At the tail end of July, AMD released its 2019 second-quarter earnings.

Media headline: "AMD drops as much as 7% after hours, Q2 net income down 70% year over year, Q3 revenue outlook below expectations."

I think it's not that bad.

Earnings Summary:

Q2 revenue $1.53B, down 13% year over year, up 20% sequentially.

Q2 GAAP net income $35M, down 70% year over year, up 119% sequentially.

Q2 Non-GAAP net income $92M, down 41% year over year, up 48% sequentially.

Q2 gross margin 41%, up 4 percentage points year over year, roughly flat sequentially.

Earnings Interpretation

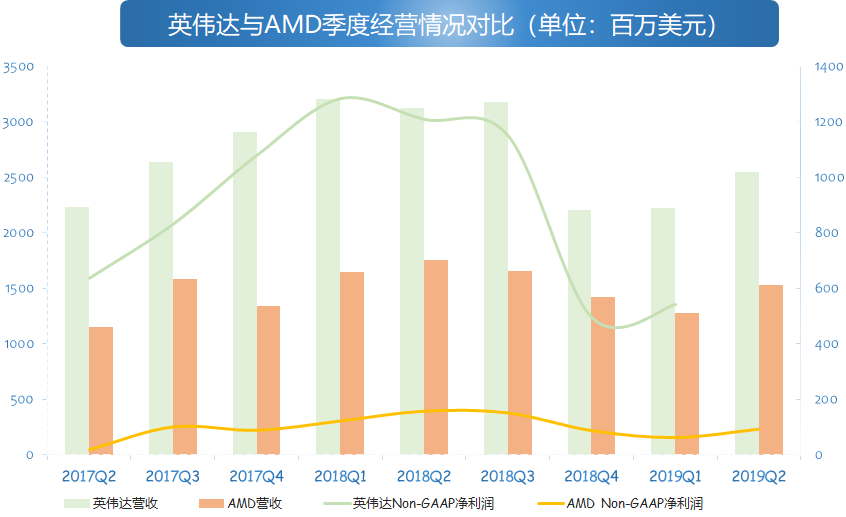

Data source: Company filings; NVIDIA 2019 Q2 revenue is guidance

Looking at quarterly data alone reveals a severe divergence between year-over-year and sequential trends. This is mainly because last year's crypto-mining boom created a high base; the comparison is even clearer against peer NVIDIA, whose overall quarterly revenue trend is quite similar to AMD's. AMD's revenue scale is gradually narrowing the gap with NVIDIA. However, NVIDIA's profitability remains substantially stronger.

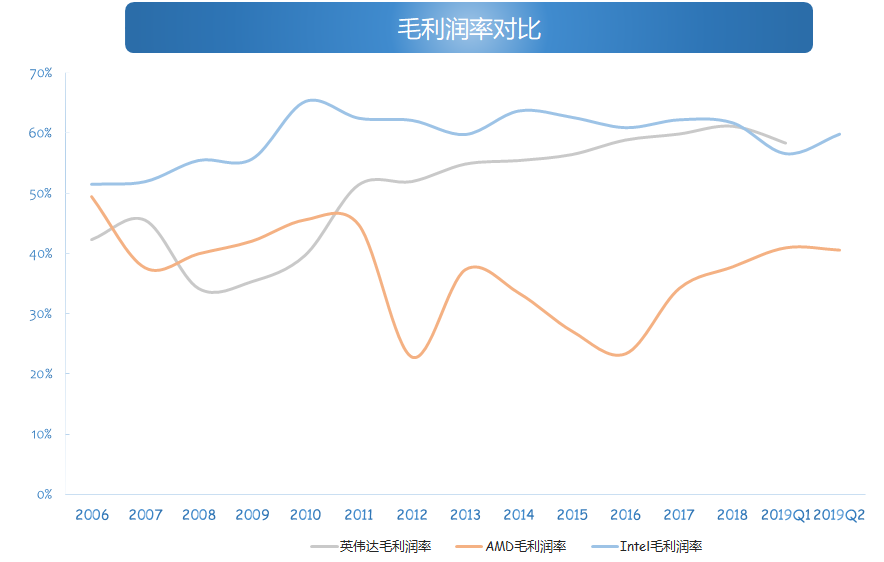

Data source: Company filing

On gross margin, AMD has firmly held above 40%; the company believes full-year Non-GAAP gross margin can reach 42%. Rivals NVIDIA and Intel both saw sharp gross margin declines in Q1.

