Microsoft FY2024 Q2 earnings summary:

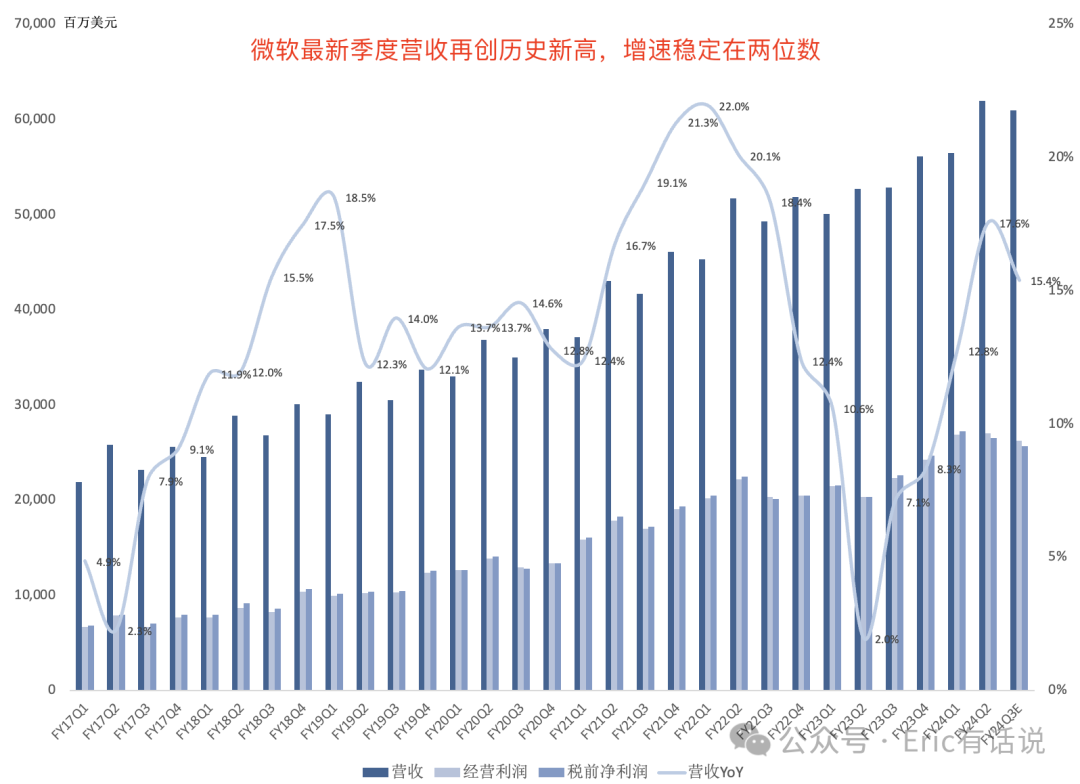

Revenue was $62.002B, up 18% year over year, a record for the fifth consecutive quarter with accelerating year-over-year growth; operating income was $27.032B, up 33% year over year, a record for the fourth consecutive quarter; net income was $21.87B, up 33% year over year.

