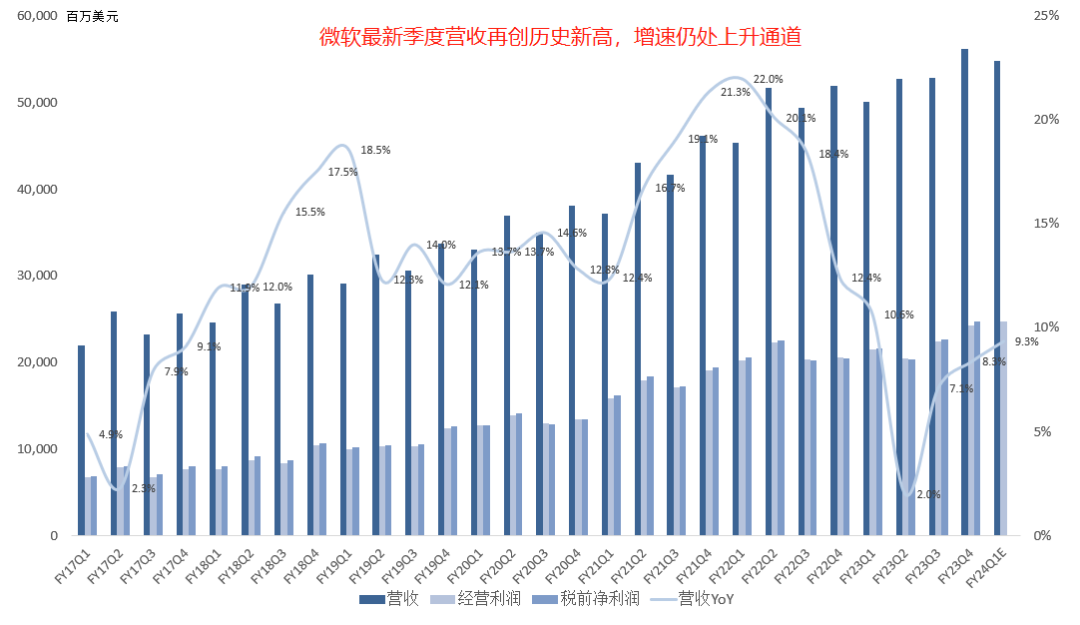

Microsoft FY2023 Q4 Earnings Summary:

Revenue rose 8% to a record $56.189B, operating income increased 18% to a record $24.254B, and net income topped $20B for the first time at $20.081B.

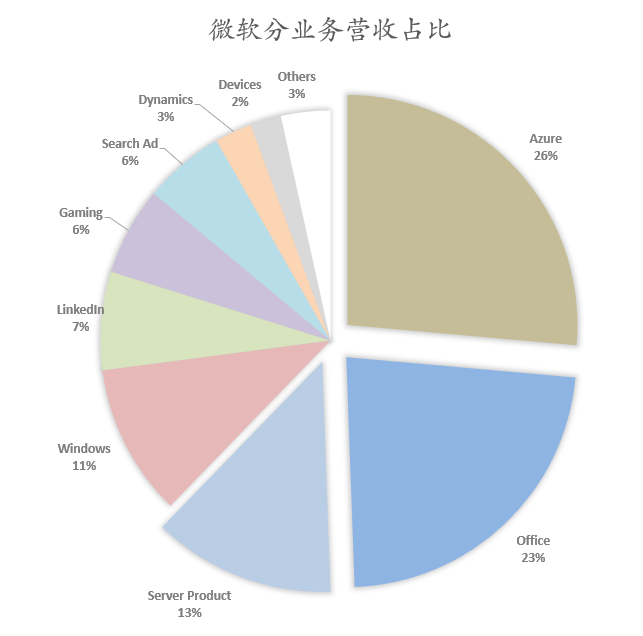

Productivity and Business Processes revenue was $18.3B, up 10% year over year; operating income was $9.1B, up 25% year over year, a new record high.

