Microsoft's FY25Q4 covers April through June 2025.

Microsoft FY2025 Q4 Earnings Summary:

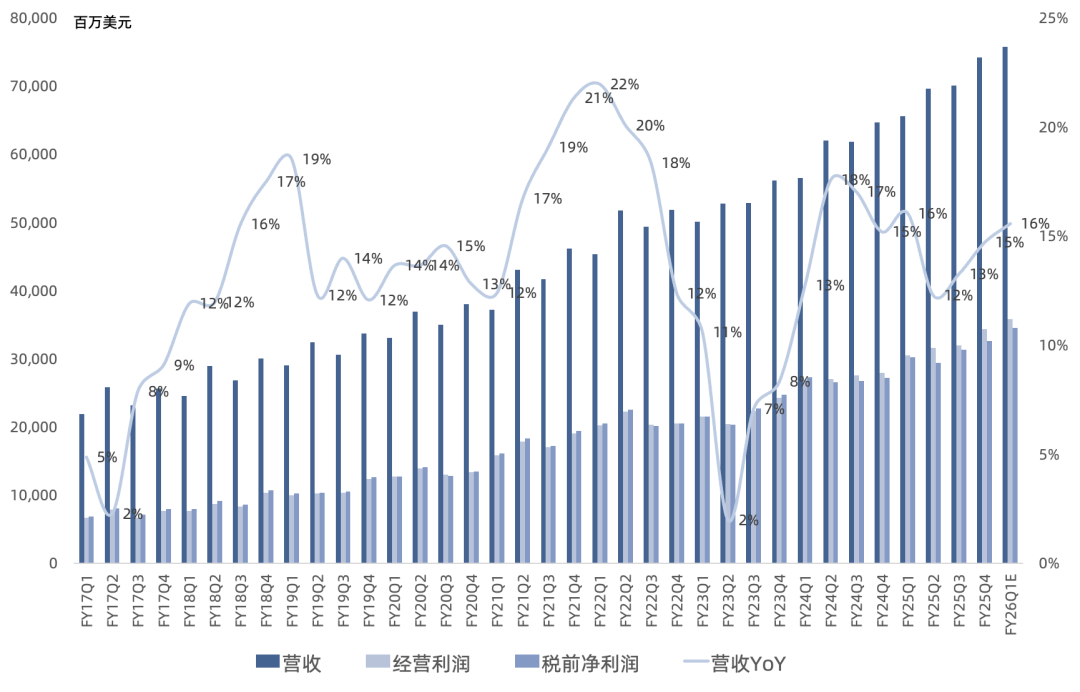

Revenue of $74.3B, up 15% year over year, setting a record for the 5th consecutive quarter with acceleration for the 2nd straight quarter; operating income of $34.3B, up 23% year over year, a record for the 10th consecutive quarter; net income of $27.2B, up 24% year over year, another all-time high.

