Microsoft FY2023 Q3 Earnings Summary:

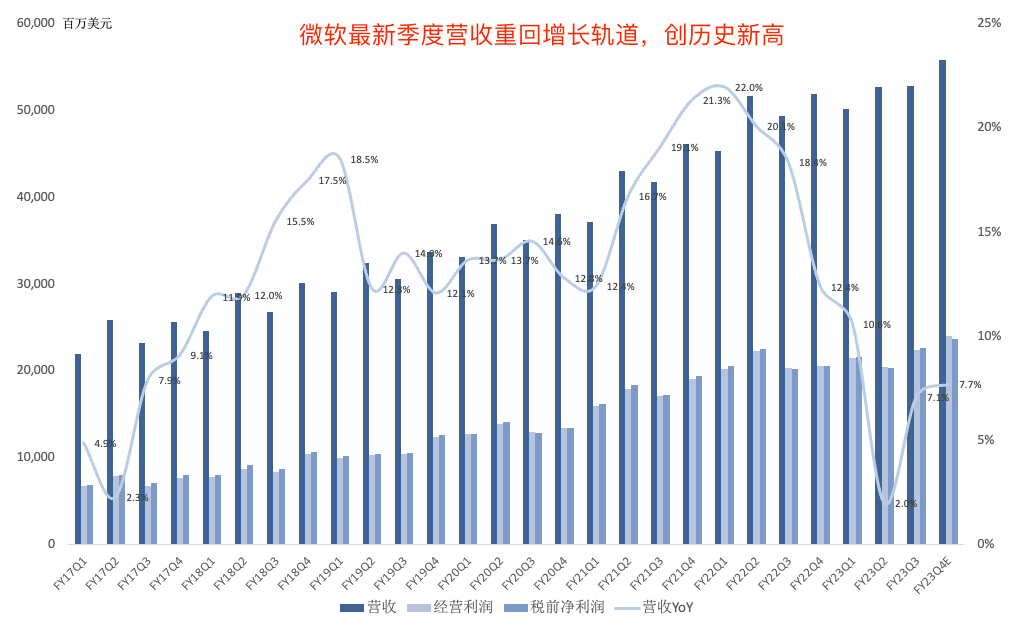

Revenue reached a record $52.857B, up 7% year over year as growth began to reaccelerate, with currency reducing growth by 3 percentage points. Operating income rose 10% to a record $22.352B, while net income increased 9% to $18.299B.

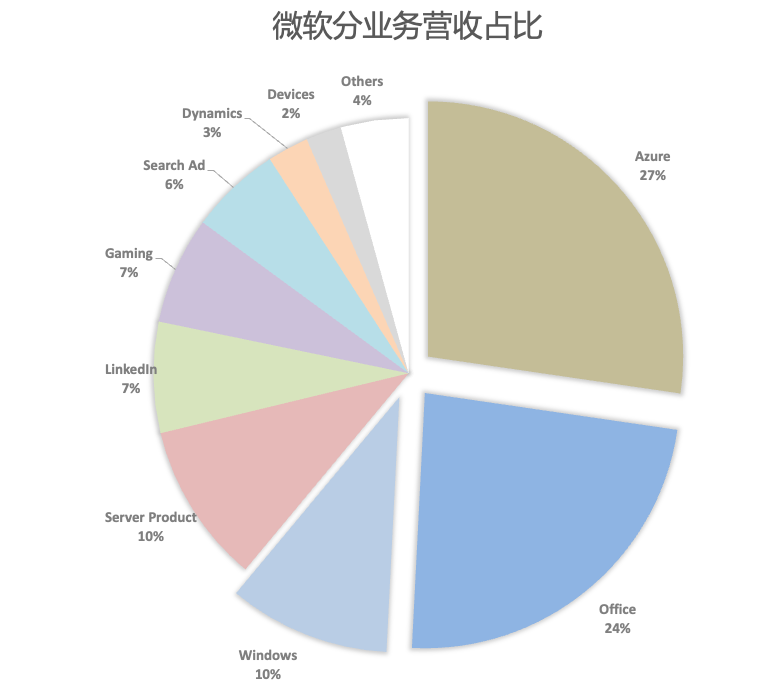

Productivity and Business Processes revenue reached $17.5B, up 11% year over year. Operating income rose 20% to a record $8.6B.