We believe that as AMD's product-line transition nears completion, gross margin will rise further. First, the lower-margin semi-custom business, pressured by the PS4 and Xbox One X/S product cycles, will continue to shrink before the next-generation console launches at the end of 2020. The rising share of non-semi-custom revenue will lift AMD's overall gross margin.

Second, per the earnings call, 7nm products carry gross margins above 50%. As 12nm and 14nm products reach end of life, AMD's overall gross margin should continue to climb.

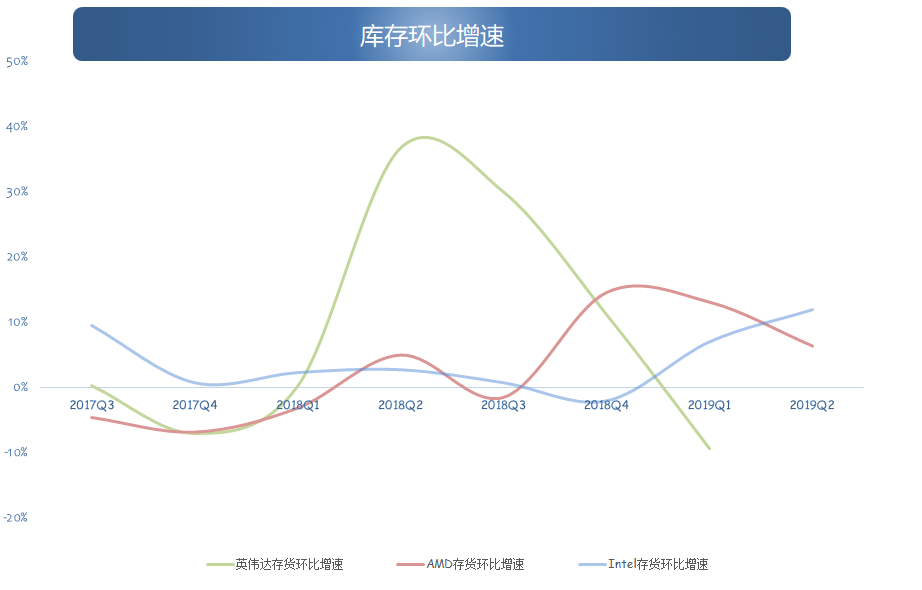

On inventory, sequential changes are no longer very meaningful. With the crypto hangover theoretically mostly digested, inventory now mainly reflects new product preparation. And per overseas reviews, ASIC miners' comprehensive returns far exceed GPUs, so the GPU mining crowd has largely disappeared; recent coin-price volatility is irrelevant. (Though management still mentions Bitcoin...)

