Microsoft's latest FY26 Q2 corresponds to calendar October/November/December 2025.

Microsoft FY2026 Q2 Summary:

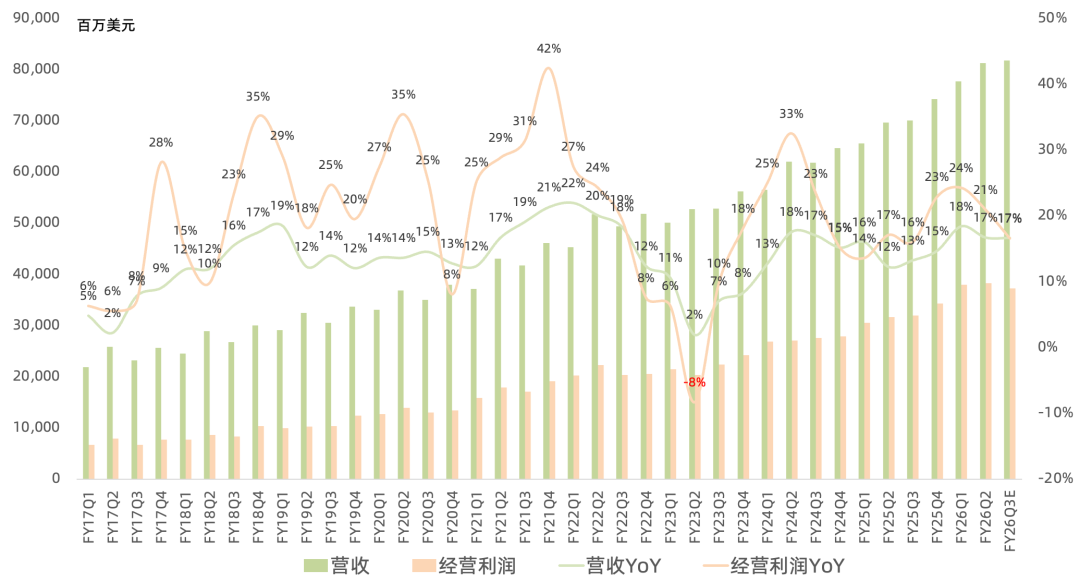

Revenue $81.3B, up 17% year over year, above consensus $80.3B and above prior guidance range $79.5-80.6B.

Gross margin 68%, down 0.7 percentage points year over year, above consensus 67.1% and above prior guidance range 66.6-67.3%.

Operating income $38.3B, up 21% year over year, above consensus $36.4B and above prior guidance range $35.55-36.95B.

Net income $38.5B, up 60% year over year; ex-$7.6B OpenAI investment gain, net income $30.9B, up 23% year over year, above consensus $29.1B.