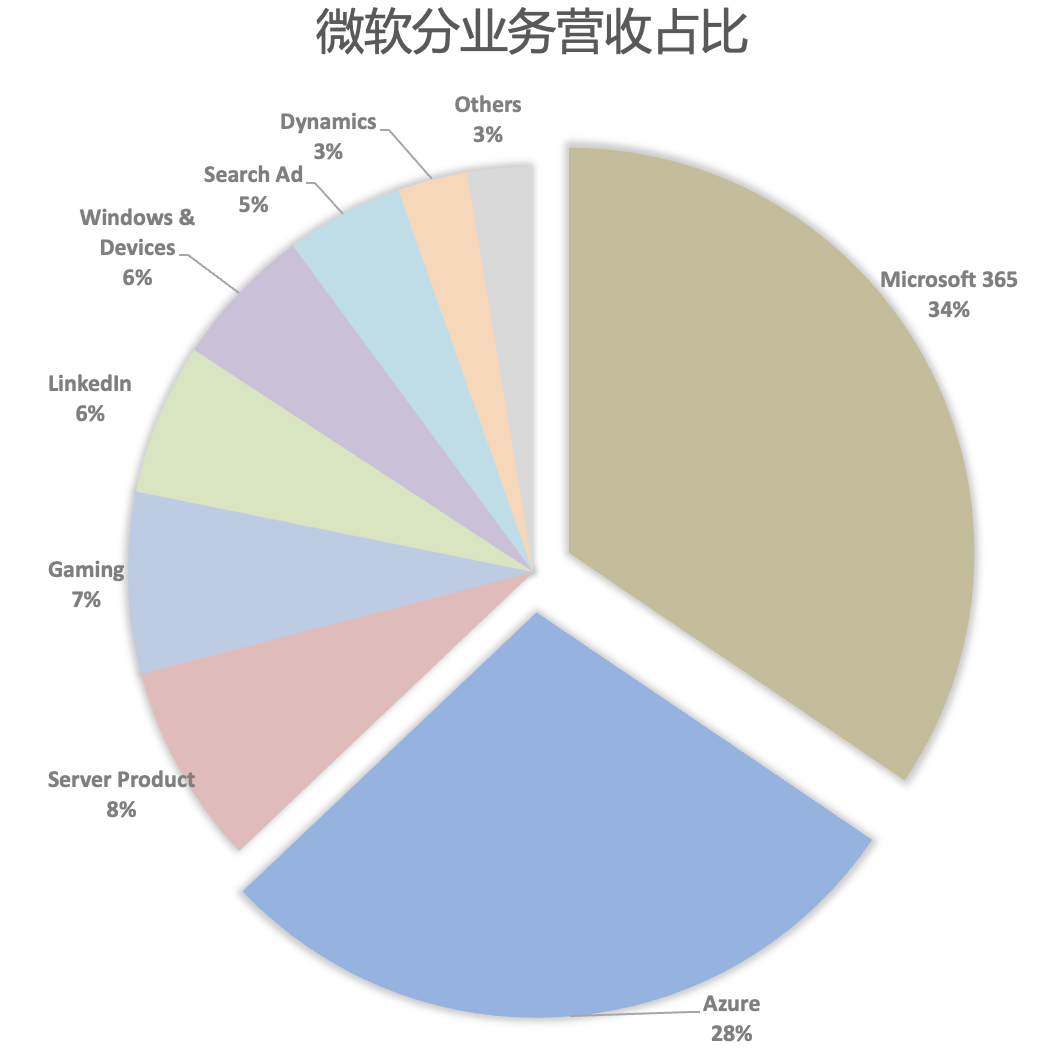

Productivity and Business Processes

Productivity and Business Processes revenue of $33.1B, up 16% year over year, with sequential growth acceleration of 6 percentage points; operating income of $19B, up 21% year over year.

