Microsoft FY2023 Q1 Earnings Summary:

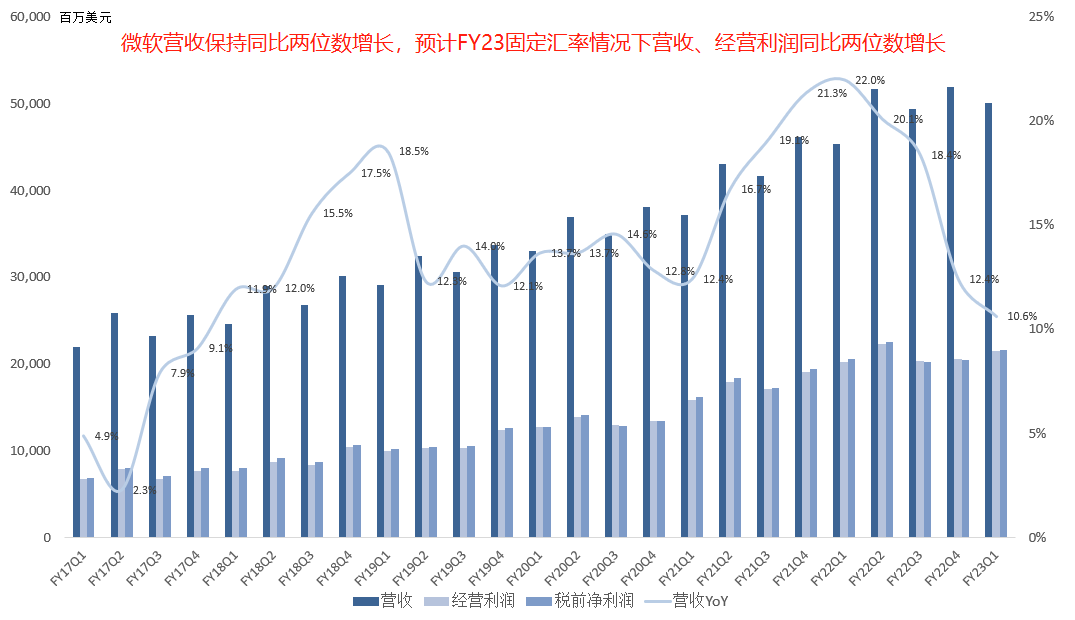

Revenue $50.122B, up 10.6% year over year, a Q1 fiscal record; with 5-point FX headwind, growth remained double-digit; operating income $21.518B, up 6.3% year over year, second-highest ever; net income $17.556B, down 14.4% year over year, mainly due to last year's unusually low tax ($19M vs $4.016B).

For comparison, Apple's latest quarter (revenue $90.146B, up 8.1% year over year; net income $20.721B, up 0.8% year over year).

