In the prior article "Global Cloud Giants Q4: AI Drives Growth, Capex Recovers," I noted that as cloud revenue growth rebounded, capex also began to recover. With Alibaba's belated report, the Q1 scorecards for all five global cloud giants are now in: AI has become a profit engine for cloud providers, while non-AI demand has returned to growth.

1

Amazon AWS

Global Cloud Leader

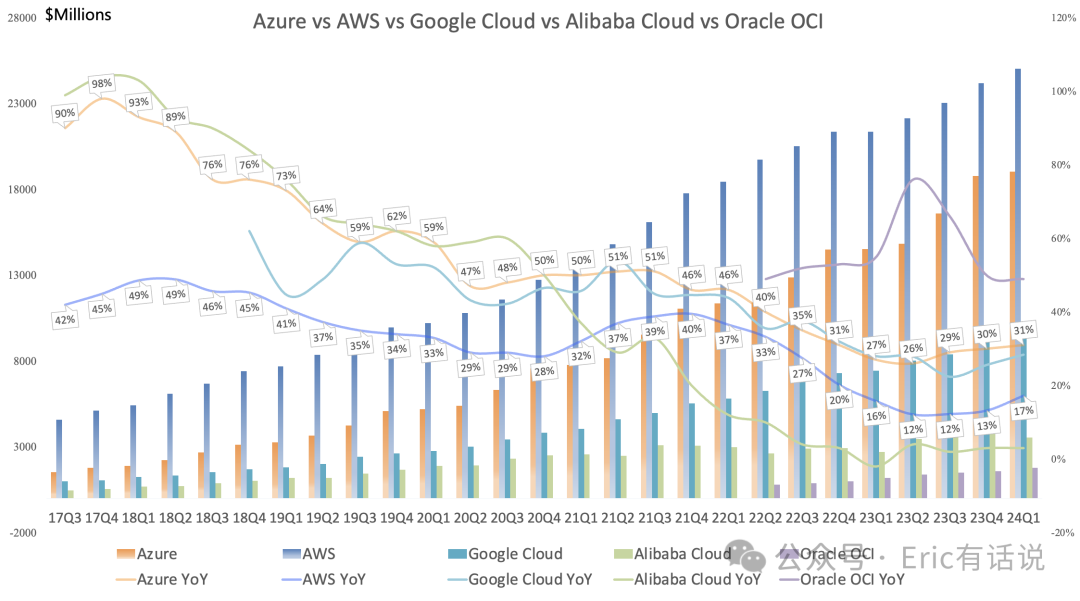

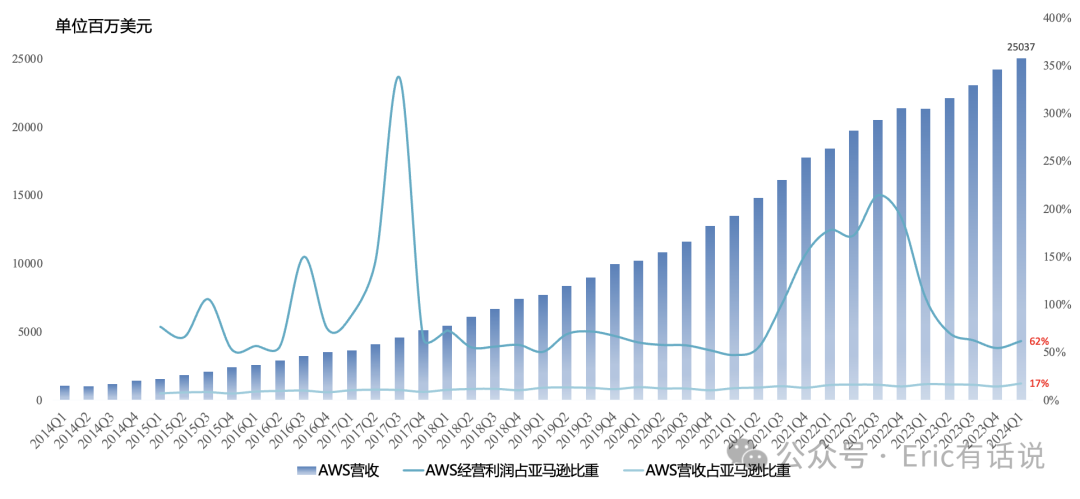

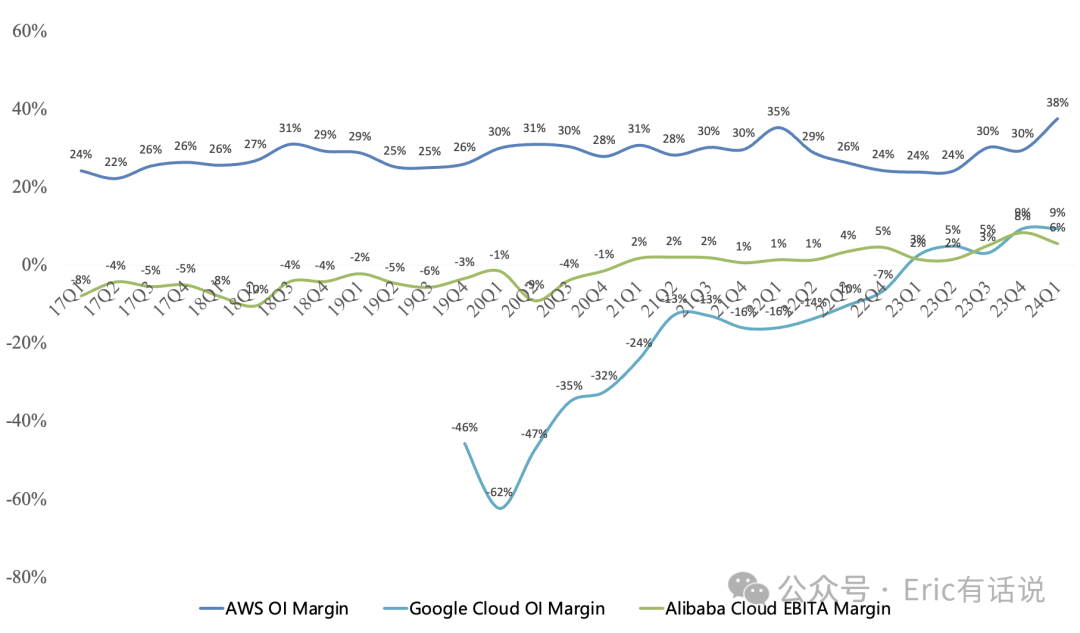

Q1 revenue was $25.037B, up 17% year over year, growth rate up 4 percentage points, up 3% sequentially; operating income was $9.421B, up 84% year over year, a record high for the third consecutive quarter; operating margin 38%, up 14 percentage points year over year, a record high.

AWS Q1 revenue accounted for 17% of Amazon's total revenue and contributed 62% of Amazon's operating income.

Since Q3 last year, enterprises of all sizes began optimizing cloud spend, slowing growth; that trend ended this quarter; both AI and non-AI growing; AWS annualized revenue >$100B; on AI, training and inference demand both strong, AWS AI annualized revenue already in the multi-billions; still early days for AI; AWS custom Trainium2 to debut H2 or early next year; SageMaker end-to-end service for AI developers in strong demand: Perplexity AI trained models 40% faster on SageMaker, Workday cut inference latency 80% on SageMaker; Bedrock now has >10,000 customers including adidas, NYSE, Pfizer, Ryanair, Toyota; Amazon Q broadly launched; 85% of global IT still not on cloud, company very bullish on AWS future; the better AWS performs, the more capex it will invest.

