AMD Q3 Earnings:

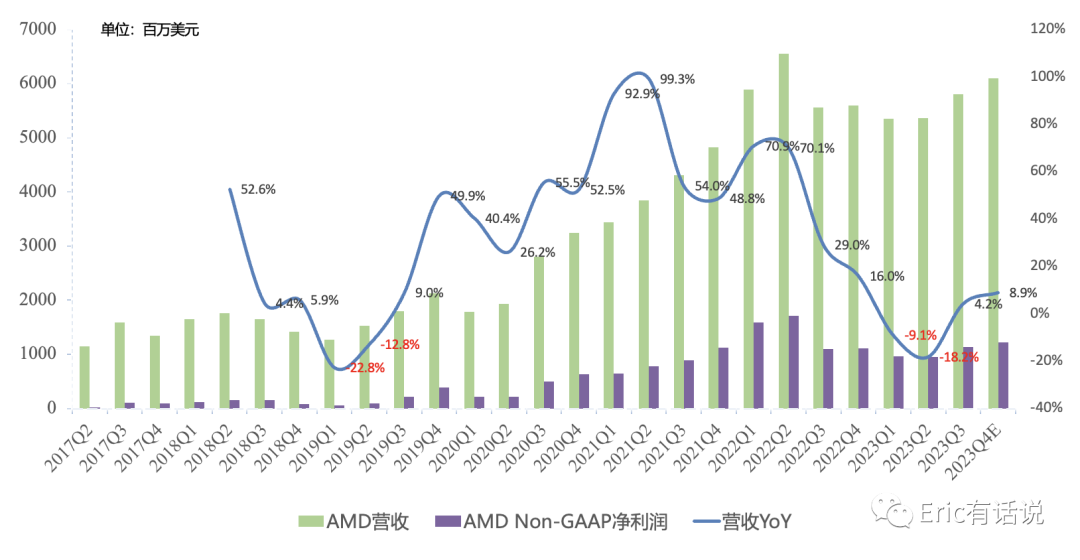

Revenue was $5.8B, up 4% year over year and 8% sequentially, above prior guidance of $5.7B; guiding Q4 revenue of $6.1B, up 9% year over year and 5% sequentially, but below prior guidance of $6.3B.

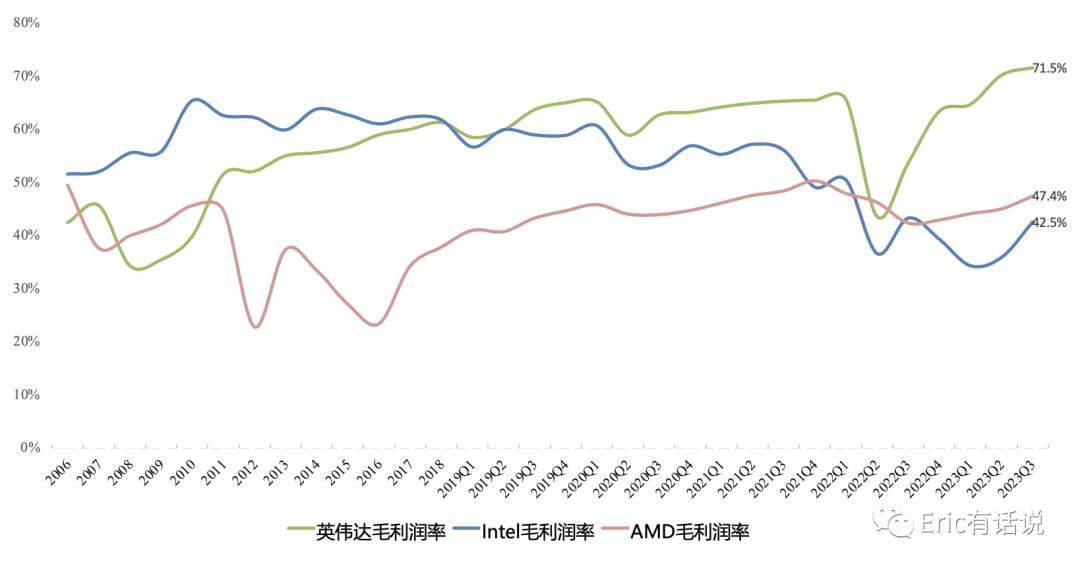

GAAP gross margin 47%, non-GAAP gross margin 51%, in line with prior guidance.