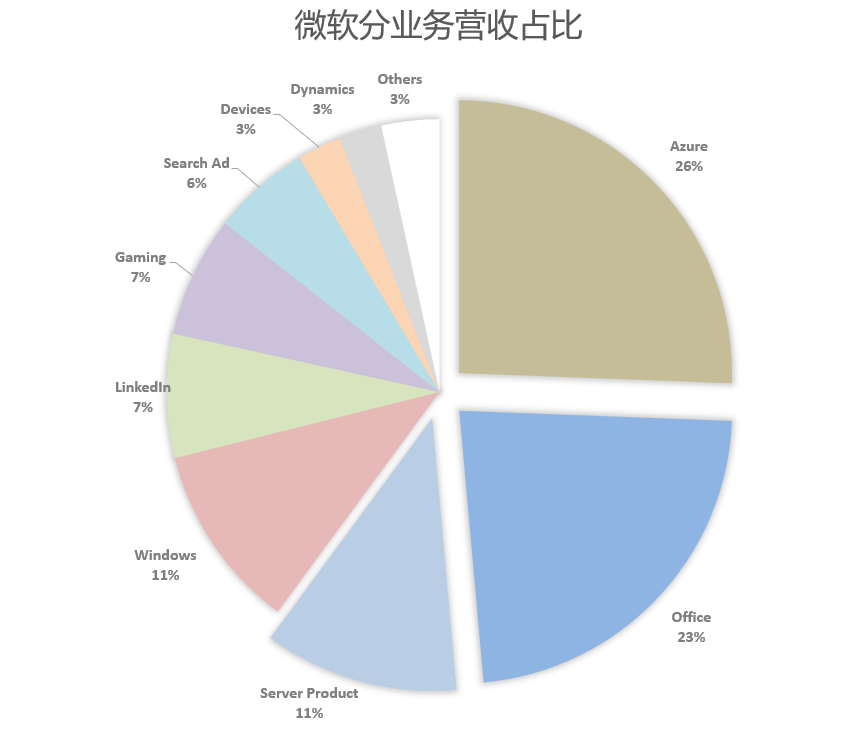

Productivity & Business Processes revenue $16.5B, up 9% year over year; operating income $8.3B, up 10% year over year;

