Our early-2025 review found cloud AI revenue surging, non-AI demand recovering faster than expected, and compute capacity still in short supply.

The divide among the three largest clouds persisted this quarter: AWS and GCP remained the AI winners, while Azure continued to lag. In the agentic AI era, cloud providers' in-house data center CPUs are becoming as important as their custom AI accelerators. Oracle and the neoclouds still face questions about debt and leverage and need simultaneous capacity and revenue ramps in the second half to ease investor concerns. Meanwhile, the more accessible 'AWS for everyone' is beginning to capture the AI-native cloud opportunity.

1

Amazon AWS

Global Cloud Leader

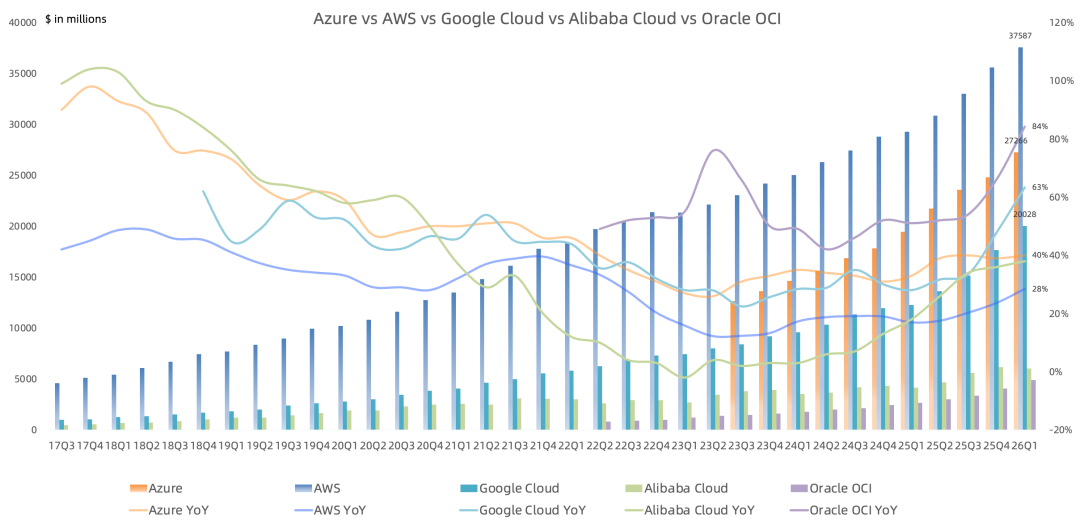

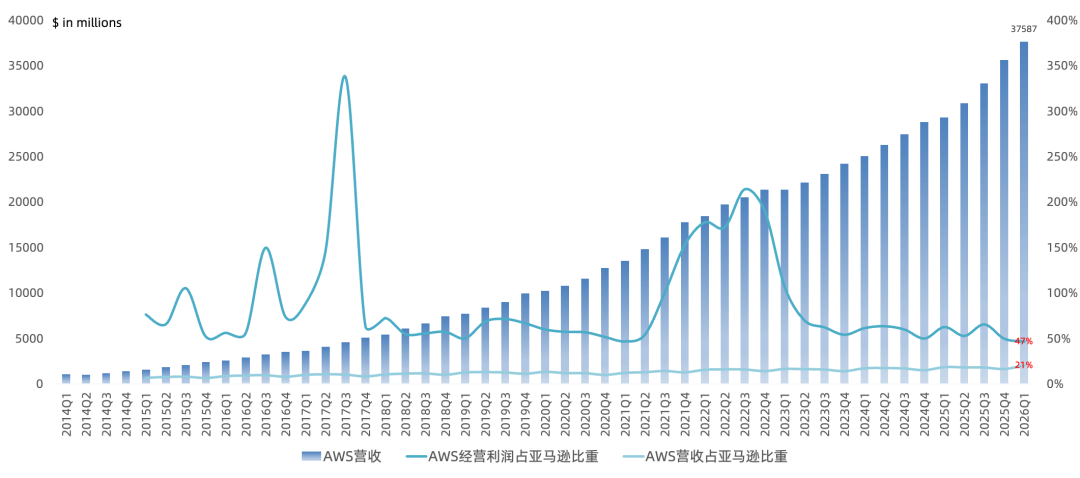

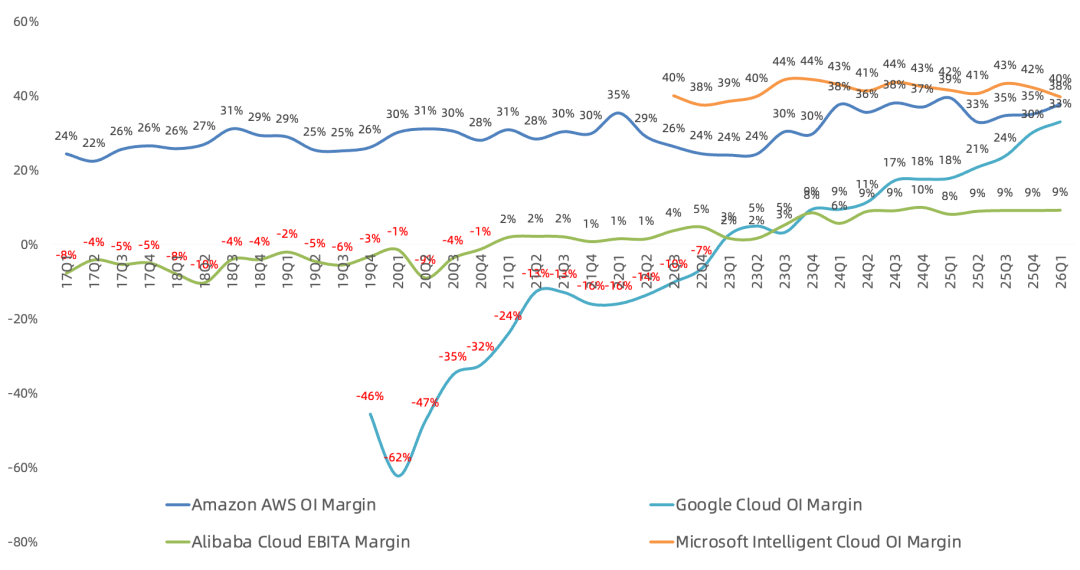

AWS Q1 revenue reached $37.6B, up 28% year over year and 6% sequentially. Growth accelerated four percentage points from the prior quarter to its fastest pace in 15 quarters. Operating income rose 23% to $14.2B, while operating margin declined one point to 38%.

AWS represented 21% of Amazon's revenue and 47% of operating income. Its AI revenue run rate now exceeds $15B annually. Backlog reached $364B, excluding the recently announced $100B Anthropic agreement, up 93% year over year and 49% sequentially.