GAAP operating income was $224M, ending 4 consecutive quarters of losses; non-GAAP operating income was $1.276B, flat year over year and up 20% sequentially; guiding Q4 non-GAAP operating income of $1.4B, up 11% year over year.

GAAP net income was $300M, up 353% year over year; non-GAAP net income was $1.135B, up 4% year over year, still a distance from the 2022Q4 peak of $1.7B; guiding Q4 non-GAAP net income of $1.219B, up 10% year over year.

Operating cash flow was $421M, down 56% year over year and up 11% sequentially; prior historical peak was $1B in 2022Q4.

Q3 by Segment:

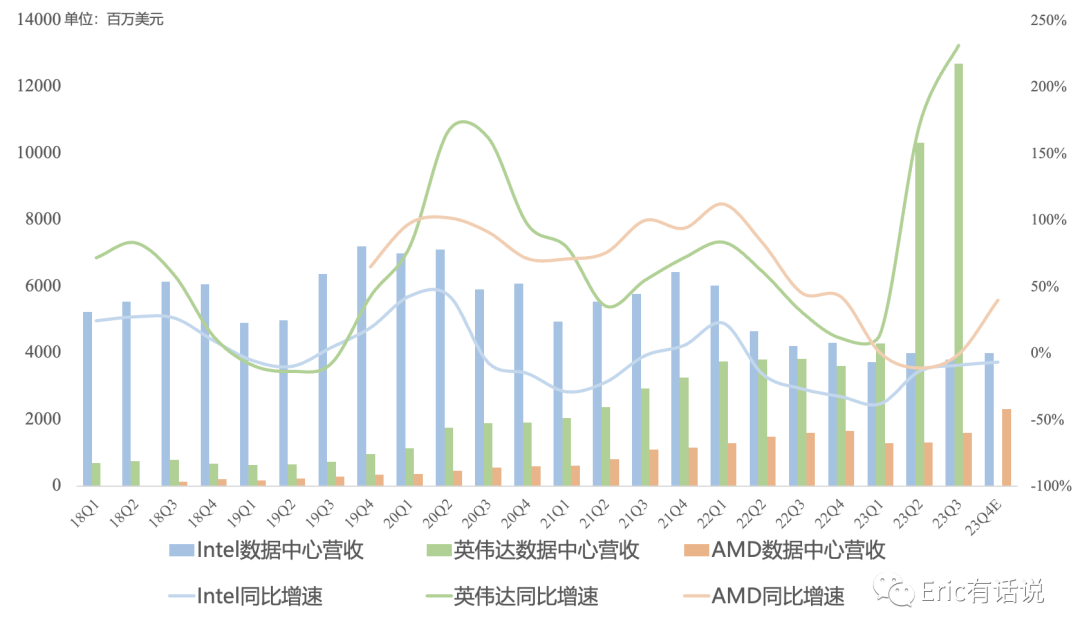

Data center revenue was $1.598B, down 1% year over year, accounting for 28% of revenue; operating income was $306M, down 40% year over year, the third consecutive quarter of decline.

EPYC revenue set another record, up double digits sequentially; 4th-gen EPYC (Genoa + Bergamo) revenue up over 50% sequentially, with shipments and revenue now representing the bulk of EPYC, driven primarily by cloud customer demand; overall server CPU market share continues to rise; enterprise achieved double-digit sequential growth despite weak industry demand; Zen 5 EPYC Turin launches in 2024; MI300A APU for the El Capitan supercomputer began shipping this month, MI300X to follow in a few weeks; ROCm integrates with PyTorch and TensorFlow ecosystems, Hugging Face uses a significant number of AMD AI chips; the MI300 product line will become the fastest AMD product to reach $1B in revenue; AMD will not sell AI products in full-system form going forward.

Guidance for data center H2 revenue up 50% vs. H1 is unchanged. Data center FPGA will grow next year but volume will be small and share low. Q4 data center GPU revenue is expected to be $400M (supercomputing); 2024 data center GPU revenue over $2B (Q1 $400M+, mostly AI customers plus some supercomputing; subsequent quarters almost entirely AI customers).

Embedded revenue was $1.243B, down 5% year over year, accounting for 21% of revenue; operating income was $612M, down 4% year over year, still AMD's highest-margin business, mostly Xilinx; embedded communications and industrial markets weak, lead times normalizing; guiding continued sequential declines in embedded revenue in Q4 this year and Q1 next year, with customer destocking continuing through H1 2024.

