Microsoft FY2024 Q1 Earnings Summary:

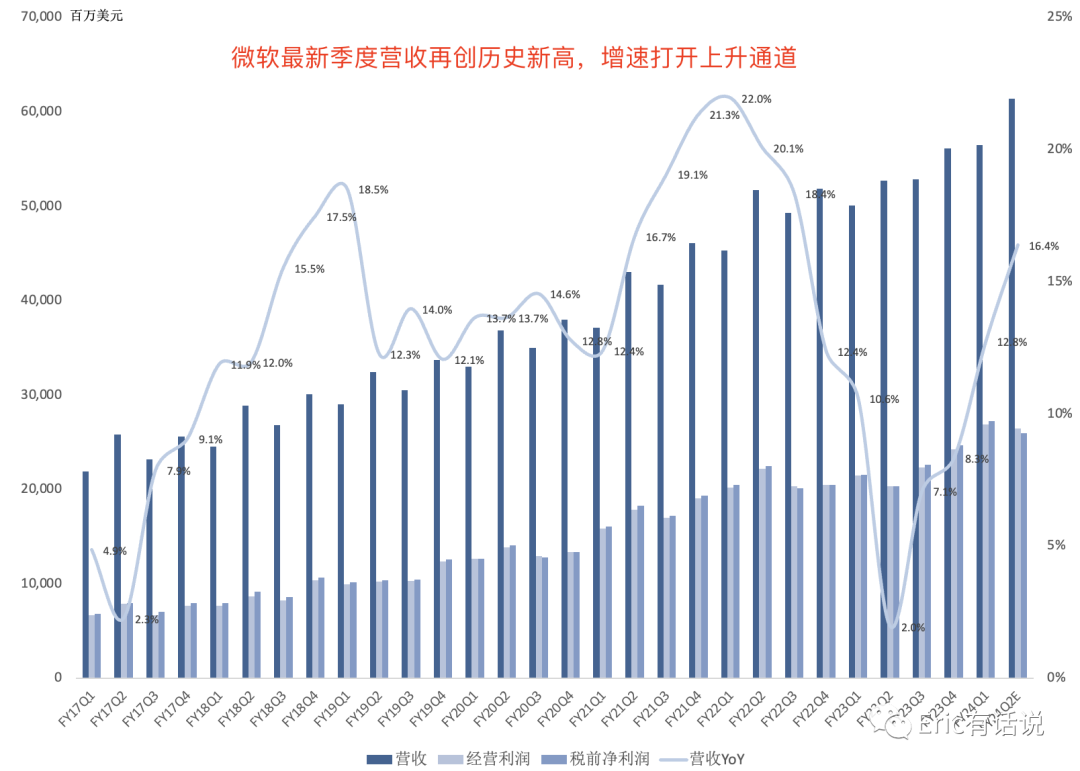

Revenue rose 13% to a fourth straight record of $56.517B, operating income increased 25% to $26.895B, and net income climbed 27% to $22.291B.