Trainium and Graviton together now exceed a $20B revenue run rate, with triple-digit year-over-year growth and 40% sequential growth. Including internal chips sold through AWS and to third parties, the annualized run rate could reach $50B this year. Anthropic and OpenAI, two leading frontier laboratories, have made very large, multi-year, multi-gigawatt training commitments, creating more than $225B of committed Trainium revenue. Trainium 2 and 3 are effectively sold out. Trainium 4 is still about 18 months from broad availability, but a large portion is already reserved. On the CPU side, Meta has committed to tens of millions of Graviton cores, and 98% of AWS's 1,000 largest EC2 customers use Graviton. AWS also continues to work closely with NVIDIA and purchase its products at scale. Management expects Trainium to save tens of billions of dollars in annual capex and provide several points of operating-margin advantage over inference performed on third-party chips. AWS may begin selling complete racks over the next several years, while current demand can absorb essentially all available production. The company has managed memory supply constraints well, and higher memory prices are creating an additional incentive for companies with on-premises infrastructure to migrate to the cloud.

Bedrock now has more than 125,000 customers. Customer spending increased 170% sequentially, and tokens processed in Q1 exceeded the total from all prior years combined. The number of developers using Amazon Q more than doubled sequentially, while enterprise usage grew nearly tenfold. AWS will also make every OpenAI model available through Bedrock.