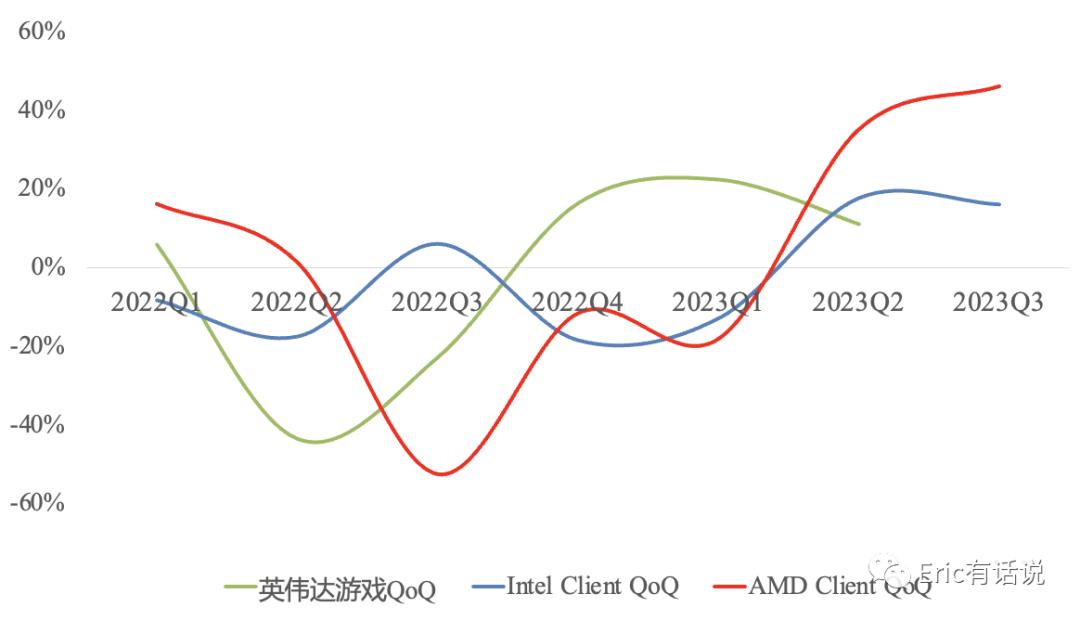

Client revenue was $1.453B, up 42% year over year and 46% sequentially, accounting for 25% of revenue. Operating income was $140M, ending four consecutive quarters of losses. Ryzen 7000 series revenue doubled sequentially, driven largely by notebooks. PC inventory has normalized. Full-year PC unit shipments are expected around 250M–255M, with growth expected next year. Q4 Client revenue is expected to grow double digits year over year and continue growing sequentially.

Gaming revenue was $1.506B, down 8% year over year, the fourth consecutive quarter of decline, accounting for 26% of revenue; operating income was $208M, up 46% year over year; gaming GPU revenue grew both year over year and sequentially; gaming console revenue declined year over year, with weak demand persisting into next year.

Guiding Q4 Client revenue up double digits year over year and sequentially, data center revenue up double digits both year over year and sequentially, gaming and embedded revenue down ~10% both year over year and sequentially, gaming console revenue down ~20% sequentially.

Next Q1 gaming and embedded revenue to continue declining sequentially; Client, EPYC server, and gaming businesses will see seasonal declines; embedded and gaming console businesses under pressure in H1 next year, with H2 recovery driving rapid company-wide gross margin expansion.

Overall, Q2 this year was indeed AMD's trough. With global semiconductor demand recovering and the AI market expanding rapidly, AMD is still on track to surpass its 2022 highs. Non-GAAP net income is expected to hold at the previously forecast $7B, supporting a valuation of $200B–$300B.

A slight disappointment: AMD cannot fire on all cylinders next year, with embedded and gaming weak in H1 offsetting some AI incremental revenue. Also, $2B+ full-year AI GPU revenue is not that much; traditional server CPU revenue can no longer grow on volume alone and must rely on ASP growth, so how much incremental contribution EPYC can still make to data center is also a question.

Previous concerns on AMD were mainly:

1) Whether Arm server CPUs represented by NVIDIA can disrupt the existing x86 server CPU market (not yet occurred, under observation)

2) Xilinx slowing significantly (currently slowing)

3) Process technology bottleneck, Intel outsourcing to TSMC (Qualcomm Win on Arm challenging x86, watching)