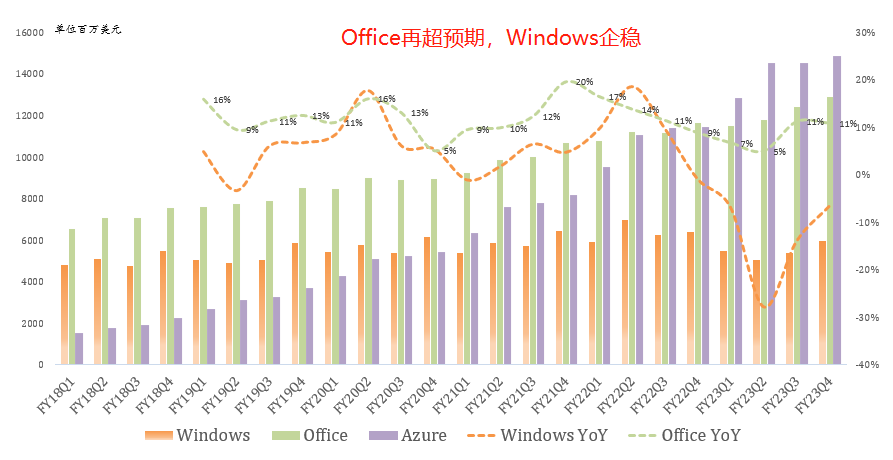

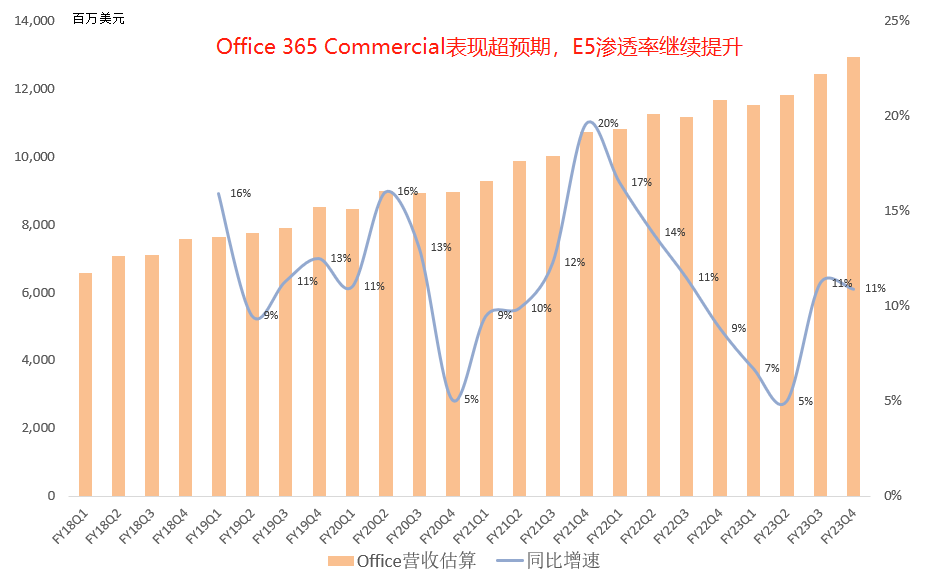

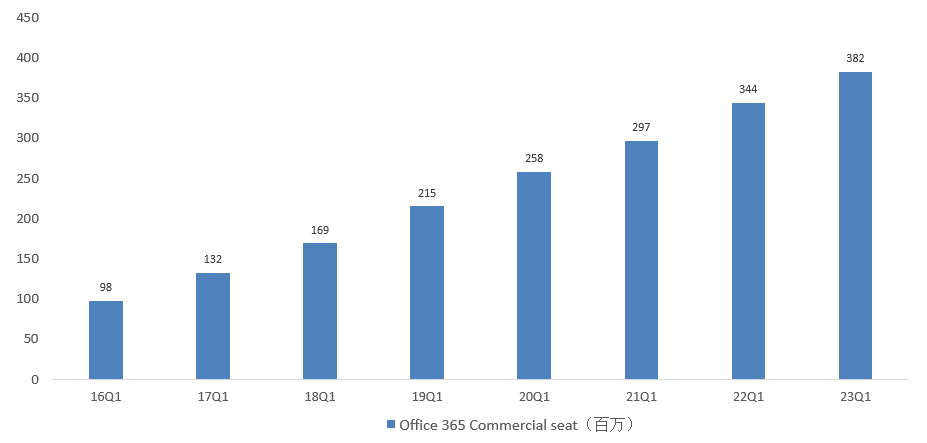

Office revenue was approximately $12.9B, up 11% year over year; enterprise E5 upgrade intent exceeded expectations; commercial seat growth driven mainly by SMBs; Office 365 Commercial seats exceed 382M; Teams MAU surpasses 300M; Teams Premium seats exceed 600K; PSTN users exceed 17M, up 45% year over year; Teams Rooms covers 70% of Fortune 500, revenue doubled year over year; Microsoft Viva MAU exceeds 35M; security serves over 1M enterprise customers, up 26% year over year; over 60% of customers purchase 4+ workloads, up 33% year over year; share gains across all segments; identity: Microsoft Entra ID MAU exceeds 610M; Security Copilot launching this fall.

