Microsoft's FY26Q3 covers January through March 2026.

Microsoft FY2026 Q3 Results Summary:

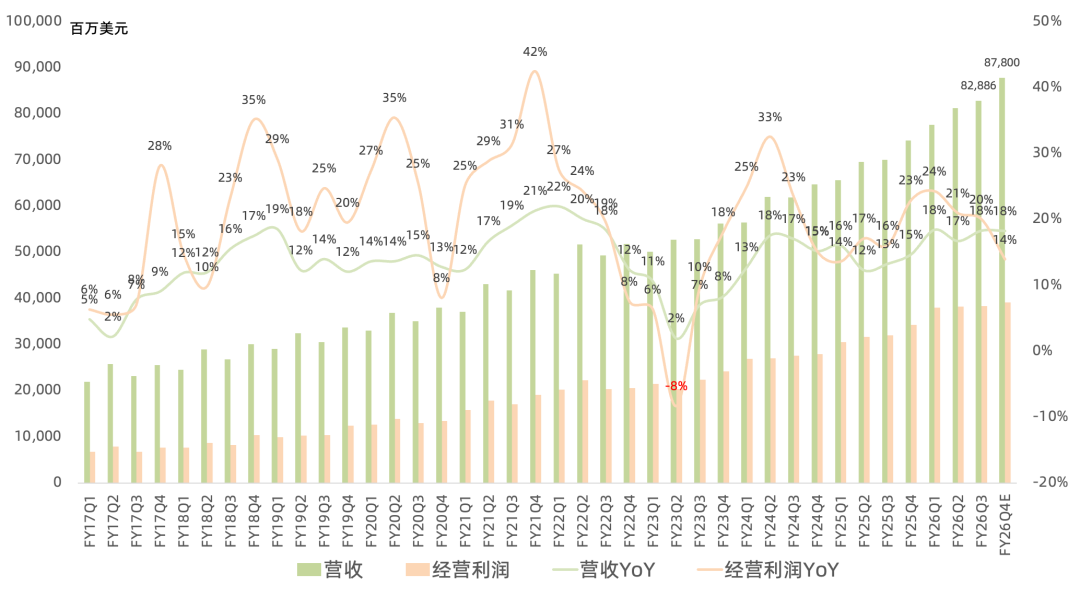

Revenue reached $82.9B, up 18% year over year and above the company's prior guidance range of $80.65B-$81.75B.

Gross margin was 67.6%, down 1.1 percentage points year over year but above the 67.4% high end of prior guidance.

Operating income reached $38.4B, up 20% year over year and above the $37.3B high end of prior guidance.

GAAP net income reached $31.8B, up 23% year over year. Non-GAAP net income was also $31.8B, up 20% and above the $30.8B high end of prior guidance.

