In yesterday's "Earnings Preview | Notebook and Data Center Explosion Imminent, AMD Poised to Make History Again," our judgments on AMD were validated one by one in the earnings report.

AMD revenue came in $5M above our prior forecast of $3.44B and $245M above guidance. Non-GAAP net income was $642M, up 189% year over year, a record high for the third consecutive quarter.

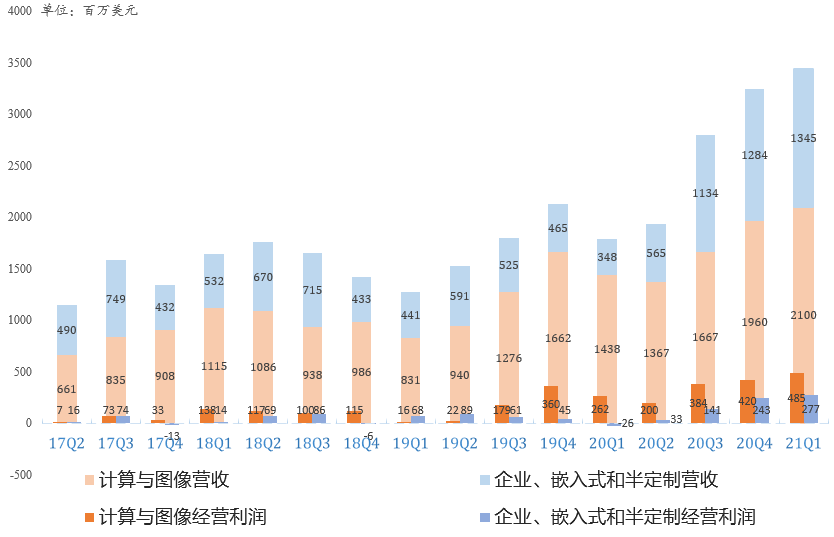

AMD Q1 Computing & Graphics revenue was $2.1B, up 46% year over year, up 7% sequentially; Enterprise, Embedded & Semi-Custom revenue was $1.345B, up 286% year over year, up 5% sequentially.

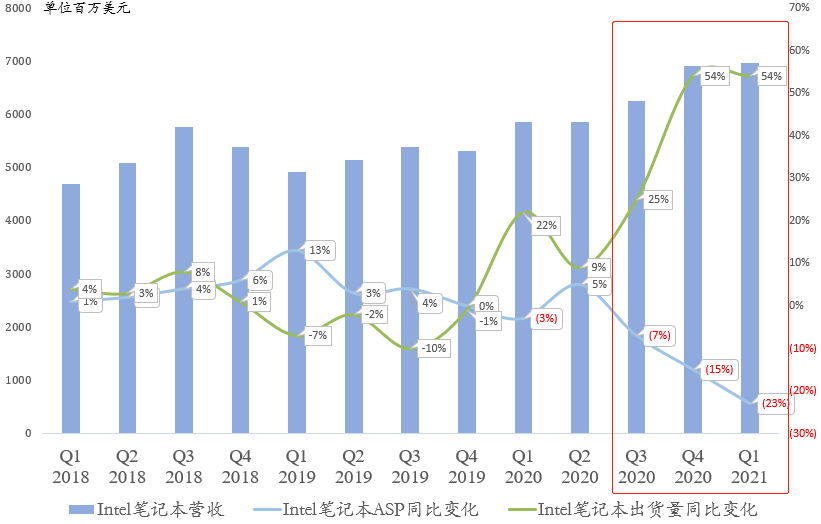

AMD notebook revenue records for sixth straight quarter, ASP hits new high

IDC data shows total PC industry shipments grew 55.2% year over year. Intel, AMD, and NVIDIA PC beats were all but guaranteed.

Per Intel's earnings, Intel notebook ASP has declined for three consecutive quarters with accelerating pace! This means Intel's shipments are heavily weighted toward entry-level Chromebooks. Yet AMD's CPU revenue hit a record while ASP grew both year over year and sequentially. Notebook revenue has set records for six straight quarters.

Viewed this way, Intel's mainstream market is indeed under serious threat from AMD.