2

Microsoft Azure

Second-Largest Global Cloud

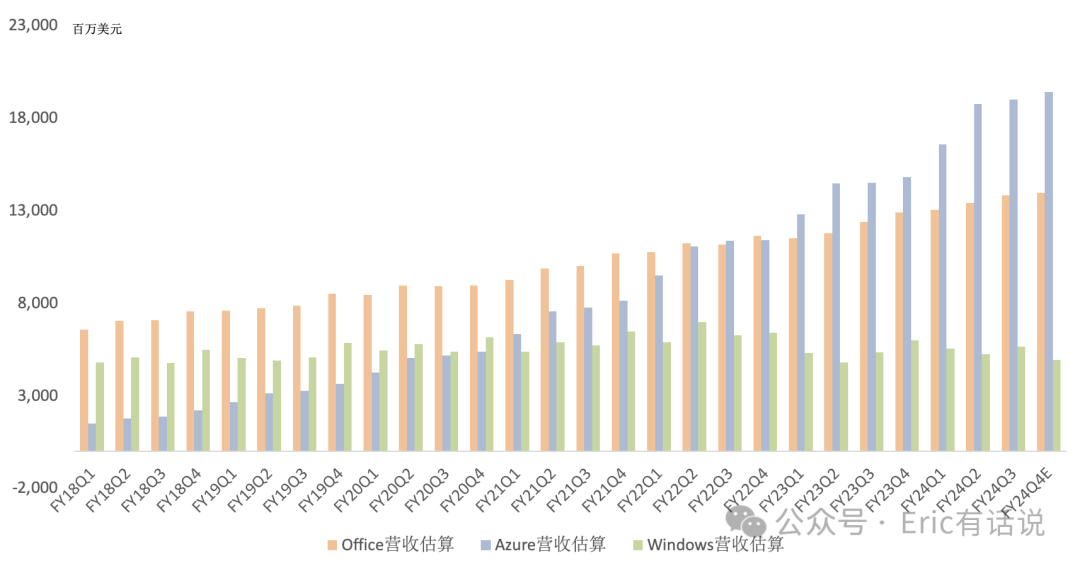

Q1 revenue was $19.033B, up 31% year over year, growth rate up 1 percentage point, continuing to lead the big three clouds, up 1% sequentially.

Intelligent Cloud (Server + Azure + Enterprise Services) operating income was $12.513B, up 32% year over year, a record high for the fifth consecutive quarter; operating margin 47%.

Intelligent Cloud revenue accounted for 43% of Microsoft's total revenue and contributed 45% of Microsoft's operating income.

Azure share continues to rise; Azure AI customer count and average spend growing; >65% of Fortune 500 use Azure OpenAI Service; seeing more accelerated migration to Azure; Azure Arc now has 33,000 customers, doubled year over year; landed Cloud Software Group and Coca-Cola multi-year, multi-billion-dollar deals this quarter; Azure $100M+ deals up 80%+ year over year, $1B+ deals doubled year over year; AI contributed 7% of Azure growth (~$1B), constrained by supply, otherwise higher; Azure non-AI demand recovering.

3

Google Cloud

Third-Largest Global Cloud

Q1 revenue was $9.574B, up 28% year over year, growth rate up 2 percentage points. Operating income $900M, operating margin 9%, a record high.

Over 60% of funded AI startups, nearly 90% of AI unicorns are Google Cloud customers; Google offers 130+ AI models, including proprietary, open-source, and third-party; AI monetization path clear: ads + cloud + subscriptions; this quarter Google Cloud growth driven by GCP, AI contributing to growth; Workspace revenue up year over year, driven by ARPU growth; GCP to continue investing while maintaining profitability.

Google Cloud revenue growth is no longer a question. Management guides for YouTube + Cloud revenue run rate >$100B by year-end, implying Q4 Google Cloud revenue around $15B. In the previous article I noted my biggest hope for Google Cloud this year is whether margins can push toward 20%.