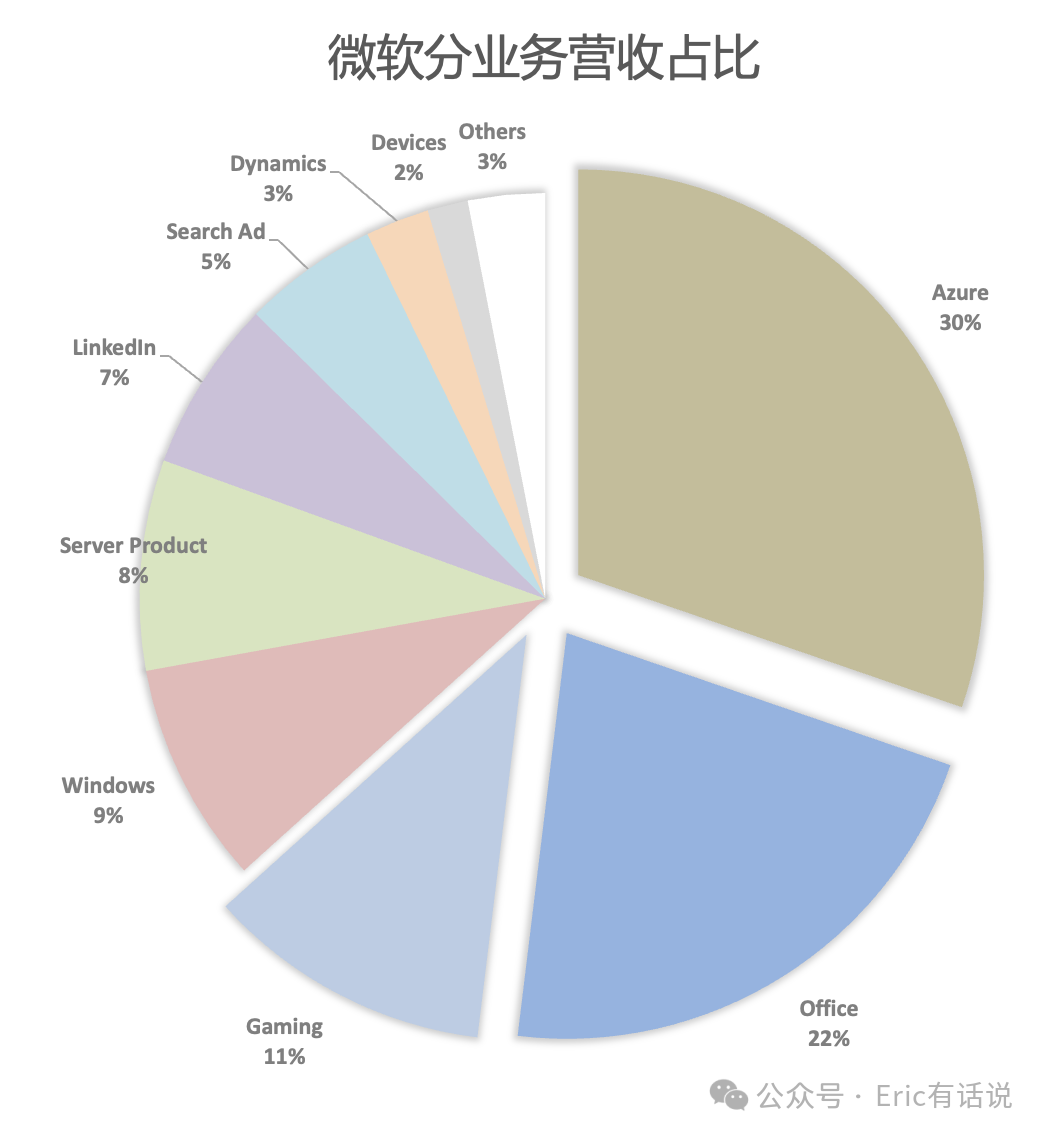

Productivity and Business Processes revenue was $19.2B, up 13% year over year; operating income was $10.3B, up 26% year over year, a new record.