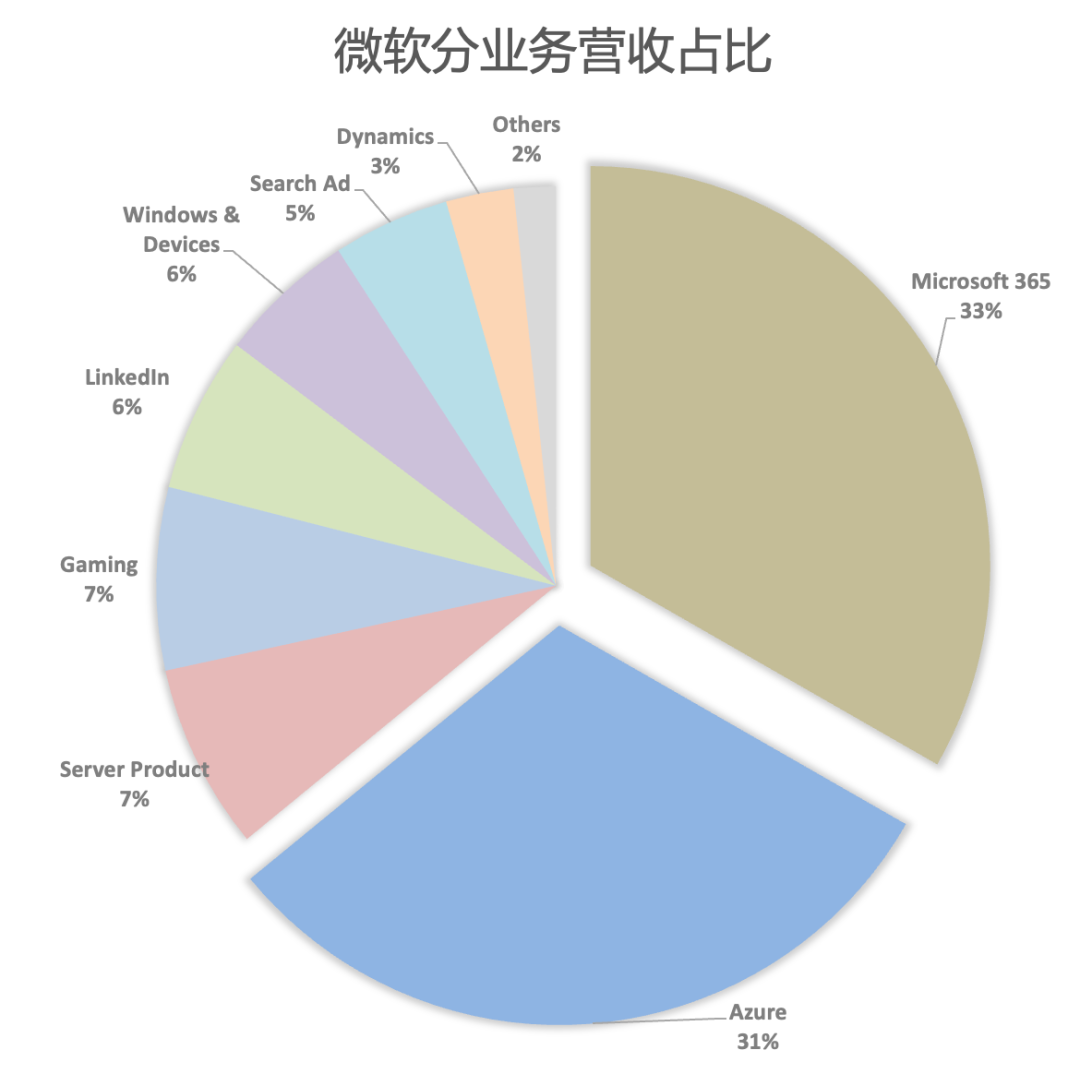

Productivity and Business Processes

Productivity (M365, LinkedIn, Dynamics) revenue $34.1B, up 16% year over year; gross margin 82.1%, up 1 percentage point year over year; operating income $20.6B, up 22% year over year.