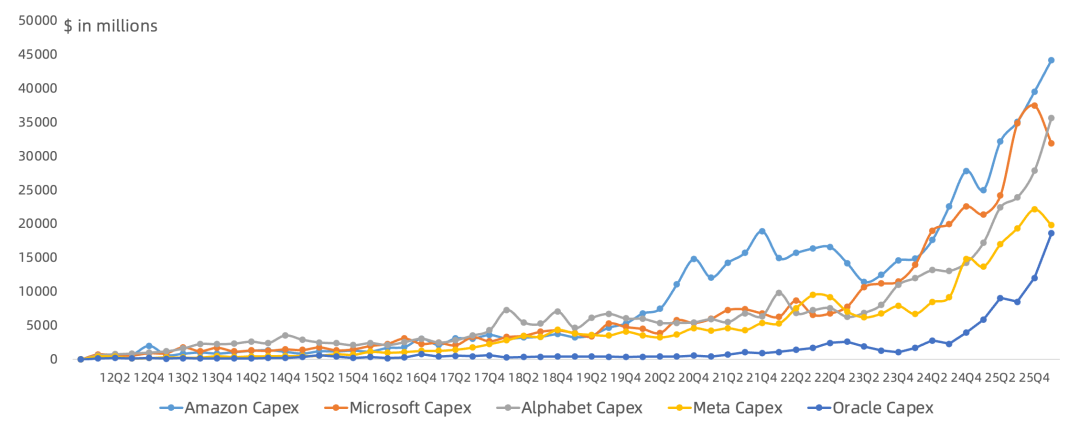

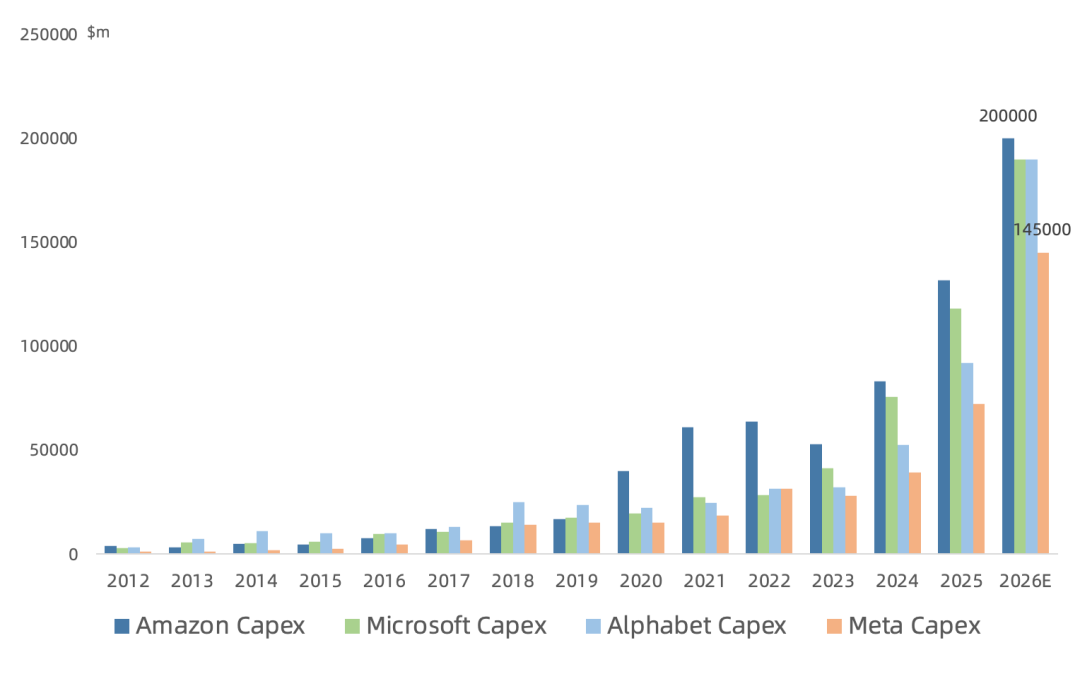

Amazon invested $39.5B of capex in Q1, mostly in AI, and maintained its $200B 2026 capex outlook. Faster AWS growth requires more near-term spending because cash must be paid for land, power, buildings, chips, servers, and networking equipment six to 24 months before customers can be billed, depending on the component. Management reiterated its ambition for AWS annual revenue to reach $300B within a decade, roughly double the current level.

2

Microsoft Azure

Second-Largest Global Cloud

Azure Q1 revenue was approximately $27.3B, up 40% year over year. Growth accelerated by only one percentage point sequentially, the smallest improvement among the three global cloud leaders.

Microsoft's Intelligent Cloud segment, which includes Server, Azure, and Enterprise Services, generated $34.7B of revenue, up 30% year over year. Gross margin fell 5.1 percentage points to 56.4%, primarily because of depreciation. Operating income rose 24% to $13.8B and operating margin reached 40%, still the highest among the three largest clouds. Intelligent Cloud contributed 42% of Microsoft revenue but only 36% of operating income, making it a relative drag on profitability.

Consumption of both AI and non-AI Azure services continued to grow, while supply is expected to remain constrained throughout the year. Azure growth should accelerate modestly in the second half of calendar 2026. AI ARR exceeded $37B, up 123% year over year, including revenue from leading model developers on Azure and Microsoft's first-party AI applications. Microsoft added 1 GW of data center capacity this quarter. Since the beginning of the year, the time from GPU arrival to deployment has fallen nearly 20% at several of its largest facilities. The Fairwater data center in Wisconsin came online six weeks ahead of schedule, allowing revenue recognition to begin earlier.

Microsoft's in-house Cobalt server CPU is now deployed in nearly half of its data center regions. As the company's largest customers expand their AI deployments, more are selecting Cobalt, prompting Microsoft to increase supply substantially.

More than 10,000 customers have used multiple models on Microsoft Foundry, including 5,000 using open-source models. The number of customers using Anthropic and OpenAI models tripled sequentially. More than 300 customers are expected to process over one trillion tokens on Foundry this year, 30% more than last quarter's estimate. Microsoft continues to develop its in-house MAI models while also innovating on top of OpenAI IP. In data and analytics, Fabric has more than 35,000 paid customers, up 60% year over year, while data stored in Fabric OneLake has nearly quadrupled. More than 15,000 customers use both Foundry and Fabric, also up 60%. GitHub Copilot is used by 140,000 enterprise organizations, with enterprise subscribers nearly tripling year over year. GitHub Copilot is now moving toward usage-based pricing.