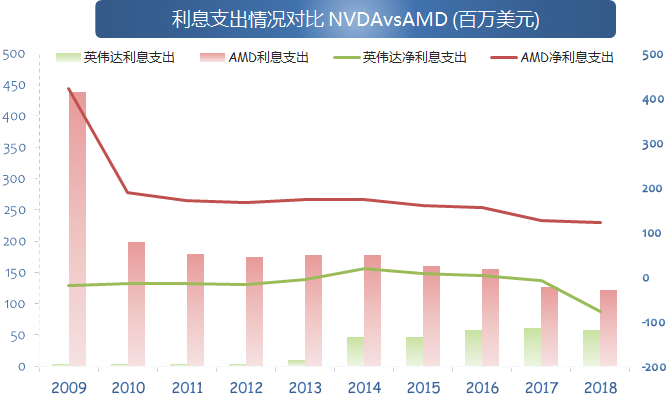

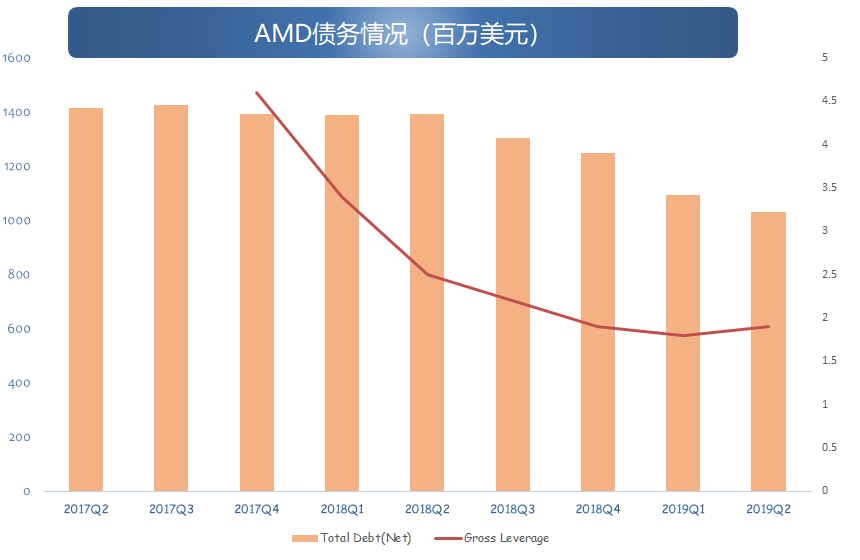

We previously discussed AMD's profitability: massive interest-bearing debt, generating net interest expense several times that of NVIDIA, is the heaviest burden on AMD's shoulders. But the debt situation is improving.

In the Q1 report, the company guided Q2 revenue of $1.52B and Non-GAAP gross margin of 41%; by that measure Q2 results met expectations.

Data source: Company Filing

Radeon VII Struggles Alone As Expected; Mobile CPU Shipments Hit 5-Year High

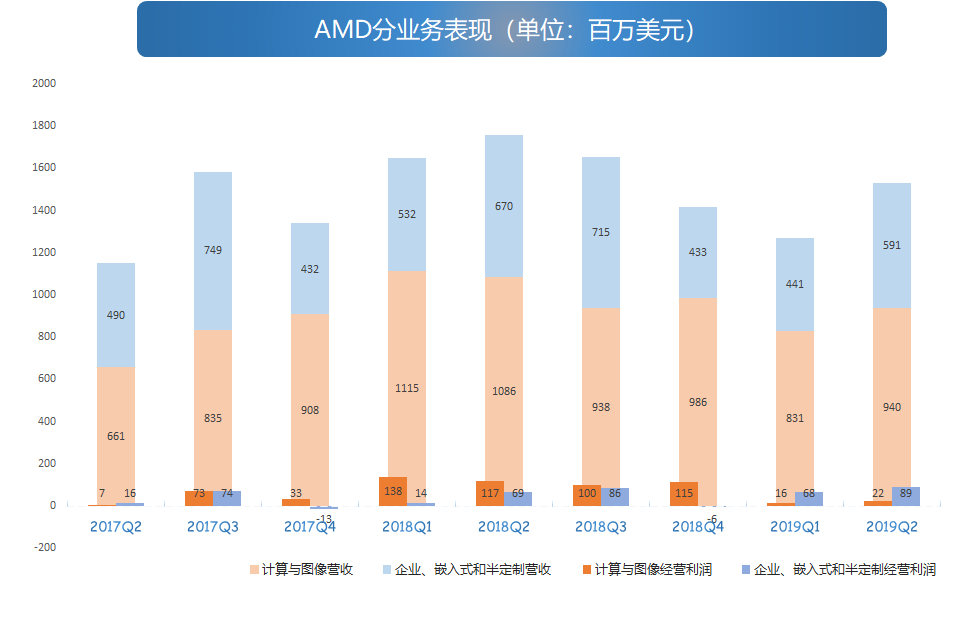

By segment, Computing & Graphics Q2 revenue was $940M, down 13% year over year, up 13% sequentially; operating income $22M, down 81.2% year over year, up 38% sequentially.