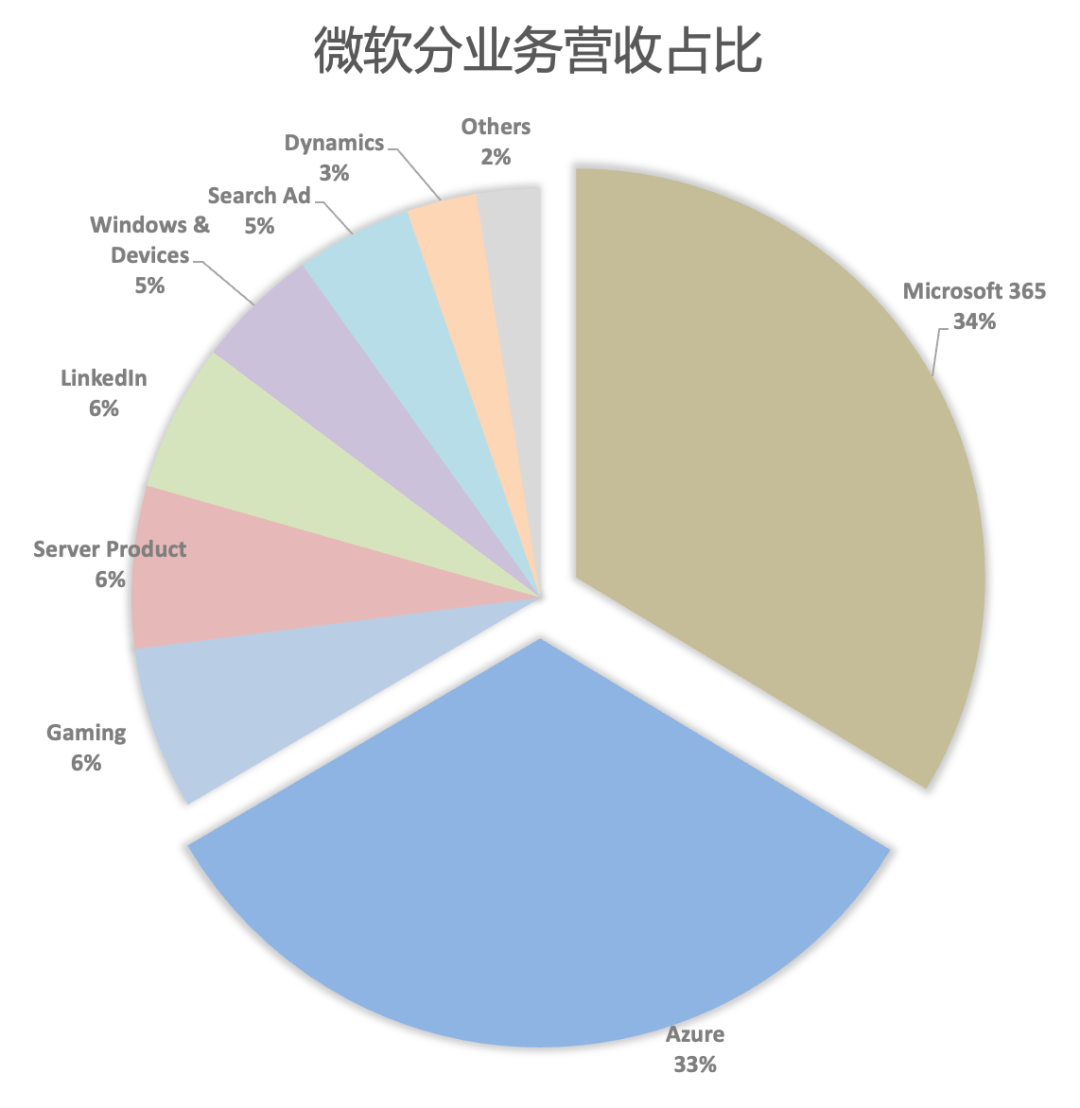

Productivity and Business Processes

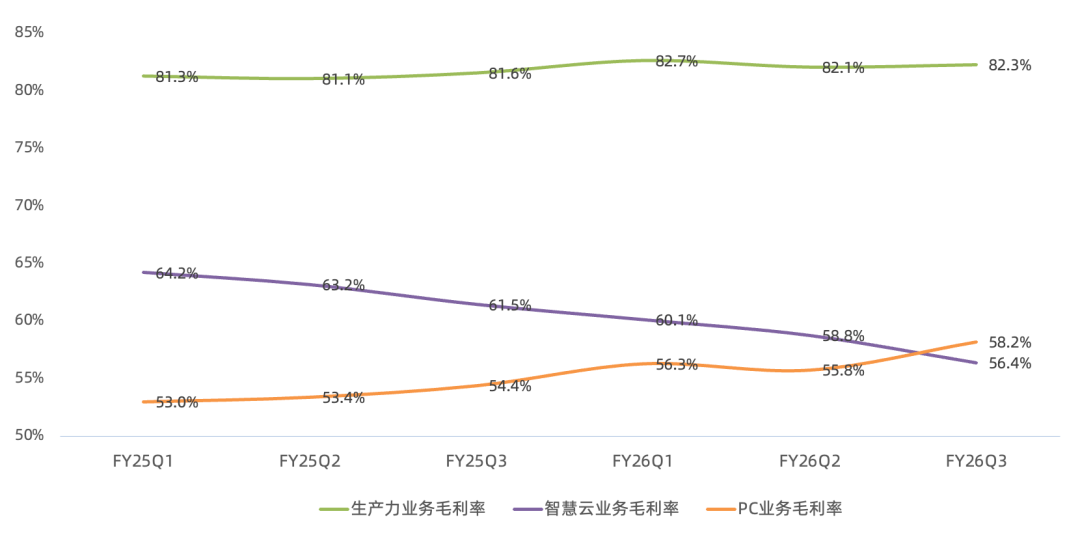

Productivity and Business Processes, which includes Microsoft 365, LinkedIn, and Dynamics, generated $35B of revenue, up 17% year over year. Gross margin expanded 1.7 percentage points to 82.3%, while operating income rose 21% to $21B.