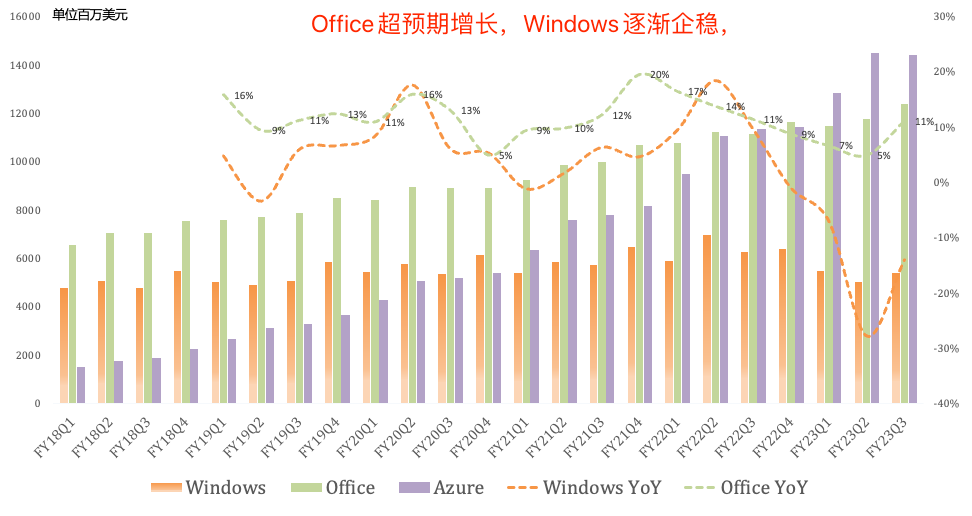

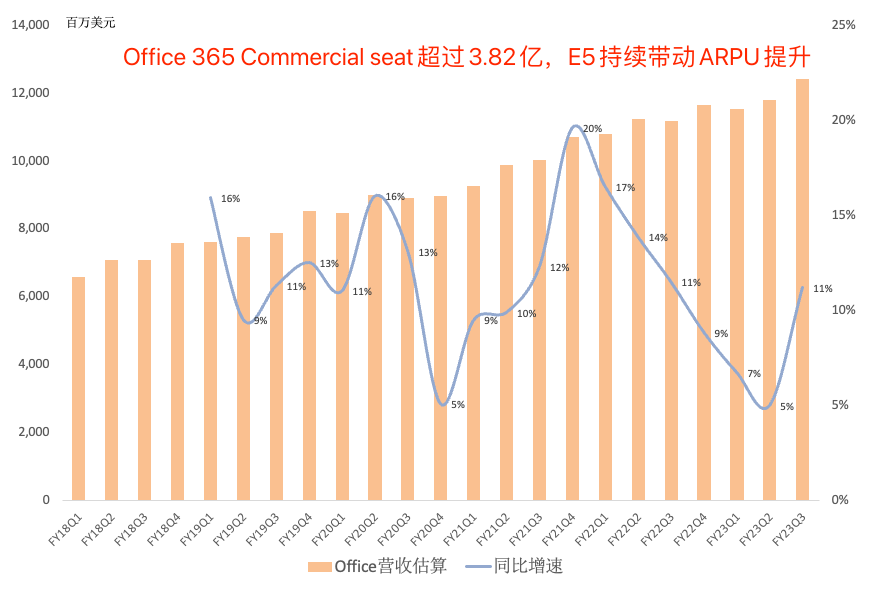

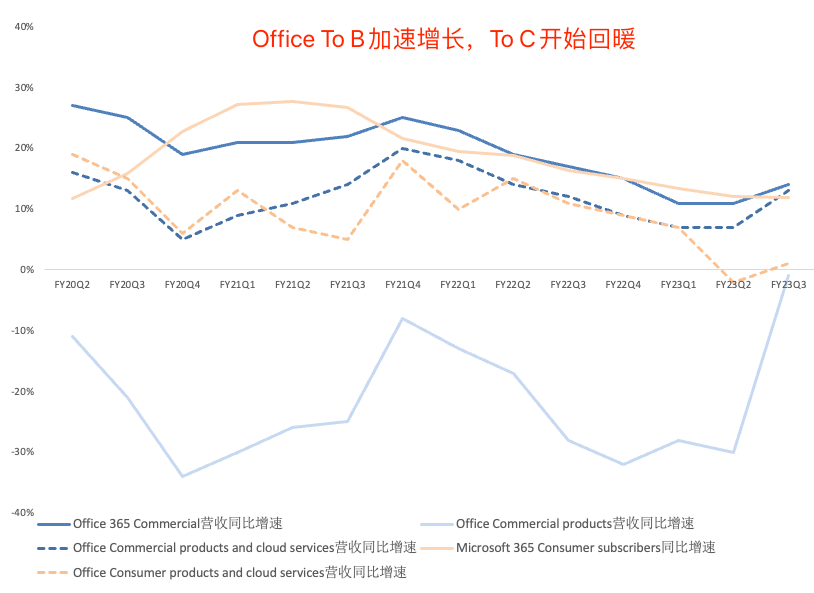

Office revenue was approximately $12.4B, up 11% year over year. Migration from Office E3 to E5 remained strong, supporting further E5 ARPU growth. Office 365 Commercial surpassed 382 million seats, while Teams exceeded 300 million monthly active users. Sixty percent of enterprise Teams customers purchased Teams Phone, Rooms, or Premium, and Teams Rooms revenue doubled. Microsoft continued to gain share in security: nearly 720,000 organizations used Azure Active Directory, up 33%, while the number of customers using at least four workloads grew 35% to nearly 600,000.