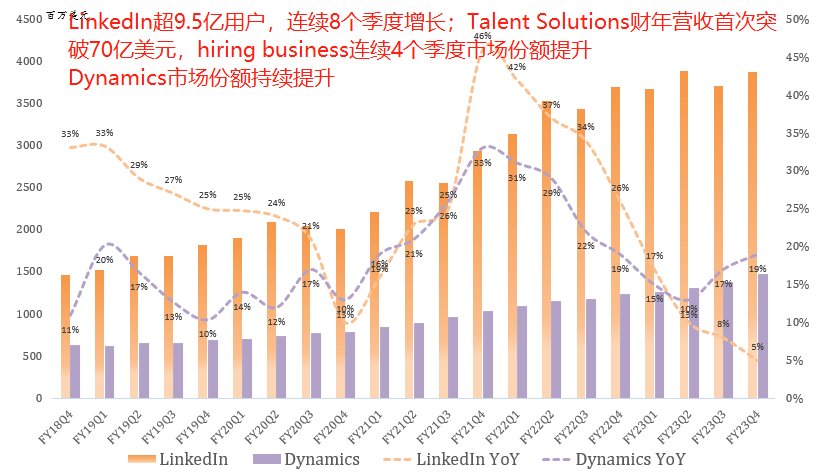

LinkedIn revenue was $3.9B, up 5% year over year; LinkedIn exceeds 950M users, up for eight consecutive quarters; Talent Solutions fiscal revenue topped $7B for the first time; hiring business gained share for four consecutive quarters.

Dynamics revenue was $1.5B, up 19% year over year, a record high for the third consecutive quarter; Dynamics products continue to gain share; customer experience, service, and finance & supply chain businesses each surpassed $1B in annual revenue; over 63K Power Platform users use AI features, up 75% sequentially; Power Automate MAU 10M, up 55% year over year.

Intelligent Cloud revenue was $24.0B, up 15% year over year, fifth consecutive quarter above $20B; operating income was $10.5B, up 20% year over year, a new record high.

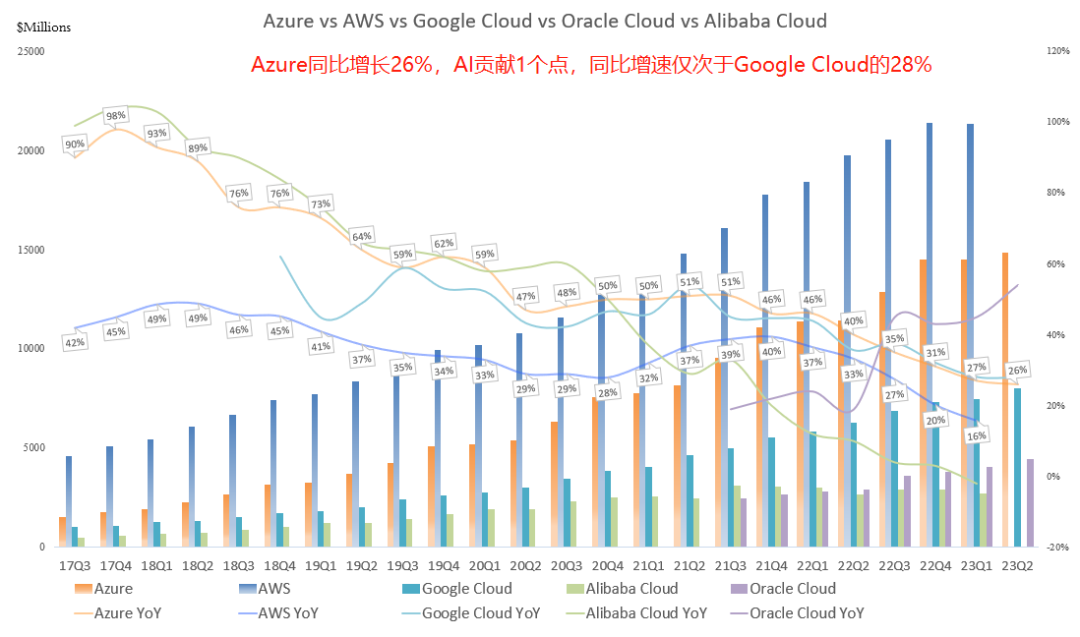

Azure revenue was approximately $14.8B, up 26% year over year, with AI contributing 1 point; Azure market share continues to rise; Azure Arc has over 18,000 customers, up 150% year over year; Azure OpenAI Service has over 11,000 customers, adding nearly 100 new customers daily this quarter; aside from AI, the global macro-driven cloud optimization trend persists.

Microsoft Fabric had over 8,000 customers trialing within one month of launch, over 50% using 4+ workloads; GitHub Copilot for Business used by over 27K organizations, doubling sequentially.