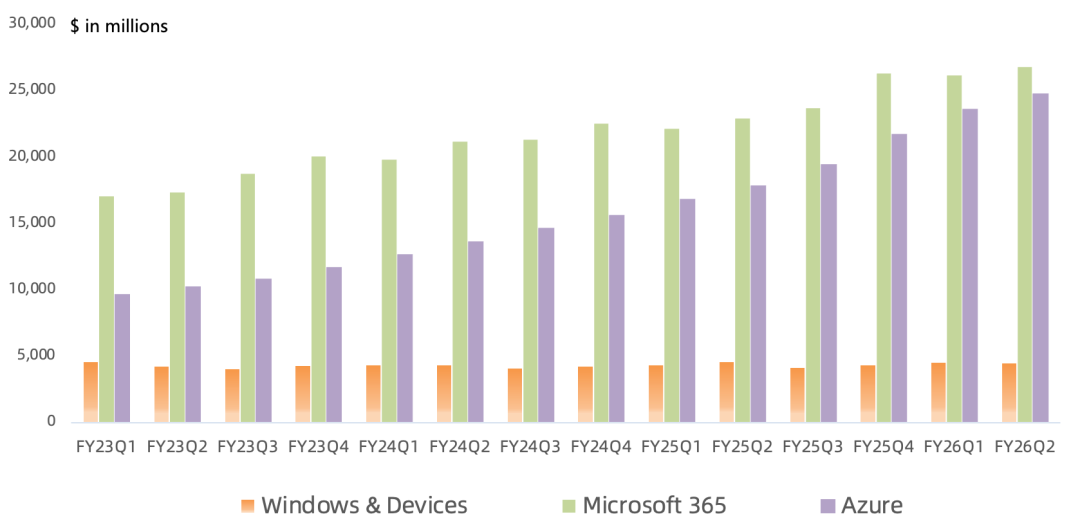

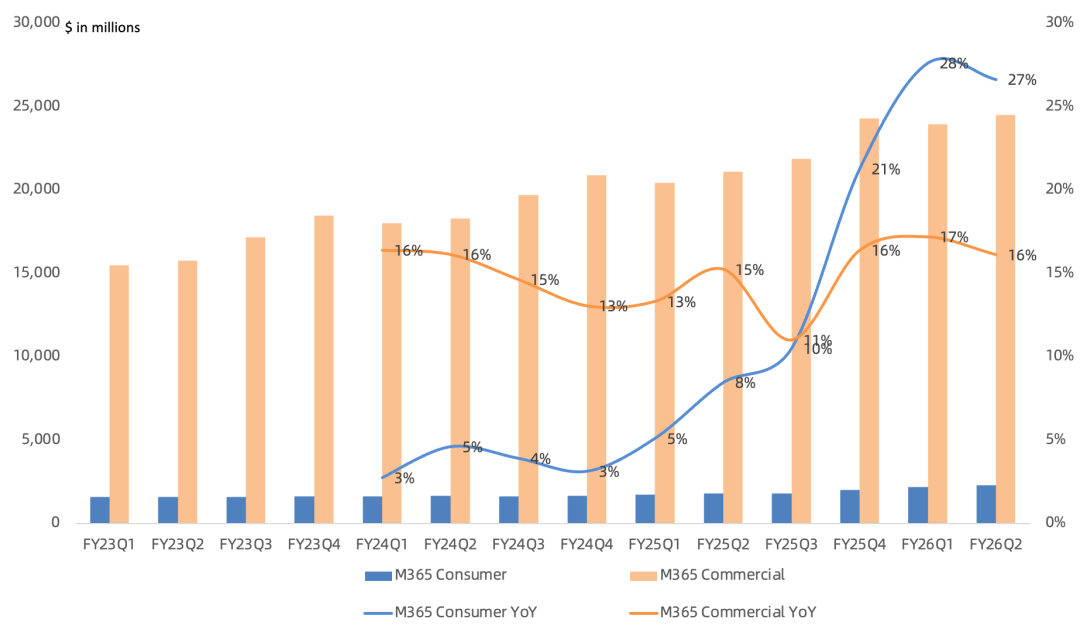

Microsoft 365 revenue ~$26.8B, up 17% year over year; M365 commercial cloud growth driven by both ARPU and seat count; ARPU growth again led by E5 and M365 Copilot; M365 commercial paid seats up 6% year over year (>430M) with revenue up 17%; M365 commercial product revenue beat expectations on higher-than-expected Office 2024 purchases; M365 consumer cloud revenue also driven by ARPU growth; M365 consumer subscriptions up 6% year over year (>90M) with revenue up 29%; DAX Copilot in healthcare helping >100K providers automate workflows.

Copilot app daily active users up nearly 3x year over year; M365 Copilot DAU up 10x year over year; M365 Copilot seats up >160% year over year, now 15M paid M365 Copilot seats and multiples more enterprise chat users; >35K-seat large customers up 2x year over year.