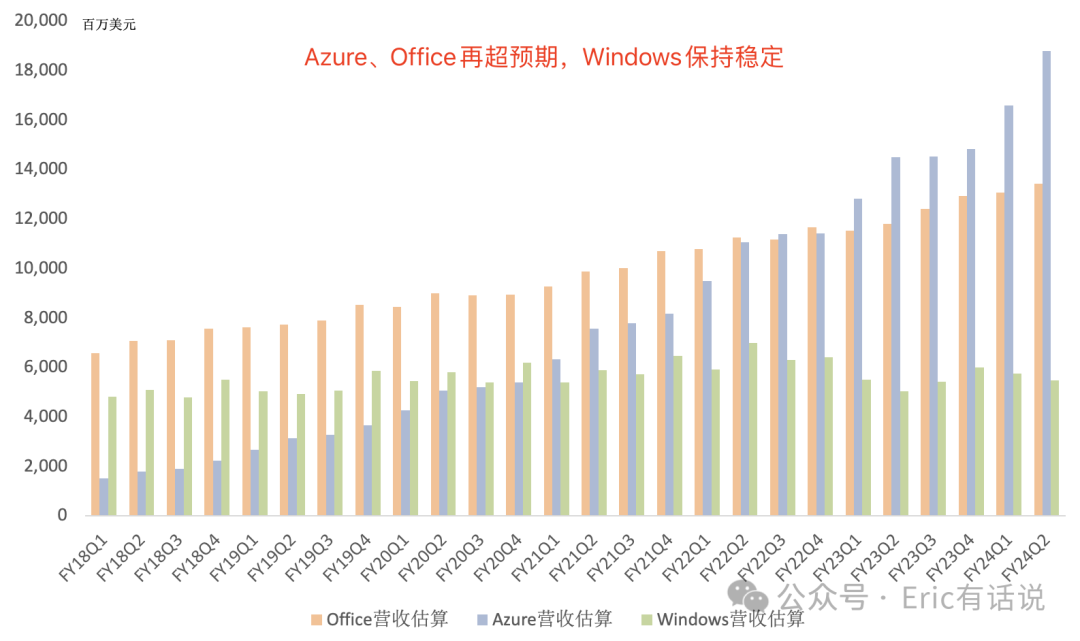

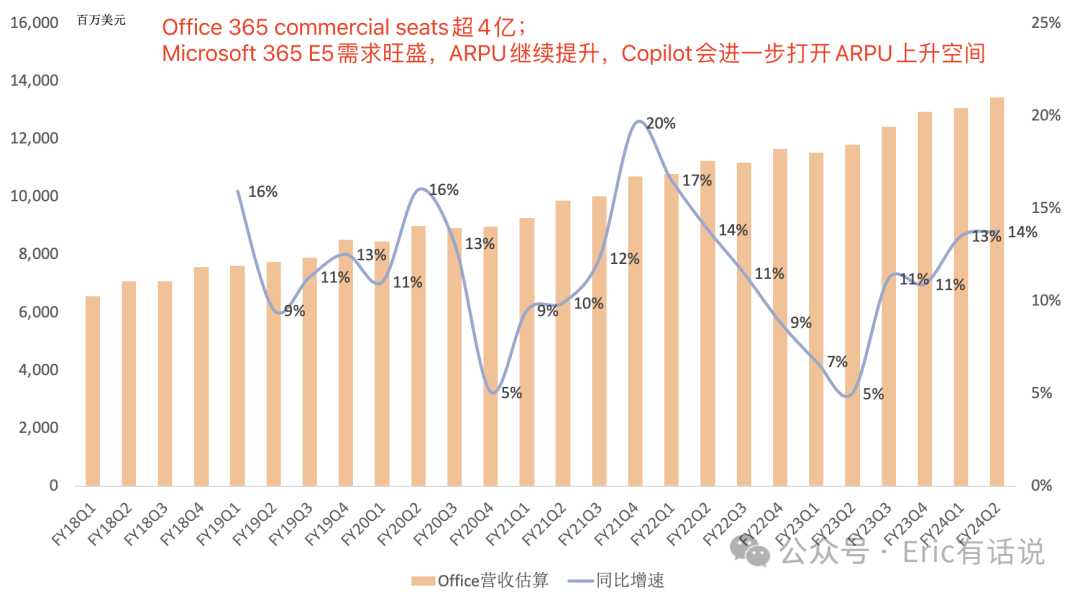

Office revenue was approximately $13.4B, up 14% year over year; Office 365 commercial seats exceed 400M; Microsoft 365 E5 demand is strong, ARPU continues to rise, and Copilot will further expand ARPU upside; Microsoft 365 Copilot adoption exceeds expectations; Copilot Pro subscription launched for individuals and families; Teams usage hits a new high; over two-thirds of enterprise customers purchase Phone, Rooms, and Premium services.

Security business has over 1M enterprise customers, with over 700K using four or more products/services.

