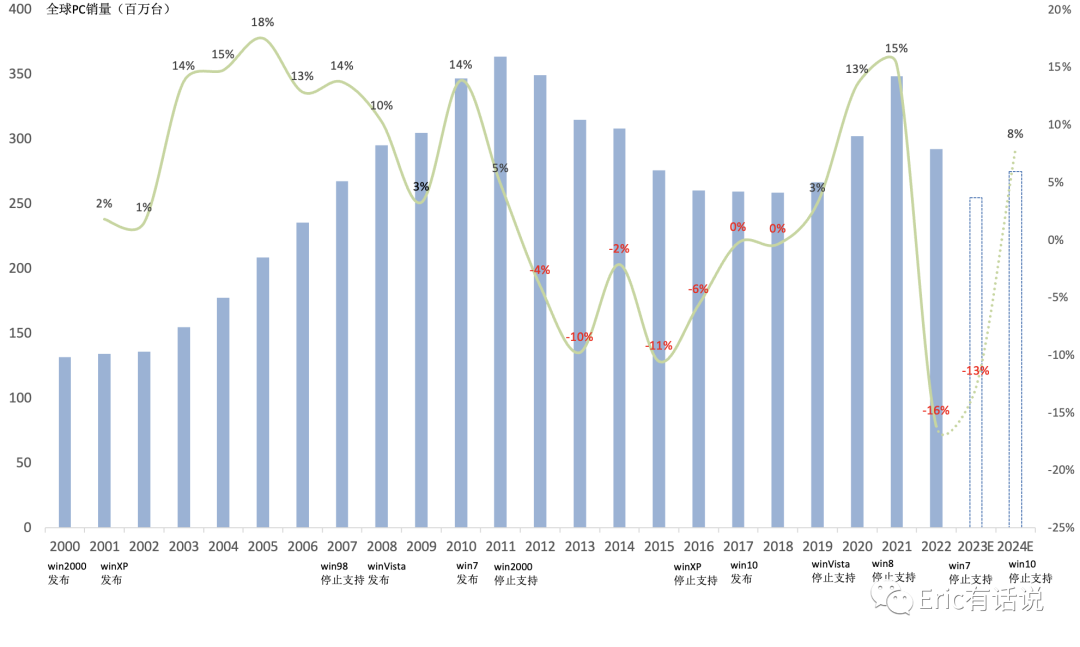

PC commercial and gaming markets grew strongly; PC inventory digestion completed in H1 this year, Q3 began sequential recovery; benefiting from Windows 10 end-of-life and Windows 12 launch; future PC TAM expected to stabilize around 300M units.

Intel 4 process Meteor Lake began low-volume shipments; Intel 7 process cumulative shipments 150M chips.

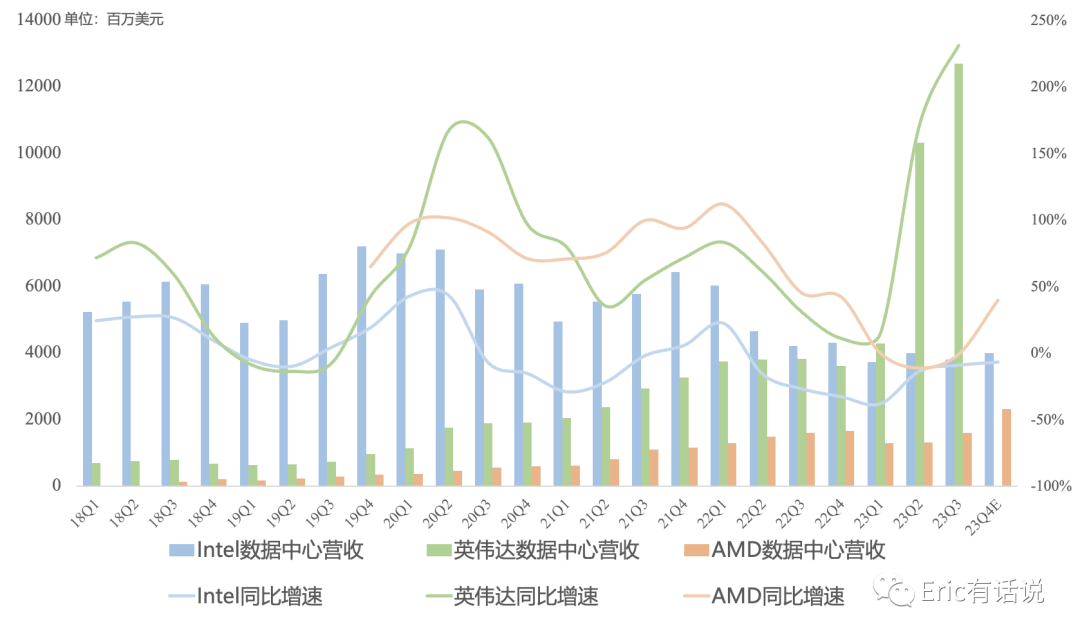

DCAI revenue $3.814B, down 9% year over year, sixth consecutive quarter of year-over-year decline, down 5% sequentially; operating income $71M, ending two consecutive quarters of losses.