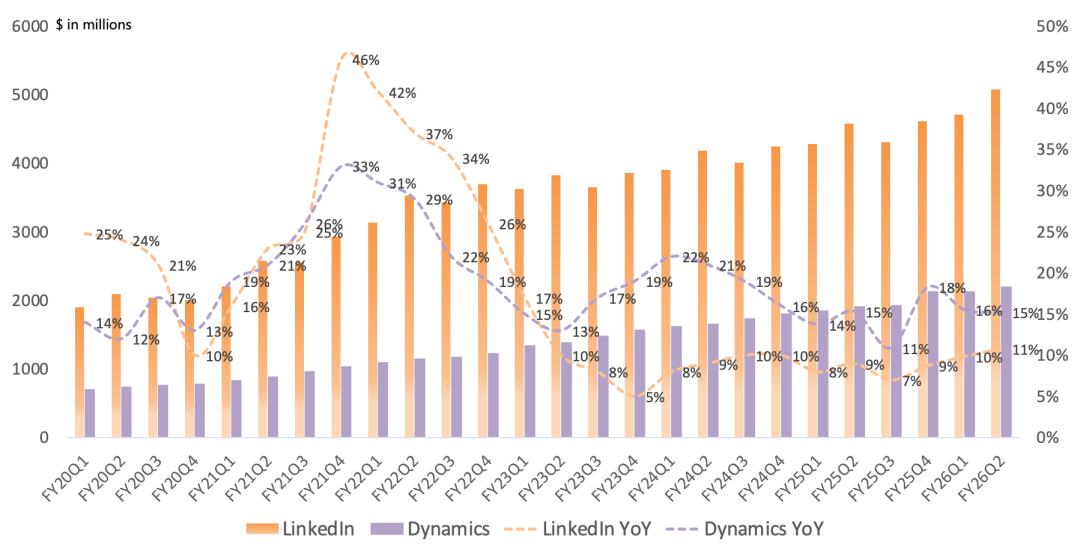

LinkedIn revenue $5.1B, up 11% year over year; LinkedIn member growth double digits, paid video ads up 30%.

Dynamics revenue $2.2B, up 15% year over year; Dynamics 365 revenue up 19% year over year; all workloads growing.

Intelligent Cloud

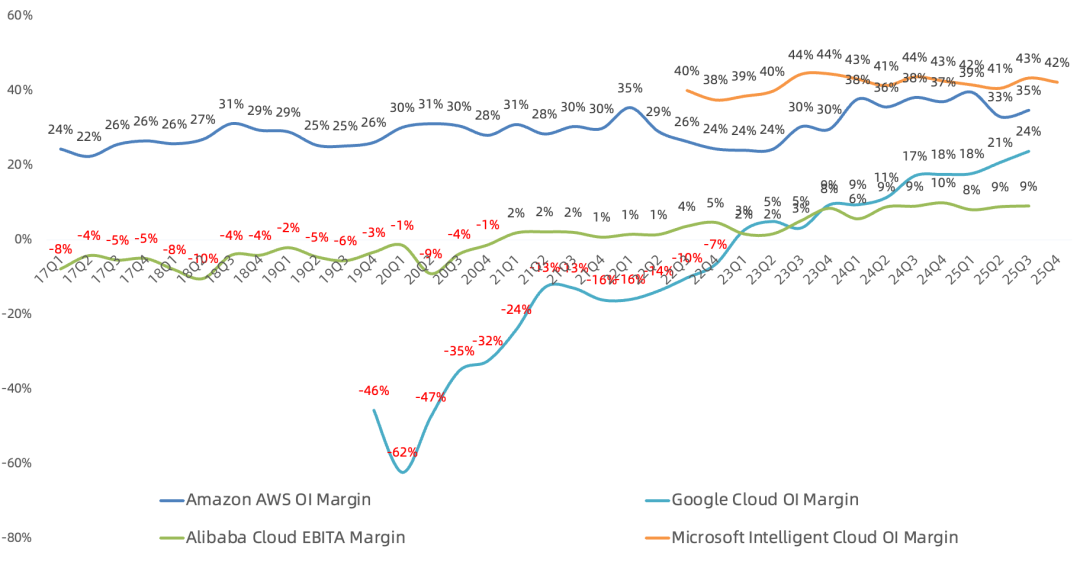

Intelligent Cloud (Azure, Server Products, Enterprise Services) revenue $32.9B, up 29% year over year; gross margin 58.8%, down 4.4 percentage points year over year; operating income $13.9B, up 28% year over year.

