Microsoft's FY25Q2 covers October through December 2024.

Microsoft FY2025 Q2 Earnings Summary:

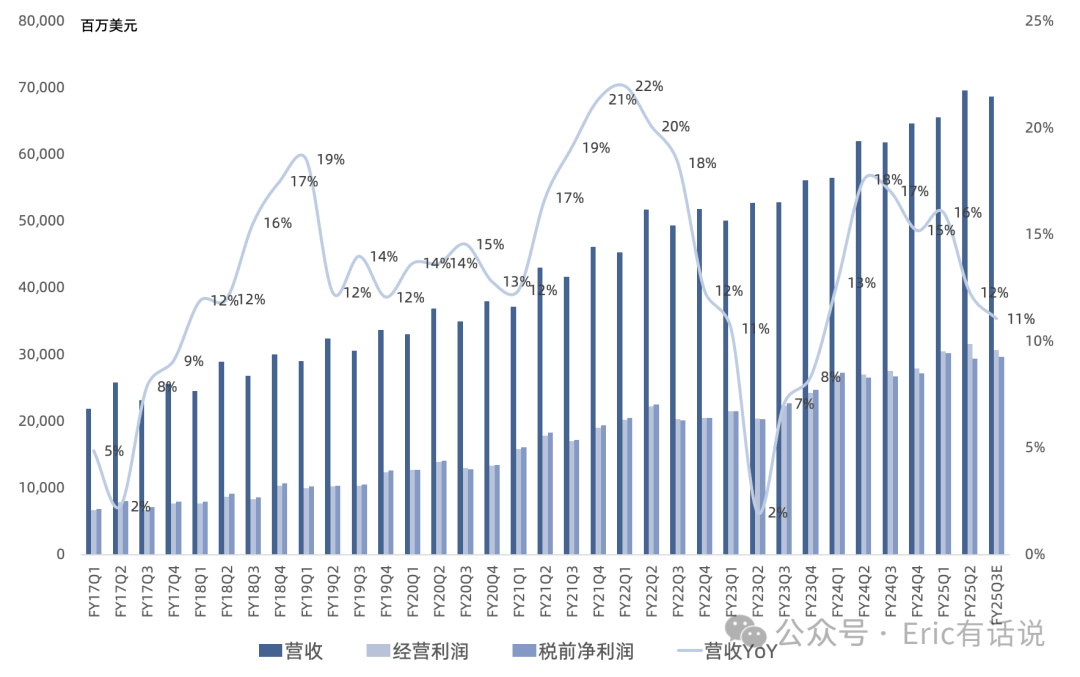

Revenue was $69.632B, up 12% year over year, setting another all-time high. Operating income was $31.653B, up 17% year over year, the eighth consecutive quarter of record highs. Net income was $24.108B, up 10% year over year.