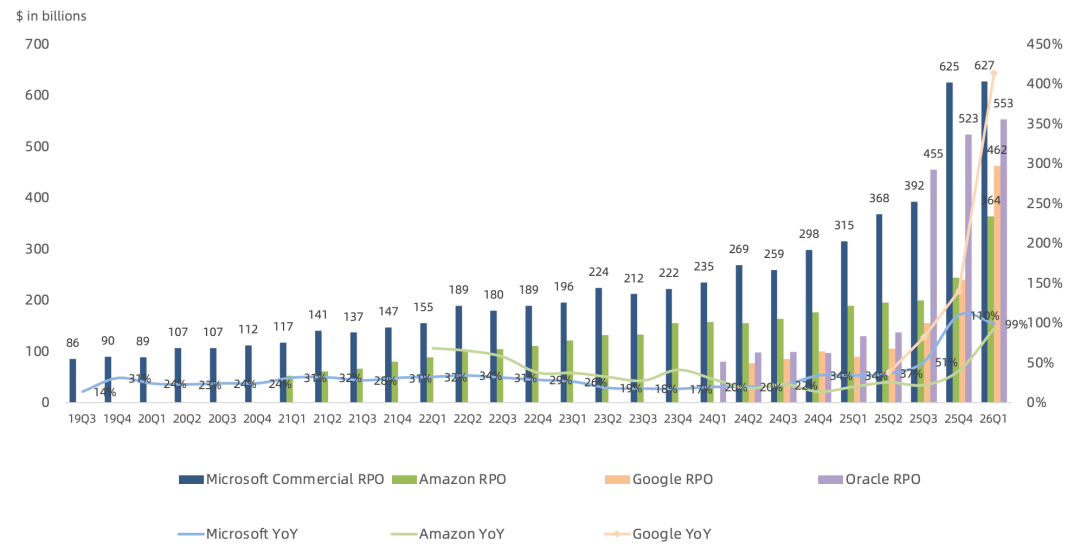

Commercial RPO reached $627B, up 99% year over year. Excluding OpenAI, RPO grew 26%, driven primarily by Anthropic, with a weighted average duration of about 2.5 years. Azure revenue is expected to grow 39%-40% next quarter. Microsoft invested $31.9B of capex this quarter, up 49%, with two-thirds allocated to short-lived assets, mainly GPUs and CPUs. Next-quarter capex should exceed $40B as higher memory prices raise infrastructure costs. Calendar 2026 capex is expected to reach $190B, including $25B attributable to memory and other chip price inflation.

3

Google Cloud

Third-Largest Global Cloud

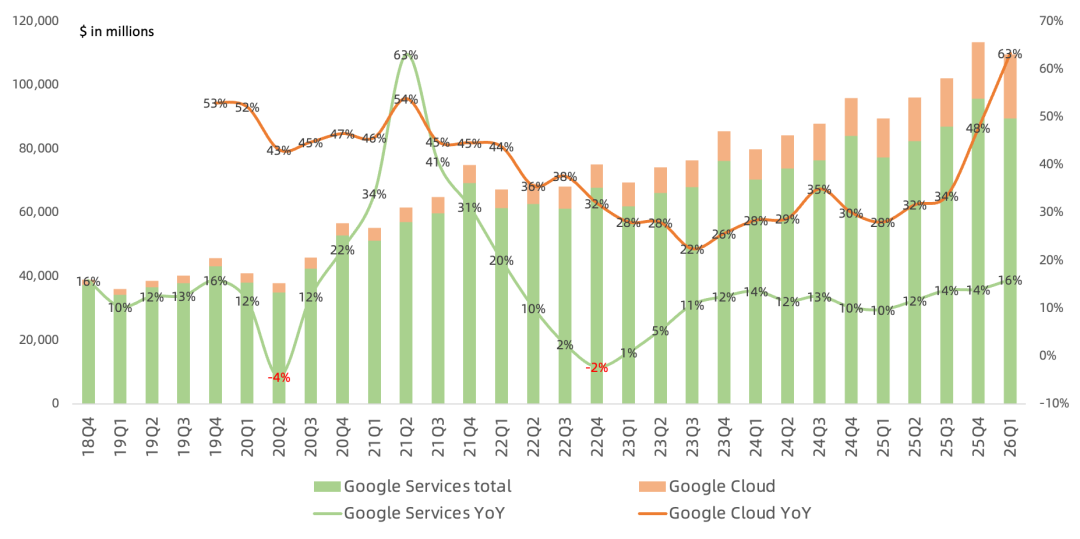

Google Cloud Q1 revenue reached $20B, up 63% year over year. Growth accelerated 16 percentage points sequentially and remained the fastest among the three global cloud leaders. Operating income reached $6.6B, while operating margin expanded 15 points to 33%, approaching AWS.

Google Cloud's five core businesses are AI infrastructure, the Vertex enterprise AI platform, the BigQuery data platform, AI cybersecurity, and the Workspace productivity suite. GCP revenue again grew faster than Cloud overall. AI solutions contributed the most to growth, driven by strong demand for leading models such as Gemini 3, while AI infrastructure also expanded rapidly as TPU and GPU deployments continued. Workspace delivered another quarter of strong double-digit growth as both seat count and average revenue per seat increased. Gemini app monetization is currently focused on effective advertising formats within AI Mode. The number of $100M-$1B contracts doubled year over year, and Google signed several deals above $1B. Customer consumption exceeded initial commitments by 45%, accelerating from last quarter. Cloud backlog nearly doubled sequentially to $462B, with slightly more than half expected to convert to revenue over the next 24 months. Gemini Enterprise paid monthly active users grew 40% sequentially, and Google's first-party models now process more than 16B tokens per minute, up from 10B last quarter.

Google's custom TPUs, Axion CPUs, and the latest NVIDIA GPUs continue to provide one of the industry's broadest compute portfolios. NVIDIA GPUs remain a core part of Google Cloud's AI accelerator lineup. In addition to available Blackwell and Hopper instances, Google Cloud expects to be among the first providers of Vera Rubin NVL72. As TPU demand grows among AI laboratories, capital-markets firms, and high-performance computing users, Google will begin delivering TPU hardware to selected customers for deployment in their own data centers, expanding the addressable market beyond cloud services.

Google invested $35.7B of capex in Q1, with roughly 60% allocated to servers and 40% to data centers and networking equipment. The 2026 capex outlook was raised to $180B-$190B, and 2027 spending is expected to increase materially again. Google will begin recognizing a small amount of revenue from on-premises TPU hardware agreements later this year, with the vast majority arriving in 2027. Hardware sales will create quarterly revenue volatility based on delivery timing.