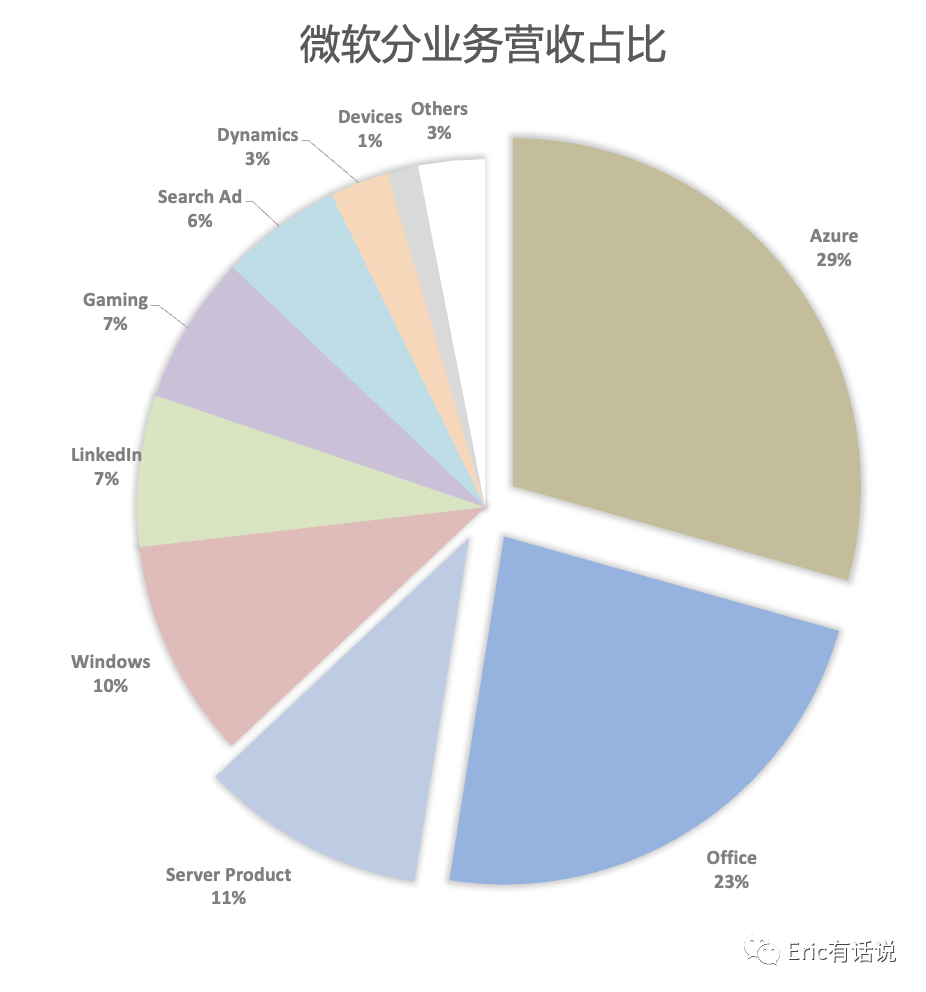

Productivity and Business Processes revenue was $18.6B, up 13% year over year; operating income was $10B, up 20% year over year, setting a new historical high.

