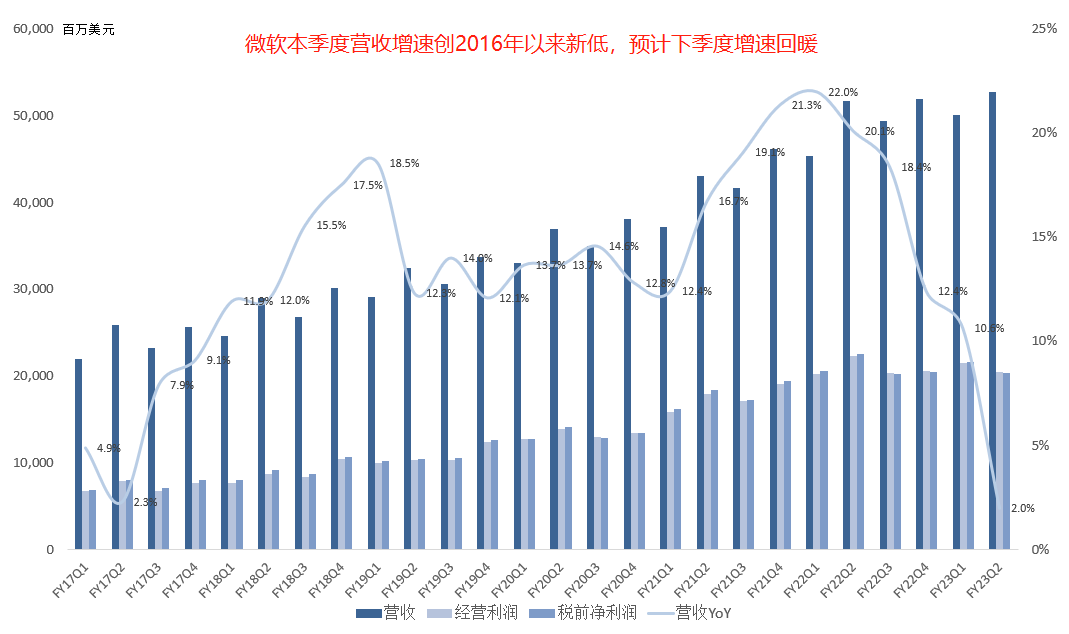

Microsoft FY2023 Q2 Earnings Summary:

Revenue $52.747B, up 2% year over year, a record high, but growth slowest since 2017; FX impact 5 points; operating income $20.399B, down 8.3% year over year, first decline since 2017; net income $16.425B, down 12.5% year over year, second consecutive quarterly decline.

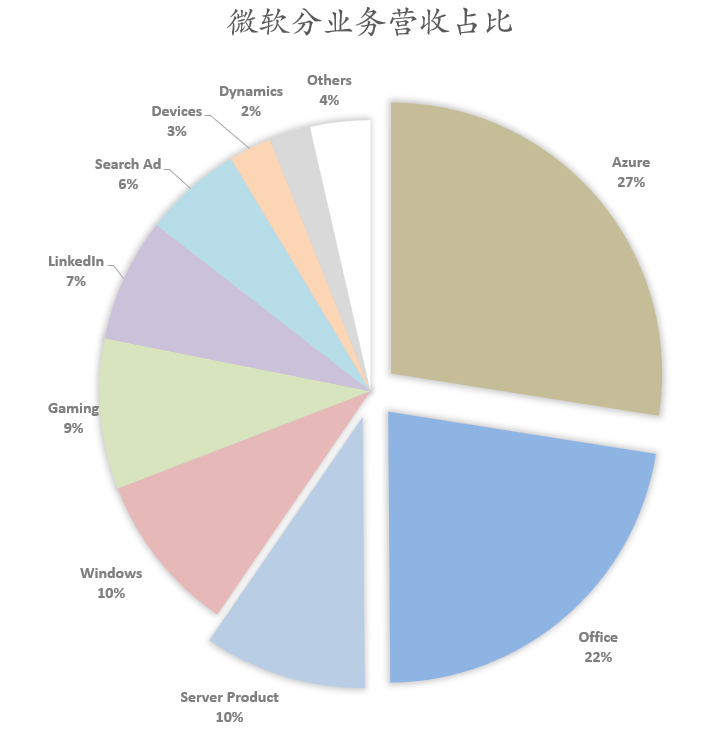

Productivity & Business Processes revenue $17.0B, up 7% year over year; operating income $8.2B, up 6% year over year;