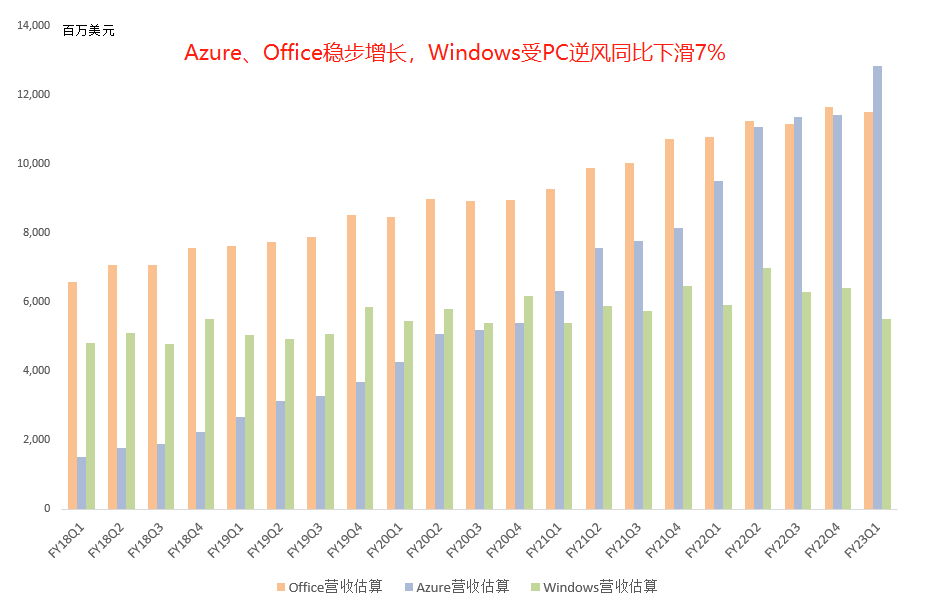

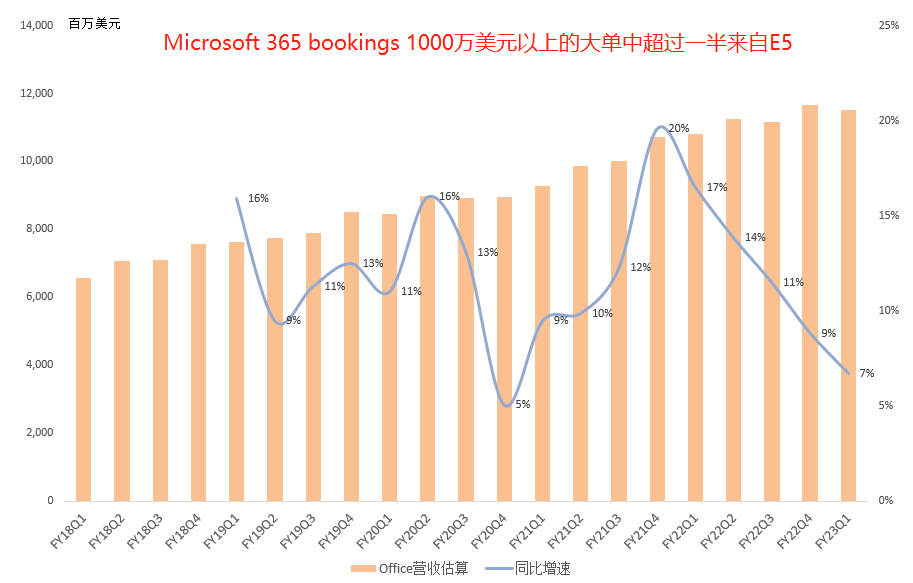

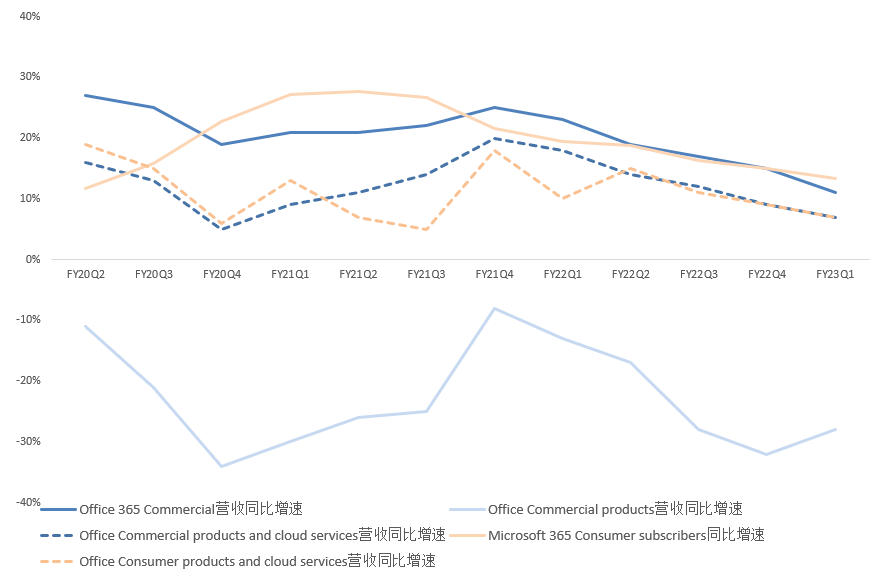

Office revenue was approximately $11.5B, up 7% year over year. The migration from Office E3 to E5 is evident; more than half of Microsoft 365 bookings over $10M are for E5. Commercial users now spend more time on Teams than on email, and 55% of Teams enterprise customers purchase Teams Rooms or Teams Phone. Security services are used by 860K enterprises, up 33% year over year; customers purchasing four or more workloads grew 50% year over year. E5 customers purchasing Sentinel security services increased 44% year over year.

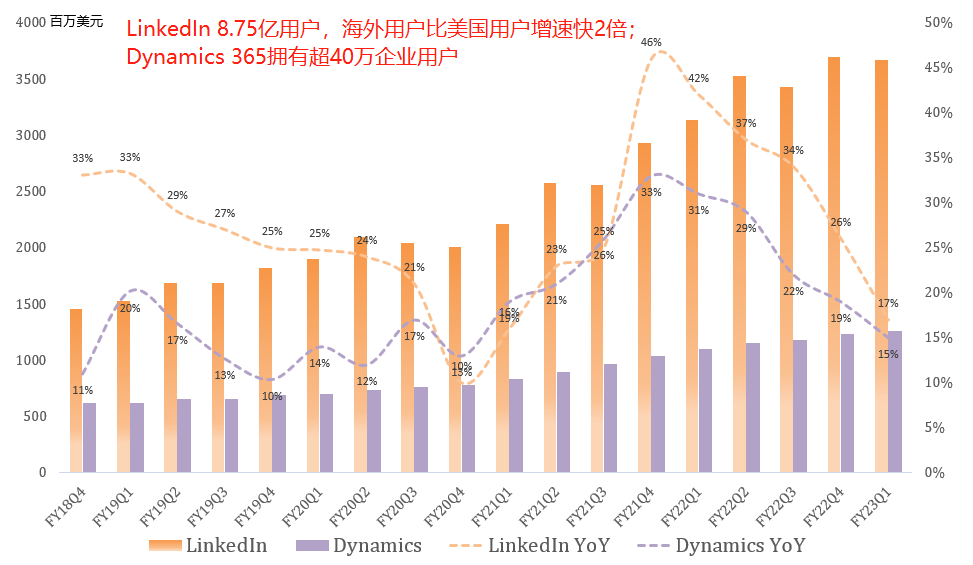

LinkedIn revenue was $3.7B, up 17% year over year. LinkedIn has 875M users; international user growth is 2x faster than U.S. user growth.