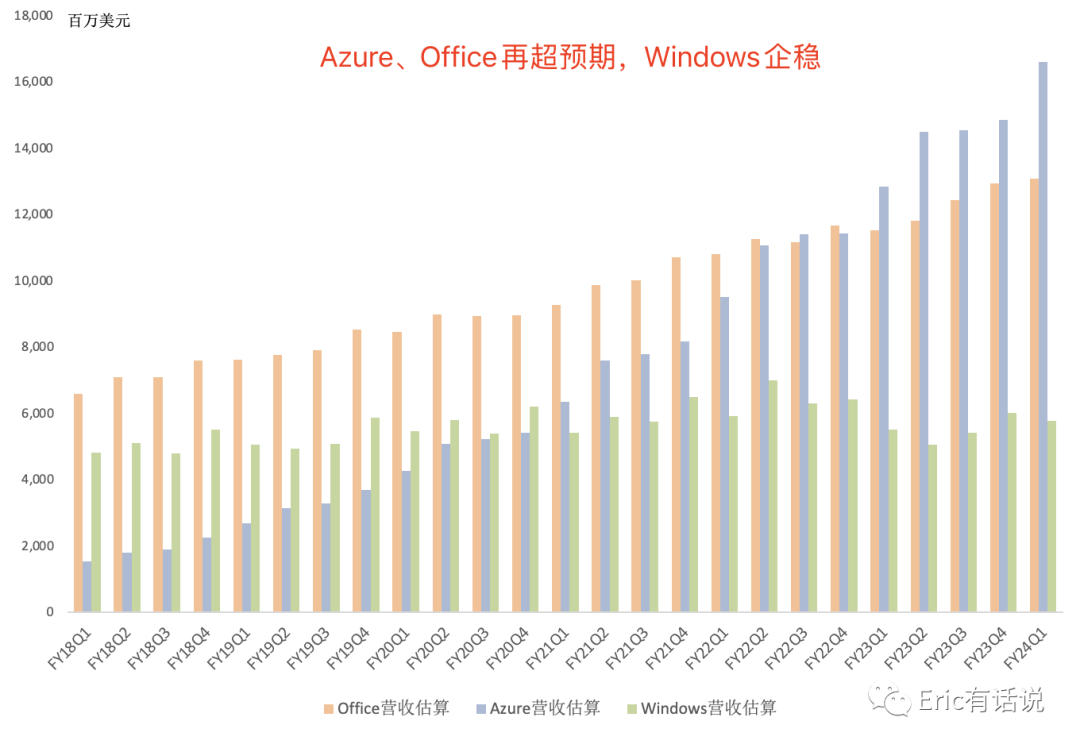

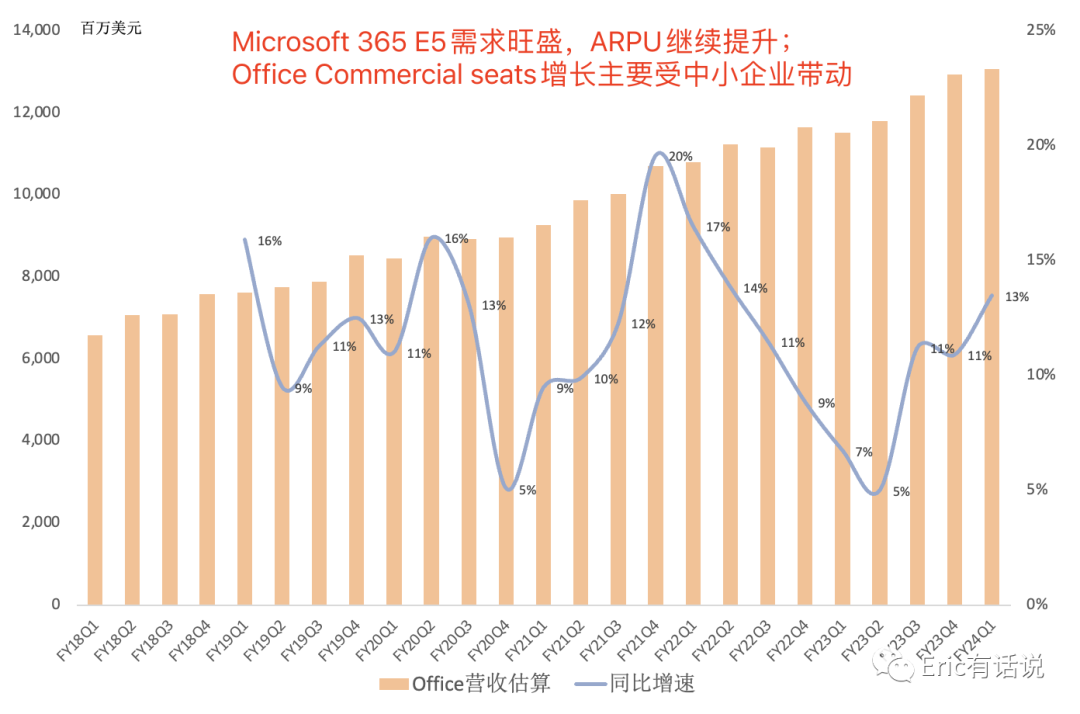

Office revenue was ~$13.1B, up 13% year over year; E5 demand exceeded expectations, ARPU continues to rise, commercial seat growth driven mainly by SMBs; Microsoft 365 Copilot has been tested by tens of thousands of employees at 40% of Fortune 100 customers, will be generally available on November 1, gradually contributing revenue; Teams MAU exceeds 320M, Teams Rooms revenue up triple digits year over year for 9 consecutive quarters, Teams Premium paid customers exceed 10K; SIEM Microsoft Sentinel has over 25K customers, annualized revenue over $1B.