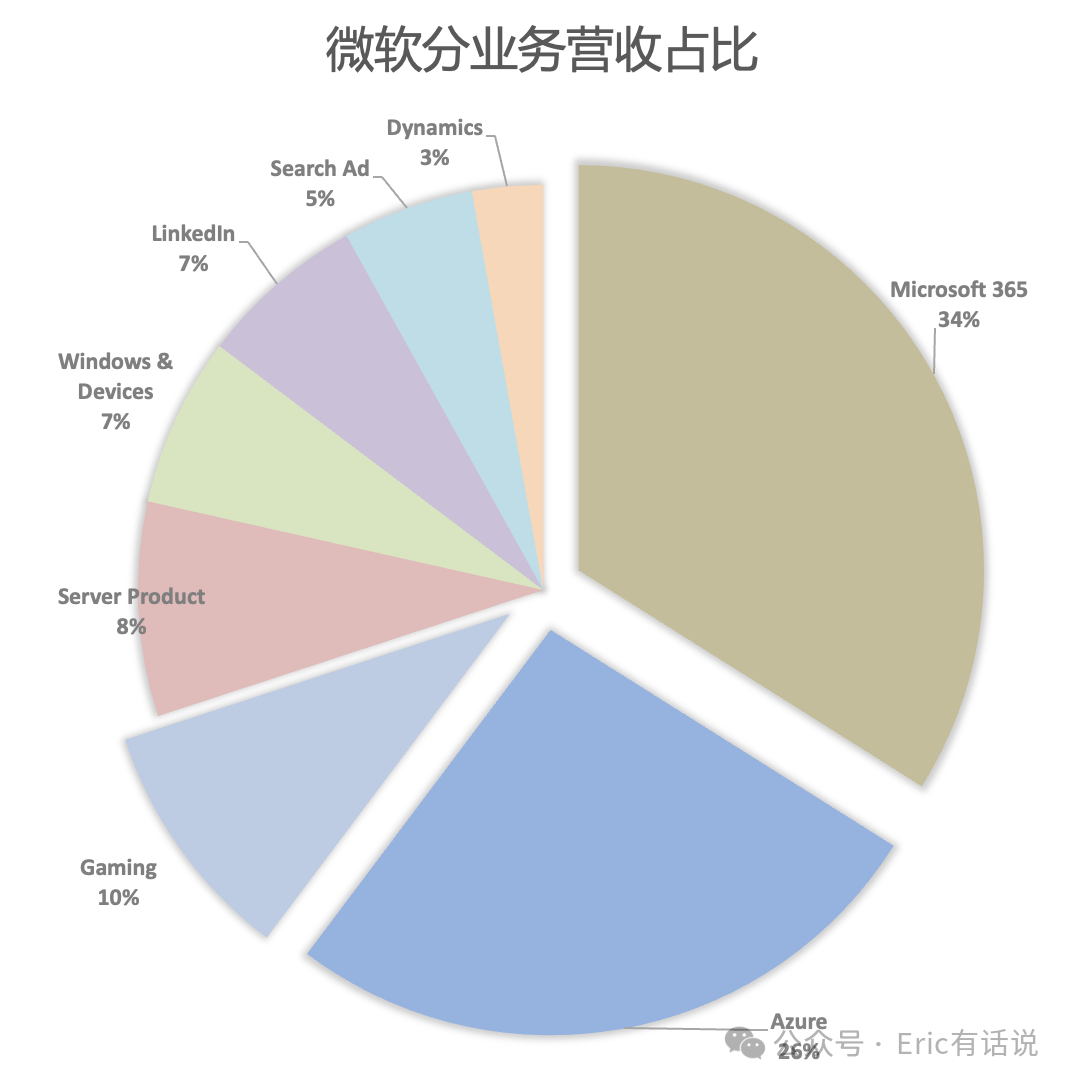

Productivity and Business Processes revenue was $29.437B, up 14% year over year. Operating income was $16.885B, up 16% year over year.