Dynamics revenue was $1.3B, up 15% year over year, setting a new record. Over 400K organizations use Dynamics 365. Power Apps MAU is approaching 15M, up 50% year over year; Power Automate MAU exceeds 7M.

Intelligent Cloud revenue was $20.3B, up 20% year over year, exceeding $20B for the second consecutive quarter. Operating income was $9.0B, up 19% year over year, a new record.

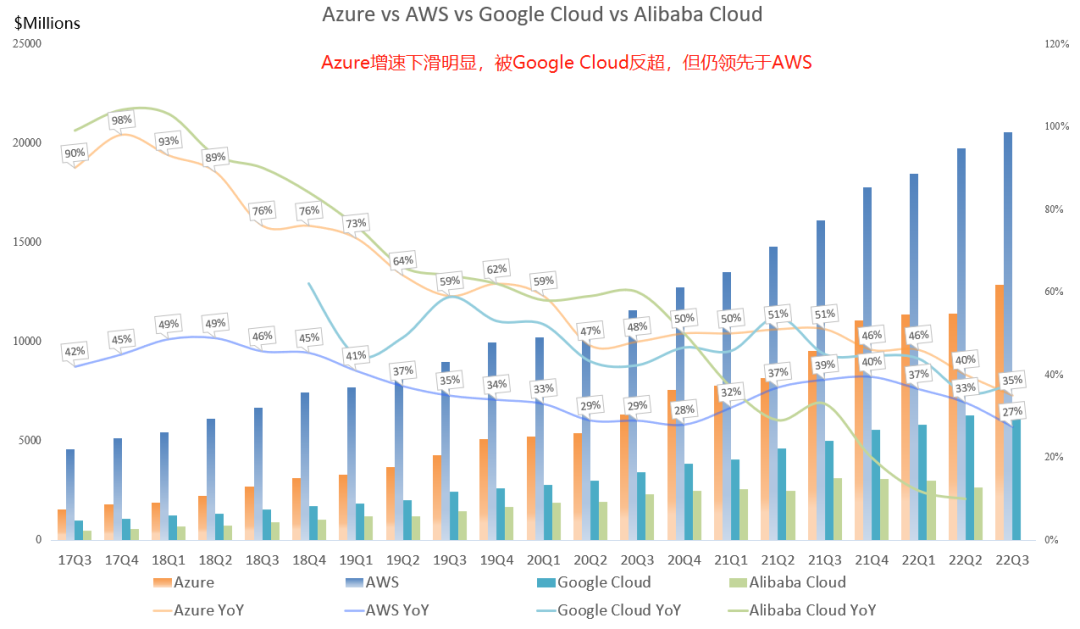

Azure revenue was approximately $12.8B, up 35% year over year, with a 7-point FX headwind. Azure Arc now has over 8,500 customers, doubling year over year. UBS has migrated more than 50% of its applications to Azure. Azure ML revenue has doubled year over year for four consecutive quarters. GitHub annualized revenue surpassed $1B, with over 90M active users.

Notably, Microsoft guided for Azure Q2 revenue to decline 5% sequentially on a constant-currency basis, which would make it the first of the three major clouds (AWS, Azure, Google Cloud) in recent years to post a sequential decline. The stock sold off sharply after hours.

Microsoft explained that backlog continues to hit new highs, but conversion to quarterly revenue may be more volatile than before. In the current macro environment, a consumption-based model like cloud computing naturally sees reduced usage when economic activity slows, as customers cut back or optimize spend.