4

Alibaba Cloud

China's Cloud Leader

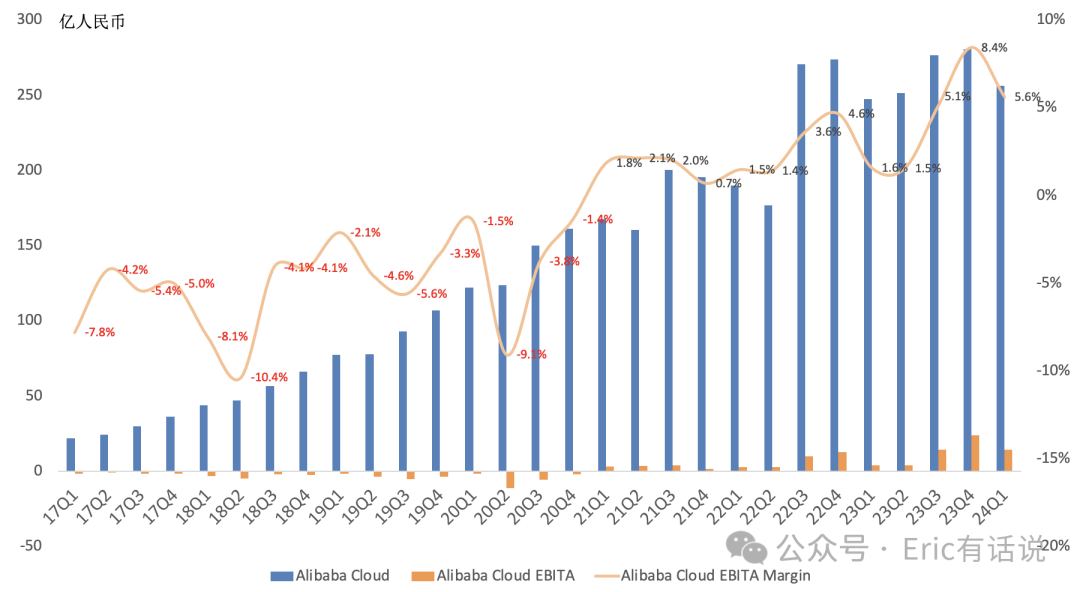

Q1 revenue was RMB 25.595B ($3.545B), up 3% year over year; excluding internal consolidation, revenue down slightly again year over year; but core public cloud including Elastic Compute, Database, AI grew double digits year over year; AI-related revenue up triple digits year over year for consecutive quarters, customers mainly model companies, internet, finance, and auto.

Q1 EBITA profit was RMB 1.432B, EBITA margin 5.6%, profitable for the 13th consecutive quarter.

5

Oracle Cloud

Global cloud #4

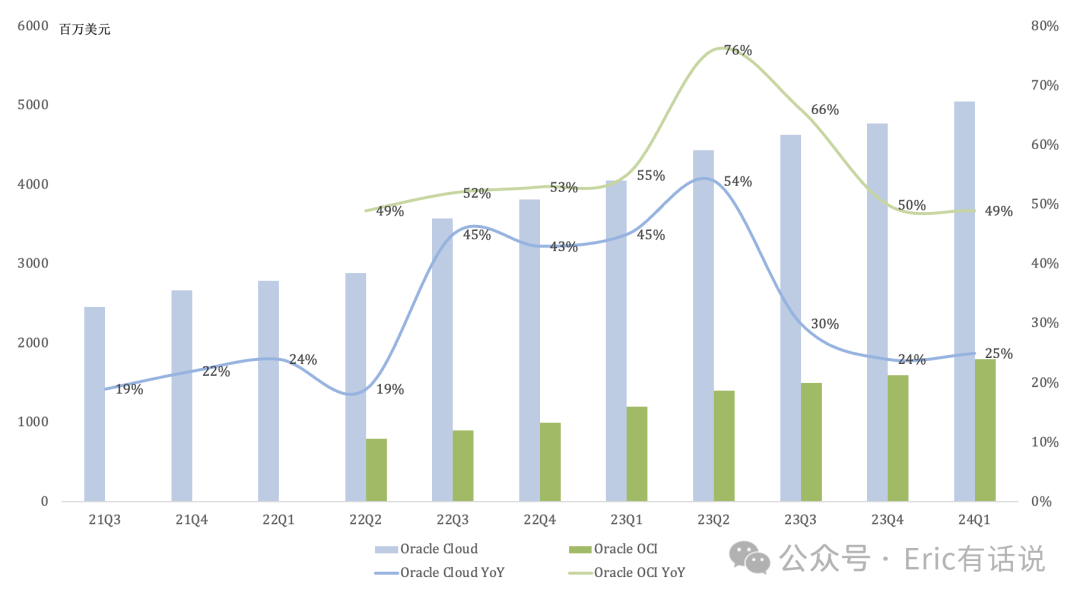

Q1 revenue was $5.054B, up 25% year over year, growth rate up 1 percentage point; ex-Cerner revenue was $4.4B, up 26% year over year; OCI (IaaS) revenue was $1.8B, up 49% year over year; SaaS revenue was $3.3B, up 14% year over year.