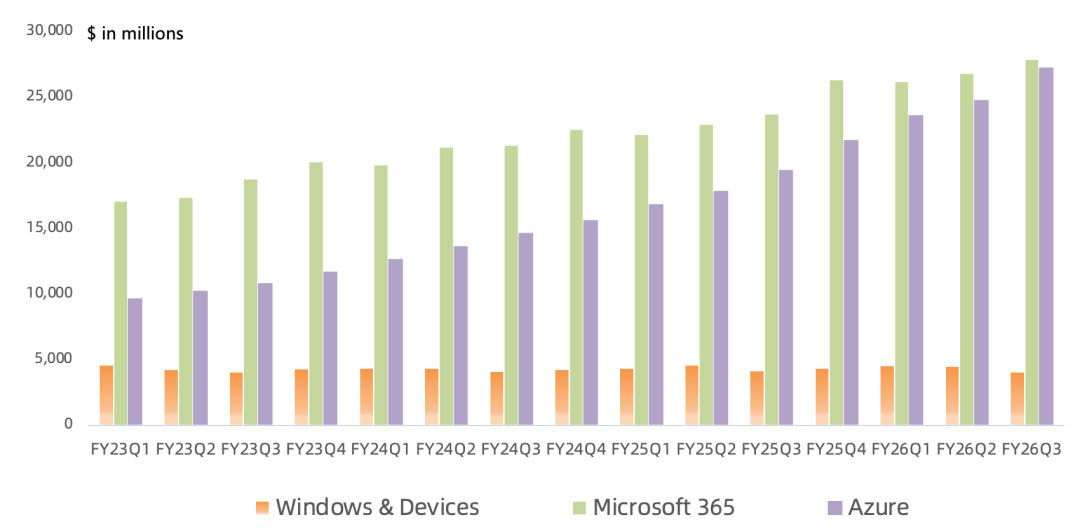

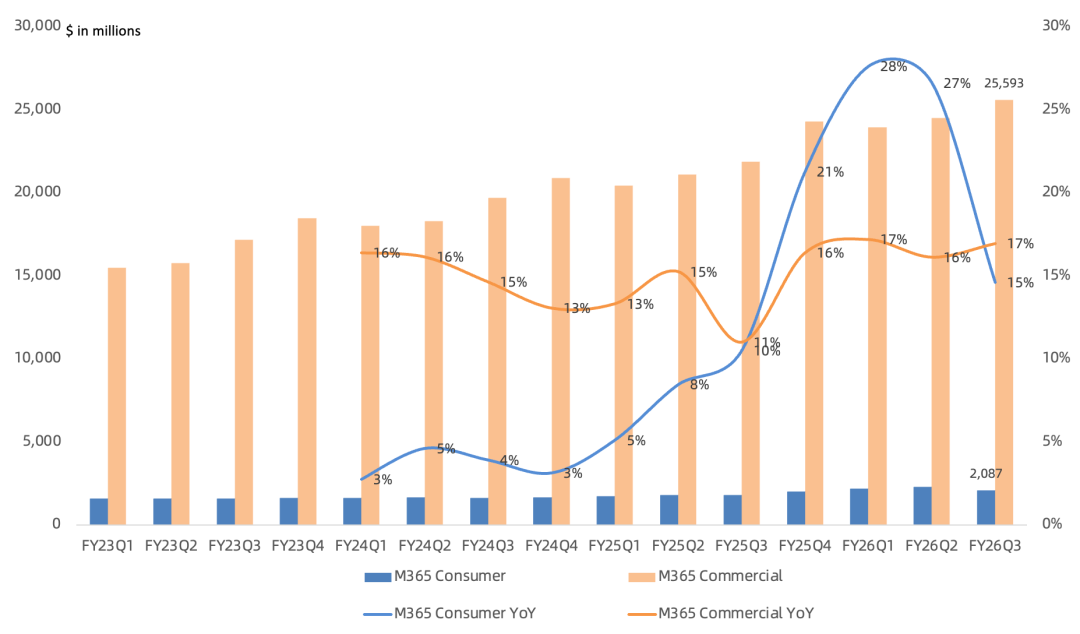

Microsoft 365 revenue was approximately $27.9B, up 18% year over year. Commercial cloud growth reflected both higher ARPU and more seats, with E5 and M365 Copilot again leading the ARPU increase. Commercial cloud revenue grew 17% as paid seats increased 6% to more than 460 million. Consumer cloud revenue rose 15%, also driven by higher ARPU, while consumer subscriptions grew 7% to nearly 95 million.