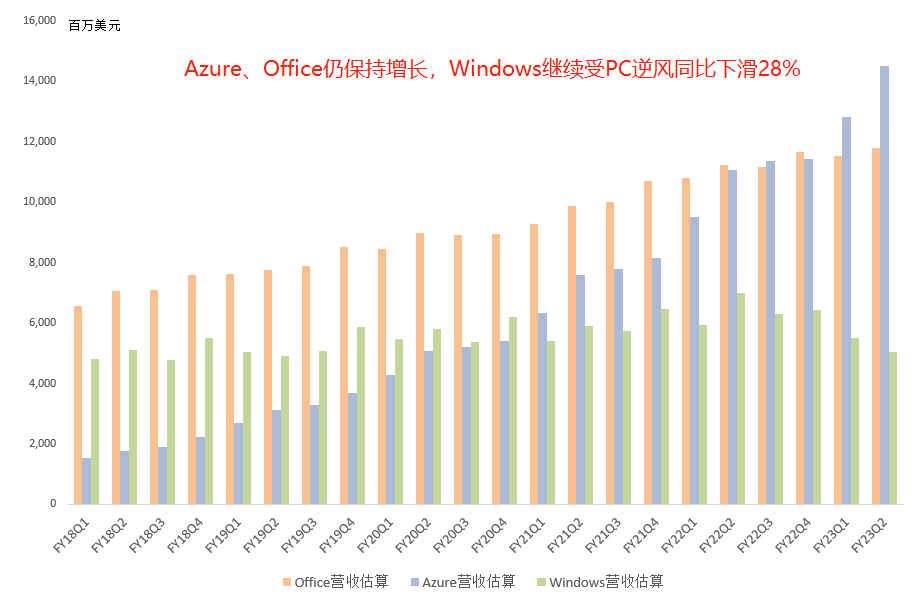

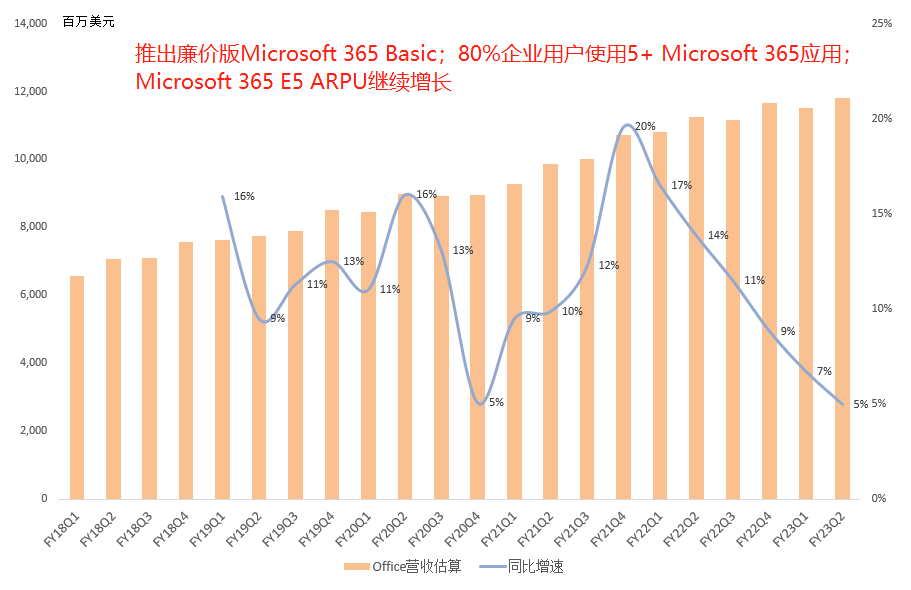

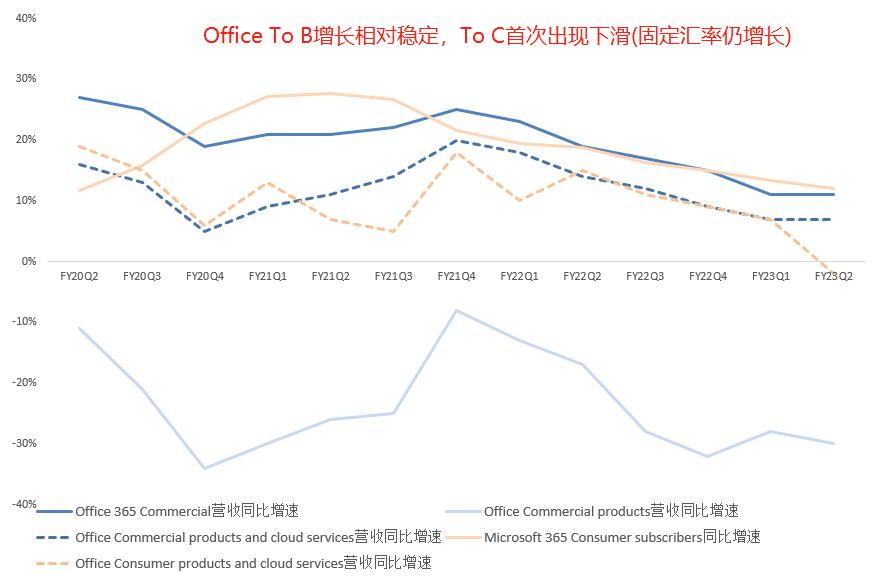

Office revenue ~$11.8B, up 5% year over year; newly launched low-cost Microsoft 365 Basic; clear trend of Office E3 migrating to E5, E5 ARPU still rising; 80% of enterprise customers use 5+ Microsoft 365 apps; Teams MAU surpassed 