This is AMD's best-ever earnings report: revenue and net income surged, PC business hit records, next-gen consoles extended a perfect launch, EPYC stole Intel share, and the data center runway is enticing.

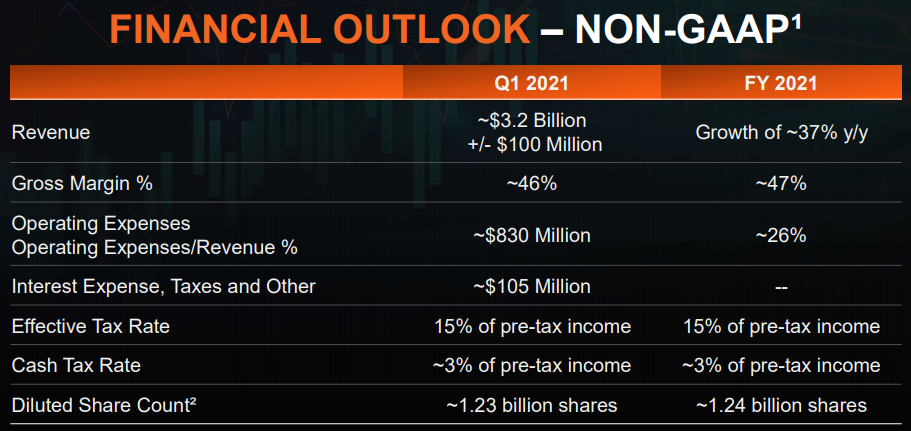

AMD embarks on a new journey! Expecting 2021 revenue up 37% year over year.

When Intel reported, we noted that AMD and NVIDIA beats were all but guaranteed.

The results confirmed it: this is yet another of AMD's best-ever earnings reports.

AMD Q4 Earnings Summary:

Revenue $3.244B, up 53% year over year, up 16% sequentially; prior guidance was $3.0B;

Non-GAAP gross margin 45%, flat year over year, up 1 ppt sequentially, in line with guidance;

Non-GAAP operating income $663M, up 64% year over year, up 26% sequentially; prior guidance was $600M;

Non-GAAP net income $636M, up 66% year over year, up 27% sequentially

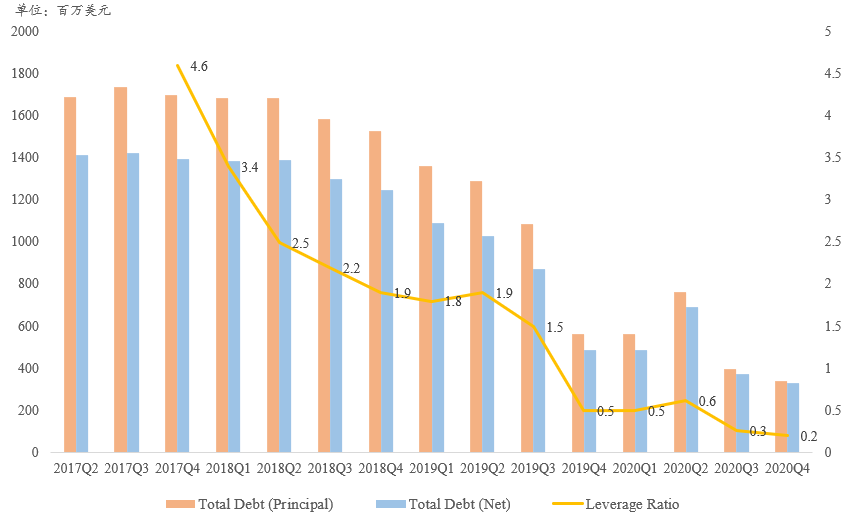

Notably, AMD's leverage further decreased this quarter, with interest-bearing debt principal down 15% sequentially and leverage ratio falling to 0.2x, fully shedding its historical baggage.