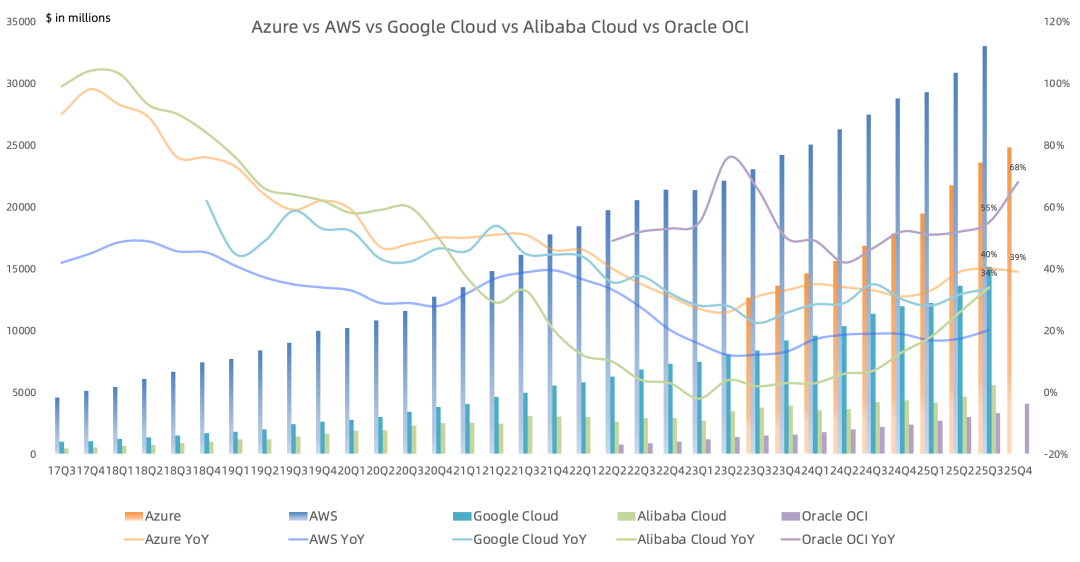

Azure revenue ~$24.8B, up 39% year over year; growth rate down 1 percentage point sequentially; customer demand continues to exceed supply; Azure growth may fluctuate quarterly depending on capacity delivery and go-live timing, and revenue recognition depending on contract mix; offers broadest model selection among hyperscalers, >1,500 customers using both Anthropic and OpenAI models on AI Foundry; continuing to invest in first-party model R&D; customers spending >$1M/quarter on AI Foundry up nearly 80%, >250 customers on track to process >1 trillion tokens on Foundry this year.

Added nearly 1 GW of data center capacity this quarter alone; announced data center investments in 7 countries supporting local data residency; most comprehensive sovereign solution portfolio across public, private, and national partner clouds.

Data & Analytics: Fabric revenue up 60% year over year, run-rate revenue >$2B, 31K paid users (28K last quarter); >80% of Fortune 500 have active agents built with Copilot Studio and Agent Builder low-code/no-code tools; GitHub Copilot Pro+ subscriptions up 77% sequentially, 4.7M paid users, up 75% year over year.

Security: Rolling out Security Copilot to all E5 customers; now 1.6M security customers (1.5M in FY25 Q4), >1M using 4+ workloads; market share improved across all served security categories.

More Personal Computing

More Personal Computing (Windows, Devices, Gaming, Advertising) revenue $14.3B, down 3% year over year; gross margin 55.8%, up 2.4 percentage points year over year; operating income $3.8B, down 3% year over year.

Windows & Devices revenue $4.5B, down 2% year over year; Win11 users reach 1B, up >45% year over year.