Enterprise, Embedded & Semi-Custom revenue was $591M, down 12% year over year, up 34% sequentially; operating income $89M, up 29% year over year, up 31% sequentially.

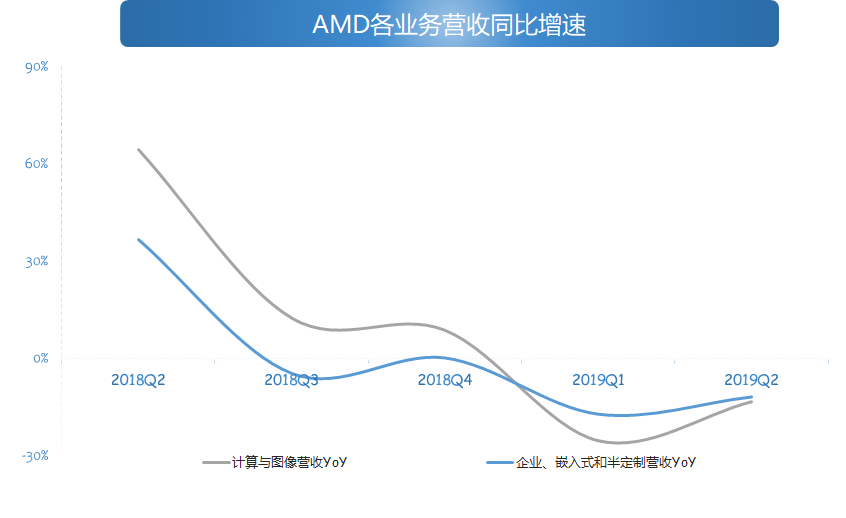

Per the earnings call, within Computing & Graphics, CPU and data center GPU remained bright spots; consumer GPU was the weak link.

We attribute this mainly to the product lineup. Last quarter's consumer GPU new product was primarily the Radeon VII. Positioned as a high-end halo product — the world's first 7nm GPU — it performed poorly post-launch, with media reporting it has been discontinued. The 7nm Navi GPU new products ship in volume in July, so their true impact won't show until Q3.

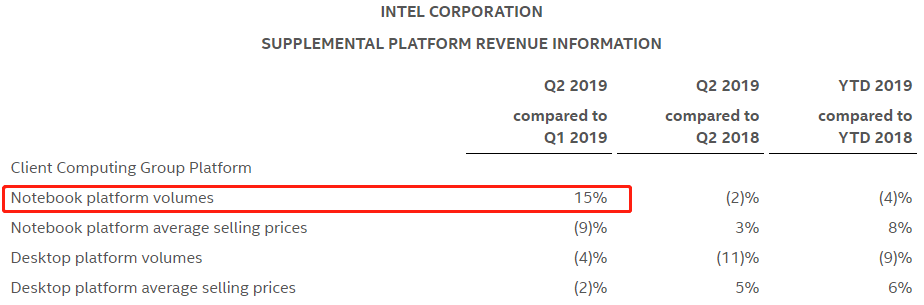

The CPU side deserves a mention on mobile CPUs (notebooks). The company said mobile CPU revenue achieved double-digit growth both year over year and sequentially, with shipments hitting a five-year high. We believe AMD capitalized on the window opened by Intel's CPU shortage.