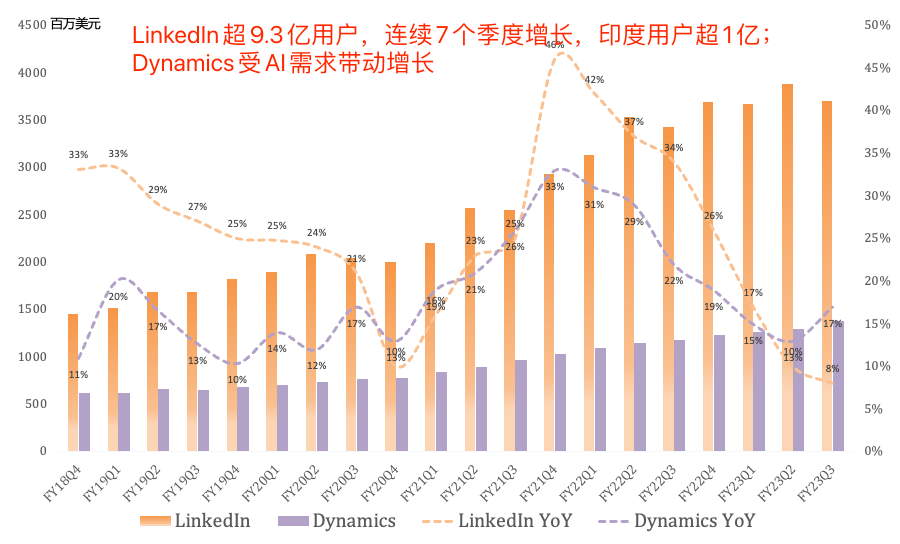

LinkedIn revenue reached $3.7B, up 8% year over year, with growth accelerating for a seventh consecutive quarter. The platform surpassed 930 million members, including more than 100 million in India, up 19%, while student membership grew 73%.

Dynamics revenue rose 17% to a record $1.4B as Dynamics 365 continued to gain market share. Power Platform approached 33 million monthly active users, up nearly 50%, with more than 36,000 organizations using its AI capabilities.

Intelligent Cloud revenue reached $22.1B, up 16% year over year and above $20B for a fourth consecutive quarter. Operating income increased 14% to a record $9.5B.