M365 Copilot, priced at $30 per user per month, added a record number of seats. Paid seats grew 250% year over year to more than 20 million. The number of customers with over 50,000 Copilot seats quadrupled, led by Accenture with more than 740,000 seats, the largest Copilot order to date. Microsoft Copilot monthly active usage has grown sixfold since the start of 2026, while weekly engagement has reached the level of Outlook. Consumption of usage-based Copilot credits nearly doubled sequentially. Customers are moving from a traditional seat model to a seat-plus-usage model, and nearly 60% of services customers now purchase usage-based credits.

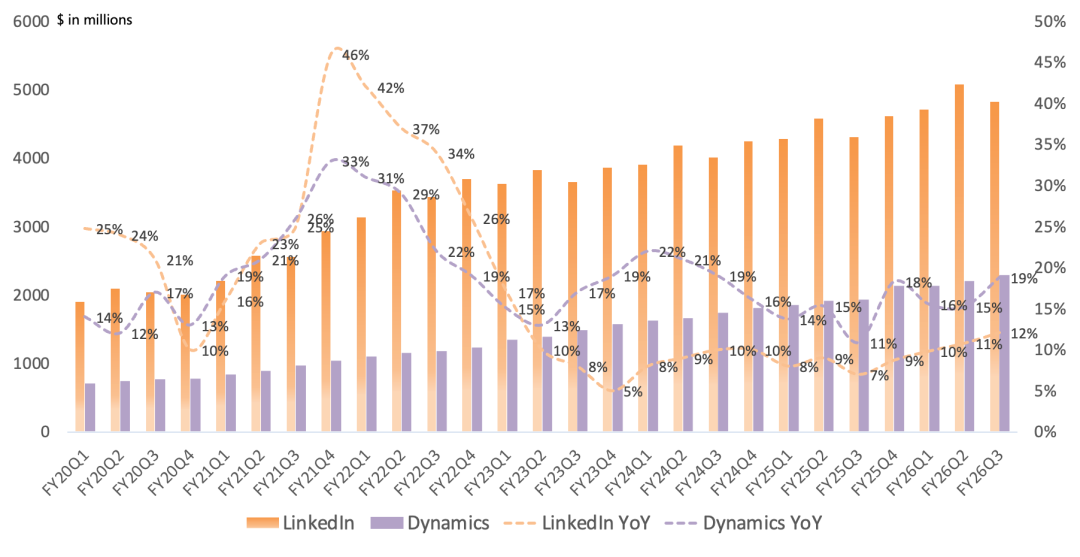

LinkedIn revenue reached $4.8B, up 12% year over year. Membership exceeded 1.3 billion, with growth across every line of business.

Dynamics revenue reached $2.3B, up 19% year over year, while Dynamics 365 revenue grew 22%. Dynamics bookings were held back by softer renewals as customers balanced spending between the traditional per-seat model and the emerging seat-plus-usage model.

Intelligent Cloud

Intelligent Cloud, which includes Azure, Server Products, and Enterprise Services, generated $34.7B of revenue, up 30% year over year. Gross margin fell 5.1 percentage points to 56.4%, while operating income increased 24% to $13.8B. In a striking reversal, Intelligent Cloud's gross margin has now fallen below that of More Personal Computing.

Azure revenue was approximately $27.3B, up 40% year over year and accelerating by 1 percentage point sequentially. Consumption of both AI and non-AI services continued to rise, while demand is expected to exceed supply throughout 2026. Management expects Azure growth to accelerate modestly in the second half of calendar 2026. AI annual recurring revenue exceeded $37B, up 123%, including revenue from leading AI model developers on Azure and Microsoft's first-party AI applications and services. More than 10,000 customers have used multiple models in Foundry, 5,000 have used open-source models, and the number using Anthropic and OpenAI models doubled sequentially. More than 300 customers are expected to process over one trillion tokens each on Microsoft Foundry in 2026, up 30% sequentially. Microsoft remains focused on its in-house MAI models while continuing to innovate on OpenAI intellectual property.

Microsoft added nearly 1 GW of total data center capacity this quarter. Since the start of 2026, the time required to bring newly delivered GPUs online at some of its largest facilities has fallen by almost 20%. The Fairwater data center in Wisconsin came online in April, six weeks ahead of schedule, allowing revenue recognition to begin earlier. Microsoft's in-house Cobalt Arm server CPU is deployed in nearly half of its data center regions. As the company's largest customer expands its AI deployment, it is choosing Cobalt CPUs more frequently, prompting Microsoft to increase supply substantially.