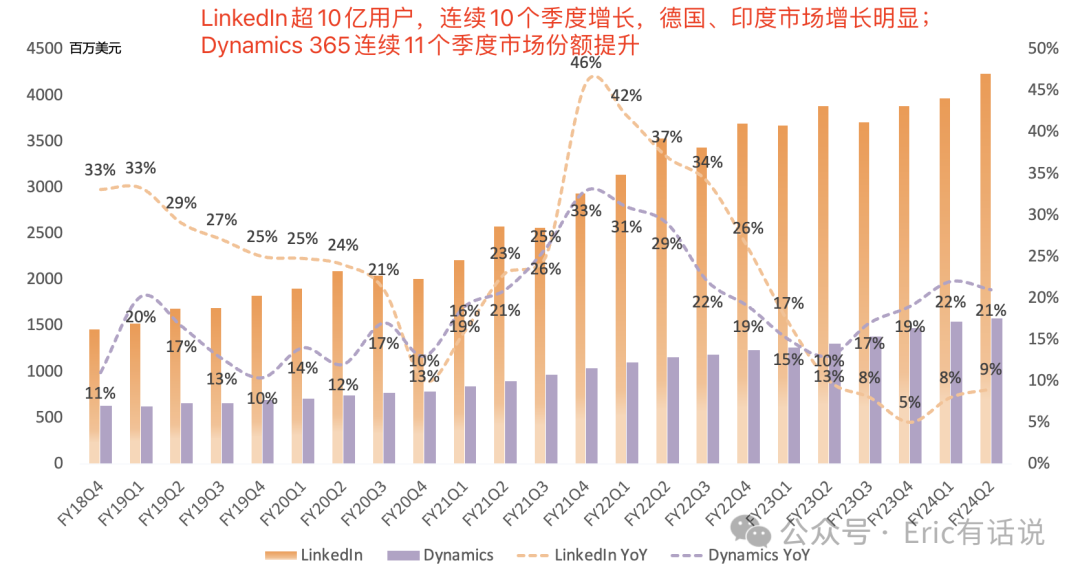

LinkedIn revenue was $4.2B, up 9% year over year; LinkedIn exceeds 1B users, growing for 10 consecutive quarters, with notable growth in Germany and India.

Dynamics revenue was $1.6B, up 21% year over year, a record for the fourth consecutive quarter; Dynamics 365 market share has risen for 11 consecutive quarters; over 230K companies have used AI features in Power Platform, up 80%+ sequentially; custom Copilot Studio now used by over 10K companies.

Intelligent Cloud revenue was $25.9B, up 20% year over year; operating income was $12.5B, up 40% year over year, a new record.

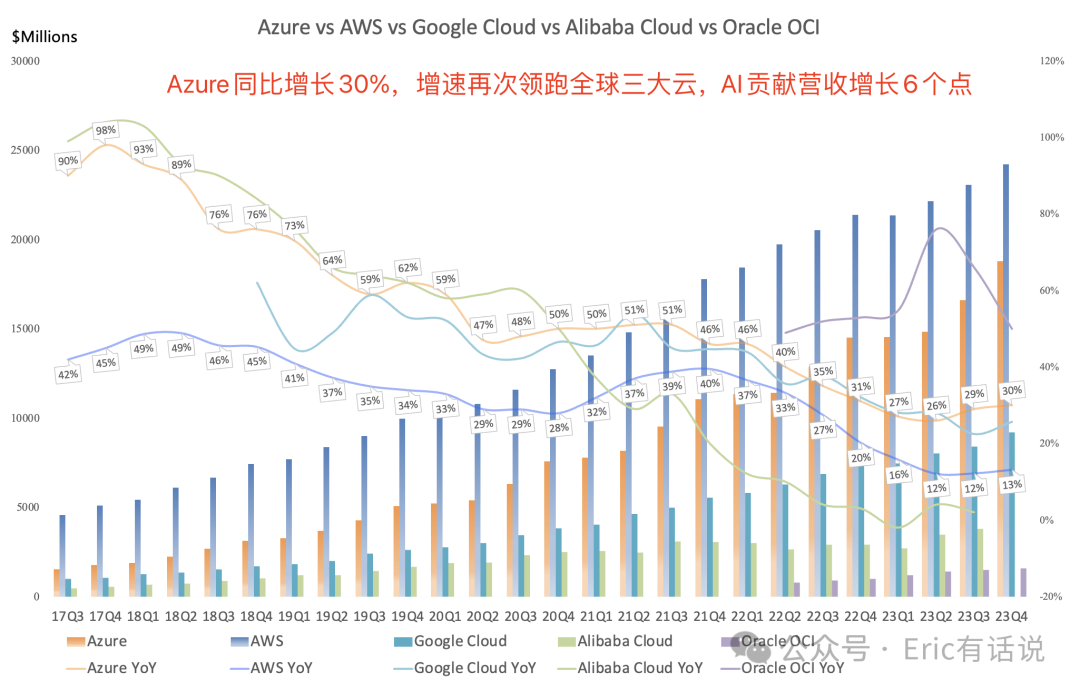

Azure revenue was approximately $18.8B, up 30% year over year; AI contributed 6 percentage points to growth (from ~$400M to ~$900M sequentially); Azure market share continues to rise; Azure AI customers exceed 53,000, over one-third are new customers; MaaS (Models as a Service) showing early traction; over half of Fortune 500 companies use Azure OpenAI Service; Azure $1B+ large deals continue to grow, including a Vodafone 10-year $1.5B deal this quarter; management noted Azure's AI services are predominantly inference, with minimal training involvement.