4

Alibaba Cloud

China's Cloud Leader

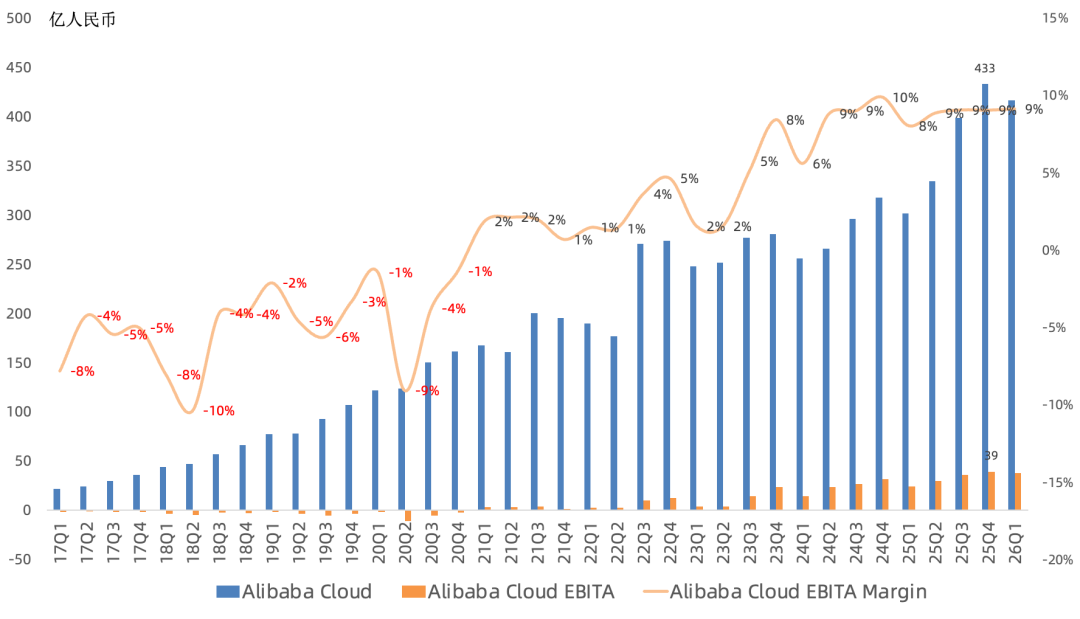

Alibaba Cloud Q1 revenue reached RMB 41.6B, or $6.04B, up 38% year over year with growth accelerating two percentage points sequentially. Excluding intercompany consolidation revenue, growth was 40%, accelerating five points. The main weakness was a sequential revenue decline, something rarely seen among the three global cloud leaders. AI-related revenue has delivered triple-digit year-over-year growth for 11 consecutive quarters and reached RMB 9B. Alibaba aims for Model-as-a-Service revenue to surpass IaaS as its largest product category. Alibaba Cloud has deployed more than 100,000 Pingtouge PPU AI chips across over 30 customers, including autonomous-driving companies.

Q1 adjusted EBITA rose 57% to RMB 3.8B, or $550M. EBITA margin held at 9%, up 1.1 percentage points year over year. Capex was RMB 26.6B, or $3.9B, compared with RMB 29B last quarter.