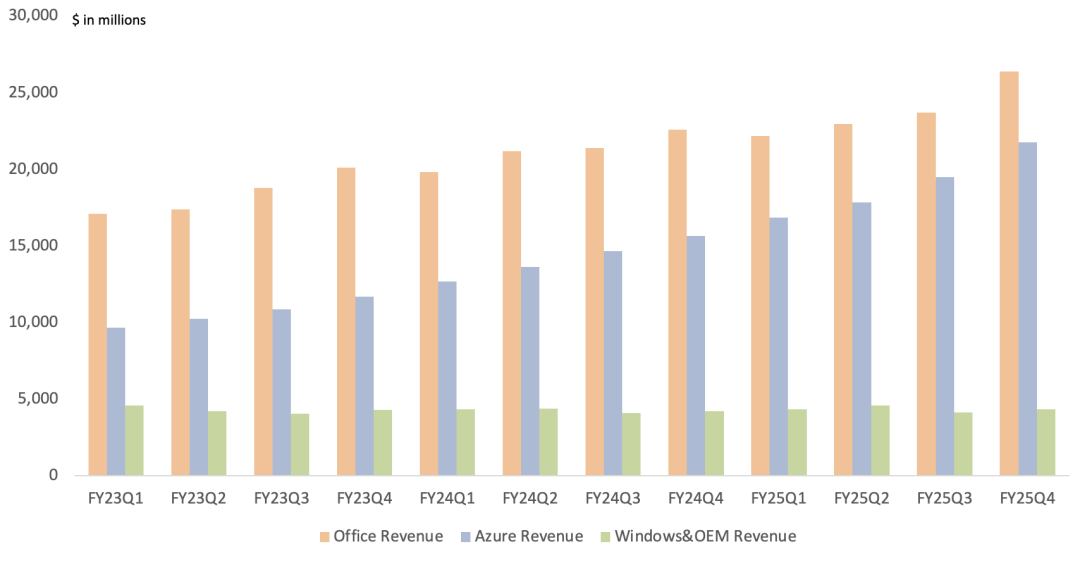

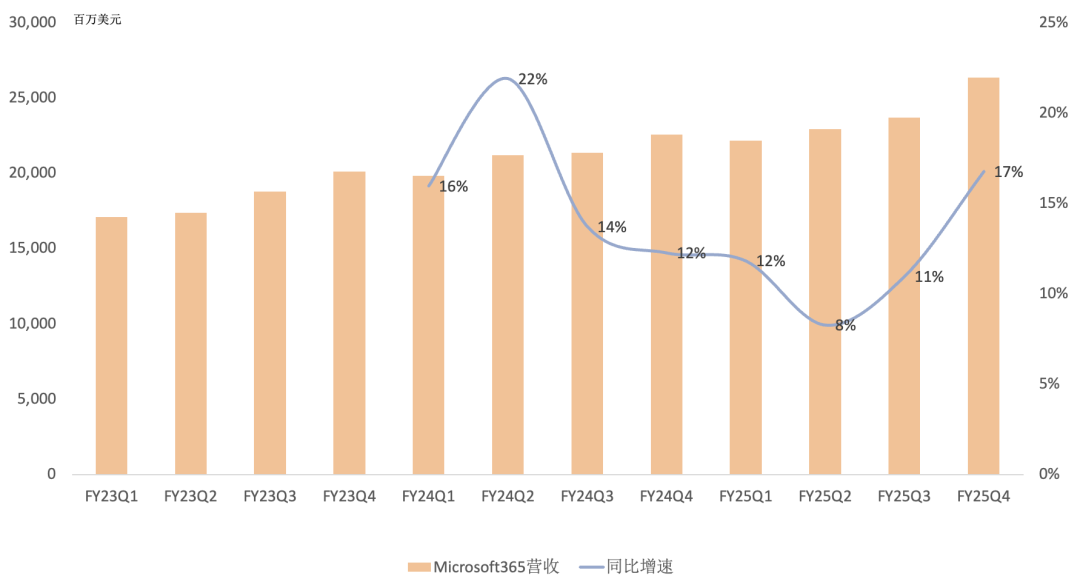

Microsoft 365 revenue of approximately $26.4B, up 17% year over year, with sequential growth acceleration of 6 percentage points; M365 commercial cloud revenue exceeded expectations, up 18% year over year, of which 2 percentage points came from current-period revenue recognition; excluding that impact, the underlying business trend remained relatively stable versus the prior quarter; strong M365 E5 and Copilot demand drove continued ARPU expansion; this quarter's net seat additions set a new high since launch, as did the number of customers buying more seats; customers created 3 million agents using SharePoint and Copilot Studio this fiscal year; in healthcare, DAX Copilot customers logged over 13 million patient encounters with AI solutions, up nearly 7x year over year.

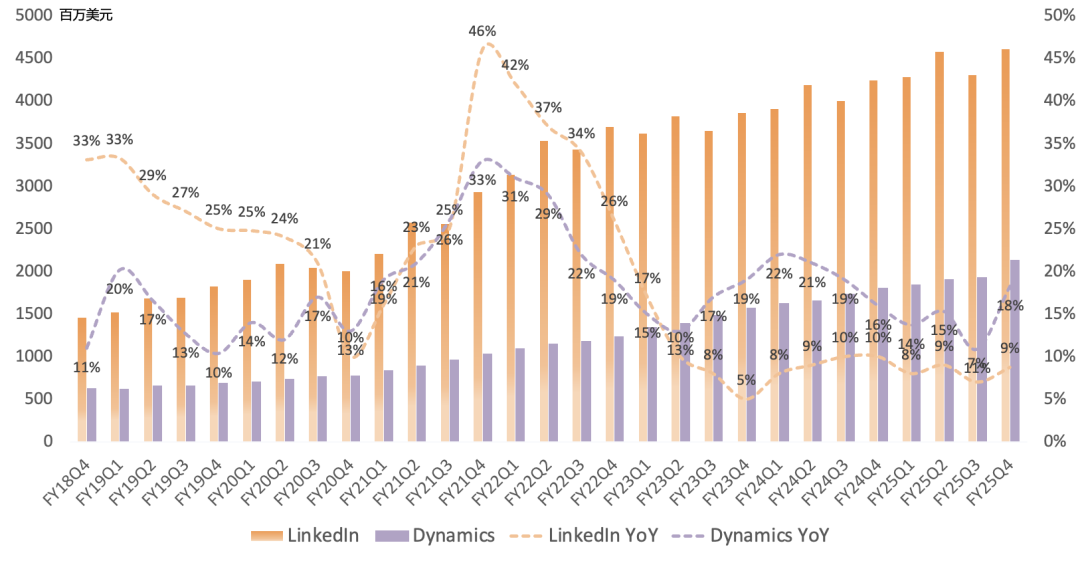

LinkedIn revenue of $4.6B, up 9% year over year; LinkedIn has 1.2 billion members and has delivered double-digit member growth for four consecutive years; all business lines grew, though Talent Solutions continues to be pressured by a soft hiring market.