Xeon revenue up slightly sequentially; Xeon ASP hit period record, but market share still declining; Q4 server market expected to begin sequential recovery; Xeon Q4 revenue expected to grow slightly sequentially.

Sapphire Rapids shipments to exceed 2M next month; Emerald Rapids began shipping in October, official launch Dec 14; Sierra Forest, Granite Rapids 24H1 on track; management believes Sierra Forest and Granite Rapids can help Intel regain server market share.

PSG (FPGA) within DCAI: revenue down mid-teens sequentially; FPGA industry inventory elevated; Q4 and next year expected to continue declining.

Gaudi portfolio pipeline nearly doubled this quarter; Gaudi 3 launching next year; integrated Falcon Shores in 2025; Gaudi currently impacted by China export controls.

NEX revenue $1.45B, down 36% year over year, sixth consecutive quarter of year-over-year decline, up 6% sequentially; operating income $17M, ending two consecutive quarters of losses; edge market began recovery in Q3; networking and telecom markets remain weak, will continue to be weak.

IFS revenue $311M, up 82% year over year, up 34% sequentially; operating loss $86M, seventh consecutive quarter of losses.

IFS revenue nearly doubled sequentially, driven primarily by packaging revenue growth and the sale of the IMS Nanofab business; TSMC invested $433M for a 10% stake in the IMS Nanofab sold by Intel; Intel 18A/3 secured one major customer order; this quarter 18A added 2 customers and advanced packaging added 2 customers, with 6 customers in discussions; wafer customer order value is in the billions of dollars, to be realized over 2-3 years; advanced packaging customer order value is in the hundreds of millions, to be realized over 2-3 quarters; IFS business scale will see significant growth next year.

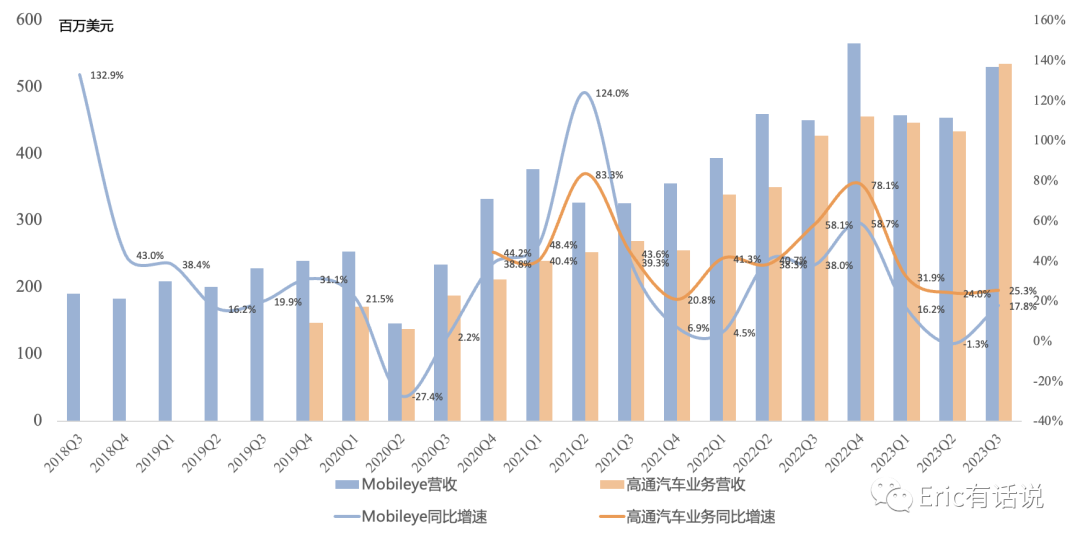

Mobileye revenue was $530M, up 18% year over year and 17% sequentially; operating income was $170M, up 20% year over year and 32% sequentially; revenue scale was surpassed by Qualcomm for the first time.

Call Highlights:

Since Pat became CEO, Intel has exited 10 businesses (this quarter added the sale of the silicon photonics product line), saving $1.8B annually; the PSG business plans to bring in strategic investors in 2024, will report results separately starting next Q1, and targets an IPO in 2025/2026.

Q4 revenue is guided to a midpoint of $15.1B, up 8% year over year, ending a streak of 7 consecutive quarters of year-over-year declines, and up 7% sequentially, with growth still primarily driven by PC; operating income turns positive, net income of $1B, swinging to a profit year over year.

Intel 20A Arrow Lake manufacture ready in H1 2024; Intel 18A also made major progress, with Clearwater Forest (Server) and Panther Lake (Client) manufacture ready in H2 2024, launching in 2025.

Long-term gross margin target is a return to the 60% level, with an operating margin target of 40%.

The first High-NA EUV lithography tool will be installed by year-end; Intel 7 process has 3 fabs in production, one of which is in Israel.

Overall, this Intel earnings report was primarily driven by a strong PC recovery, contributing substantial revenue and profit growth. At a critical juncture, the traditional core business delivered first. Notably, the current PC recovery appears more a result of inventory normalization than a demand surge; the Windows 10 end-of-life and Windows 12 launch next year may be what drives significant demand growth.

As for the process roadmap and the IFS big picture, they remain to be observed. The good news is Intel has successfully passed the earnings trough; the bad news is that data center and the traditional core PC business will face more competition.