280M; Teams Rooms active devices >500K, up 70% year over year; customers with >1,000 rooms doubled year over year; Security business TTM revenue >$20B; customers with 4+ workloads up 40% year over year;

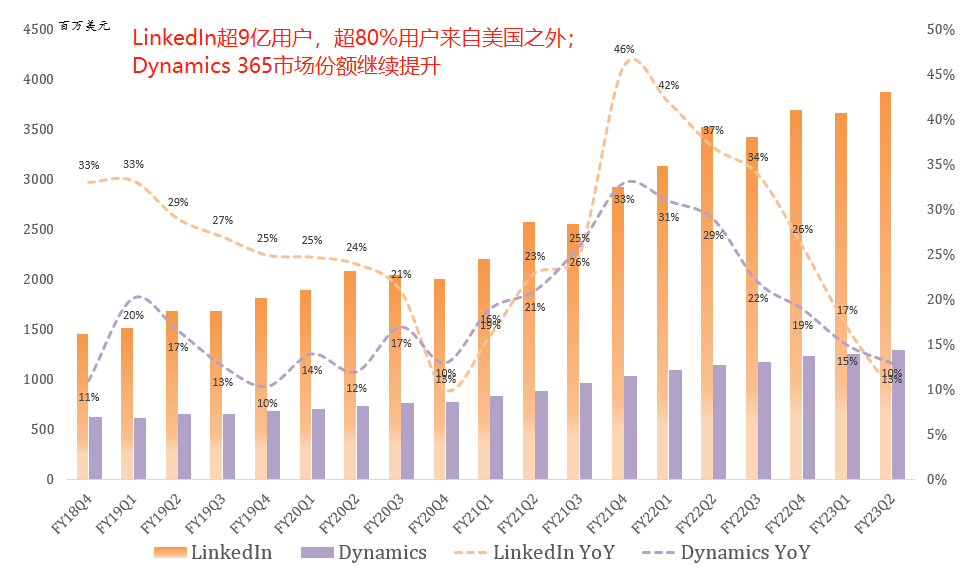

LinkedIn revenue $3.9B, up 10% year over year, a record high; LinkedIn >900M users, >80% outside the US;