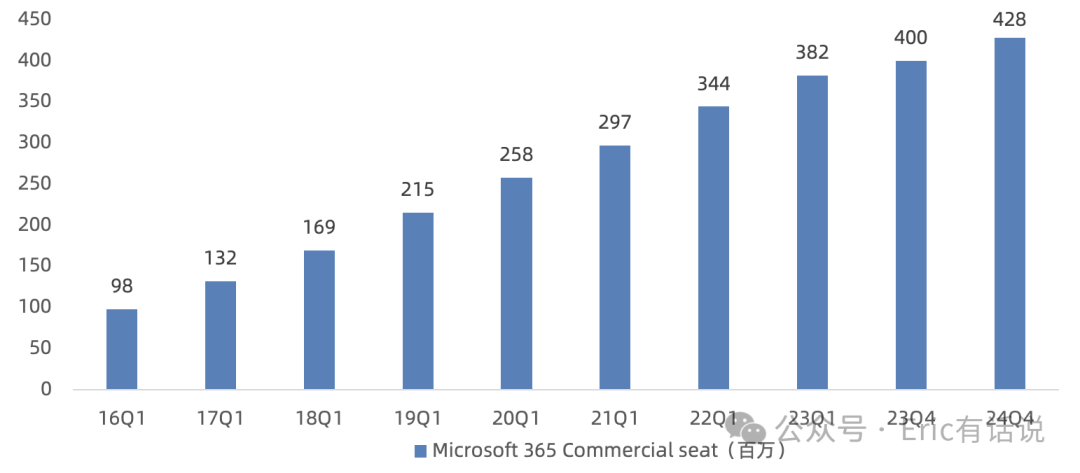

Microsoft 365 revenue was approximately $23B, up 9% year over year. Strong M365 E5 and Copilot demand drove continued ARPU uplift. Since launch, M365 Copilot customer seats have grown over 10x in the past 18 months. Daily Copilot users doubled sequentially. Usage intensity grew over 60% sequentially. Custom Copilot Studio now has over 160,000 organizations using it. This quarter, 400,000 custom agents were created, doubling sequentially.

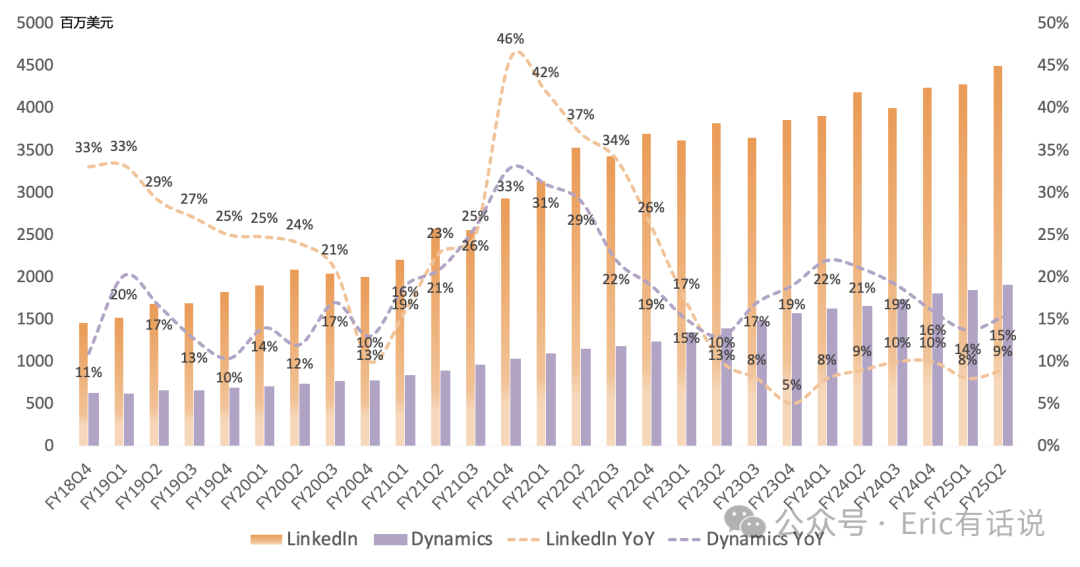

LinkedIn revenue was $4.5B, up 9% year over year. LinkedIn Premium annualized revenue surpassed $2B for the first time. LinkedIn subscribers have grown nearly 50% year over year over the past two years. Nearly 40% of users use AI features. Hiring business market share continues to rise.

Dynamics revenue was $1.9B, up 15% year over year. Dynamics 365 revenue grew 19% year over year.

Intelligent Cloud revenue was $25.544B, up 19% year over year, setting another all-time high. Operating income was $10.851B, up 14% year over year, setting another all-time high.