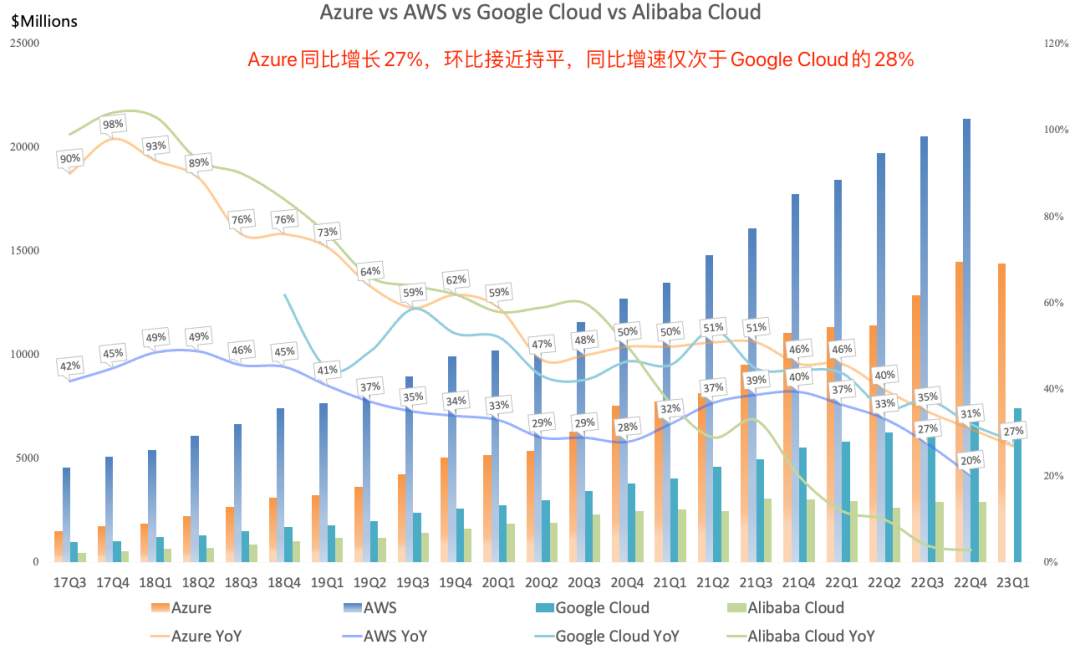

Azure generated approximately $14.4B of revenue, up 27% year over year despite a 4-percentage-point currency headwind. Azure Arc surpassed 15,000 customers, up 150%, while Azure OpenAI Service exceeded 2,500 customers, an elevenfold sequential increase. OpenAI used Cosmos DB. GitHub was used by 76% of the Fortune 500, and more than 10,000 organizations adopted Copilot for Business. Outside AI, however, the macro-driven trend toward cloud optimization and cost control continued.

More Personal Computing revenue declined 9% year over year to $13.3B, while operating income fell 14% to $4.2B.

Windows revenue was approximately $5.4B, down 14% year over year, even as monthly active Windows devices reached another record. More than 90% of the Fortune 500 was deploying or had already deployed Windows 11, and over one-third of enterprise customers purchased cloud-delivered Windows.

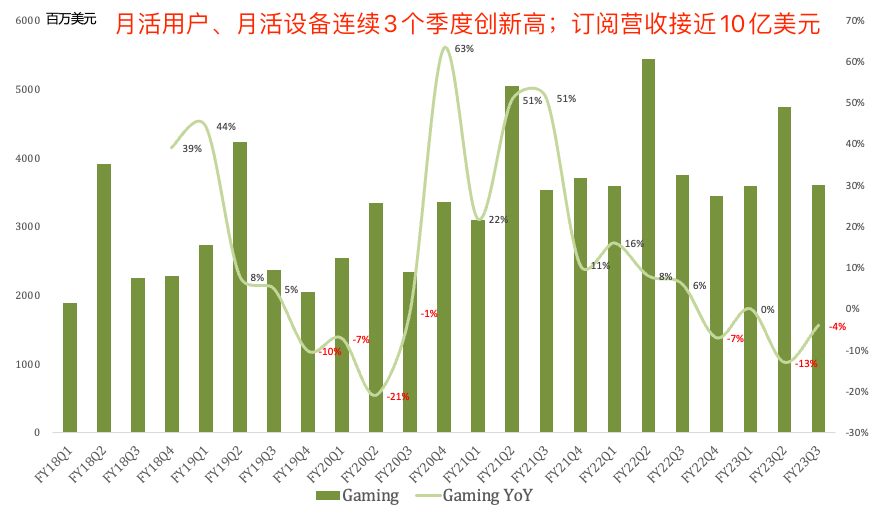

Gaming revenue declined 4% year over year to $3.6B. Xbox hardware revenue fell 30% to approximately $600M, while software revenue grew 3% to about $3B. Gaming monthly active users and devices set records for a third consecutive quarter, subscription revenue approached $1B, and Microsoft's first-party games reached more than 500 million players.

Search advertising revenue rose 10% year over year to $3.1B. Edge gained browser share for an eighth consecutive quarter, while Bing surpassed 100 million daily active users and made meaningful share gains in the United States.

Devices revenue fell 30% year over year to $1.2B, although commercial PC demand was better than expected.

Commercial remaining performance obligation increased 26% to $196 billion. Roughly 45% will be recognized in revenue in the next 12 months, up 18% year-over-year. The remaining portion, which will be recognized beyond the next 12 months, increased 34%.

Currency reduced quarterly revenue growth by 3 percentage points and operating income growth by 4 points. Management expected a 2-point currency headwind to revenue growth in the following quarter. FY23Q4 guidance implied 8% year-over-year revenue growth and 14% net income growth. Capital expenditure was expected to rise sharply sequentially, primarily to fund Azure AI infrastructure.

Overall, this was a characteristically Microsoft quarter: stable execution despite significant headwinds. Microsoft has remained the most consistent earnings performer among the technology giants in recent years.

ChatGPT was not yet contributing direct, material growth to Microsoft, but Satya Nadella remained confident in the long-term synergy discussed on the earnings call. OpenAI's customer base had relatively little overlap with Microsoft's, leaving substantial future cross-selling potential. Microsoft expected Azure to grow 27% year over year, including 1 percentage point from AI services.

The key question is how effectively Microsoft can commercialize these AI technologies and how much synergy they can create across Azure, Office, and Windows. The opportunity is for Microsoft to become a true AI-as-a-Service company.

*All segment revenue figures above are estimates.