In data and analytics, Fabric surpassed 35,000 paid customers, up 60% year over year, while data stored in Fabric OneLake nearly quadrupled. More than 15,000 customers now use both Foundry and Fabric, also up 60%. Cosmos DB revenue grew 50%, driven by AI application workloads. GitHub Copilot is used by 140,000 enterprise organizations, and enterprise subscribers nearly tripled. Microsoft announced earlier in the week that GitHub Copilot will move to usage-based pricing.

In cybersecurity, the number of Security Copilot customers doubled year over year.

More Personal Computing

More Personal Computing, which includes Windows, Devices, Gaming, and advertising, generated $13.2B of revenue, down 1% year over year. Gross margin expanded 3.8 percentage points to 58.2%, while operating income increased 4% to $3.7B.

Windows and Devices revenue reached $4B, down 2% year over year. Windows surpassed 1.6 billion monthly active devices. Windows OEM revenue grew slightly and exceeded expectations as OEMs and channel partners continued building inventory amid rising memory prices.

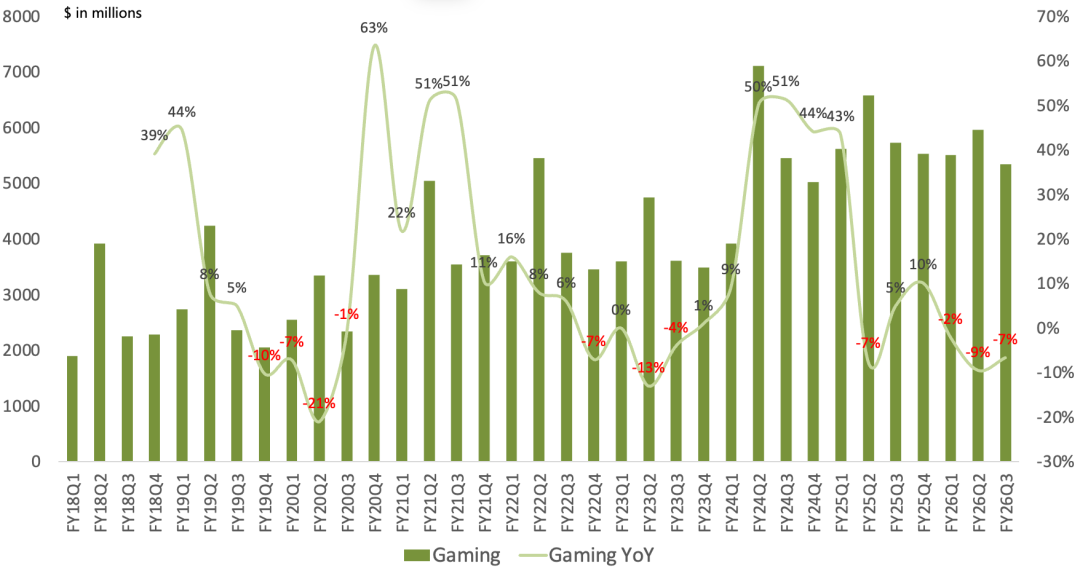

Gaming revenue reached $5.3B, down 7% year over year. Xbox hardware revenue fell another 33%, while higher-margin software revenue declined 5%. Xbox monthly active users and game-streaming hours both set records this quarter.

Search advertising revenue reached $3.8B, up 12% year over year. Edge gained share for a twentieth consecutive quarter, while Bing reached one billion monthly active users for the first time.