5

Oracle Cloud

Global Cloud Challenger

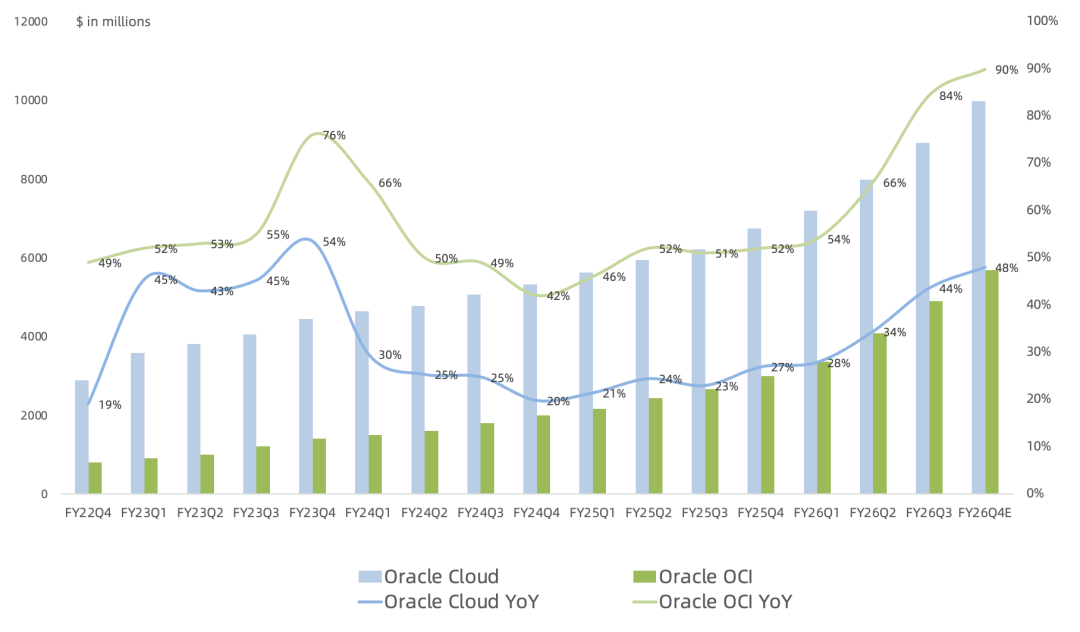

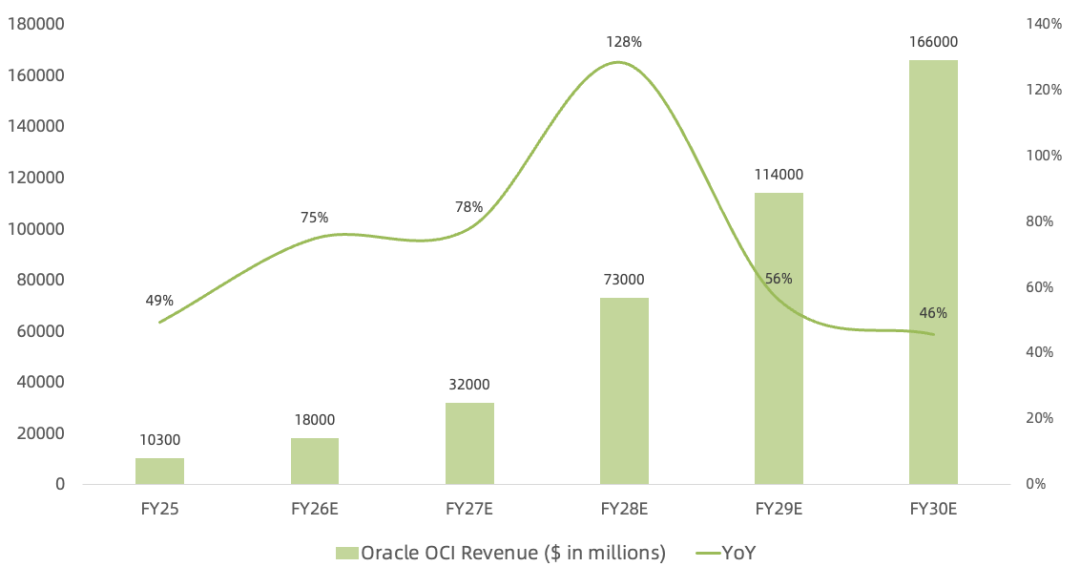

Oracle Cloud Q1, reported earlier as FY26Q3, generated $8.9B of revenue, up 44% year over year with growth accelerating ten percentage points sequentially. OCI infrastructure revenue reached $4.9B, up 84%, with growth accelerating 18 points. Management previously projected IaaS revenue of $32B, $73B, $114B, and $166B in FY27 through FY30, with OCI gross margin between 30% and 40%. This quarter OCI gross margin reached 32%, AI-related OCI revenue grew 243%, and Oracle delivered 400 MW of capacity.

Oracle maintained its $50B FY26 capex guidance but did not provide a specific FY27 figure. Management said Oracle's infrastructure expansion is becoming less dependent on its own capital. More than $29B of contracts involve customer-supplied hardware or customer prepayments, allowing Oracle to expand without generating negative cash flow.

MultiCloud Database revenue through Azure, GCP, and AWS grew 531% year over year. The service is live in 33 Azure regions, 14 Google Cloud regions, and eight AWS regions, with 22 additional regions planned next quarter. Cloud Database revenue grew 35%, while RPO exceeded $553B, up 325% year over year and $29B sequentially.

Oracle Cloud revenue is guided to grow 44%-48% in FY26Q4. Oracle maintained its $67B FY26 total revenue outlook and raised FY27 guidance to $90B from $85B. Oracle now owns 15% of TikTok US and holds one board seat. In February, it announced plans to raise up to $50B through debt and equity. Oracle has raised $30B so far and does not expect to issue bonds beyond the announced amount during calendar 2026.

6

CoreWeave & Nebius

Two AI Neocloud Leaders

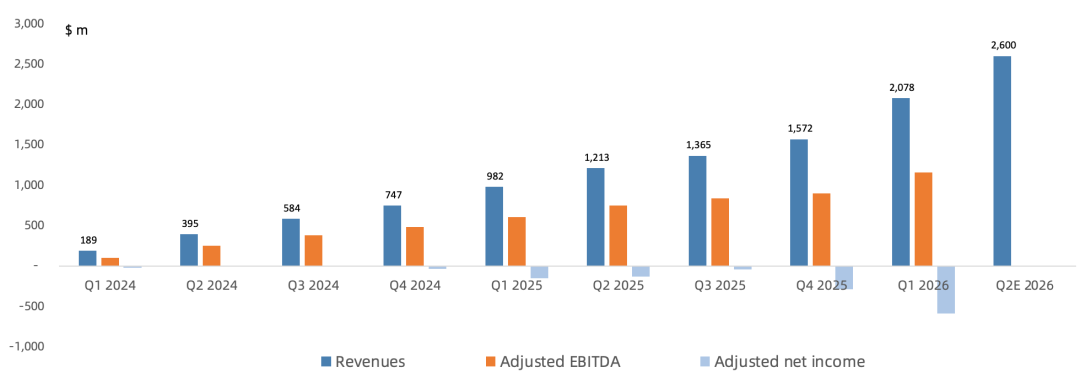

CoreWeave Q1 revenue reached $2.08B, up 112% year over year. Gross margin after depreciation was only 4.3%, down 12 percentage points, while adjusted operating margin was 1%. Adjusted EBITDA rose 91% to $1.16B, but EBITDA margin declined six points to 56%. Q1 capex reached $6.8B, far above revenue. Heavy debt and depreciation therefore continue to raise questions about long-term profitability.