Dynamics revenue of $2.1B, up 18% year over year; Dynamics 365 revenue up 23% year over year; Dynamics 365 market share continues to rise, with growth across all workloads.

Intelligent Cloud

Intelligent Cloud revenue of $29.9B, up 26% year over year, with sequential growth acceleration of 5 percentage points; operating income of $12.1B, up 23% year over year.

Azure revenue of approximately $21.7B, up 39% year over year, with sequential growth acceleration of 6 percentage points; annualized revenue run rate exceeds $75B, up 34% year over year; both Azure AI and non-AI revenue exceeded expectations this quarter, driven by accelerating core infrastructure growth, primarily from the largest customers (likely OpenAI); AI's contribution to Azure growth was in line with expectations, but no specific percentage was disclosed — possibly because AI customers like OpenAI are now contributing substantial non-AI revenue, making it increasingly difficult to separate AI from non-AI workloads; AI demand grew so rapidly that even with more data centers coming online, the AI capacity shortfall extends into early 2026 (previously expected to persist only after June); Azure AI Foundry processed over 5 quadrillion tokens this fiscal year, up 7x year over year; 80% of Fortune 500 companies are using Azure AI Foundry.

Microsoft now operates over 400 data centers across 70 global regions, more than any other CSP; all regions now support liquid cooling; in the past 12 months alone, over 2 GW of new capacity was added; this quarter Microsoft launched its Sovereign Cloud, spanning public and private cloud deployments; cloud migration continues to accelerate; Azure's three growth drivers: cloud migration + cloud-native SaaS scale expansion + AI.

Microsoft Fabric is becoming the complete data and analytics platform for the AI era, covering everything from SQL to NoSQL to analytics workloads; revenue up 55% year over year, with over 25,000 paying customers (up from 21,000 last quarter), making it the fastest-growing database product in Microsoft history; Azure Databricks and Snowflake on Azure also accelerated; adoption of the new Foundry Agent Service is accelerating, with 14,000 customers now using it to build agents that automate complex tasks; GitHub Copilot users exceed 20 million (up from 15 million last quarter), enterprise customers up 75% sequentially, and 90% of the Fortune 100 use GitHub Copilot.

Security customers near 1.5 million (up from 1.4 million last quarter); Entra now extends identity, policy, and access control to agents; Defender secures nearly 2 million GenAI applications.

More Personal Computing

PC revenue of $13.5B, up 9% year over year; operating income of $3.2B, up 34% year over year.

Windows & Devices revenue of $4.3B, up 2% year over year; Windows 10 support ends in October.

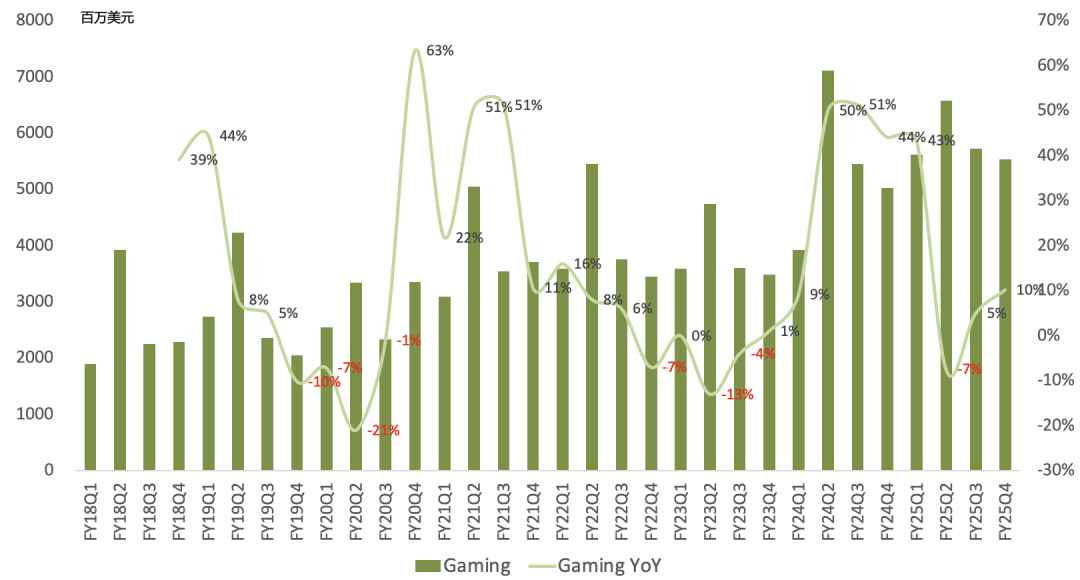

Gaming revenue of $5.5B, up 10% year over year; Xbox hardware revenue down 22% year over year, software revenue up 13%; gaming MAU exceeds 500 million; Microsoft is now a top publisher on both Xbox and PlayStation; Call of Duty: Black Ops 6 has reached 50 million players with over 2 billion total hours played; the Minecraft movie's success drove the game's MAU and revenue to all-time highs this quarter; cloud-streamed gaming hours surpassed 500 million; Game Pass annual revenue approached $5B for the first time.