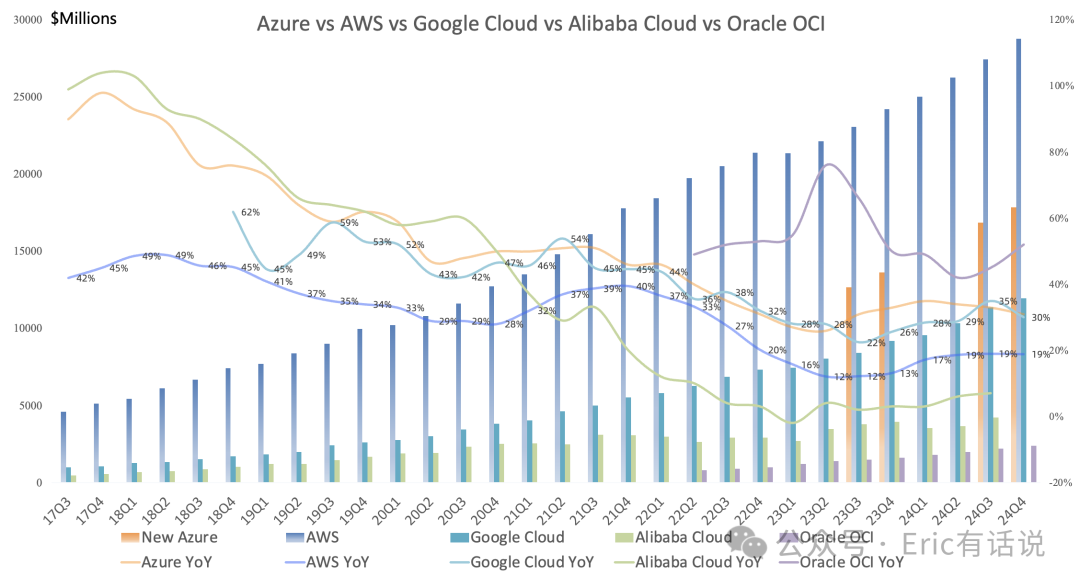

Azure revenue was approximately $17.8B, up 31% year over year. AI contributed 13 percentage points of growth ($1.8B). AI business growth exceeded expectations. Azure non-AI growth fell short of expectations. Capacity constraints persist through the end of FY25. Azure AI Foundry MAU exceeds 200,000. SLMs represented by Phi have been downloaded over 20M times cumulatively.

Fabric paid customers exceed 19,000 (up from 16,000 last quarter). Power BI and Fabric are deeply integrated, with MAU over 30M, up 40% year over year. GitHub users now exceed 150M, up 50% year over year over the past two years.

More Personal Computing revenue was $14.651B, flat year over year. Operating income was $3.917B, up 32% year over year.

Windows & Devices revenue was $4.6B, up 5% year over year.

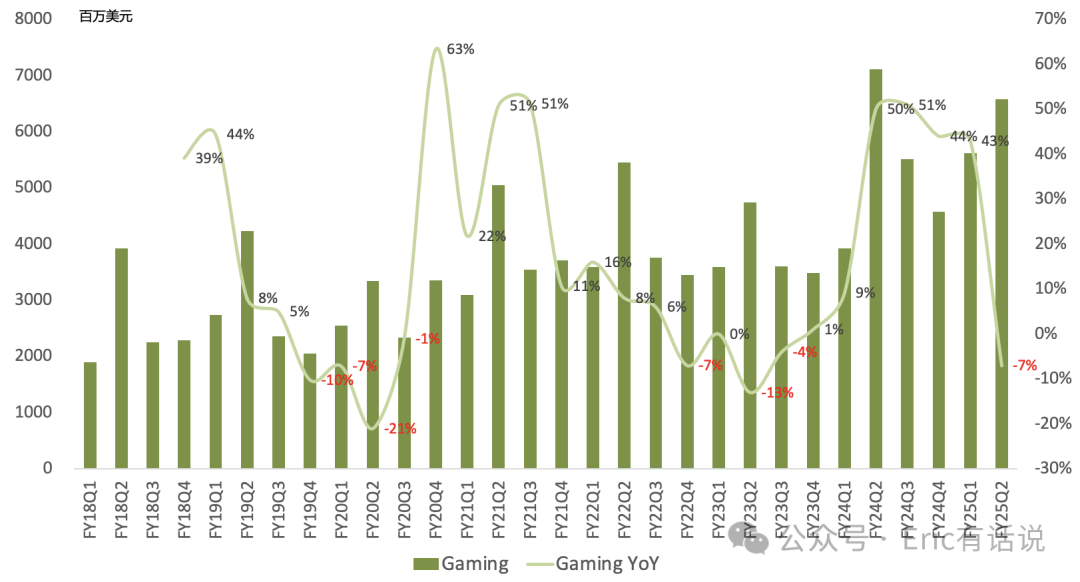

Gaming revenue was $6.6B, down 7% year over year. Xbox hardware revenue down 29% year over year. Software revenue up 2% year over year. Xbox Cloud Gaming hours played hit a new high. Game Pass revenue set a quarterly record. PC Game Pass subscribers up over 30% year over year.