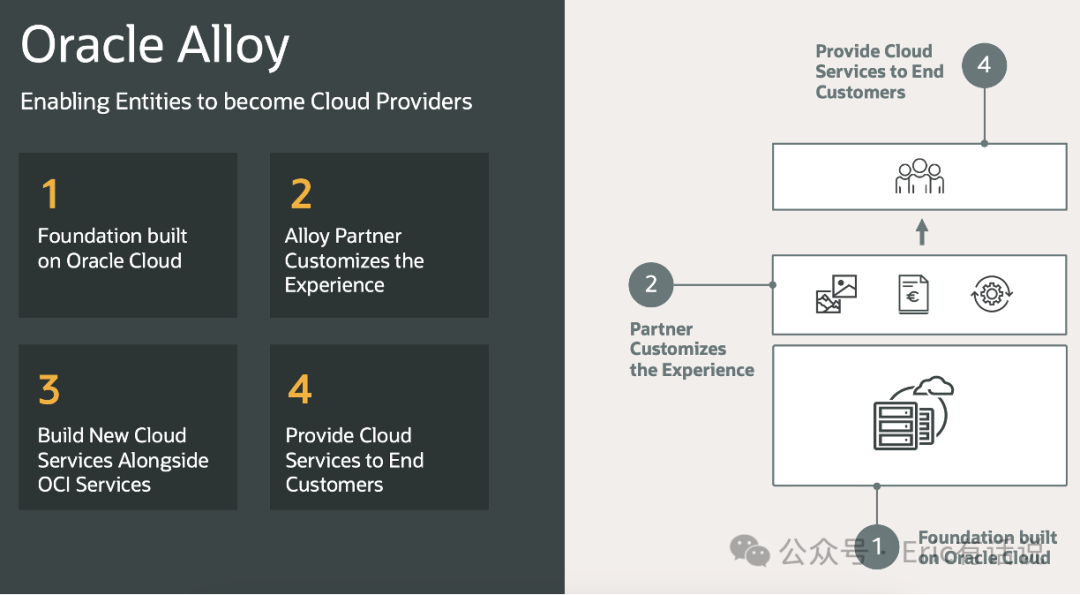

Cloud revenue exceeded license revenue for the first time this quarter; Gen2 Infra Cloud revenue up 52% year over year, annualized $6.7B; OCI consumption revenue up 63% year over year; Cloud Database up 34% year over year, annualized $1.9B, becoming another major growth driver; RPO $80B, growing faster than revenue due to supply constraints; 40 new AI customer orders >$1B; 20 data centers now interconnected with Azure/Microsoft, 3 ordered this quarter; Oracle Alloy progressing well in Japan.