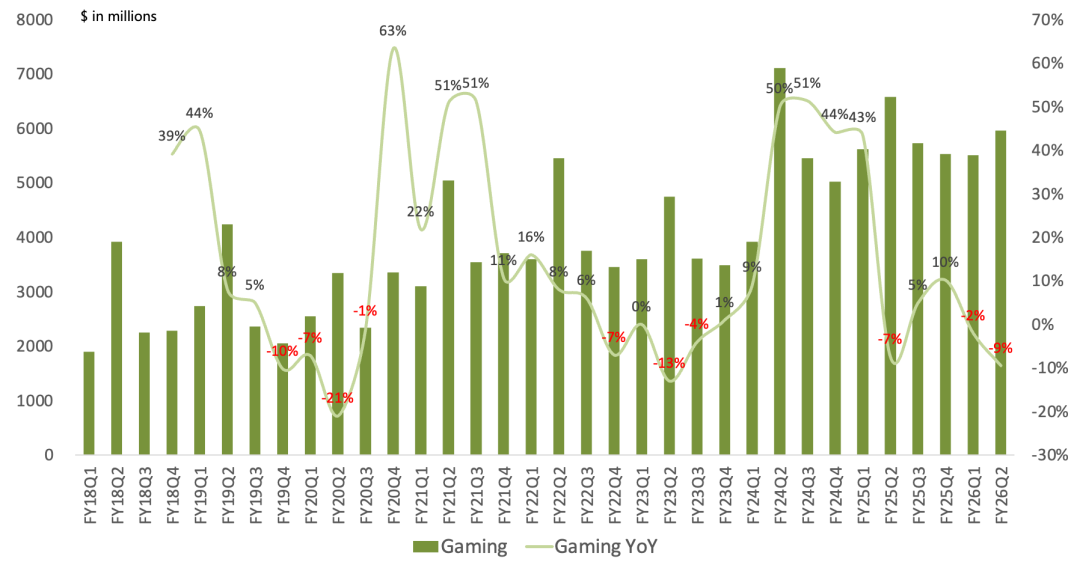

Gaming revenue $6.0B, down 9% year over year; Xbox hardware revenue continues steep decline down 32% year over year; high-margin software/services revenue down 5% year over year; Gaming recorded impairment charge (likely Activision Blizzard); memory price increases to impact future PC market.

Search & Advertising revenue $3.8B, up 10% year over year; Windows, Edge, and Bing all gained share this quarter.

Earnings Call Highlights

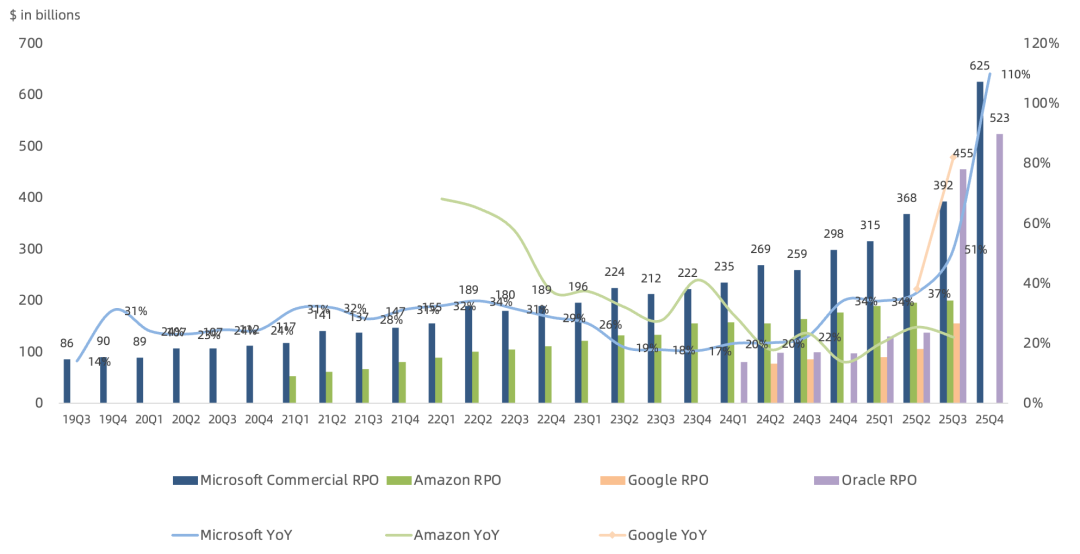

OpenAI and Anthropic mega-deals drove commercial RPO to $625B this quarter, up 110% year over year and up $233B sequentially; 45% from OpenAI; ex-OpenAI customer RPO up 28% year over year, primarily driven by Anthropic; weighted average duration ~2.5 years; 25% of Microsoft RPO to be recognized within 12 months, up 39% year over year; RPO metric has lost market credibility since Oracle's dramatization, and OpenAI's outsized share heightens concerns.