Dynamics revenue $1.3B, up 13% year over year, another record; Dynamics 365 steadily gaining share; Power Automate >45K users, up >50% year over year;

Intelligent Cloud revenue $21.5B, up 17% year over year, third consecutive quarter above $20B; operating income $8.9B, up 9% year over year;

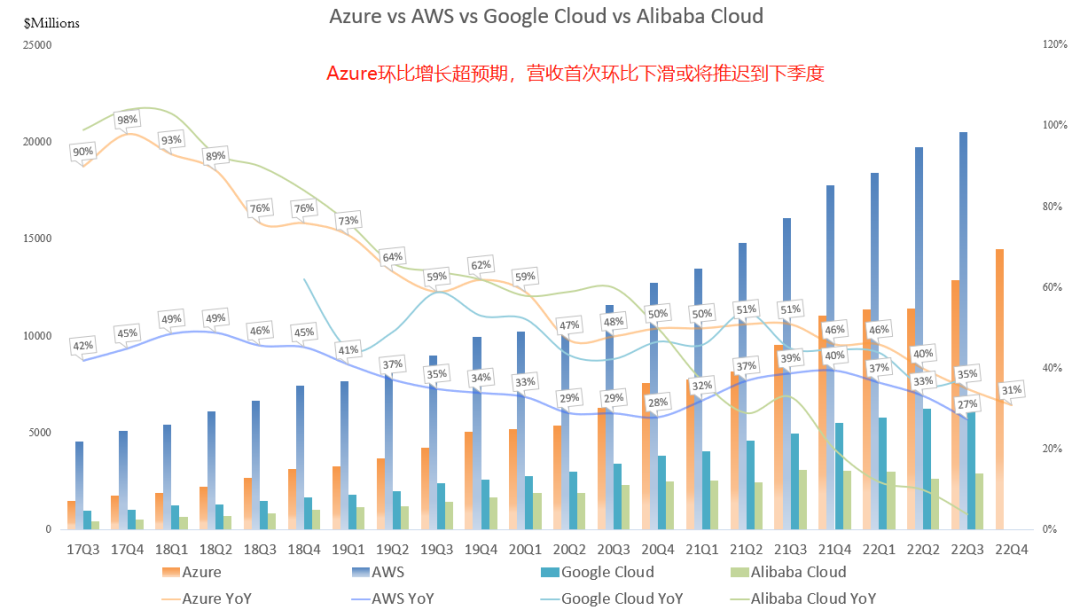

Azure revenue ~$14.5B, up 31% year over year, FX impact 7 points; Azure Arc now >12K customers, doubled year over year; Azure OpenAI Service launched, ChatGPT coming soon; Microsoft is OpenAI's exclusive cloud provider; Azure ML revenue doubled year over year for fifth consecutive quarter; GitHub >100M active developers, Copilot >1M users; Duolingo, Lemonade, Volkswagen's CARIAD adopting Copilot;

Notably, Microsoft guided for Azure Q3 revenue to decline 4%-5% sequentially on a constant-currency basis, which would be Azure's first sequential revenue decline.

Microsoft explained last quarter: backlog keeps hitting new highs, but quarterly conversion can be more volatile. In today's macro, a consumption-based cloud model naturally sees usage drop when business activity slows, as customers use less or optimize spend.