Earnings Call Highlights

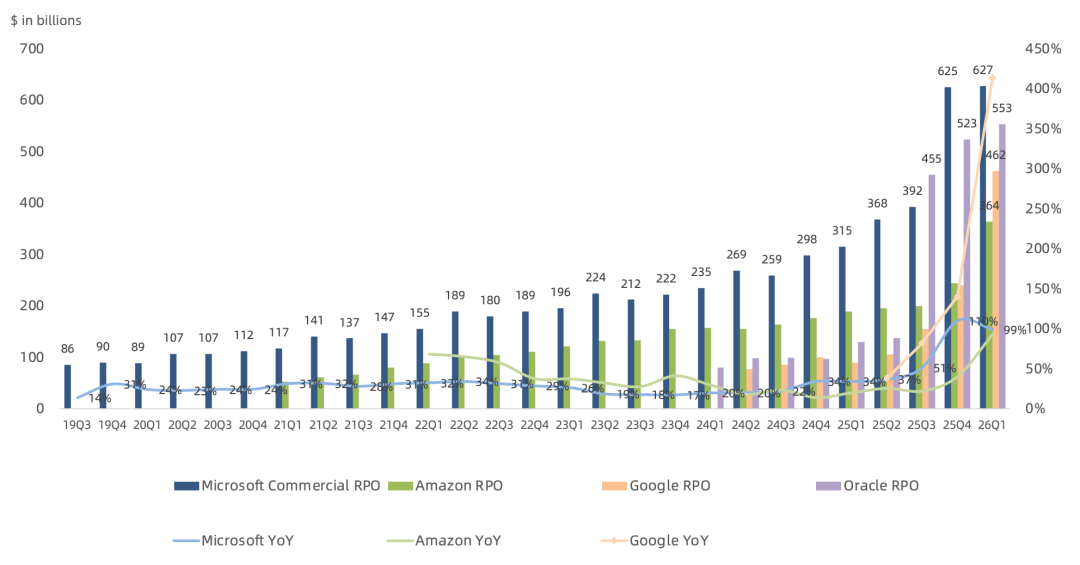

Commercial remaining performance obligations reached $627B, up 99% year over year, with a weighted average duration of about 2.5 years. Approximately 25% is expected to convert to revenue over the next twelve months, up 39%. RPO excluding OpenAI grew 26%. Investors have become increasingly skeptical of RPO after Oracle's use of the metric, and Microsoft's unusually high OpenAI concentration has intensified those concerns.

Microsoft expects FY26Q4 revenue of $86.7B-$87.8B, up 13%-15% year over year. At the high end, gross margin would be 66.5%, down 4.1 percentage points, operating income would reach $39.1B, up 14%, and net income would reach $31.6B, up 16%. Microsoft Cloud gross margin is expected to decline further to 64% because of continued AI investment and product mix. Management expects both FY27 revenue and operating income to grow at double-digit rates.

For FY26Q4, Azure revenue is expected to grow 39%-40% year over year. M365 Commercial Cloud should grow 13%-14%, Consumer Cloud in the low twenties, LinkedIn 10%, and Dynamics 365 in the low teens. Windows OEM and Devices is expected to decline in the mid-to-high teens, search advertising to grow in the high single digits, and gaming services to decline in the low teens. Commercial bookings should increase year over year.

FY26Q4 capital expenditure is expected to exceed $40B, with rising memory prices adding to the bill. Microsoft is projected to spend $190B in calendar 2026, up 61% from $118B in 2025, including approximately $25B caused by higher prices for memory and other chips. The AI infrastructure race is still intensifying.

Microsoft's latest agreement with OpenAI gives it access to a royalty-free frontier model and all associated intellectual-property rights through 2032, while the revenue-sharing arrangement continues through 2030.

Microsoft formally launched the new M365 E7 plan on May 1, 2026, moving the business from a purely seat-based model toward seat plus usage. M365 E3 provides the enterprise productivity foundation; E5 adds advanced security, compliance, analytics, and Teams Phone; and E7 adds Copilot, Agent 365, and Entra Suite. Pricing is $36 per user per month for E3, $57 for E5, and $99 for E7.

Overall, the results again demonstrated Microsoft's stability. Sustaining double-digit revenue and profit growth while investing at this intensity is impressive. Yet the continuing decline in gross margin remains a serious risk, and foundation models are forcing the SaaS business model to shift from seats toward usage.

As Noted Last Quarter:

Despite the previously favorable outlook, Microsoft now faces two major challenges:

1. The tradeoff between gross margin and growth will continue to intensify.

2. Satya Nadella's strategy of positioning Microsoft as the scaffolding of the AI era will be tested as foundation models improve rapidly, reinforcing the market's concern that AI may consume traditional software.

This quarter offered no evidence that Microsoft's margin decline is easing. After years of enjoying a substantial profitability advantage, Microsoft Cloud is gradually being caught by Amazon AWS and Google Cloud.

On the transformation of software economics, Nadella made the direction explicit this quarter: any business that charges per user, whether productivity, coding, or security, will evolve into a combination of per-user and usage-based pricing.

The reason for this shift is that foundation models are rapidly eroding software gross margins, as illustrated by GitHub Copilot's urgent move to usage-based pricing. AI model providers are changing as well. Early products relied on memberships or seats, but token-intensive use cases such as coding can undermine the model provider's own margins under a flat subscription. Anthropic's recent tightening of subscription allowances is one example.

The key question is whether Microsoft's new software pricing model can arrest the decline in gross margin.