Cosmos DB data transactions grew 42% year over year; Microsoft Fabric's OneLake data storage grew 46% sequentially; GitHub revenue grew 40%+ year over year; GitHub Copilot paid subscribers exceed 1.3M, up 30% sequentially; over 50K enterprises use GitHub Copilot for Business.

More Personal Computing revenue was $16.9B, up 19% year over year; operating income was $4.3B, up 29% year over year.

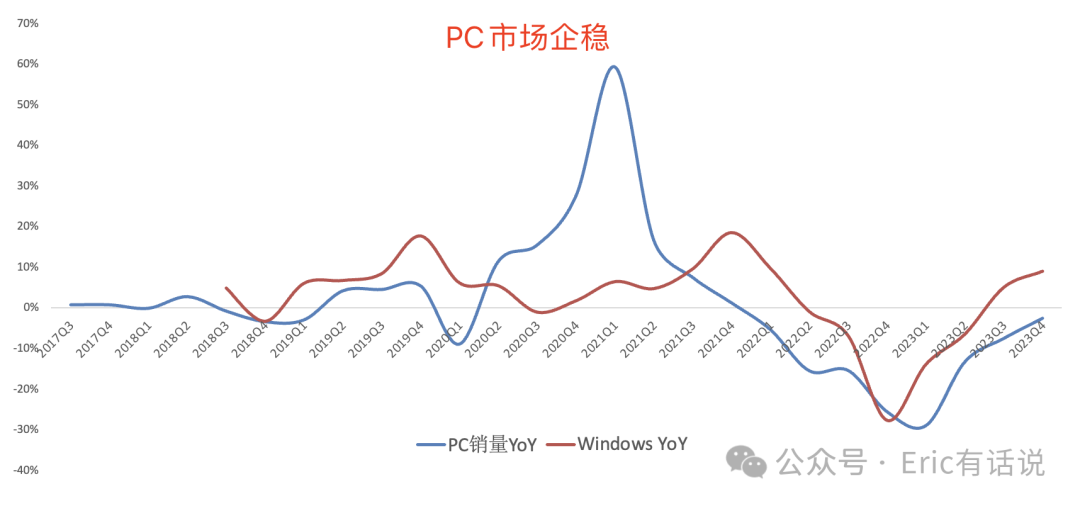

Windows revenue was approximately $5.5B, up 9% year over year, as the PC market continued to stabilize; Copilot in Windows has reached more than 75M Windows 10/11 PCs; Windows 365 Cloud PC usage grew 50%+ year over year; Win11 commercial deployments doubled year over year.

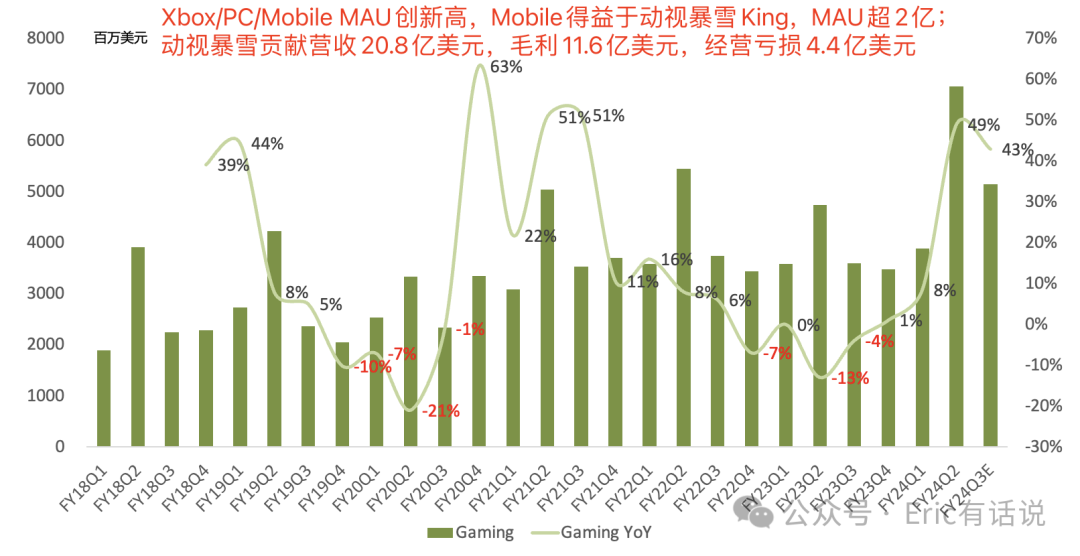

Gaming revenue was $7.1B, up 49% year over year; Xbox hardware revenue rose 3% year over year, while software revenue surged 61% year over year; Xbox/PC/Mobile MAU hit a new high, with Mobile MAU exceeding 200M, benefiting from Activision Blizzard King; Activision Blizzard contributed $2.08B in revenue, $1.16B in gross profit, and a $440M operating loss; Activision Blizzard will impact next quarter by $700M in COGS and $300M in OPEX; cloud gaming hours played grew 44% year over year; the console market showed some softness.