Search advertising revenue was $3.6B, up 21% year over year. Edge and Bing market share continue to rise. Edge U.S. Windows desktop share exceeds 30%, up for 15 consecutive quarters.

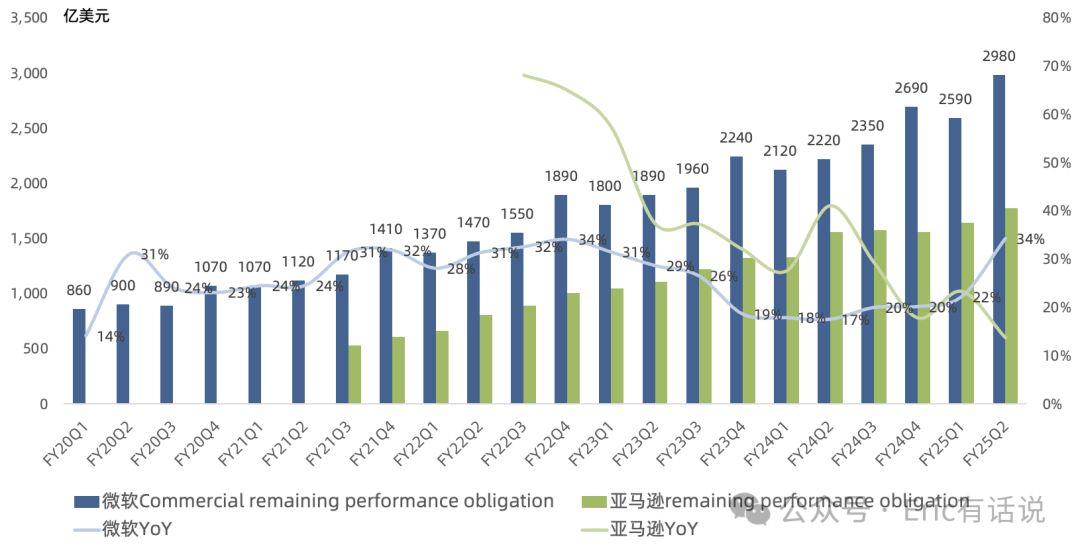

Growth in $100M+ Azure and Microsoft 365 deals drove commitment growth. Commercial RPO was $298B, up 34% year over year. Annuity mix 97%.

FY25Q3 revenue is guided to grow 11% year over year. Operating income is guided to grow 11% year over year. Azure guided to grow 31%-32% year over year. As AI capacity expands, Azure will accelerate. Microsoft 365 guided to grow 14%-15% year over year. LinkedIn guided to grow low-to-mid single digits. Dynamics 365 guided to grow mid-teens. Windows OEM & Devices guided to decline low-to-mid single digits. Search advertising guided to grow mid-teens. Gaming guided to grow low single digits.

This quarter, AI revenue run rate exceeded $13B ($3.3B quarterly), primarily from Azure AI ($1.8B) and M365 Copilot ($1.5B). Copilot business showed strength across new seats, expansion seats, and ARPU. AI has become the fastest-growing business in Microsoft's history.

It is expected that over half of cloud and AI capex is for long-lived assets monetized over 15+ years, with the remainder used to procure servers opportunistically based on customer demand. FY25Q3 and FY25Q4 capex are expected to be similar to this quarter; FY26 capex will continue to grow but at a slower pace, with spending shifting toward servers directly tied to revenue (inference).

Overall, this earnings release continues to highlight the stability of Microsoft's performance. The comprehensive Copilot integration across Microsoft's SaaS products is progressing smoothly, steadily lifting ARPU, following the "decoupling" from OpenAI.

Microsoft's AI dual towers — Azure AI + Copilot — still offer upside, though Wall Street may have limited near-term patience.