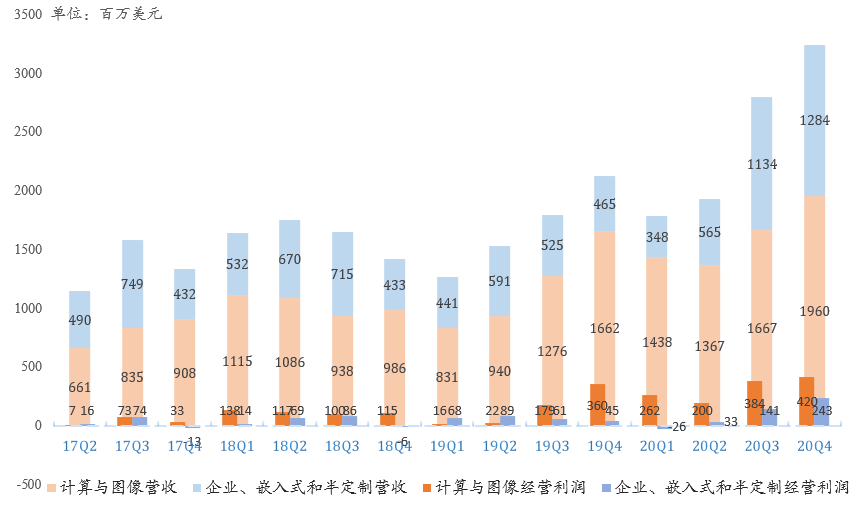

PC business sets another record! Notebook revenue hits new high

AMD Q4 Computing & Graphics revenue was $1.96B, up 17.9% year over year, up 17.6% sequentially, a record high; operating income $420M, up 16.7% year over year.

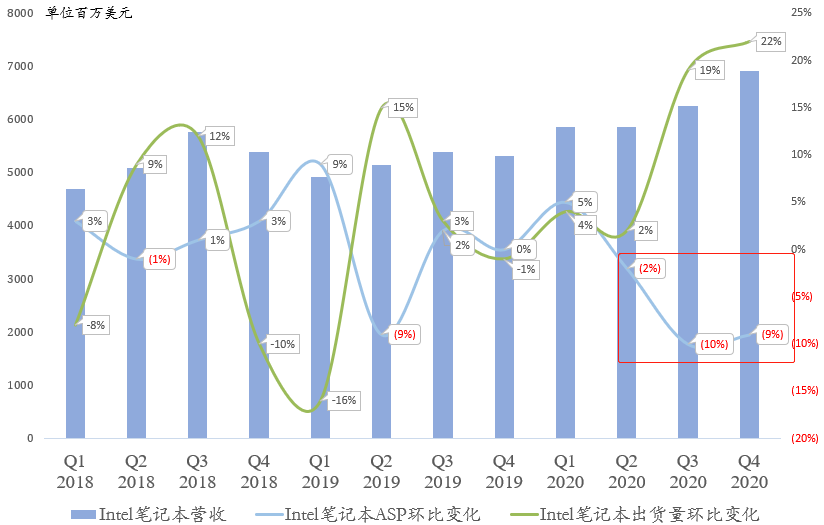

The notebook business we've been bullish on continues to deliver. This quarter, notebook CPU shipments grew double digits year over year and revenue hit a record, driving total PC CPU revenue to a record high! In contrast, Intel's notebook ASP has fallen sequentially for three straight quarters, underscoring the pressure AMD is applying.

Desktop CPU revenue also achieved double growth year over year and sequentially. Notably, Zen 3-based Ryzen 5000 desktop series launch set a record, doubling the prior generation's launch revenue.

On graphics, with RDNA 2 notebook parts not yet launched, revenue was driven mainly by desktop Radeon 6000 series; revenue fell year over year but rose sequentially, and the segment's presence remains modest. However, management is confident in 2021 graphics demand.

Next-gen console business extends perfect launch

Next-gen consoles have been a highlight of AMD's earnings for several quarters, because PS5 and Xbox Series X are selling like hotcakes.

AMD Q4 Enterprise, Embedded & Semi-Custom revenue was $1.284B, up 176% year over year, up 13% sequentially! Operating income $243M, up 72% year over year.

Historically, consoles take 4-6 quarters to fully ramp. But management says this time is different, expecting supply constraints to persist through first-half 2021. The market's only worry is that low console margins drag down corporate gross margin; CEO Lisa Su says console margins are steadily improving.