Projected FY26Q3 revenue of $80.65-81.75B, up 15-17% year over year; gross margin ceiling of 67.4%, down 1.3 percentage points year over year; operating income guidance ceiling of $37.3B, up 17% year over year; net income guidance ceiling of $30.8B, up 19% year over year. Microsoft Cloud gross margin at 65%, continuing to decline, impacted by ongoing AI investment and product mix.

Projected FY26Q3 Azure growth of 37-38% year over year; M365 Commercial Cloud up 13-14% year over year, Consumer Cloud up mid-to-high twenties% year over year; LinkedIn up low double digits year over year, Dynamics 365 up high teens% year over year, Windows OEM & Devices down low teens% year over year, Search Advertising up high single digits year over year, Gaming Services down mid-single digits year over year. On commercial bookings, excluding last year's OpenAI contract adjustment, core business is expected to achieve healthy growth on a growing deferred revenue base.

This quarter capex was $37.5B, up 66% year over year, with 2/3 allocated to short-lived GPU and CPU assets to support growing Azure platform demand, and the remainder to long-lived assets that will support monetization for 15+ years, including $6.7B in finance leases primarily for large data center sites. Projected FY26Q3 capex to decline sequentially, mainly due to changes in delivery cadence; rising storage prices will impact capex. Microsoft's cumulative capex over the past four quarters totaled $118B, versus Meta's $72.2B; Meta's 2026 capex guidance is $115-135B, indicating the AI arms race continues.

Management stated that purchased GPUs were already covered by long-term contracts with major customers spanning the full useful life before procurement, meaning investment is essentially collecting cash before buying inventory, with no risk of cost recovery failure.

This quarter recognized a $7.583B after-tax investment gain from OpenAI, versus a $939M loss recognized in the year-ago quarter. Notably, starting this quarter Microsoft recognizes OpenAI gains/losses based on 'changes in OpenAI's balance sheet net assets proportional to ownership stake' rather than 'OpenAI's income statement operating profit/loss proportional to ownership stake.'

Overall, this earnings report continues to highlight Microsoft's stability, especially maintaining double-digit revenue and profit growth amid intense capital spending—no small feat—but the market is not buying it.

The market clearly ignored management's comments last quarter, still hoping higher capex would drive higher Azure revenue growth. Instead, new compute was prioritized for Copilot and proprietary large models where revenue impact is slower, while Azure—the fastest ROI—was neglected. Management responded: 'If we allocated all newly online GPUs to Azure, Azure growth would certainly exceed 40%, but the company must also serve high-margin businesses like M365 and Copilot and proprietary large model R&D needs.'

Despite the previously favorable outlook, Microsoft now faces two major challenges:

1. The trade-off between gross margin and growth will continue to ferment. The market's biggest AI concern remains monetization; the fastest landing spots are cloud and advertising, but cloud inherently carries lower gross margins. Microsoft worries about further margin erosion and deliberately tilts compute toward the higher-margin Copilot business. Management notes that, as with the CPU era of cloud, margins will improve over time. But can today's market style wait that long? Moreover, for cloud rivals with smaller scale and lower margins than Microsoft, this presents a potential opportunity to erode Azure share.

2. Nadella's strategy of positioning Microsoft as the 'scaffolding of the AI era' will be challenged amid rapid iteration of AI foundation models—the market's feared 'AI eats software' narrative. Even if not disrupted by foundation models, 'if you can't beat them, join them' comes at a cost: gross margin. Will software companies accustomed to high margins have as good a time in the AI era?