CoreWeave backlog reached $99.4B, up 284% year over year and $38.7B sequentially. Of that amount, $35.8B is expected to convert to revenue within 24 months, up 208%. New verticals have already grown above $1B. In financial services, technology-driven firms are expanding core machine-learning workloads on CoreWeave, producing nearly $10B of backlog. Jane Street added $6B of capacity this quarter, while Hudson River Trading joined as a new customer. Physical AI and spatial computing have also contributed more than $1B of backlog. CoreWeave operates 49 data centers worldwide with about 1 GW of active power, up 250 MW sequentially, and 3.5 GW of contracted power, up 400 MW. Active power should more than double to above 1.7 GW by the end of 2026, with a target above 8 GW by 2030. Demand is accelerating across the portfolio: average pricing for A100, H100, H200, and L40S increased sequentially, 2026 capacity remains effectively sold out, and allocations for capacity coming online next year are extending the trend into 2027. Inference now accounts for well over half of deployed compute.

CoreWeave expects next-quarter revenue of $2.45B-$2.5B, with the high end up 114% year over year, and adjusted operating income of $30M-$90M. Management expects Q1 to mark the profit trough and a meaningful second-half ramp. The 2026 capex range is now $31B-$35B after raising the low end. Full-year revenue guidance remains $12B-$13B, implying roughly 140% growth at the midpoint, with adjusted operating income of $900M-$1.1B. Year-end 2026 ARR is expected to reach $18B-$19B after raising the low end, followed by more than $30B by the end of 2027. Management remains confident in a long-term 25% operating-margin target.

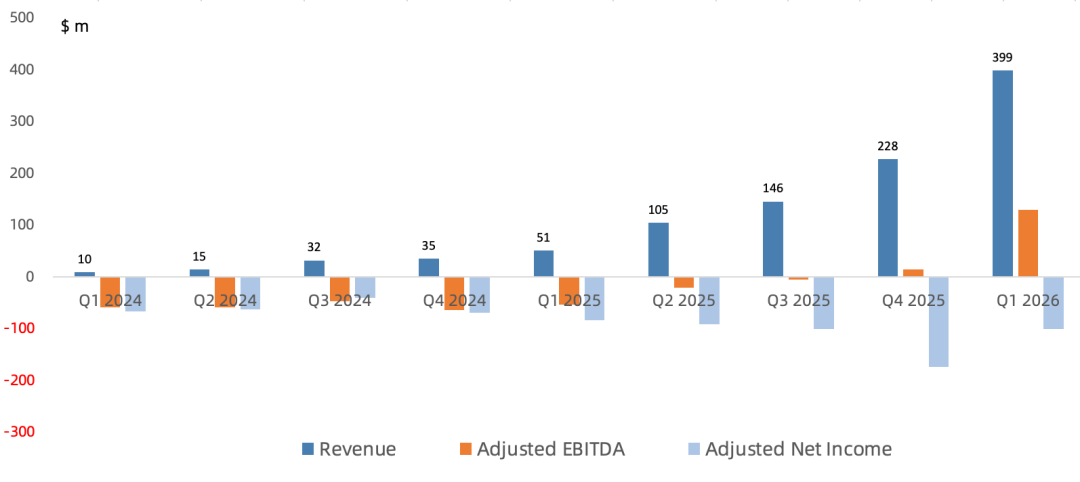

Nebius Q1 revenue reached $399M, up 684% year over year. Core AI cloud revenue was $390M, up more than 841% and representing nearly 98% of total revenue. Record pipeline generation increased 3.5 times sequentially, and multiple customers typically compete for every GPU that comes online. Gross margin after depreciation was 20.9%. Adjusted EBITDA reached $130M with a 33% margin, while Q1 capex surged to $2.47B.

Nebius acquired agentic AI search tool Tavily in February and added Eigen AI and Clarifai in May to strengthen inference optimization. NVIDIA ranked Eigen AI as the leading high-speed inference provider. Eigen optimizes at the model layer, while Clarifai works at the system layer, together strengthening Nebius's internal Token Factory product. Token Factory won Revolut and monday.com as customers this quarter. Nebius has signed more than 3.5 GW of power capacity and expects more than 4 GW of contracted power by the end of 2026, with 800 MW-1 GW active. Capacity is fully utilized and sold out. The company also secured a $27B Meta agreement, consisting of a five-year $12B contract beginning in 2027 plus a $15B option. Demand continues to exceed available capacity, supporting strong pricing for both older and newer GPUs. Prices increased again this quarter, every chip category remains sold out, and customers including hyperscalers are prepaying to secure future capacity.

Nebius raised its 2026 capex outlook to $20B-$25B, reflecting investment in 2027 capacity scheduled to come online early next year. That capacity should begin contributing revenue in the first half of 2027 and is already backed by customers and commitments, including Meta. The company expects 2026 revenue of $3B-$3.4B, a 40% adjusted EBITDA margin, and year-end ARR of $7B-$9B. Beginning in Q1 2026, Nebius extended the depreciable life of servers and networking equipment from four years to five.