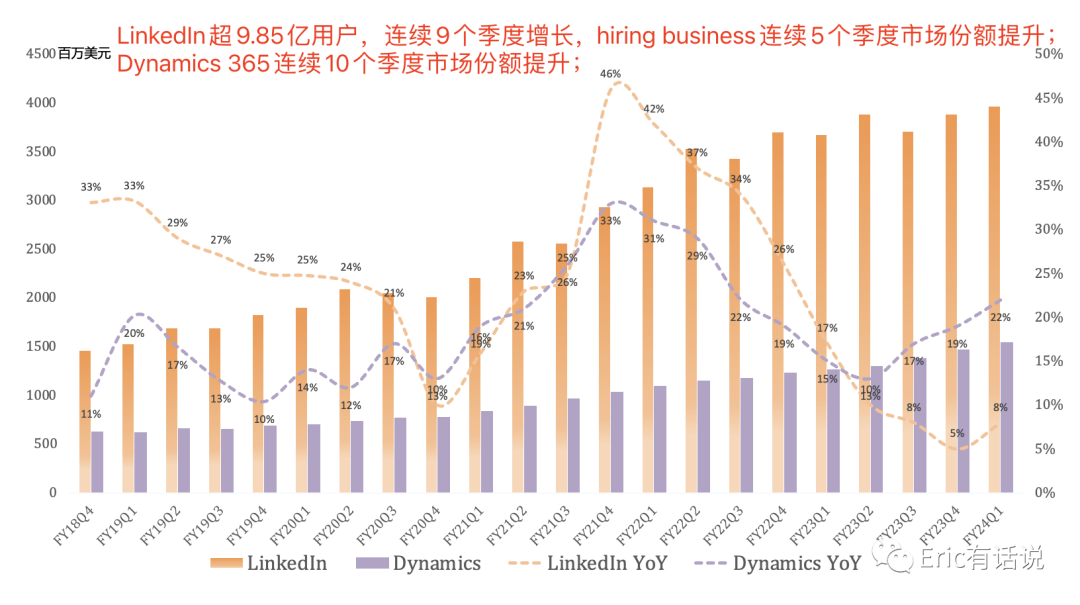

LinkedIn revenue was $4B, up 8% year over year; LinkedIn exceeds 985M users, up for 9 consecutive quarters; Premium subscriptions up 55% year over year, hiring business market share up for 5 consecutive quarters; bookings continue to decline year over year.

Dynamics revenue was $1.5B, up 22% year over year, setting a new historical high for 3 consecutive quarters; Dynamics 365 market share up for 10 consecutive quarters; over 126K companies have used AI features in Power Platform, EY enabled Copilot for 170K of its Power Platform users; Power Apps MAU 20M, up 40% year over year.

Intelligent Cloud revenue was $24.3B, up 19% year over year, exceeding $20B for the 6th consecutive quarter; operating income was $11.8B, up 31% year over year, setting a new historical high.

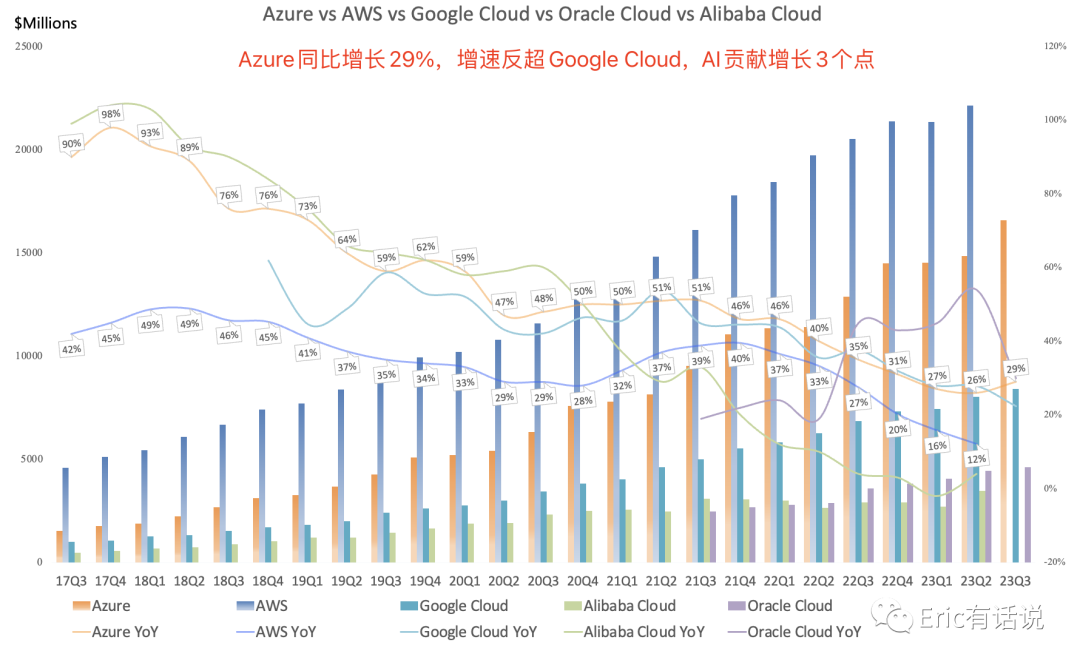

Azure revenue was ~$16.6B, up 29% year over year, with AI contributing 3 points of growth; Azure market share continues to rise, seeing more customers migrate to Azure; Azure Arc now has over 21K customers, up 140% year over year; Azure OpenAI Service customers exceed 18K; Azure AI customers beyond OpenAI include first-party, Meta, Hugging Face; aside from AI, the cloud customer cost-optimization trend driven by global macroeconomic slowdown continues; Azure has over 60 global data center regions, with the best AI training and inference infrastructure; Azure is the only cloud provider besides Oracle Cloud to offer Oracle database services.