Search advertising revenue was approximately $3.4B, up 8% year over year; Edge browser has gained market share for 11 consecutive quarters, and Bing market share is also rising.

Devices revenue declined 9% year over year.

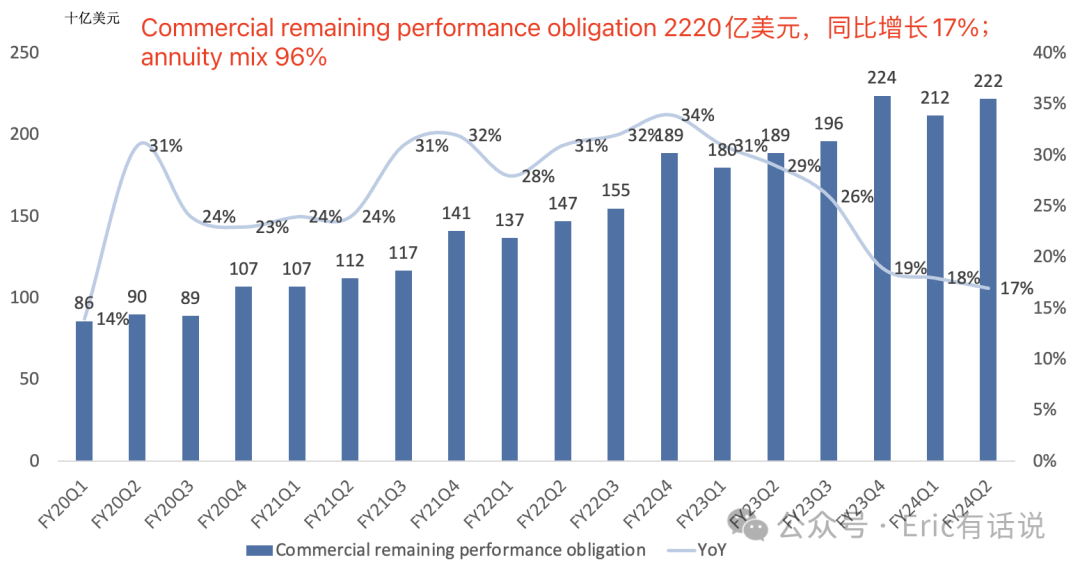

Commercial remaining performance obligation increased 17% to $222 billion . Roughly 45% will be recognized in revenue in the next 12 months, up 15% year-over-year. The remaining portion, which will be recognized beyond the next 12 months, increased 19%.

Guides FY24Q3 revenue up 15% year over year, net income up 15% year over year; Azure up 30% year over year, with AI contribution continuing to increase; Office 365 up 15% year over year; gaming revenue up 40%+ year over year, of which 45% comes from Activision Blizzard; next quarter capex will increase significantly sequentially, still directed at AI servers, and subsequent capex may fluctuate due to timing differences in data center deployments; expects FY24 full-year operating margin to expand 1-2 percentage points year over year.

Overall, this earnings report once again highlighted the stability of Microsoft's performance, with Azure beating expectations again and delivering AI results ahead of Office. Office Copilot monetization will further open up ARPU upside for Microsoft 365, and Microsoft reiterated that its current ARPU remains low relative to the industry, leaving substantial room for growth.

The margin improvement this quarter again came as a surprise; even Wall Street was astonished that massive AI spending has not materially dented profits, and Microsoft remains committed to aggressively investing in AI servers.

My long-term view on Microsoft remains unchanged: the key question is how far Microsoft can commercialize these AI technologies and what degree of synergy they can generate across the Azure/Office/Windows three-engine flywheel.

Microsoft's AI business model is now mature and clear: Azure provides AI MaaS while simultaneously increasing cloud market share, and Copilot opens ARPU upside for Microsoft's SaaS business. As the leader in AI commercialization, we look forward to more surprises from Microsoft.

*All segment revenue figures above are estimates.