Additionally, Microsoft noted that higher energy costs pressured Azure gross margin.

Personal Computing revenue was $13.3B, up 0.1% year over year. Operating income was $4.2B, down 17% year over year.

Windows revenue was approximately $5.5B, down 7% year over year. Monthly active Windows devices are 20% above pre-pandemic levels. Win10/Win11 users spent 8.5x more time on PCs versus pre-pandemic (overtime?).

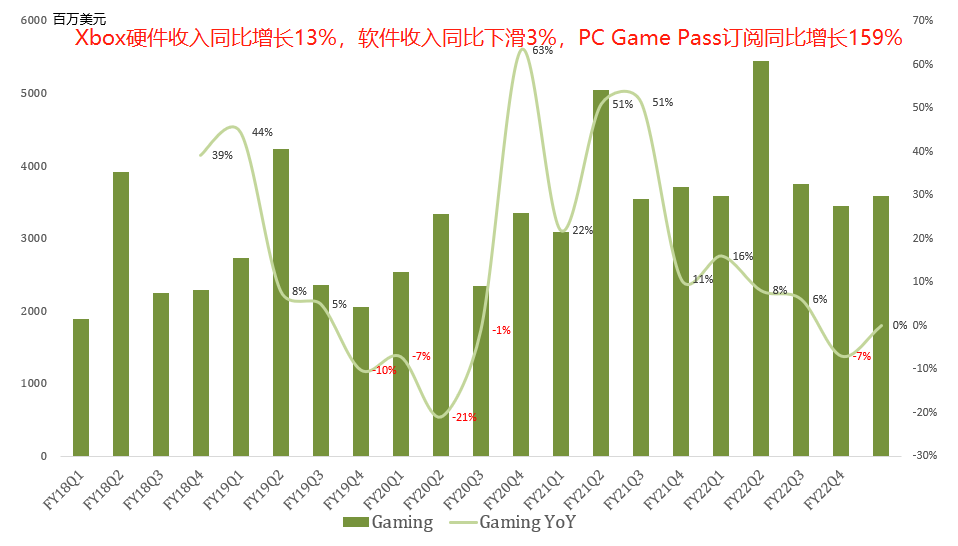

Gaming revenue was $3.6B, up slightly year over year. Xbox hardware revenue rose 13% year over year; content and services revenue fell 3% year over year. Xbox Game Pass subscriptions continue to grow. PC Game Pass subscriptions surged 159% year over year. Cumulative users who have tried cloud gaming exceed 20M.

Search and news advertising revenue was $2.9B, up 16% year over year. Edge, Start, and Bing daily usage hit records; this segment still has significant monetization headroom.

Devices revenue was $1.3B, up 2% year over year. Surface declined low-double-digits year over year, but HoloLens contributed material revenue.

Microsoft expects FY2023 revenue and operating income to grow double digits on a constant-currency basis, with broader commercial business up 20% year over year. Commercial remaining performance obligation increased 31% to $180B. Roughly 45% will be recognized as revenue in the next 12 months, up 23% year over year.

FX reduced revenue growth by 5 points and operating income growth by 9 points this quarter. FX is expected to reduce revenue growth by 5 points next quarter.

"FX impact on Microsoft this quarter was the largest among the mega-caps. Despite numerous headwinds, Microsoft upheld the dignity of the U.S. Big 4 tech stocks, delivering double-digit revenue growth and single-digit net income growth. Backlog hit a record; commercial bookings far exceeded company expectations. The $189B RPO underscores the vast runway ahead for the king of digitalization." — from 'Microsoft's Previous Earnings'

The Azure guidance 'miss' sparked market concern about Microsoft's future growth, but AWS faces the same dynamics. Still, delivering double-digit growth at this scale in this economy proves the strength of Microsoft's business model and the cloud model more broadly. Microsoft also has Apple-like untapped monetization opportunities.

In the near term, Microsoft is not immune to the economic cycle. But long term, as Nadella said, 'global digital spend as a share of GDP' is still small; we are in the early innings of global digitalization, and Microsoft is the global leader.

*All segment revenue figures above are estimates.