Microsoft Fabric has over 16K active customers, including 50%+ of the Fortune 500; GitHub Copilot has over 1M paid users, over 37K organizations use GitHub Copilot for Business, up 40% sequentially; since acquisition 5 years ago, GitHub developers up 4x year over year.

More Personal Computing revenue was $13.7B, up 3% year over year; operating income was $5.2B, up 23% year over year.

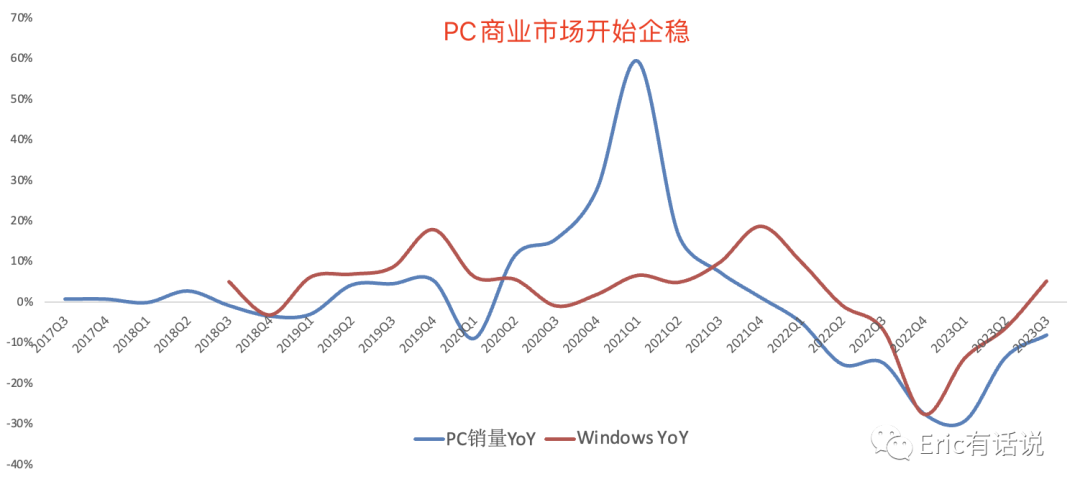

Windows revenue was ~$5.8B, up 5% year over year; commercial PC market beginning to stabilize.