More Personal Computing revenue $14.2B, down 18% year over year; operating income $3.3B, down 48% year over year;

Windows revenue ~$5.0B, down 28% year over year; monthly active Windows devices 10% above pre-pandemic; Win11 enterprise penetration still rising; Windows 365 and Azure Virtual Desktop usage up 2/3 year over year;

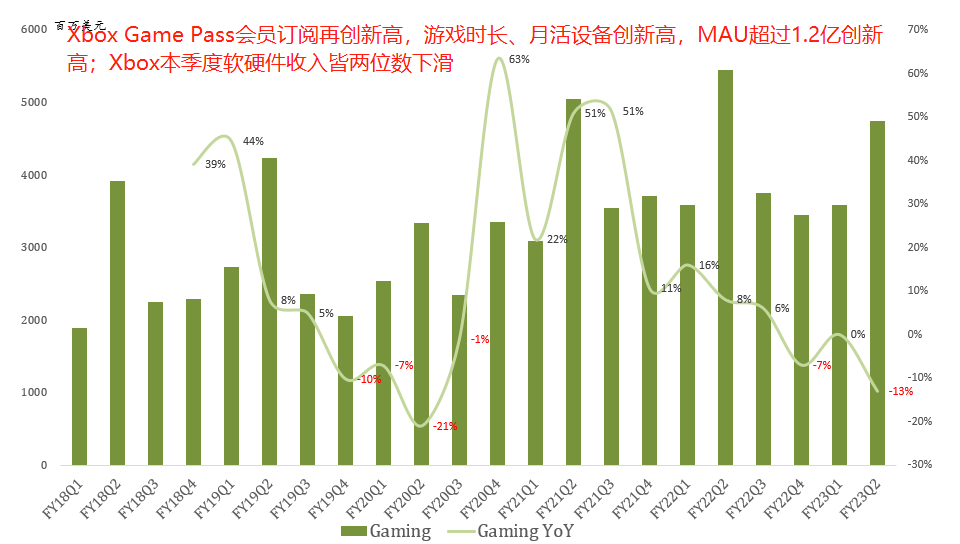

Gaming revenue $4.7B, down 13% year over year; Xbox hardware down 13% year over year, content & services down 12% year over year; Xbox Game Pass subscriptions new high; engagement hours, monthly active devices new high; MAU >120M new high;

Search & news advertising revenue $3.1B, up 10% year over year; Edge share up for seventh consecutive quarter; Bing US share also rising; Start personalized content DAU up 30%+; Xandr contributed 6% of advertising.

Devices revenue $1.3B, down 39% year over year, hit by weak consumer electronics.

Given PC market uncertainty, Microsoft did not give full-year revenue guidance; expects FY23 operating income down 2% year over year; broader commercial business up 20% year over year. Commercial remaining performance obligation increased 29% to $189B. Roughly 45% will be recognized in revenue in the next 12 months, up 24% year over year. The portion recognized beyond 12 months increased 32%.

This quarter FX impacted revenue growth by 5 points, operating income growth by 9 points; expects FX impact of 3 points on next quarter's revenue growth. FY23 Q3 revenue guidance implies 4% year-over-year growth.

ChatGPT has exploded recently; Microsoft, a long-time NLP investor, has partnered with OpenAI for nearly four years. So Microsoft's announcement to integrate ChatGPT across all products is no surprise. Azure OpenAI Service is live, ChatGPT coming soon; Microsoft naturally becomes OpenAI's exclusive cloud provider. And the flagship Office + ChatGPT synergy is powerful—Bing might even get a lift from ChatGPT.

Although the near-term global economic outlook is challenging, long term, as Nadella said, 'global digital spend/GDP' is still small; we are in the early stages of global digitalization, and Microsoft is the global digitalization leader. Microsoft's biggest future catalyst is how far it can commercialize these AI technologies and what synergies they create with the Azure/Office/Windows flywheel. Looking forward to Microsoft becoming a true AIaaS company.

*All segment revenue figures above are estimates.