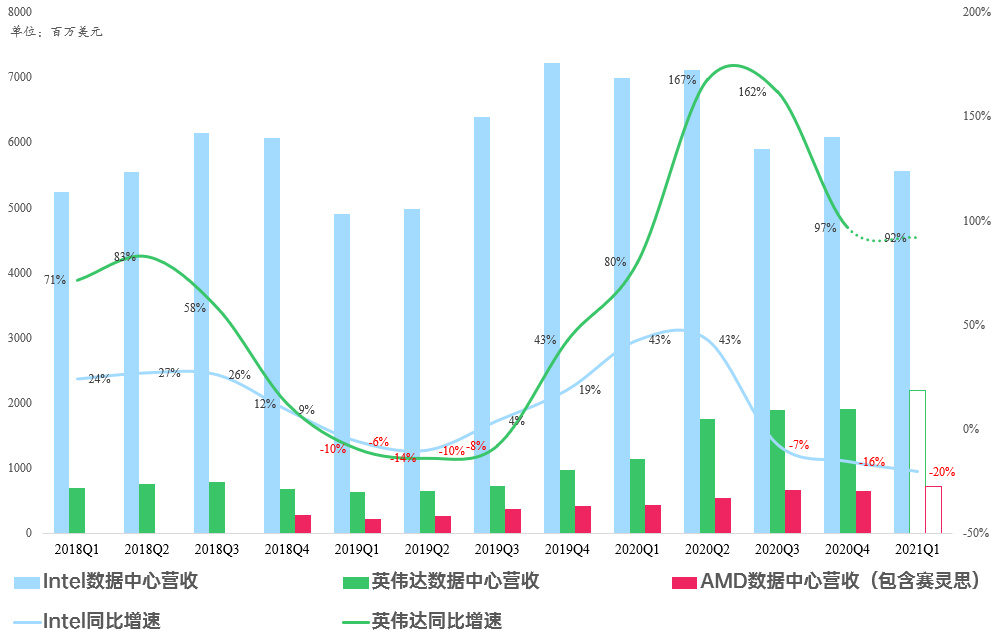

Data center robust all year, aggressively taking Intel share

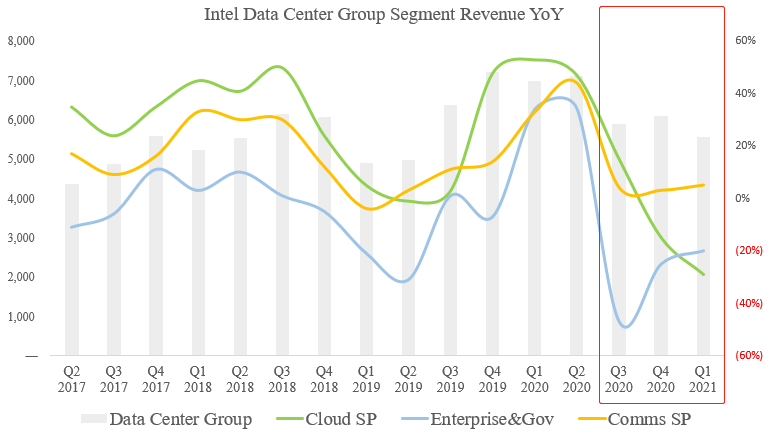

Intel's Q1 data center revenue was $5.564B, down 20.4% year over year, even including the Optane business. Intel's data center revenue share hit a new low since 2017 at just 28.3%. Even scarier, Q1 data center operating margin fell to 22.9%, a new low.

We previously judged that because NVIDIA DGX data centers deeply bind AMD EPYC with NVIDIA DGX A100, EPYC would further eat into Intel Xeon share. That was confirmed by Intel's earnings, and now again by AMD's earnings.

AMD EPYC Q1 revenue doubled year over year and continued to grow sequentially, setting another record, with cloud computing tied to NVIDIA performing exceptionally well. This contrasts sharply with Intel's plummeting cloud revenue.

Additionally, next-gen console business surged year over year, with only a modest sequential decline; PS5 global shipments have exceeded 7.8M units since launch. Management expects the second half to be even stronger.

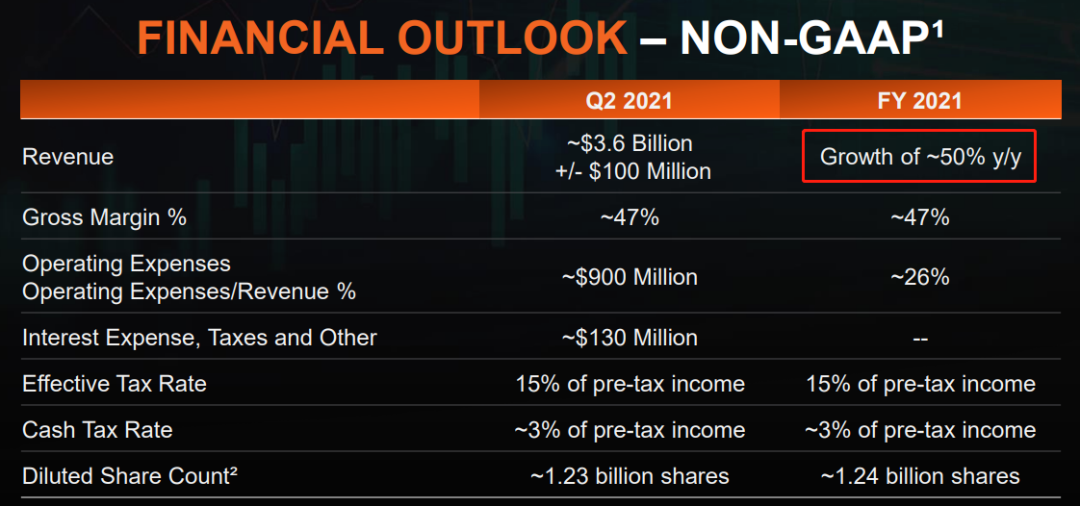

Continuing the Intel comeback, AMD sharply raises full-year revenue guidance

Faced with such a strong Q1, management significantly raised full-year revenue guidance (growth from 37% to 50%) and issued a Q2 guide of $3.6B, again a record high.

Not that AMD is sailing smoothly; capacity constraints persist. Simultaneous product-line refreshes across CPU, GPU, data center, and consoles have drained TSMC capacity.

Moreover, the global ABF substrate shortage is intensifying, to the point where Intel is scrambling to secure ABF substrate supply.

Lisa Su also noted on the call that, besides TSMC's full support, AMD plans to invest in the substrate industry, whose importance has been underestimated.

Overall, this is yet another of AMD's best-ever earnings reports, and the progress of the Xilinx acquisition is equally worth watching. But faced with Arm's strong rise, Lisa Su has not made a forward-looking layout—perhaps that is the gap between AMD and NVIDIA.

If AMD's logic is overtaking Intel, NVIDIA's is leading the future.