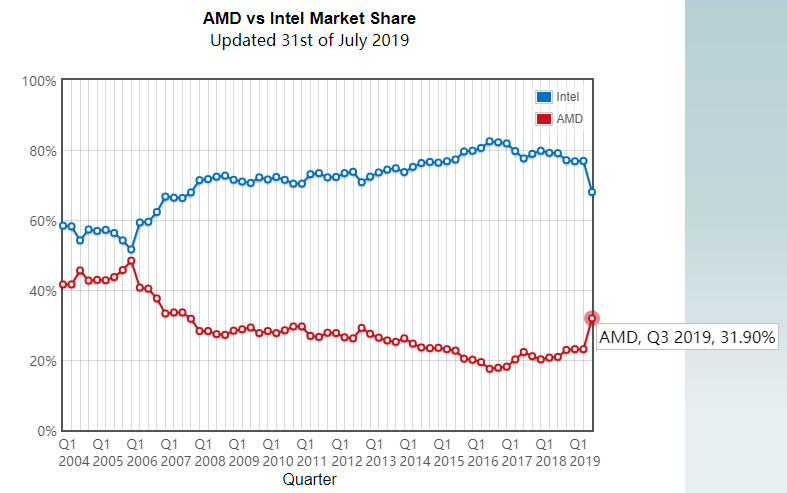

As noted before, Intel's capacity crunch forced many PC OEMs to raise the share of AMD CPU models, such as Lenovo. Plus, notebooks are now the main volume driver for gaming, where AMD's presence has been too weak. Especially with mobile CPU performance long criticized, Intel — despite obsessing over 14nm+++ — still commands a dominant notebook share. Per Intel's Q2 report, notebook CPU shipments grew 15% sequentially, the standout in the CCG segment.

Data source: Intel earnings

Unknown whether AMD's mobile CPU lineup will get a 7nm upgrade in the second half.

Data Center Business Soars Against the Tide

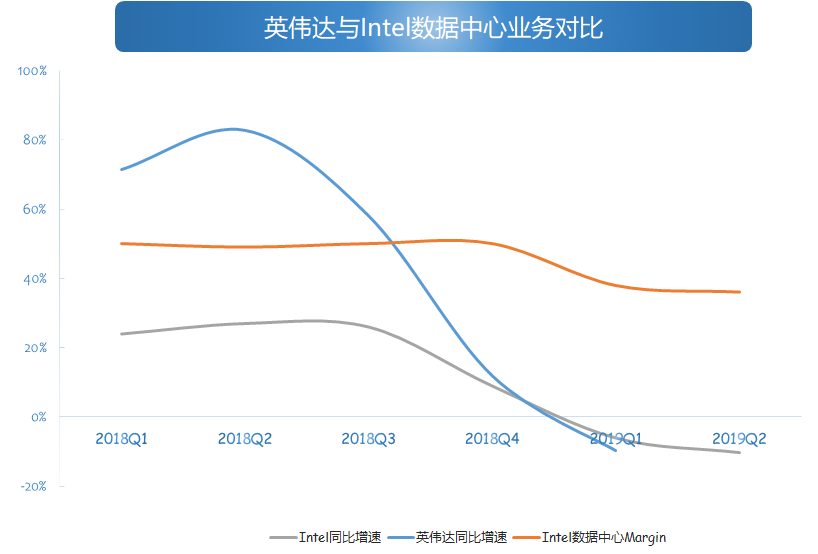

Data center is the business with the most overlap among Intel, NVIDIA, and AMD. Intel and NVIDIA both saw data center revenue decline year over year in 2019 Q1; Intel failed to reverse the year-over-year decline in Q2 either. Intel's data center is mainly CPU, NVIDIA's mainly GPU, while AMD has both CPU and GPU — EPYC and Radeon.

In the first half of 2019, AMD scored wins in both cloud and supercomputing. In cloud, it secured orders from AWS, Microsoft, and Google Stadia; in supercomputing, it won the U.S. Department of Energy's Frontier project.