6

DigitalOcean

AWS for Everyone

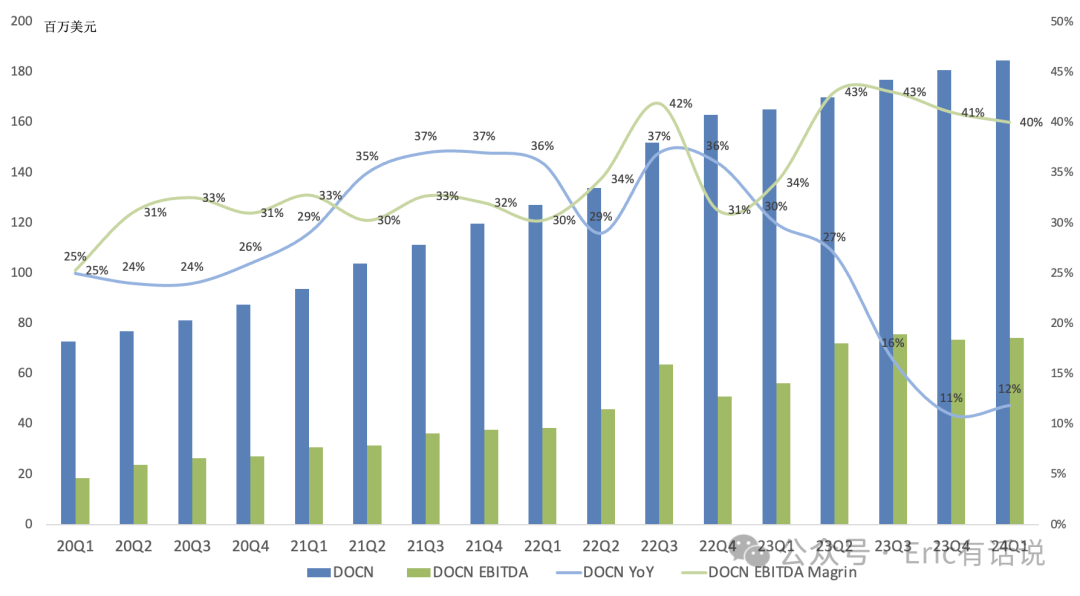

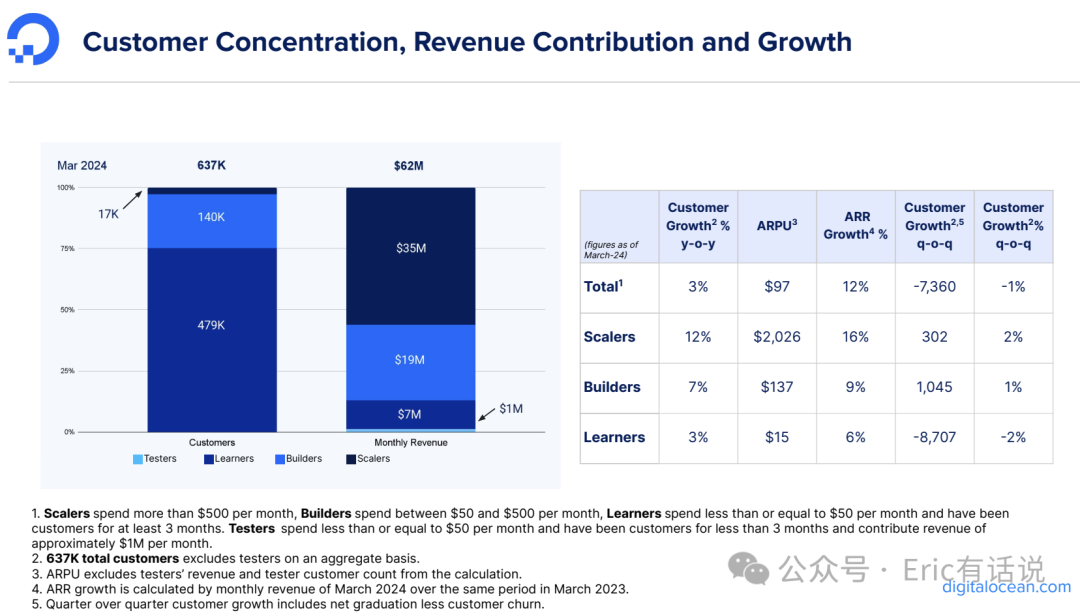

Q1 revenue was $185M, up 12% year over year; ARR $749M, up 12% year over year; gross margin 61%, up 5 percentage points year over year; operating margin 6%; Monthly ARPU $95.13, up 8% year over year; guided Q1 revenue up 11% year over year.

Q1 EBITDA profit was $74.3M, up 32% year over year; EBITDA margin 40%; Net Dollar Retention Rate rebounded slightly to 97% but remains below 100%.

DigitalOcean's clear trait is its SMB customer base, making it highly sensitive to macro cycles; while ARPU keeps rising, customer count has hit a growth ceiling. Previously noted its core problem is lack of growth, which is fatal for a small-scale player. The rise of AI clouds like CoreWeave also impacts traditional small cloud vendors. But if the cloud industry overall recovers, will DigitalOcean see growth return?

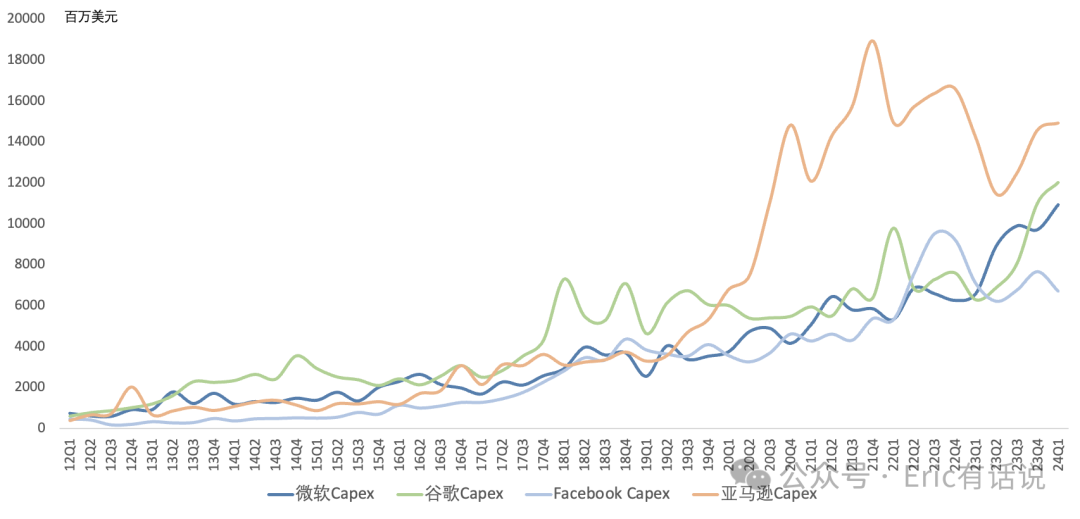

Conclusion

Cloud Capex surged again this quarter; FAMG Q1 Capex total up 31% year over year, a record high for the second consecutive quarter, up 4% sequentially; as AI's contribution to cloud revenue growth exceeds expectations, future cloud Capex concentration on GPU servers will continue to rise.