7

DigitalOcean

AWS for Everyone

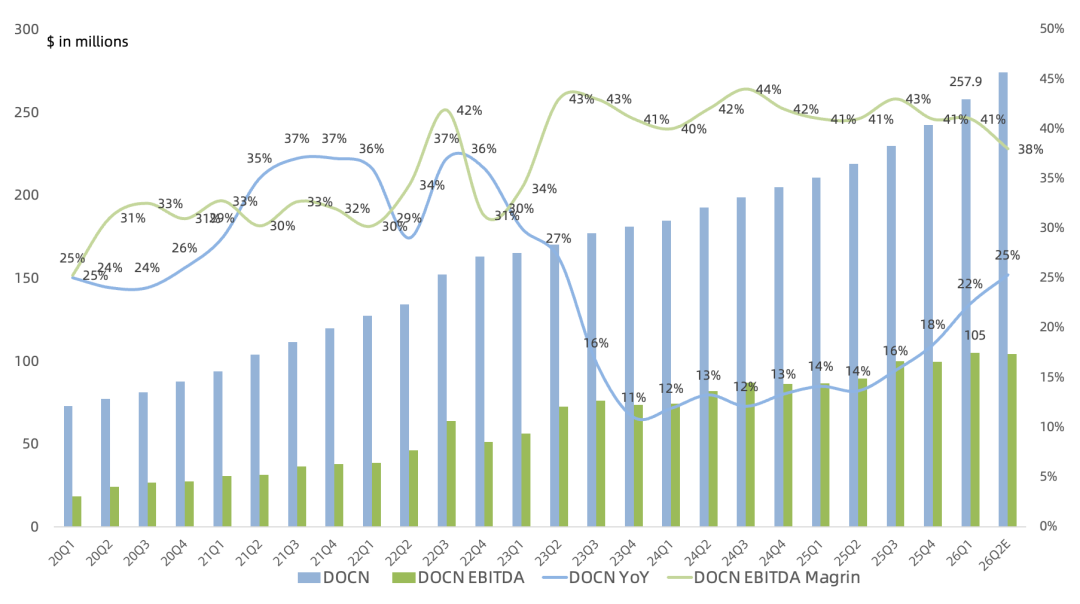

DigitalOcean Q1 revenue reached $260M, up 22% year over year. ARR reached $1.03B, also up 22%, including $170M of AI ARR, up 221% and more than doubling for a seventh consecutive quarter. Gross margin declined five percentage points to 56%, while operating margin fell four points to 14%.

Q1 EBITDA rose 22% to $110M, while EBITDA margin held at 41%. RPO increased to $243M from $134M last quarter.

DigitalOcean primarily serves small and medium-sized businesses, making it sensitive to macroeconomic cycles. Its top 25 customers contribute only 10% of revenue. I previously argued that DigitalOcean moved too slowly as AI-native competitors such as CoreWeave and Nebius emerged. H100 instances did not become available to all customers until October 1 last year, and the company's first AI product, GenAI Platform, launched only in early November. DigitalOcean now offers H100, H200, B300, MI300X, MI325X, and MI350X instances.

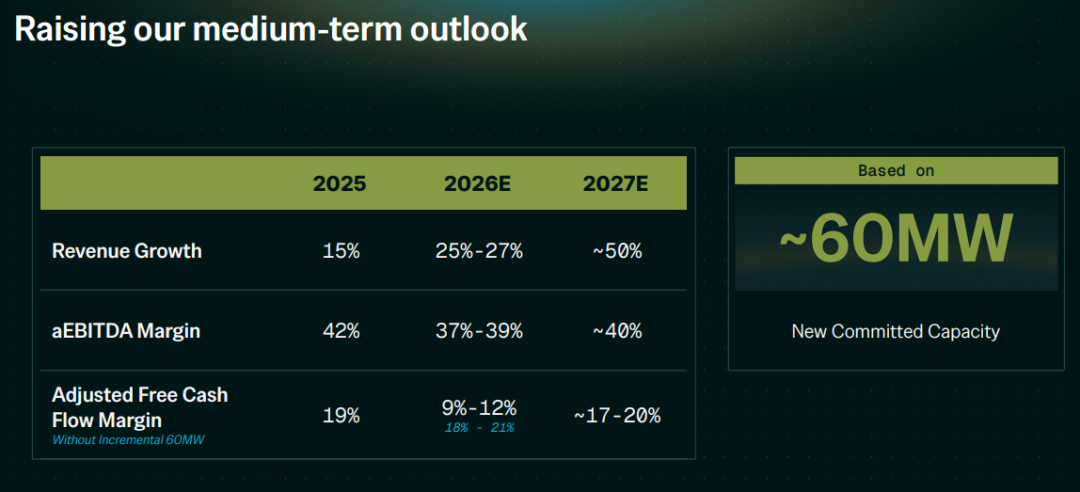

DigitalOcean currently carries less leverage than the leading neoclouds, but it is increasing capex and leverage to respond more quickly to AI demand. The company raised $888M through an equity offering this quarter, added a 60 MW data center construction target, and has secured 135 MW of total capacity. It raised its revenue growth outlook to 25%-27% for 2026 and 50% for 2027.

Conclusion

Cloud capex surged again this quarter. Combined Q1 capex for FAMG and Oracle exceeded $150.3B, up 81% year over year and still accelerating. As compute demand rises sharply, the upper end of 2026 capex guidance for the four FAMG companies reaches $725B, up 75%, ten percentage points faster than in 2025.

Cloud providers will continue concentrating more capex in GPU servers, even as the market treats that spending as overinvestment. Amazon repeatedly compares the current buildout with the early days of cloud computing. Today, cloud remains the clearest and highest-return use case for AI. One underappreciated dynamic is that as AI startups scale, their demand for traditional cloud services also increases.