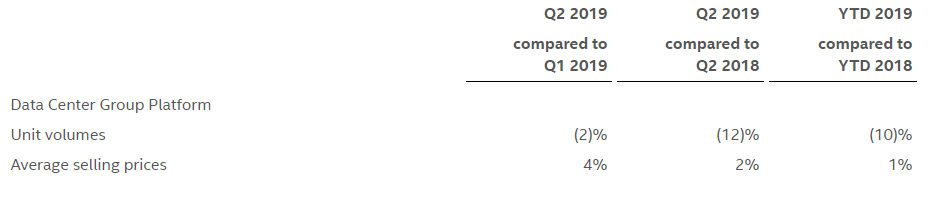

AMD's Q2 data center CPU and GPU businesses both grew significantly year over year and sequentially. Data center revenue share remains around 15%, with Q2 split slightly favoring CPU over GPU. On margins, referencing Intel's still-rising data center ASP, EPYC faces limited price-war threat for now.

Data source: Intel earnings

Overall, with the official shipment of second-gen EPYC Rome in the second half, data center remains a bright spot for AMD.

Samsung, the Savior?

Previously Samsung and AMD reached a mobile GPU partnership. At the time, Samsung seemed the bigger beneficiary — Exynos could finally crush Qualcomm Snapdragon. But I was wrong; AMD is the real winner. Under the deal, Samsung pays AMD $100M, with a small portion recognized in Q2 and the rest split roughly evenly between Q3 and Q4 revenue.

On the earnings call, Wall Street showed intense interest. Under relentless analyst questioning, AMD disclosed that this revenue differs from traditional IP licensing, requires deducting some costs, but carries a gross margin above the company average. At a 40% gross margin, the deal would contribute $40M in gross profit — a meaningful amount for AMD.

Second Half Worth Anticipating

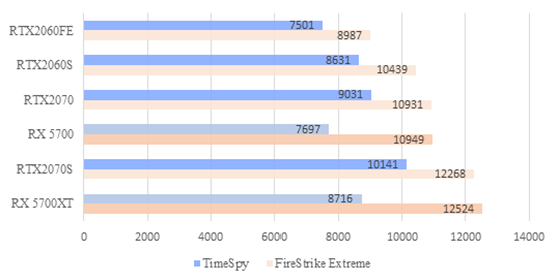

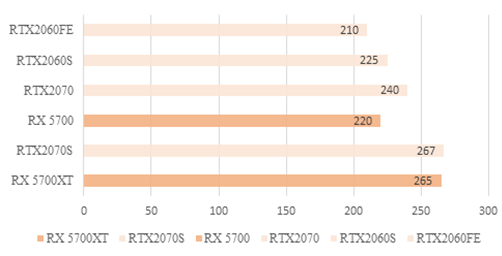

Lisa Su has consistently emphasized that the second half is typically AMD's "peak season." This year is no exception, especially with new products rolling out. The 7nm Navi-based RX 5700 series launched recently and market response has been very strong.

Source: ZOL 3DMark review

Source: ZOL GPU power consumption review

Whether from 3DMark scores, real-game benchmarks, or the long-criticized power consumption, the AMD Radeon RX 5700 series significantly exceeded expectations. Combined with AMD's aggressive pricing in China, second-half Radeon shipments are expected to be substantial. The third-gen Ryzen CPU needs no further elaboration — performance gains are obvious, daring to go toe-to-toe with Intel.

Source: PassMark

The company's full-year outlook calls for mid-single-digit year-over-year revenue growth (assume 5%). If Q3 comes in at the guided $1.8B, Q4 would need to reach $2.2B, implying 54.8% year-over-year growth!

Even with the $100M Samsung boost, spreading it across Q3/Q4 and netting it out still leaves Q4 requiring 51% year-over-year growth!

Full-year Non-GAAP operating expense ratio outlook is ~30%; Q1/Q2 ratios were 39%/33% respectively.

On free cash flow, Q1/Q2 were negative, but full-year guidance is positive. If 2019 free cash flow turns positive, AMD will achieve its first positive free cash flow in three years.

Overall, the company is confident about the second half.

Conclusion

"2019 will be the year AMD blooms in both CPU and GPU."

If you think Q2 missed expectations, your expectations likely didn't account for AMD's Q2 product gap. My only doubt is whether the full-year gross margin outlook is overly conservative.

But overall, I maintain my prior view: "For AMD, Q3 is the real final exam; Q2 was just a mock test."