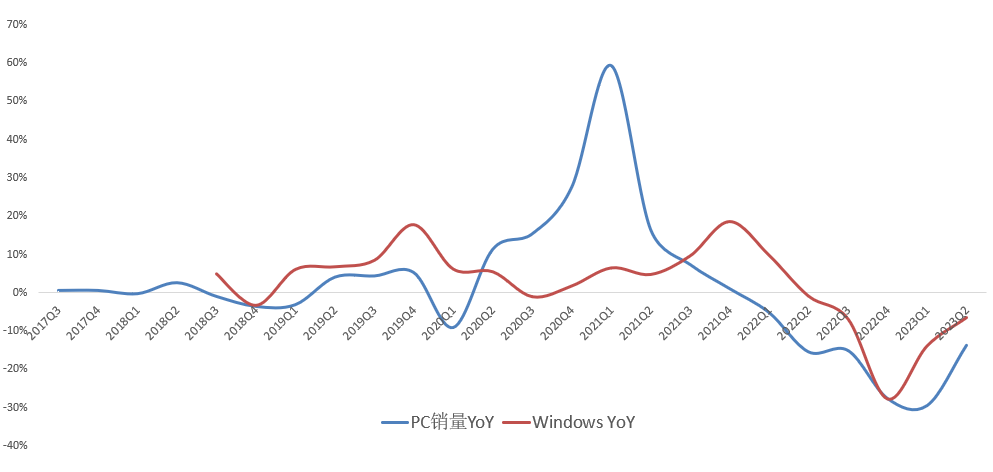

More Personal Computing revenue was $13.9B, down 4% year over year; operating income was $4.7B, up 4% year over year.

Windows revenue was approximately $6.0B, down 7% year over year; Microsoft 365 Copilot in paid preview with 600 enterprises; monthly active Windows 11 devices doubled year over year; Azure Virtual Desktop / Windows 365 cloud PC trailing-twelve-month revenue exceeds $1B.

Gaming revenue was $3.5B, up 1% year over year; Xbox hardware revenue down 13% year over year; content and services revenue up 5% year over year; gaming MAU and active devices hit records for the fourth consecutive quarter.

Search and news advertising revenue was $3.2B, up 8% year over year; Edge browser share up for nine consecutive quarters.

Devices revenue was $1.2B, down 20% year over year.

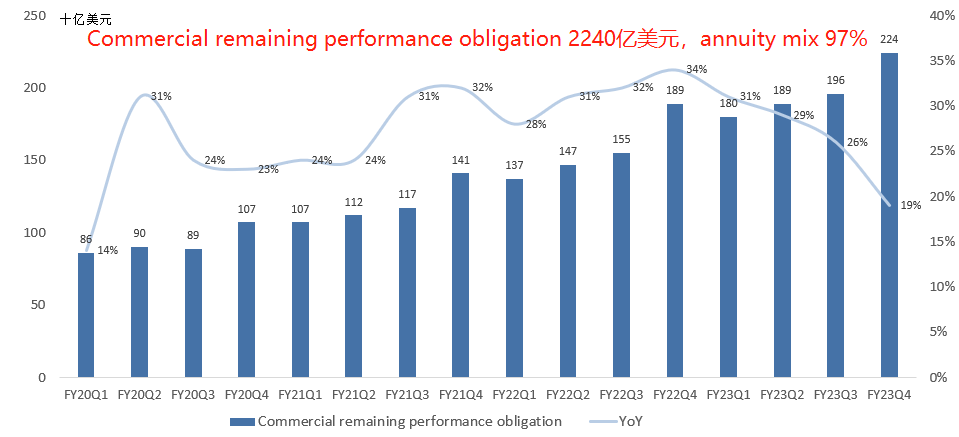

Commercial remaining performance obligation increased 19% to $224 billion. Roughly 45% will be recognized in revenue in the next 12 months, up 13% year-over-year. The remaining portion, which will be recognized beyond the next 12 months, increased 22%.

FY24Q1 revenue is guided to grow 9% year over year; net income up 15% year over year. Azure up 25%–26% year over year, of which 2 percentage points from AI. Azure AI results will mainly appear in FY24H2. AI business margins expand quickly; AI adoption curve is also expected to be fast. Future capex will grow sequentially each quarter, primarily for AI investment.

This quarter, the number of Azure and Microsoft 365 deals above $10M hit a new high, with Azure's average annualized contract value reaching a record;

Overall, this earnings report remains in Microsoft's steady style, with Office slightly beating expectations. The market priced in AI performance realization too aggressively, too impatiently. The trillion-dollar incremental opportunity is right there; it just needs time.

As for those saying Azure growth is weak, it's like the semiconductor industry — don't forget what the macro environment looks like. Global SaaS is sluggish; Google Cloud, on a low base, only grew 28%, and AWS is still unknown — AWS year-over-year growth was only 11% in April.

Our previous view on Microsoft has always been: the biggest watch item is to what extent Microsoft can commercialize these AI technologies, and what degree of synergy they can generate with the Azure/Office/Windows three engines.

In the near term, the market may focus more on AI's incremental contribution to Office 365 Commercial, whose margin is far higher than Azure's. Of course, I also look forward to Azure revenue overtaking AWS sooner rather than later.

*All segment revenue figures above are estimates.