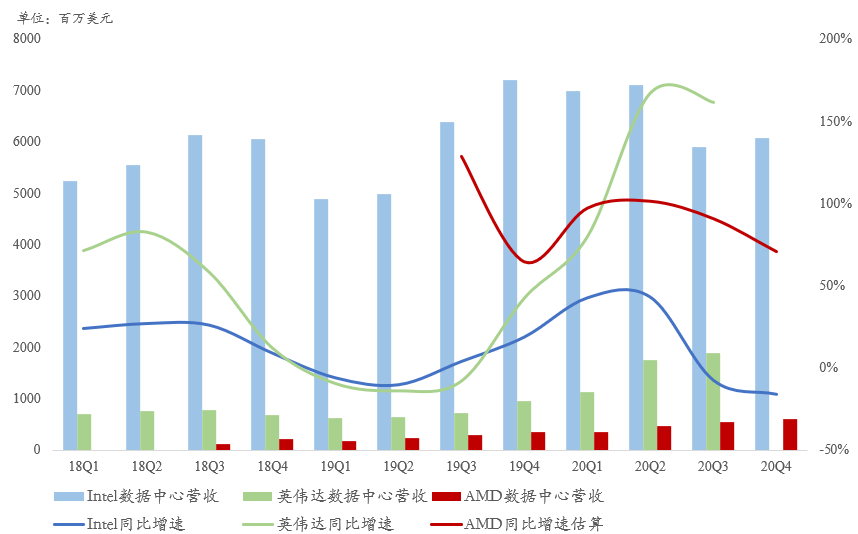

EPYC successfully wins Intel customers, AMD data center remains optimistic

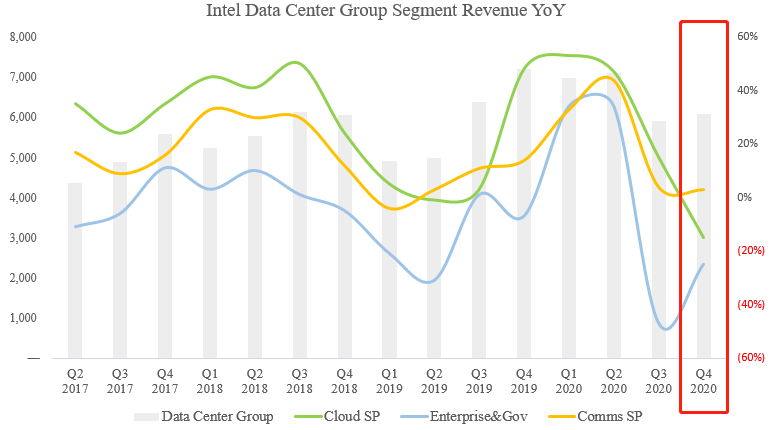

Intel Q4 data center revenue was $6.088B, down 15.6% year over year; data center ASP ticked up slightly sequentially; 5G business was the sole bright spot.

Notably, Intel Q4 government/enterprise revenue continued to fall 25% year over year; retail customers grew low single digits for two straight quarters; cloud customer revenue fell 15% year over year in Q4.

Interestingly, AMD's Q4 call stated that data center cloud and enterprise revenue grew significantly sequentially, especially cloud, which was brilliant, and expects continued sequential growth in Q1. We have reason to believe AMD truly took Intel customers; given the vast share gap (~10%-90%), AMD's data center CPU runway is enormous.

AMD's Q4 data center star remains EPYC. EPYC Q4 revenue set another record, estimated above $500M. But data center GPU remains weak, only up sequentially, consistent with our long-standing view that AMD's data center benchmark is Intel, not NVIDIA. We estimate AMD Q4 data center revenue around $600M.

In contrast, Intel's Q1 data center outlook is somewhat pessimistic, with broad data center down 25% year over year. Yet Micron, SK hynix and other memory giants are uniformly bullish on data center. AMD likewise is optimistic on Q1 data center. Notably, Q1 is also the quarter where Intel's 10nm Ice Lake server CPU and AMD's 7nm Milan EPYC go head-to-head.

Capacity constraints exist, but management confident; full-year guidance strong

In "Yesterday's Preview" we noted that in AMD's best era and Intel's worst, it would be awkward if capacity couldn't keep up.

Since H2 2020, AMD's desktop RDNA 2 GPUs, data center CDNA GPUs, console SoCs, Zen 3 Ryzen and EPYC have all concentrated at TSMC, making AMD TSMC's second-largest customer, with potential to surpass Apple as the largest. Recent rumors that Intel will place large orders at TSMC have raised concerns about AMD capacity being squeezed.

On today's call, facing analysts' challenges, Lisa Su acknowledged Q4 capacity was tight but said discussions with TSMC were settled and 2021 capacity is not an issue.

AMD also issued 2021 full-year guidance, expecting revenue up 37% year over year! Intel provided none. The next highly anticipated earnings is NVIDIA's.

As said before, the era's train has quietly turned; 2021 may still belong to AMD and NVIDIA. Once the Xilinx acquisition closes, the three-kingdoms standoff among NVIDIA, Intel, and AMD will formally arrive.