Search advertising revenue of $3.6B, up 21% year over year.

Earnings Call Highlights

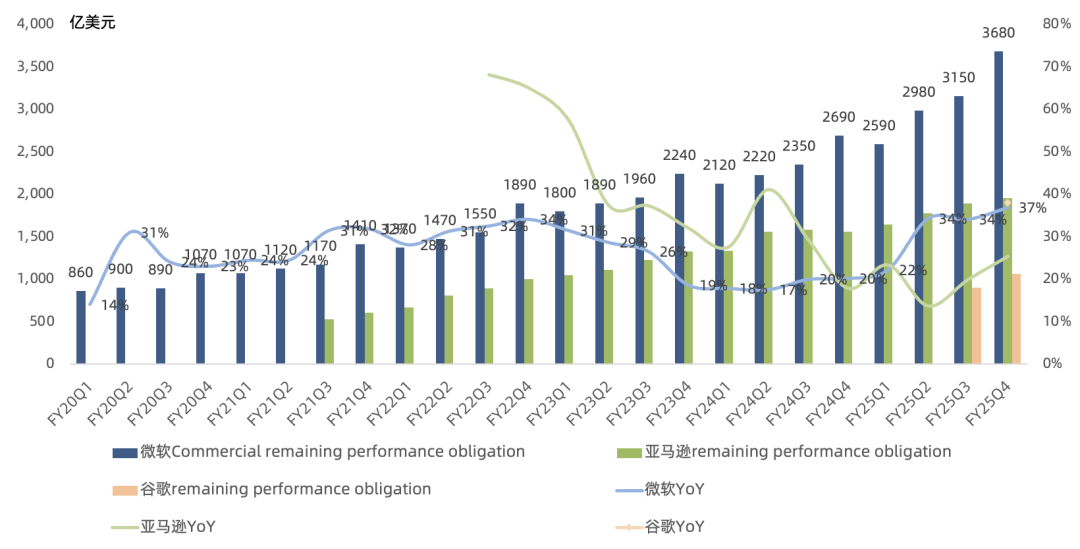

The number of Azure and Microsoft 365 contracts worth tens of millions and hundreds of millions of dollars increased, driving commitments to new highs; commercial RPO of $368B, up 37% year over year and up $53B sequentially, an all-time high; annuity mix of 98%.

Guiding FY26 Q1 revenue growth of 16% year over year, marking the 3rd consecutive quarter of sequential acceleration; operating income growth of 17% year over year; Azure growth of 37% year over year; M365 commercial cloud growth of 13%-14%, consumer cloud growth in the low-teens; LinkedIn growth in the high single digits; Dynamics 365 growth in the high-teens; Windows OEM & Devices decline in the mid-to-high single digits; search advertising growth in the low-to-mid-teens; gaming revenue growth in the mid-to-high single digits.

Over half of cloud and AI capex supports long-lived assets monetized over 15+ years; the remainder goes to servers, including CPUs and GPUs, driven by strong demand signals; expecting FY26 Q1 capex above $30B; FY26 full-year capex trend consistent with Q1; FY26 overall capex growth slows versus FY25 but far exceeds the previous full-year $80B guidance from Nadella.

FY26 full-year guidance: Revenue up double digits year over year. Operating income up double digits year over year. Operating margin flat.

Overall, this report again highlights the resilience of Microsoft's business model, especially against a backdrop of intense capital spending. The Copilot-ification of Microsoft's SaaS portfolio is progressing well, steadily lifting ARPU; OpenAI has grown from contributing only cloud AI revenue to now contributing substantial cloud non-AI revenue, becoming a secret weapon for Azure to overtake AWS in the AI era. Future negotiations with Azure will be critical for Microsoft, and the power dynamic between the two has subtly shifted.

This quarter also saw a dramatic shift among the cloud big three: Microsoft Azure benefits from OpenAI, Google Cloud benefits from Gemini and a large OpenAI deal, while AWS — backed by Anthropic's Claude — posted middling results, raising concerns that Amazon will continue to lose share in the GenAI era.

Microsoft's AI dual-tower strategy has shifted from Azure AI + Copilot to Azure + Copilot.