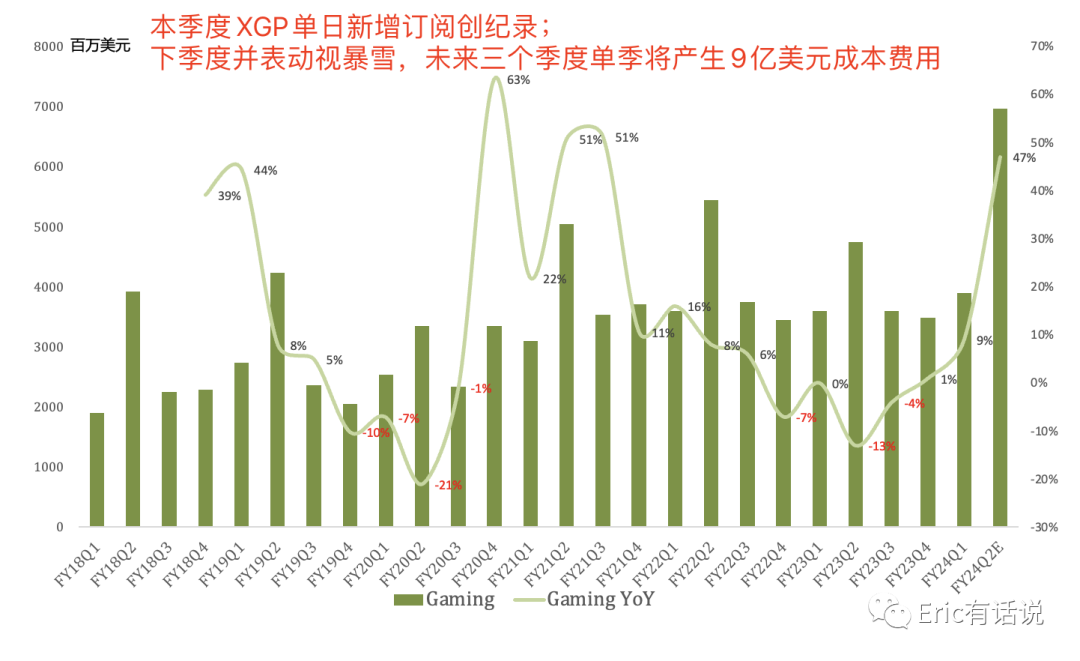

Gaming revenue was $3.9B, up 9% year over year; Xbox hardware revenue down 7% year over year, software revenue up 13% year over year; this quarter set a record for single-day Xbox Game Pass subscriber additions; Starfield players exceed 11M, 50% of playtime on PC; Minecraft cumulative units sold exceed 300M; Microsoft now owns $13B worth of game franchises; Activision Blizzard acquisition closed October 13, next quarter impact of $500M COGS and $400M OPEX, Q3 and Q4 still carry this $900M cost.

Search and news advertising revenue was $3.2B, up 10% year over year; Edge browser market share up for 10 consecutive quarters.

Devices revenue down 22% year over year.

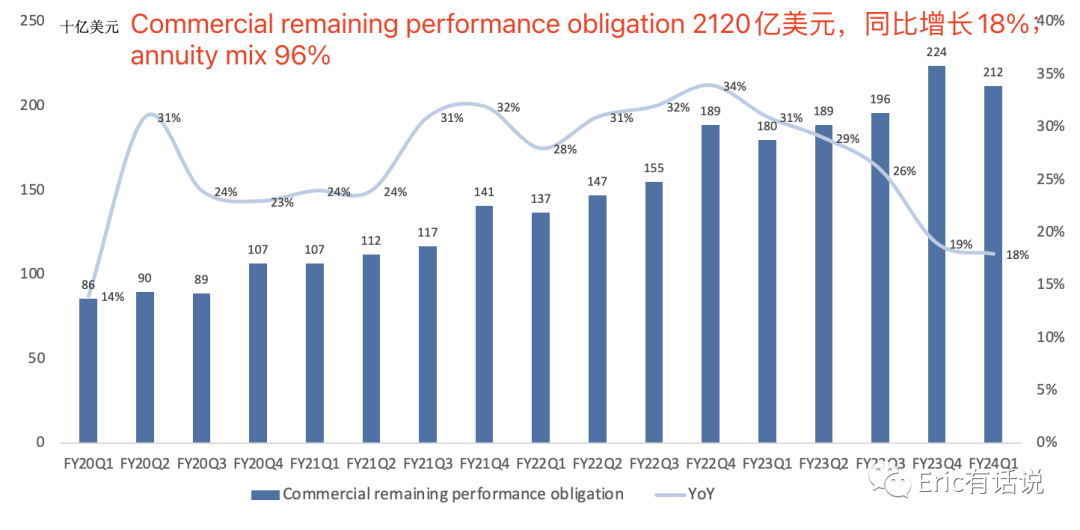

Commercial remaining performance obligation increased 18% to $212 billion. Roughly 45% will be recognized in revenue in the next 12 months, up 15% year-over-year. The remaining portion, which will be recognized beyond the next 12 months, increased 20%.

Guiding FY24Q2 revenue up 16% year over year, net income up 28% year over year; Azure up 26-27% year over year, with AI contribution increasing; H2 Azure growth consistent with Q2; gaming revenue up 45%+ year over year, with 35% from Activision Blizzard; future capex growing sequentially, still investing in AI servers; guiding FY24 full-year operating margin flat.

Overall, this report saw Azure significantly exceed expectations, especially against the backdrop of a notable deceleration at Google Cloud. While the market waited for Microsoft Copilot AI revenue to materialize, Azure struck first. Of course, this Azure strength is not just Azure AI business; as Nadella said, this quarter saw clear customer migration, with AI customers drawn by Azure AI also adopting other Azure services.

The margin dynamics this quarter were another surprise: Azure, previously a drag on gross margin, actually drove gross margin expansion this quarter. The market had worried that high-intensity AI investment would pressure margins, but that did not happen at Microsoft; instead, AI business gross margins are expanding rapidly, which is undoubtedly good news for the AI hardware industry.

Our previous view on Microsoft has always been: the biggest watch item is to what extent Microsoft can commercialize these AI technologies, and what degree of synergy they can generate with the Azure/Office/Windows three engines.

Currently, Azure is the first to see AI commercialization results; next quarter we watch Office Copilot; Windows will have to wait for Win12 next year.

*All segment revenue figures above are estimates.